Asia Pacific Microsurgery Robot Market Research Report – Segmented By Application (Oncology surgery, Ophthalmology surgery, Obstetrics and gynecology surgery, Micro anastomosis, Reconstructive surgery, ENT surgery), End-User, Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2024 to 2033

Asia Pacific Microsurgery Robot Market Insights

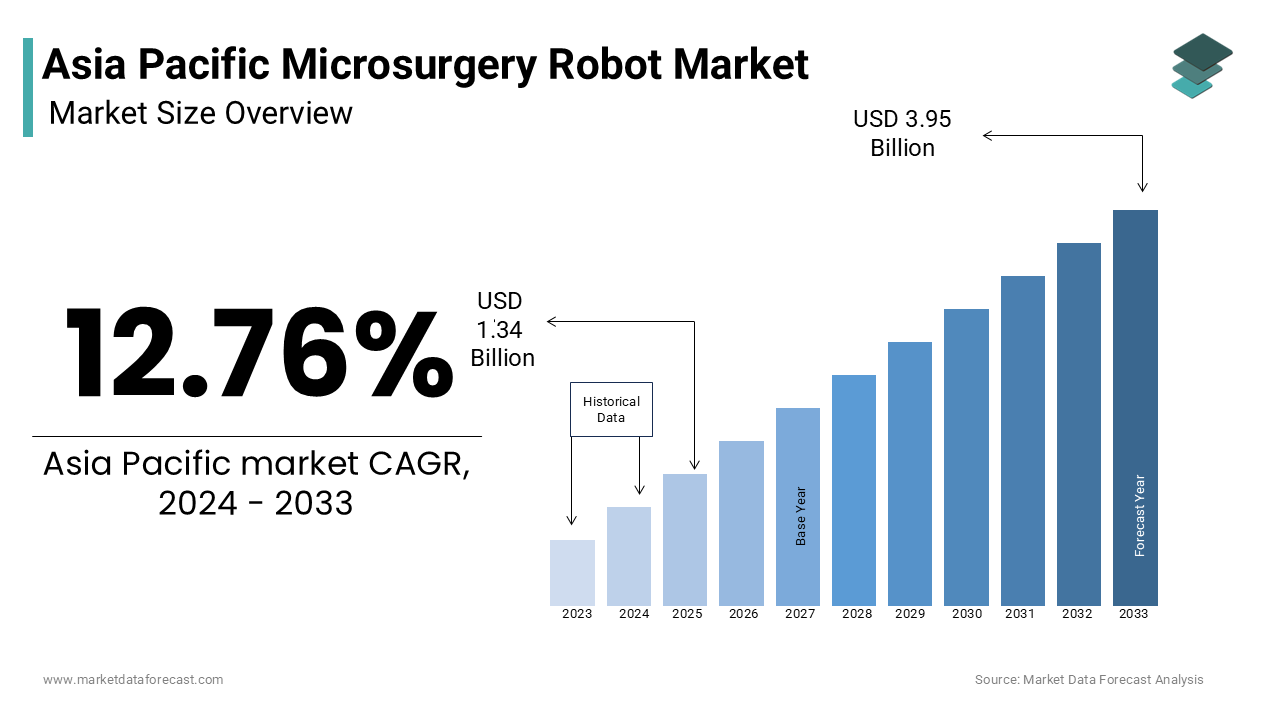

In 2024, the Asia Pacific Microsurgery Robot Market was valued at USD 1.34 billion and is forecasted to grow to USD 3.95 billion by 2033, at a CAGR of 12.76%.

The microsurgery robot systems are designed to enhance surgical accuracy, reduce human error, and improve patient outcomes by enabling sub-millimeter-level precision that surpasses manual capabilities. The demand for microsurgery robots in the Asia Pacific is being driven by a growing burden of chronic diseases, an aging population, and increasing healthcare investments. According to the World Health Organization, the proportion of the population aged 60 and above in the Asia Pacific is expected to double by 2050, significantly increasing the prevalence of age-related conditions requiring complex surgical interventions. Additionally, as per the Asia Pacific Economic Cooperation (APEC), healthcare expenditure in the region has been rising steadily, particularly in high-income countries like Japan and South Korea, where advanced surgical technologies are more readily adopted.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases Requiring Precision Surgery

The increasing prevalence of chronic diseases that necessitate highly precise surgical interventions is accelerating the growth of the Asia Pacific microsurgery robot market. Conditions such as diabetic retinopathy, Parkinson’s disease, and various types of cancer are on the rise across the region, necessitating the use of advanced robotic systems capable of performing complex microsurgeries with minimal invasiveness. According to the World Health Organization, non-communicable diseases (NCDs) account for over 60% of all deaths in the Asia Pacific region with cardiovascular diseases, cancer, and diabetes being the leading contributors. In countries like China and India, the growing incidence of diabetes has led to a surge in related complications such as retinopathy and neuropathy, which often require microsurgical interventions. The ability of microsurgery robots to perform intricate procedures with high precision makes them an essential tool in managing these complex conditions.

