- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$1.16 BnMarket Estimate, 2026

$1.23 BnMarket Forecast, 2034

$2.02 BnCAGR, 2026–2034

6.36%Executive Summary: Asia Pacific Passive Fireproofing System Market

- Market Scope: Comprehensive regional Asia Pacific passive fireproofing system market analysis covering product categories, application segments, country leadership frameworks, key growth drivers, market trends, and competitive landscape.

- Market Valuation: Valued at USD 1.16 billion (2025), estimated at USD 1.23 billion (2026), and projected to reach USD 2.02 billion by 2034, registering a robust CAGR of 6.36% (2026–2034).

- Primary Growth Drivers: Stringent fire safety regulations, rapid urbanization, expanding infrastructure projects, and rising fire protection awareness across residential, commercial, and industrial sectors. Notable trends include cementitious materials, intumescent paints, compartmentalization systems, and green building developments.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Product Type & Application | Cementitious Materials segment (45.8% market share in 2025) and Construction segment (50.7% total revenue) | Intumescent Coatings (8.5% CAGR) and Oil & Gas segment (9.2% CAGR) |

| By Region & Country | China (led the Asia Pacific market with a 35.8% market share in 2025) | Asia Pacific region overall (expanding at a steady CAGR of 6.36%) |

Major Market Players & Market Structure

Market Structure: Highly competitive fire protection and construction materials landscape featuring major international enterprises competing through product innovation, strategic partnerships, firestop sealant launches, and specialized training/awareness programs.

Key Companies: Lloyd Insulations (India) Limited, Illbruck, Sharpfibre Limited, Hempel A/S, Rudolf Hensel GmbH, HILTI, Carboline, Morgan Advanced Materials plc, Contego International Inc, Tecresa Protección Pasiva, S.L., Isolatek International, 3M, PPG Industries, Inc., Etex Group, AkzoNobel, and Hilti Corporation.

Asia Pacific Passive Fireproofing System Market Size

The size of the Asia Pacific passive fireproofing system market was worth USD 1.16 billion in 2025. The Asia Pacific market is anticipated to grow at a CAGR of 6.36% from 2026 to 2034 and be worth USD 2.02 billion by 2034 from USD 1.23 billion in 2026.

A passive fireproofing system is focusing on materials and technologies designed to contain fires and prevent structural collapse during emergencies. These systems include fire-resistant coatings, intumescent paints, firestops, and insulation materials that are integrated into buildings to enhance safety without requiring active intervention. The region's rapid urbanization and infrastructure development have amplified the need for robust fireproofing solutions.

MARKET DRIVERS

Stringent Regulatory Frameworks

Stringent fire safety regulations are a primary driver of the passive fireproofing system market in the Asia Pacific. Governments across the region have implemented comprehensive building codes and safety standards to mitigate fire risks, particularly in densely populated urban areas. For example, in Australia, all new commercial and residential structures must incorporate passive fireproofing measures, including fire-resistant walls and compartmentalization systems. Similarly, India mandates the use of fire-retardant materials in high-rise buildings, ensuring compliance with global safety benchmarks.

These regulations are enforced through rigorous inspections and penalties for non-compliance, compelling builders and developers to adopt advanced fireproofing technologies. Like, a significant potion of new construction projects in the region now integrate passive fireproofing systems, reflecting the influence of regulatory frameworks. Furthermore, the rise in multi-story developments, particularly in cities like Mumbai and Tokyo, has intensified the demand for fire-resistant coatings and insulation materials.

Rising Incidences of Fire Hazards

Another significant driver is the increasing frequency of fire hazards in the region, exacerbated by industrial accidents and electrical malfunctions. Also, fire-related fatalities in the Asia Pacific account for a notable share of global fire deaths annually, showing the urgent need for preventive measures. Industrial facilities, such as chemical plants and refineries, are particularly vulnerable due to the presence of flammable materials.

For instance, a 2021 fire at a petrochemical plant in South Korea caused major damages, prompting companies to invest in passive fireproofing solutions like fire-resistant cladding and intumescent coatings. As per the study, fire incidents in industrial settings have considerably risen annually over the past five years, driving demand for reliable fire containment systems.

MARKET RESTRAINTS

High Initial Costs

One of the primary restraints impacting the adoption of passive fireproofing systems in the Asia Pacific is the high initial cost associated with these technologies. Fire-resistant materials, such as intumescent paints and firestop sealants, often come at a premium compared to conventional construction materials. According to the Asian Development Bank, small and medium-sized enterprises (SMEs) in the APAC allocate limited share of their budgets to safety measures, leaving limited room for investment in advanced fireproofing solutions. This financial barrier is particularly pronounced in emerging economies like Indonesia and Vietnam, where construction projects are often cost-sensitive. Developers frequently opt for cheaper alternatives, compromising on fire safety to meet budget constraints. Besides, retrofitting existing structures with passive fireproofing systems can be prohibitively expensive, deterring property owners from upgrading their facilities. So, the overall cost burden remains a significant obstacle, especially for rural or underdeveloped areas with limited access to funding.

