Asia Pacific Nanotechnology In Medical Devices Market Research Report – Segmented By Product ,Application, End-User & Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore & Rest of APAC) - Industry Analysis (2025 to 2033)

APAC Nanotechnology in Medical Devices Market Size

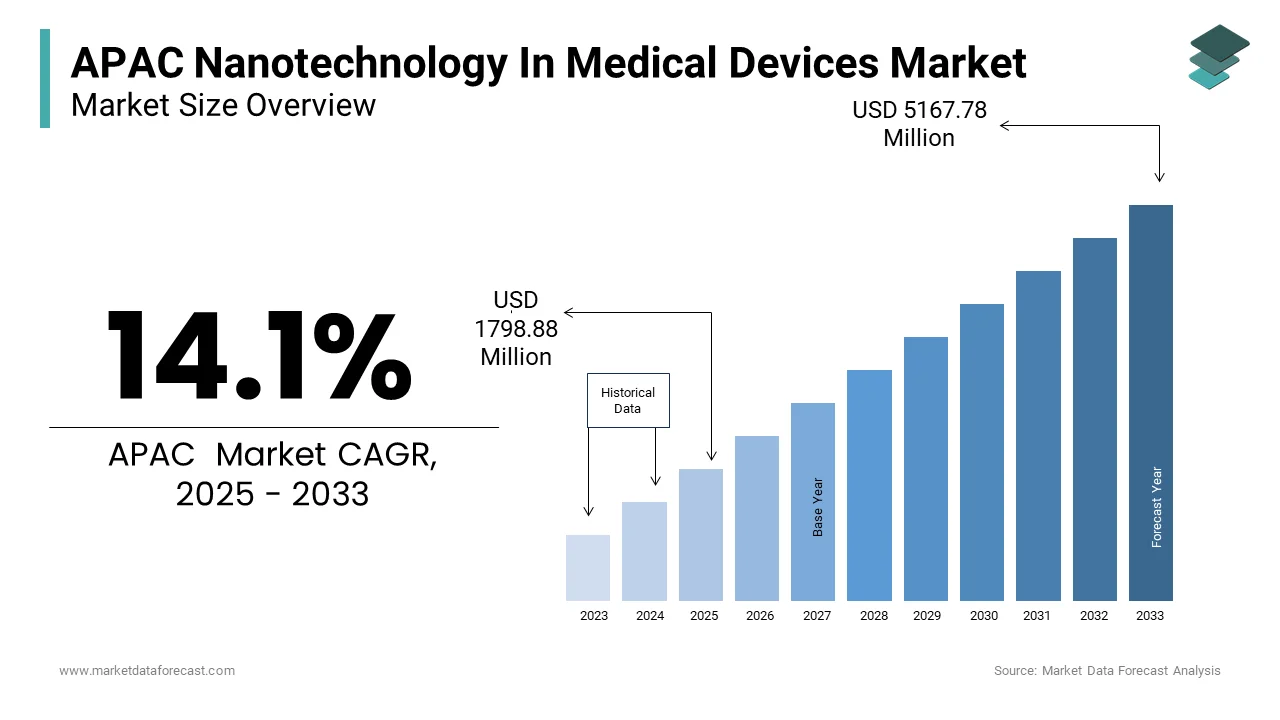

The APAC Nanotechnology in Medical Devices Market Size was valued at USD 1576.58 Million in 2024. The APAC Nanotechnology in Medical Devices Market Size is expected to have 14.1 % CAGR from 2025 to 2033 and be worth USD 5167.78 Million by 2033 from USD 1798.88 Million in 2025.

The nanotechnology in medical devices are advanced application that enhances precision, reduces invasiveness, and improves patient outcomes across various clinical settings. Asia Pacific has emerged as a focal point for technological advancements, with countries like Japan, South Korea, China, and India leading the charge. The growing prevalence of chronic diseases, coupled with rising healthcare expenditures, has accelerated the adoption of nanotechnology-enabled solutions. Additionally, government initiatives are playing a pivotal role in fostering growth. For instance, the Department of Science and Technology in India launched the Nano Science and Technology Mission, which allocates significant funding toward biomedical applications of nanotechnology. Meanwhile, Japan's Ministry of Education, Culture, Sports, Science and Technology has been actively supporting R&D projects that integrate nanotechnology into next-generation medical devices.