Expansion of Robotic Surgery Infrastructure in Healthcare Facilities

The rapid expansion of robotic surgery infrastructure within hospitals and specialty clinics is additionally propel the growth of the Asia Pacific microsurgery robot market. Over the past decade, there has been a significant increase in the installation of robotic surgical systems, particularly in countries with advanced healthcare systems such as South Korea, Australia, and Singapore. According to the Asia Pacific Economic Cooperation (APEC), the number of robotic surgical systems installed in hospitals across the region has more than tripled since 2015. In South Korea, the Ministry of Health and Welfare has been actively promoting the adoption of robotic-assisted surgeries through policy incentives and training programs for surgeons. The Royal Australasian College of Surgeons has emphasized the importance of robotic surgery in improving clinical outcomes, which is leading to increased procurement of microsurgery robots by major hospitals. In emerging markets like India, private healthcare providers are also investing in robotic platforms to attract medical tourists seeking high-quality surgical care.

MARKET RESTRAINTS

High Acquisition and Maintenance Costs of Microsurgery Robots

The high acquisition and maintenance costs associated with these advanced surgical systems is restricting the growth of the Asia Pacific microsurgery robot market. According to the World Bank, healthcare spending per capita in countries such as Indonesia, the Philippines, and Vietnam remains significantly lower than in developed economies, which is limiting the ability of hospitals to invest in high-cost medical robotics. In addition to the initial purchase cost, the ongoing expenses related to maintenance, software upgrades, and specialized training for surgical teams further add to the financial burden. This economic barrier restricts widespread adoption, particularly in rural and semi-urban hospitals where budget constraints are more pronounced. Even in countries like India and Thailand, where private hospitals are increasingly adopting robotic systems, affordability remains a key challenge for public healthcare institutions. The high cost of microsurgery robots continues to be a significant impediment to their broader integration across the Asia Pacific region.

Regulatory and Reimbursement Challenges Across the Region

The complex and inconsistent regulatory and reimbursement landscape across different countries is limiting the growth of the Asia Pacific microsurgery robot market. Each nation in the region has its own set of medical device regulations, which can delay market entry and increase compliance costs for manufacturers. According to the Asia Pacific Economic Cooperation (APEC), regulatory approval timelines in countries like India and Indonesia can take significantly longer than in more developed markets such as Japan and Australia, due to varying standards and documentation requirements.

In addition to regulatory hurdles, reimbursement policies for robotic-assisted surgeries remain fragmented. In countries like China and Malaysia, while there is growing acceptance of robotic surgery in private hospitals, public health insurance schemes often do not cover the full cost of robotic procedures by making them unaffordable for a large portion of the population. As per the Chinese National Healthcare Security Administration, only a limited number of robotic surgical procedures are included in the national reimbursement list, restricting patient access and hospital adoption.

MARKET OPPORTUNITIES

Increasing Adoption of Telemedicine and Remote Surgery Applications

The increasing adoption of telemedicine and remote surgery applications is setting up new opportunities for the growth of the Asia Pacific microsurgery robot market. The feasibility of performing remote microsurgical procedures is becoming a reality with advancements in 5G connectivity and digital health infrastructure. The National Institute of Information and Communications Technology has been conducting trials on remote robotic surgeries using ultra-low latency networks, which is aiming to bring high-precision surgical care to remote islands and underserved regions. These developments indicate a growing trend toward leveraging microsurgery robots in telemedicine applications by offering a transformative pathway for expanding surgical access across the Asia Pacific.