Lack of Awareness and Training

A further restraint is the lack of awareness and technical expertise regarding passive fireproofing systems. Many builders, architects, and contractors in the region are unfamiliar with the latest advancements in fireproofing technologies, leading to suboptimal implementation. According to the research, a small percentage of construction professionals in Southeast Asia receive formal training on fire safety systems, resulting in improper installation and maintenance of passive fireproofing measures.

This knowledge gap is compounded by the absence of standardized certification programs for fireproofing products. For instance, counterfeit or low-quality materials often flood markets in countries like Thailand and the Philippines, undermining the effectiveness of fireproofing systems. Furthermore, end-users, such as homeowners and tenants, are often unaware of the importance of passive fireproofing, reducing demand for these solutions.

MARKET OPPORTUNITIES

Expansion of Smart Cities and Urban Infrastructure

The proliferation of smart city initiatives presents a significant opportunity for the passive fireproofing system market in the Asia Pacific. Governments across the region are investing heavily in urban infrastructure to accommodate growing populations and enhance living standards. For instance, Singapore’s initiative allocates substantial resources to develop fire-resistant buildings equipped with advanced passive fireproofing technologies. Smart cities prioritize sustainability and resilience, creating a conducive environment for innovations in fireproofing materials. Technologies like intumescent coatings and fire-resistant glass are increasingly integrated into green buildings to meet energy efficiency and safety standards. Apart from these, the rise of mixed-use developments, combining residential, commercial, and recreational spaces, amplifies the demand for compartmentalization systems that prevent fire spread.

Growth of Industrial and Commercial Sectors

The expansion of industrial and commercial sectors in the Asia Pacific offers another lucrative opportunity for passive fireproofing systems. Also, the APAC’s manufacturing output surged between 2020 and 2022, supported by increased production in automotive, electronics, and pharmaceutical industries. These sectors require specialized fireproofing solutions to safeguard assets and personnel from potential fire hazards.For example, data centers, which are critical to the digital economy, rely on fire-resistant insulation and firestop systems to protect sensitive equipment. Like, the number of hyperscale data centers in the region is projected to double in the coming years, creating a robust pipeline for passive fireproofing technologies. Similarly, the booming e-commerce sector has led to the establishment of large-scale warehouses, where fire containment systems play a vital role in minimizing risks.

MARKET CHALLENGES

Counterfeit and Substandard Products

A pressing challenge facing the Asia Pacific passive fireproofing system market is the prevalence of counterfeit and substandard products, which undermine safety standards and erode trust in the industry. Like, counterfeit fireproofing materials account for significant portion of the market in some Southeast Asian countries, posing significant risks to building occupants. These products often fail to meet international fire safety standards, increasing the likelihood of catastrophic failures during emergencies. The influx of counterfeit goods is fueled by weak enforcement mechanisms and inadequate quality control measures in certain regions. For instance, a 2020 investigation revealed that a notable portion of fireproofing materials tested did not comply with required performance benchmarks. This issue is further exacerbated by price-sensitive buyers who prioritize cost over quality, inadvertently supporting the proliferation of substandard products.

Limited Adoption in Rural Areas

Another significant challenge is the limited adoption of passive fireproofing systems in rural and underdeveloped areas, where awareness and infrastructure remain inadequate. According to the United Nations Development Programme, a large percentage of the Asia Pacific population resides in rural regions, many of which lack access to modern fire safety technologies. Traditional construction practices, which rely on locally sourced materials, often overlook fireproofing considerations, leaving communities vulnerable to fire hazards.

Apart from these, the absence of stringent building codes in rural areas further impedes the adoption of passive fireproofing measures. For example, a study by the Asian Institute of Technology found that a very small portion of rural buildings in countries like Cambodia and Laos incorporate fire-resistant materials.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Lloyd Insulations (India) Limited, Illbruck, Sharpfibre Limited, Hempel A/S, Rudolf Hensel GmbH, HILTI, Carboline, Morgan Advanced Materials plc, Contego International Inc, Tecresa Protección Pasiva, S.L., Isolatek International, 3M, PPG Industries, Inc., Etex Group, and others. |