MARKET DRIVERS

Rising Demand for Precision Medicine and Personalized Healthcare

One of the primary drivers fueling the U.S. eClinical solutions market is the growing emphasis on precision medicine and personalized healthcare approaches. Precision medicine relies heavily on data-driven decision-making, real-world evidence, and streamlined clinical trial processes areas where eClinical technologies excel. This trend is further supported by the U.S. Food and Drug Administration’s (FDA) increased endorsement of decentralized clinical trials, which leverage eClinical platforms such as electronic clinical outcome assessments (eCOA), electronic patient-reported outcomes (ePRO), and interactive response technology (IRT). In 2023, FDA guidance encouraged the use of remote monitoring tools, directly influencing the adoption of these digital solutions. Moreover, biopharmaceutical companies are increasingly outsourcing clinical trial operations to contract research organizations (CROs) that utilize advanced eClinical software, improving efficiency and reducing time-to-market for new therapies.

Regulatory Support and Digital Transformation in Clinical Trials

Regulatory support from key agencies such as the U.S. Food and Drug Administration (FDA) and the Office for Human Research Protections (OHRP) has played a crucial role in accelerating the adoption of eClinical solutions. The FDA’s evolving regulatory framework encourages the use of digital tools to improve trial transparency, compliance, and patient engagement. In 2022, the FDA released updated guidelines promoting the use of electronic informed consent (eConsent) and remote monitoring technologies, especially in post-pandemic clinical trial environments.

This regulatory shift aligns with broader industry trends toward digital transformation. A survey conducted by the Tufts Center for the Study of Drug Development found that 82% of pharmaceutical companies in the U.S. have invested in eClinical infrastructure since 2021 to enhance trial agility and reduce operational costs. The push for real-world evidence (RWE) generation has intensified the need for advanced data capture mechanisms. These investments reinforce the foundational role of eClinical solutions in modernizing clinical development and ensuring compliance with evolving regulatory expectations.

MARKET RESTRAINTS

High Implementation Costs and Technical Complexity

Despite the growing demand for eClinical solutions, one of the major restraints impacting market growth is the high implementation cost and technical complexity associated with deploying these systems. Small and mid-sized biotech firms often face financial and operational barriers when integrating eClinical tools such as electronic data capture (EDC), clinical trial management systems (CTMS), and interactive response technology (IRT). Furthermore, the integration of legacy systems with modern eClinical software can be cumbersome and resource-intensive. Many organizations rely on outdated infrastructure that is not easily compatible with newer digital tools, requiring extensive customization and training. Additionally, the shortage of skilled personnel capable of managing complex eClinical ecosystems adds another layer of difficulty. The Association of Clinical Data Management reported in 2023 that only 32% of clinical research professionals felt adequately trained to handle advanced eClinical tools without external consulting support.

Data Privacy Concerns and Cybersecurity Vulnerabilities

Data privacy concerns and cybersecurity vulnerabilities represent a significant restraint on the U.S. eClinical solutions market. As clinical trials increasingly rely on digital data collection and cloud-based storage, the risk of cyberattacks and data breaches has escalated. These incidents have led to heightened scrutiny from both regulators and patients. The Health Insurance Portability and Accountability Act (HIPAA) imposes strict requirements on how protected health information (PHI) must be handled, adding compliance burdens for organizations deploying eClinical tools. Moreover, a survey conducted by PwC found that 68% of clinical trial participants expressed concern about their personal health data being compromised if collected through digital platforms. This reluctance impacts recruitment rates and delays trial timelines. Additionally, cybersecurity threats such as ransomware attacks have disrupted trial operations, with some organizations reporting downtime lasting weeks

MARKET OPPORTUNITIES

Expansion of Decentralized Clinical Trials (DCTs)

The rapid expansion of decentralized clinical trials (DCTs) presents a significant opportunity for the U.S. eClinical solutions market. DCTs leverage digital tools such as telemedicine, wearables, mobile apps, and home nursing services to conduct clinical research remotely, thereby reducing site dependency and enhancing patient accessibility. This shift is driven by both patient demand and sponsor interest in accelerating trial timelines. Patients benefit from reduced travel burdens and greater flexibility, while sponsors gain access to broader and more diverse participant pools. Additionally, the rise of virtual trial platforms and hybrid models has spurred demand for integrated eClinical systems that can manage remote data capture, real-time monitoring, and centralized analytics.