Expansion of Medical Tourism and Private Healthcare Infrastructure

The expansion of medical tourism and private healthcare infrastructure in countries like Thailand, India, and Singapore is additionally to fuel the growth of the Asia Pacific microsurgery robot market. These nations have emerged as leading medical tourism hubs, attracting international patients seeking high-quality surgical care at competitive costs. According to the Medical Tourism Association, Thailand alone welcomed over 4 million medical tourists in 2022, many of whom sought advanced surgical procedures, including robotic-assisted microsurgeries. Private healthcare providers in these countries are investing heavily in cutting-edge surgical technologies to enhance their global competitiveness.

MARKET CHALLENGES

Shortage of Skilled Robotic Surgeons and Training Infrastructure

The shortage of skilled robotic surgeons and inadequate training infrastructure is acting as big barrier for the Asia Pacific microsurgery robot market players. The operation of microsurgery robots requires specialized training and expertise, which is currently limited in many countries across the region. According to the Asia Pacific Economic Cooperation (APEC), the number of certified robotic surgeons per million population remains significantly lower in emerging markets such as Vietnam, the Philippines, and Indonesia compared to developed nations like Japan and Australia.

The lack of trained professionals limits the effective utilization of microsurgery robots and slows down their adoption rate. The governments and healthcare institutions are increasingly investing in simulation-based training centers and international collaborations to enhance surgical education.

Ethical and Legal Concerns in Robotic-Assisted Surgery

The growing concern around ethical and legal issues associated with robotic-assisted surgery is another attribute that is impeding the growth of the Asia Pacific microsurgery robot market. As surgical robots become more autonomous and integrated with artificial intelligence, questions surrounding liability, patient consent, and data security are becoming more pronounced. In emerging countries like Thailand and Malaysia, regulatory bodies are still in the early stages of developing guidelines for robotic surgery, creating a fragmented legal landscape. These ethical and legal ambiguities pose a significant barrier to the widespread adoption of microsurgery robots, as healthcare providers and policymakers seek to balance innovation with patient safety and regulatory compliance.

SEGMENTAL ANALYSIS

By Application Insights

The oncology surgery segment was the largest by occupying 28.3% of the Asia Pacific microsurgery robot market share in 2024 with the rising incidence of cancer across the region and the increasing adoption of minimally invasive surgical techniques for tumor removal and reconstruction. As per the International Agency for Research on Cancer (IARC), Asia accounts for more than 50% of global cancer cases, with China and India witnessing the fastest growth in cancer diagnoses. In China alone, over 4.8 million new cancer cases were reported in 2022, which is necessitating advanced surgical interventions. Additionally, in Japan, where the aging population is particularly vulnerable to cancer, the government has been promoting robotic-assisted surgeries as part of its national cancer control strategy. According to the National Cancer Center of Japan, over 40% of cancer surgeries in major hospitals now involve robotic assistance.

The ophthalmology surgery segment is lucratively growing with an expected CAGR of 16.8% from 2025 to 2033 with the increasing prevalence of vision-related disorders in aging populations, and the need for ultra-precise surgical interventions. According to the World Health Organization, the Asia Pacific region accounts for nearly 40% of global cases of visual impairment and blindness, with conditions such as cataracts, glaucoma, and age-related macular degeneration being particularly prevalent. In countries like India and China, the growing number of diabetic retinopathy cases has further fueled demand for robotic-assisted eye surgeries. The Japanese Ministry of Health, Labour and Welfare has been supporting clinical trials for robotic eye surgery, aiming to improve surgical outcomes and reduce complications.

By End Use Insights

The hospitals and clinics segment in the Asia Pacific microsurgery robot market held a dominant share in 2024 with the high volume of surgical procedures performed in these settings and the increasing integration of robotic-assisted systems in operating rooms. In countries like South Korea and Singapore, leading hospitals such as Samsung Medical Center and Singapore General Hospital have adopted microsurgery robots to enhance surgical precision and improve patient outcomes. In addition, in Japan, where the healthcare system emphasizes advanced medical technologies, the majority of robotic-assisted surgeries are conducted in hospital settings. Moreover, in Australia, the Royal Australasian College of Surgeons has emphasized the importance of integrating robotic systems into hospital surgical departments to meet the growing demand for minimally invasive procedures.

The Ambulatory surgical centers (ASCs) segment is substantially growing with a CAGR of 15.4% from 2025 to 2033 with the increasing preference for outpatient surgical procedures, which offer lower costs, shorter recovery times, and reduced hospital-acquired infection risks. In South Korea, the Ministry of Health and Welfare has introduced policies to encourage the use of ASCs for non-emergency surgeries, particularly in urban areas where hospital bed occupancy rates are high. This has led to increased investment in robotic platforms for outpatient microsurgical procedures.