Integration of Artificial Intelligence and Machine Learning in Clinical Trials

Another transformative opportunity in the U.S. eClinical solutions market lies in the integration of artificial intelligence (AI) and machine learning (ML) into clinical trial operations. AI-powered analytics are increasingly being used to optimize trial design, predict patient outcomes, and identify suitable candidates for enrollment. According to a report by McKinsey, AI-driven patient matching tools have improved screening efficiency by up to 45%, significantly reducing the time required to enroll qualified participants.

Machine learning algorithms also play a crucial role in data cleaning and anomaly detection. By automating error identification and correction, these tools enhance data quality and regulatory compliance. Moreover, predictive analytics powered by AI is enabling proactive risk mitigation in clinical trials. Sponsors using AI-based risk prediction models reported a 30% reduction in protocol deviations, as noted by Oracle Health Sciences. These advancements are driving a paradigm shift in how clinical trials are managed, making them more efficient, cost-effective, and patient-centric.

MARKET CHALLENGES

Interoperability Issues Across Disparate Systems

One of the foremost challenges facing the U.S. eClinical solutions market is the lack of interoperability across disparate clinical trial systems. Despite the proliferation of digital tools such as electronic data capture (EDC), clinical trial management systems (CTMS), and safety databases, seamless data exchange remains elusive. The absence of standardized data formats and communication protocols exacerbates this issue. While initiatives such as HL7 FHIR and CDISC standards aim to promote harmonization, widespread adoption remains inconsistent. This fragmentation not only increases operational inefficiencies but also heightens the risk of data discrepancies and compliance violations. A survey by the Society for Clinical Data Management found that data reconciliation across incompatible systems consumed up to 25% of total trial management time.

Evolving Regulatory Requirements and Compliance Burdens

Evolving regulatory requirements pose a persistent challenge for stakeholders in the U.S. eClinical solutions market. As digital tools become more embedded in clinical trial operations, regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) continue to refine their oversight frameworks. In 2023, the FDA issued updated guidance on the use of digital health technologies in clinical investigations by introducing new validation and documentation mandates that many sponsors find difficult to navigate.

Compliance with regulations such as 21 CFR Part 11, which governs electronic records and signatures, requires rigorous validation, audit trails, and secure data handling practices. According to a report by Accenture, nearly 50% of pharmaceutical firms experienced delays in trial timelines due to non-compliance with evolving eClinical regulations. Additionally, the introduction of the EU’s General Data Protection Regulation (GDPR) has further complicated cross-border clinical trial operations involving U.S.-based sponsors. Moreover, regulatory uncertainty around emerging technologies like blockchain and AI in clinical data management creates hesitancy among developers and sponsors.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 14.1 % |

| Segments Covered | By Product ,Application, End-User |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | China, India, Japan, South Korea, Australia, New Zealand, Thailand, Indonesia, Philippines, Vietnam, Singapore, Rest of APAC. |

| Market Leader Profiled | AMAG pharmaceuticals, Jude Medical, Inc., Smith & Nephew, Inc., PerkinElmer |

SEGMENTAL ANALYSIS

By Product Insights

The Clinical Trial Management Systems (CTMS) segment was the largest by accounting for 25.4% of the share of the U.S. eClinical solutions market, accounting for approximately 25% of total revenue in 2024. CTMS platforms are instrumental in managing the complex logistics and workflows involved in clinical trials, including budgeting, resource allocation, timelines, and regulatory compliance.

One key driver behind CTMS dominance is its essential role in streamlining trial execution amid rising complexity and costs. According to a report by the Tufts Center for the Study of Drug Development, the average cost of developing a new drug exceeded $2.6 billion in 2023, with operational inefficiencies contributing significantly to this figure. CTMS adoption helps mitigate these inefficiencies by automating scheduling, document tracking, and site monitoring, thereby reducing delays and administrative overhead.

Another major factor is the increasing volume of multi-site and global trials. As per Frost & Sullivan, over 70% of clinical trials initiated in the U.S. in 2023 spanned multiple sites, necessitating centralized management systems to ensure coordination and data consistency. Additionally, regulatory agencies such as the FDA have emphasized the importance of real-time visibility into trial operations, further reinforcing the need for robust CTMS platforms across sponsor organizations and contract research organizations (CROs).

The Electronic Clinical Outcome Assessment (eCOA) segment is projected to grow at the fastest rate in the U.S. eClinical solutions market, registering a compound annual growth rate (CAGR) of 14.8% from 2024 to 2030. This rapid expansion is primarily driven by the increasing emphasis on patient-centricity and real-world evidence generation in clinical development.

eCOA tools—such as mobile apps, wearables, and electronic diaries—are gaining traction due to their ability to capture high-quality, real-time patient-reported outcomes (PROs). According to a survey conducted by the Clinical Outcome Assessment Community, nearly 60% of biopharmaceutical firms reported improved data accuracy after implementing eCOA systems, compared to traditional paper-based methods.

Moreover, the U.S. Food and Drug Administration (FDA) has actively encouraged the use of digital endpoints in regulatory submissions. In its 2023 guidance update, the FDA highlighted that over 45% of new drug applications reviewed included some form of eCOA data, reflecting growing acceptance of these tools in evaluating therapeutic efficacy. The rise of decentralized clinical trials (DCTs) has further accelerated demand for eCOA solutions, with sponsors seeking flexible and scalable data collection mechanisms that align with evolving trial models.

By Delivery Mode Insights

The licensed enterprise or on-premise delivery mode currently holds the largest share of the U.S. eClinical solutions market, representing nearly 40% of total deployments in 2024. This preference stems from the need for greater control, customization, and data security among large pharmaceutical companies and CROs conducting high-stakes clinical trials.

A primary driver of this dominance is the stringent regulatory environment governing clinical trial data handling. Many sponsors, particularly those operating in highly regulated therapeutic areas such as oncology and neurology, opt for on-premise solutions to maintain full oversight of their data infrastructure. According to a report by Deloitte, over 65% of surveyed pharmaceutical executives indicated that data sovereignty concerns were a decisive factor in selecting on-premise deployment options.

Additionally, legacy system integration plays a crucial role in sustaining on-premise adoption. A study published in Applied Clinical Trials noted that more than half of all large-scale clinical trial sponsors still rely on older IT infrastructures incompatible with cloud-native architectures. These organizations often choose licensed enterprise models to avoid costly and disruptive system overhauls, ensuring continuity in trial execution while meeting compliance requirements set forth by the FDA and other regulatory bodies.

The cloud-based delivery mode is anticipated to register the highest growth within the U.S. eClinical solutions market, with a projected CAGR of 16.2% between 2024 and 2030. This rapid adoption is fueled by the increasing shift toward agile, scalable, and cost-effective clinical trial operations, especially among small-to-mid-sized biotech firms and academic research institutions.

Cloud-based platforms offer advantages such as faster deployment, reduced capital expenditure, and seamless scalability—factors that appeal to organizations looking to accelerate trial timelines without heavy upfront investments. According to Grand View Research, cloud-hosted eClinical solutions accounted for over 50% of new system implementations in 2023, driven largely by the rise of decentralized clinical trials (DCTs) and hybrid trial models.

Furthermore, the push for interoperability and real-time data access has made cloud infrastructure indispensable. As per a report by McKinsey, cloud-enabled clinical trial environments demonstrated a 30% improvement in cross-functional collaboration and data synchronization. With leading vendors like Oracle Health Sciences and Medidata expanding their cloud portfolios, and regulators increasingly endorsing remote data access models, the momentum for cloud-based eClinical solutions is expected to sustain well into the next decade.

By Development Phase Insights

Phase III clinical trials represent the largest segment in the U.S. eClinical solutions market, capturing an estimated 35% of total spending in 2024. This phase involves extensive testing across large patient populations to confirm a drug’s efficacy, monitor side effects, and compare it against existing treatments—making it both the most expensive and data-intensive stage of drug development.

According to the Tufts Center for the Study of Drug Development, the average cost of conducting a Phase III trial in the U.S. exceeds $30 million, with some trials surpassing $100 million depending on duration and complexity. Given the high stakes involved, sponsors heavily rely on advanced eClinical tools such as EDC, CTMS, and safety reporting systems to ensure data integrity, regulatory compliance, and efficient trial execution.