REGIONAL ANALYSIS

China Microsurgery Robot Market Insights

was the top performer of the Asia Pacific microsurgery robot market by accounting for 27.2% of share in 2024 with the country’s expanding healthcare infrastructure, increasing prevalence of chronic diseases, and strong government initiatives to promote advanced surgical technologies. The Chinese government has been actively investing in medical robotics as part of its broader healthcare modernization strategy. According to the National Medical Products Administration, over 1,200 robotic surgical systems were installed in Chinese hospitals by the end of 2022, with a significant portion used for microsurgical procedures in oncology and urology. In addition, leading domestic companies such as MicroPort and Auge Medical have been developing indigenous robotic surgical platforms to reduce reliance on imported systems. Furthermore, the growing number of medical tourism cases and the expansion of private healthcare networks have also contributed to market growth.

Japan Microsurgery Robot Market Insights

Japan microsurgery robot market held 20.3% of share in 2024. The country’s well-developed healthcare system, aging population, and early adoption of robotic surgical technologies have made it a key market for microsurgery robots. According to the Japanese Ministry of Health, Labour and Welfare, over 30% of Japan’s population is aged 65 or older, leading to a surge in demand for complex surgical procedures in fields such as neurology, ophthalmology, and cardiovascular surgery. The University of Tokyo Hospital and Osaka University Medical School have been at the forefront of robotic-assisted microsurgery research and clinical applications. Additionally, Japanese companies such as Sony and Olympus have been developing advanced robotic surgical systems tailored to the local market. The Ministry of Economy, Trade and Industry has also supported innovation in surgical robotics through funding and policy incentives.

South Korea Microsurgery Robot Market Insights

South Korea microsurgery robot market growth is likely to have significant CAGR throughput the forecast period with the emphasis on medical innovation, digital health infrastructure, and public-private collaboration has fueled the adoption of microsurgery robots. The South Korean government has actively supported the development and adoption of robotic-assisted surgical systems through initiatives such as the “K-Medical Industry Development Plan,” which aims to position the country as a global leader in medical technology. In addition, leading hospitals such as Severance Hospital and Asan Medical Center have been integrating microsurgery robots into their surgical departments, particularly in oncology and reconstructive surgery. Moreover, domestic companies like Curexo and Rebotics have been developing next-generation robotic surgical platforms, aiming to reduce dependency on foreign manufacturers.

India Microsurgery Robot Market Insights

India microsurgery robot market growth is expected to have steady growth opportunities with the rapid economic growth, expanding private healthcare sector, and increasing demand for advanced surgical procedures contributing to its growing market presence. Additionally, the Indian government’s Ayushman Bharat scheme has improved access to advanced medical treatments, encouraging hospitals to adopt cutting-edge surgical technologies. Moreover, the growing prevalence of chronic diseases such as diabetes and cancer has further fueled the demand for microsurgery robots in Indian hospitals.

Australia Microsurgery Robot Market Insights

Australia microsurgery robot market growth is driven by the well-developed healthcare system, high per capita healthcare expenditure, and strong emphasis on surgical innovation have contributed to the widespread adoption of microsurgery robots. Leading hospitals such as Royal Melbourne Hospital and St. Vincent’s Hospital have integrated microsurgery robots into their surgical departments, particularly for procedures in oncology, urology, and gynecology. The Royal Australasian College of Surgeons has been actively promoting the benefits of robotic surgery in improving patient outcomes and reducing recovery times. Additionally, the Australian government has been supporting the development of local surgical robotics companies through funding and research grants. Companies such as Monash University’s biomedical engineering division have been working on next-generation microsurgery robotic platforms tailored to the Australian healthcare landscape.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Key players in the Asia Pacific Microsurgery Robot Market include Intuitive Surgical, Medtronic, Stryker Corporation, Zimmer Biomet, Smith & Nephew, Asensus Surgical, Renishaw plc, Corindus Vascular Robotics, Medrobotics Corporation, and Microsure.

The Asia Pacific microsurgery robot market growth is driven by rapid technological advancements, increasing healthcare investments, and growing demand for precision surgical solutions. While global players such as Intuitive Surgical, Medtronic, and Stryker maintain a strong presence, regional companies are also emerging as key contenders by offering cost-effective and locally adapted robotic platforms. The competition is not only centered on product innovation but also on expanding service networks, training programs, and strategic collaborations with healthcare institutions.