Additionally, the FDA mandates rigorous documentation and traceability for Phase III studies, which increases reliance on structured eClinical platforms. In 2023, over 60% of New Drug Applications (NDAs) submitted to the FDA contained data from Phase III trials managed using integrated eClinical systems. Furthermore, the trend toward adaptive trial designs and biomarker-driven stratification in Phase III studies has heightened the demand for real-time data analytics and patient monitoring tools, reinforcing the dominance of this development phase in the eClinical solutions landscape.

Phase IV clinical trials are experiencing the fastest growth in the U.S. eClinical solutions market, projected to expand at a CAGR of 15.6% through 2030. These post-marketing surveillance studies are becoming increasingly important as regulators and payers demand long-term real-world evidence (RWE) to support drug approvals and reimbursement decisions.

The Centers for Medicare & Medicaid Services (CMS) reported in 2023 that over $1.2 billion was allocated to support real-world data initiatives linked to post-approval drug monitoring. This funding has spurred increased investment in eClinical technologies capable of capturing longitudinal patient outcomes outside of controlled trial settings. Moreover, the FDA’s Sentinel Initiative—which leverages digital health records and patient registries to track drug safety—has further boosted the demand for eClinical tools tailored for Phase IV studies.

In addition, the rise of value-based healthcare models has intensified the focus on drug performance in diverse patient populations. As per a report by IQVIA, more than 40% of newly approved drugs in 2023 were accompanied by post-marketing commitments requiring ongoing real-world data collection. To meet these obligations efficiently, pharmaceutical companies are turning to cloud-based EDC, ePRO, and safety monitoring platforms, driving significant growth in the Phase IV segment of the U.S. eClinical solutions market.

By End-User Insights

Pharmaceutical and biotechnology companies collectively constitute the largest end-user segment in the U.S. eClinical solutions market, commanding approximately 45% of total expenditures in 2024. These organizations drive demand due to their substantial investments in drug discovery, regulatory compliance, and clinical trial efficiency enhancement.

A key reason for their dominance is the sheer scale of clinical development activities undertaken by major pharma players. According to the Pharmaceutical Research and Manufacturers of America (PhRMA), there were over 9,000 investigational medicines in development globally in 2023, with more than 40% of these trials being conducted in the U.S. Managing such a vast pipeline requires sophisticated eClinical tools, including EDC, CTMS, and pharmacovigilance software.

Additionally, the industry’s transition toward decentralized and AI-driven trial models has further entrenched pharma and biotech firms as the primary consumers of eClinical technologies. As per a McKinsey analysis, top-tier pharmaceutical companies spent an average of $120 million annually on digital trial infrastructure in 2023, with mid-sized firms allocating proportionally higher percentages of their R&D budgets to similar investments. These trends underscore the pivotal role of pharma and biotech organizations in shaping the trajectory of the U.S. eClinical solutions market.

Medical device manufacturers are emerging as the fastest-growing end-users in the U.S. eClinical solutions market, with a projected CAGR of 14.4% over the forecast period. This growth is driven by the increasing complexity of medical device trials and the tightening of regulatory requirements surrounding device approval and post-market surveillance.

Unlike pharmaceutical trials, medical device studies often involve smaller sample sizes, shorter timelines, and more variable endpoints—necessitating specialized eClinical tools for efficient data capture and regulatory submission. According to the U.S. Food and Drug Administration (FDA), in 2023, over 1,500 pre-market approval (PMA) applications were submitted for Class III medical devices, each requiring extensive clinical data collection and validation.

Moreover, the implementation of the EU’s Medical Device Regulation (MDR) and the FDA’s Unique Device Identifier (UDI) mandate has amplified the need for real-time, compliant clinical data systems. As per a report by Frost & Sullivan, over 60% of medical device firms adopted dedicated eClinical platforms between 2021 and 2023 to meet these evolving standards. The convergence of digital health and connected diagnostics is also fueling demand for integrated eClinical solutions, positioning medical device manufacturers as a rapidly expanding segment in the U.S. market.

COUNTRY LEVEL ANALYSIS

China was the largest contributor by holding 30.1% of the APAC Nanotechnology In Medical Devices market share in 2024. The Chinese government has prioritized nanomedicine through initiatives like the "National Key R&D Program," allocating over CNY 2.5 billion (~USD 350 million) in 2023 alone for biomedical nanotechnology research. Institutions such as the National Center for Nanoscience and Technology have spearheaded the development of nano-drug delivery systems and diagnostic biosensors.

Japan was positioned second with 22.2% of the APAC Nanotechnology In Medical Devices market share in 2024. Japan has long been a global leader in precision engineering and materials science, providing a solid foundation for nanotechnology applications in healthcare. Hospitals and research institutions such as Osaka University and Tokyo Medical and Dental University are pioneering the use of nanoscale imaging agents and antimicrobial-coated implants. Additionally, Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) has streamlined regulatory pathways for innovative nanotechnologies, accelerating commercialization.

India Nanotechnology In Medical Devices market growth is lucratively to grow with a CAGR in the next coming years. The Department of Science and Technology’s Nano-Mission program has played a crucial role in advancing nanomedicine, funding over 250 research projects since its inception. Moreover, India’s cost-effective manufacturing ecosystem is attracting multinational players to establish R&D centers focused on scalable nanodevice production. Companies like Dr. Reddy’s and Apollo Hospitals are collaborating on nano-biosensor development for chronic disease management.

South Korea Nanotechnology In Medical Devices market is likely to grow steadily throughput the forecast period. South Korea’s dense network of semiconductor and electronics manufacturers provides a unique advantage in producing miniaturized biosensors and implantable medical devices. For instance, Samsung Medison has integrated nanoscale imaging agents into ultrasound systems to enhance diagnostic clarity.

Australia Nanotechnology In Medical Devices market is expected to grow prominently in the next coming years. The Australian Government’s Cooperative Research Centres (CRC) program has funded several nanotechnology-focused healthcare projects, including the development of nanostructured antimicrobial surfaces for catheters and implants. Moreover, Australia’s proximity to major Asian markets positions it as a gateway for technology transfer and clinical trials. Institutions such as the University of Melbourne and CSIRO have been instrumental in developing nano-biosensors for remote patient monitoring, aligning with national telehealth initiatives.

Top Players in the Market

Oracle Health Sciences (Oracle Corporation)

Oracle plays a pivotal role in shaping the global eClinical solutions landscape through its comprehensive suite of clinical trial technologies. The company’s offerings include electronic data capture, clinical analytics, and trial management systems that streamline the entire drug development lifecycle. Known for innovation and scalability, Oracle continues to influence market dynamics by integrating advanced technologies such as artificial intelligence and machine learning into its platforms, which is making clinical trials more efficient and patient-centric.

Medidata Solutions (A Dassault Systèmes Company)

Medidata has long been recognized as a leader in digital transformation within clinical research. Its cloud-based platform supports end-to-end clinical trial operations, from protocol design to regulatory submission. With a strong focus on real-world evidence and decentralized trial models, Medidata contributes significantly to improving trial efficiency and patient engagement globally. The company's continuous R&D efforts ensure it remains at the forefront of technological advancement in the eClinical space.

Parexel Informatics (Parexel International Corporation)

Parexel Informatics delivers robust eClinical tools tailored for complex and large-scale clinical studies. Its integrated solutions support data collection, safety monitoring, and trial execution across therapeutic areas. As a major contract research organization (CRO), Parexel leverages its eClinical expertise to enhance sponsor collaboration and accelerate time-to-market for new therapies. Its contributions extend beyond the U.S., influencing global clinical development standards and practices.

Top Strategies Used by Key Market Participants

Expansion Through Strategic Acquisitions

Leading players frequently acquire niche technology providers or complementary service firms to enhance their product portfolios and expand their market reach. These acquisitions enable them to integrate cutting-edge capabilities, strengthen customer relationships, and offer more comprehensive eClinical solutions tailored to evolving industry needs.

Development of Integrated and AI-Driven Platforms

To stay competitive, companies are investing heavily in building unified platforms that combine multiple eClinical functions into seamless ecosystems. Incorporating artificial intelligence and machine learning further enhances predictive analytics, patient recruitment, and data quality, allowing sponsors to conduct smarter and faster clinical trials.