Market participants are increasingly focusing on enhancing clinical adoption by addressing the skill gap among surgeons and improving access to robotic-assisted procedures in both urban and rural settings. Additionally, the integration of artificial intelligence, teleoperation, and modular system designs is redefining the competitive dynamics.

Top Players in the Asia Pacific Microsurgery Robot Market

One of the leading players in the Asia Pacific microsurgery robot market is Intuitive Surgical, the pioneer behind the da Vinci Surgical System. While originally a U.S.-based company, Intuitive Surgical has significantly expanded its footprint in the Asia Pacific through strategic partnerships, training programs, and localized support services. The company plays a pivotal role in setting global standards for robotic-assisted surgery, influencing clinical adoption and regulatory frameworks in the region.

Medtronic is another key participant shaping the dynamics of the Asia Pacific microsurgery robot market. With its Hugo Robotic-Assisted Surgery System, Medtronic brings a flexible, multi-disciplinary platform tailored to meet the diverse surgical needs across the region. The company emphasizes affordability, modular integration, and collaboration with local healthcare providers to drive adoption in both urban and semi-urban hospitals.

Stryker Corporation is also making significant inroads in the Asia Pacific market with its Mako robotic-arm assisted technology. Originally focused on orthopedics, Stryker has expanded into microsurgery applications, leveraging its reputation for precision and reliability. The company is actively engaging with regional healthcare institutions to build awareness and training infrastructure, which is strengthening its presence in the evolving robotic surgery ecosystem.

Top Strategies Used by Key Market Participants

A primary strategy employed by key players in the Asia Pacific microsurgery robot market is localization of technology and services, where companies adapt their robotic platforms to suit regional healthcare infrastructures, regulatory environments, and surgical practices. This includes offering region-specific training, service support, and cost-optimized models to enhance accessibility.

Another major approach is strategic partnerships with local hospitals, universities, and research institutions that aimed at fostering clinical adoption, conducting joint research, and building a strong user base of trained robotic surgeons. These collaborations also help in gaining regulatory approvals and establishing clinical credibility.

The expanding digital integration and telemedicine compatibility is gaining traction as companies incorporate AI, cloud-based analytics, and remote surgical capabilities into their systems. This not only enhances surgical precision but also aligns with the growing demand for connected healthcare solutions across the Asia Pacific region.

RECENT MARKET DEVELOPMENTS

- In March 2024, Intuitive Surgical launched a regional training center in Singapore to support the development of robotic surgery skills among surgeons and medical professionals across Southeast Asia, aiming to expand clinical adoption.

- In July 2023, Medtronic partnered with a leading Japanese hospital to conduct clinical trials for its next-generation robotic platform, focusing on microsurgical applications in neurology and ophthalmology.

- In November 2023, Stryker announced a collaboration with a South Korean healthcare technology firm to develop AI-integrated surgical robotics tailored for the Asia Pacific market, emphasizing precision and adaptability.

- In February 2024, a major Chinese robotics firm expanded its distribution network by signing agreements with private hospital chains in India and Indonesia to introduce cost-effective microsurgery robots for regional healthcare providers.

MARKET SEGMENTATION

This research report on the Asia Pacific Microsurgery Robot Market is segmented and sub-segmented based on categories.

By Application

- Oncology surgery

- Ophthalmology surgery

- Obstetrics and gynecology surgery

- Micro anastomosis

- Reconstructive surgery

- ENT surgery

- Gastrointestinal surgery

- Cardiovascular surgery

- Ureterorenoscopy

- Neurovascular surgery

- Urology surgery

- Other applications

By End Use

- Hospitals and clinics

- Ambulatory surgical centers

- Research institutes

- Other end-users

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What challenges does the Asia Pacific Microsurgery Robot Market face?

High initial costs, lack of skilled professionals, and limited adoption in rural areas are significant challenges.

What is the expected growth rate of the Asia Pacific Microsurgery Robot Market?

The market is expected to grow at a robust CAGR due to increasing acceptance of robotic technology in surgical applications.

What is driving the growth of the Asia Pacific Microsurgery Robot Market?

Key drivers include rising demand for minimally invasive procedures, technological advancements, and increasing healthcare investments in emerging Asian economies.

What is the future outlook for the Asia Pacific Microsurgery Robot Market?

The outlook is highly positive, with increasing adoption, technological innovation, and expansion into emerging healthcare markets.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com