Focus on Decentralized Clinical Trial Technologies

With the rise of patient-centric trial models, key players are prioritizing the development of decentralized trial tools such as mobile apps, wearables, and remote monitoring systems. This shift aligns with industry trends toward flexibility, broader patient access, and real-time data capture, reinforcing the relevance of modern eClinical solutions.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing an active role in the APAC Nanotechnology in Medical Devices Market are AMAG pharmaceuticals, Jude Medical, Inc., Smith & Nephew, Inc., PerkinElmer, Inc., Acusphere, Inc., 3M Company, Affymetrix, Inc., Starkey Hearing Technologies, and Stryker Corporation.

The competition in the APAC nanotechnology in medical devices market is intensifying as both global giants and regional innovators strive to capture a larger share of this rapidly evolving sector. Established players from Japan, South Korea, and China are leveraging their strong R&D capabilities and manufacturing infrastructure to introduce cutting-edge nano-enabled medical solutions. At the same time, emerging biotech firms and startups are disrupting traditional paradigms by introducing novel applications in diagnostics, drug delivery, and implantable devices.

This dynamic landscape is characterized by a blend of collaboration and rivalry, with companies forming strategic alliances to accelerate product development while also competing fiercely in technology differentiation and market expansion. Government policies and funding initiatives further influence competitive positioning, as nations seek to build domestic dominance in nanomedicine. Additionally, the increasing convergence between pharmaceuticals, digital health, and nanotechnology is blurring industry boundaries, prompting cross-sector partnerships and diversification strategies.

RECENT HAPPENINGS IN THE MARKET

In February 2024, Fujifilm Healthcare announced a partnership with a Singapore-based nanotech startup to co-develop next-generation nano-contrast agents for enhanced MRI imaging. This collaboration aims to improve early detection of neurological disorders and cancers by leveraging ultra-sensitive nanoparticle formulations.

In June 2024, Hitachi, Ltd. launched an internal innovation division dedicated exclusively to nano-biomedical applications. This initiative focuses on integrating nanotechnology with AI-driven diagnostics to create smarter, more responsive medical devices tailored for the APAC market.

In September 2024, Samsung Medison introduced a new line of portable ultrasound devices embedded with nano-sensor technology designed to offer real-time blood flow analysis by enhancing diagnostic accuracy for cardiovascular and tumor-related conditions.

In November 2024, Takeda Pharmaceutical in collaboration with a Japanese nanomaterials firm, initiated clinical trials for a nano-drug delivery system targeting pancreatic cancer, which is aiming to improve therapeutic efficacy and reduce systemic side effects.

In March 2025, Canon Electron Tubes & Devices, a subsidiary of Canon Inc., unveiled a new nanoscale biosensor platform intended for wearable health monitoring applications. This technology is expected to support continuous physiological tracking and early disease warning systems within the APAC telehealth ecosystem.

MARKET SEGMENTATION

This research report on the apac nanotechnology in medical devices market has been segmented and sub-segmented into the following categories.

By Product

- Active Implantable Devices

- cardiac pacemakers

- Neurostimulators

- Implantable Drug Delivery Systems

- Biochips

- Lab-On-A-Chip Devices

- DNA Microarrays

- Protein Microarrays

- Implantable Materials

- Nanocomposite Materials

- Biodegradable Polymers

- Coatings For Implants

- Medical Textiles and Wound Dressings

- Nanofiber Dressings

- Antimicrobial Textiles

- Smart Textiles For Monitoring

- Other Products(Nanoparticles For Imaging, Diagnostic Devices Incorporating Nanotechnology)

By Application

- Therapeutic Applications

- Diagnostic Applications

- Research Applications

By End-Users

- Hospitals

- Clinics

- Other End-Users

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What are the key drivers of the APAC nanotechnology in medical devices market?

Major drivers include rising demand for minimally invasive procedures, growing geriatric population, increasing chronic diseases, and government support for nanomedicine R&D.

Which countries in APAC are leading in nanotechnology medical device adoption?

China, Japan, South Korea, and India are among the leading countries due to strong R&D investment, technological infrastructure, and expanding healthcare sectors.

What are the major applications of nanotechnology in medical devices?

Applications include targeted drug delivery systems, nano-imaging agents, nano-sensors for diagnostics, orthopedic implants, and wound healing devices.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com