SEGMENTAL ANALYSIS

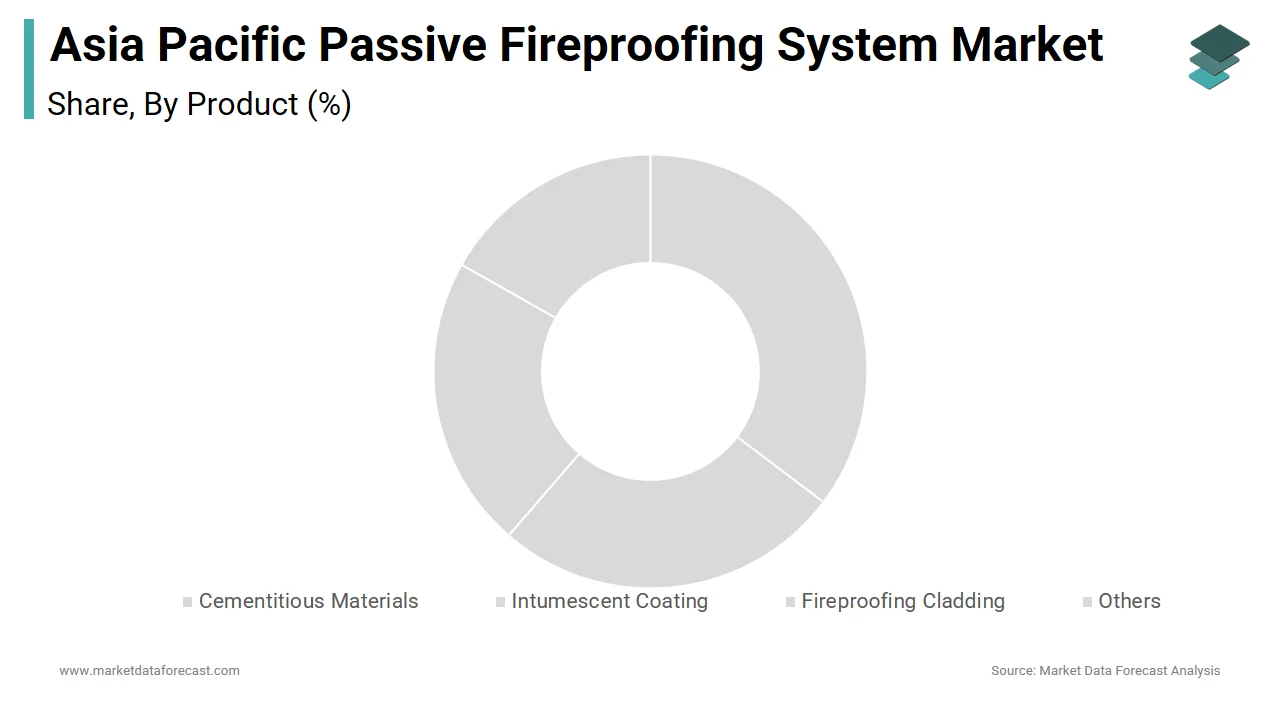

By Product Insights

The cementitious materials segment dominated the Asia Pacific passive fireproofing system market by holding a market share of 45.8% in 2025. This dominance is driven by their widespread use in construction due to their cost-effectiveness and versatility. According to the International Energy Agency, the APAC accounts for considerable share of global cement production, making it a natural hub for cementitious fireproofing solutions. These materials are primarily used in structural steel protection, ensuring compliance with stringent fire safety regulations.

A crucial aspect moving this segment's prowess is the rapid urbanization across the region. The United Nations Department of Economic and Social Affairs projects that urban areas in Asia Pacific will house an additional 1.2 billion people by 2050, necessitating the construction of fire-resistant high-rise buildings. For instance, in China, where a notable portion of new constructions are high-rise structures, cementitious coatings are integral to meeting fire safety codes. Also, these materials are favored for industrial applications, such as refineries and power plants, where they provide reliable fire resistance at elevated temperatures. Another influencing factor is government mandates. In Australia, all commercial buildings exceeding four stories must incorporate passive fireproofing measures, with cementitious materials being a preferred choice due to their durability.

The intumescent coatings segment is the fastest-growing in the Asia Pacific passive fireproofing system market, with a CAGR of 8.5%. This is fueled by their superior performance and aesthetic appeal, particularly in modern architectural designs. Like, the adoption of intumescent coatings in the APAC has significantly increased annually over the past five years, driven by advancements in material science and increasing awareness of fire safety.

The surge in green building initiatives is a significant driver. Singapore’s Green Mark Scheme, which certifies sustainable buildings, emphasizes the use of eco-friendly fireproofing materials like intumescent coatings. These coatings not only protect structures but also align with energy efficiency goals by reducing thermal conductivity. Also, the booming e-commerce sector has amplified demand for fireproof warehouses, where intumescent coatings safeguard steel frameworks without compromising space utilization.

Another contributing point is the rise of retrofitting projects. As per the Asian Development Bank, a considerable share of existing buildings in major cities like Tokyo and Mumbai require fireproofing upgrades, with intumescent coatings being a popular choice due to their ease of application and minimal structural impact.

By Application Insights

The construction industry held the largest share of the Asia Pacific passive fireproofing system market by accounting for a 50.7% of the total revenue in 2025. This is due to the region's unprecedented infrastructure development, driven by urbanization and industrialization. The Asian Development Bank (ADB) report that the construction sector is a significant driver of the global economy, with substantial investments in both infrastructure and building projects.

A basic driver is the proliferation of high-rise buildings, particularly in densely populated cities like Shanghai and Delhi. The National Fire Protection Association reports that a large share of new high-rise constructions in the region incorporate passive fireproofing measures to comply with international safety standards. For example, in Japan, where earthquakes pose additional risks, fire-resistant materials are mandatory to prevent secondary disasters.

Besides, the rise of mixed-use developments amplifies demand.

The oil and gas sector is the quickest rising application in the Asia Pacific passive fireproofing system market, with a CAGR of 9.2%. This progress is propelled by the increasing complexity of industrial operations and the heightened risk of fire hazards in refineries and offshore platforms. Stringent safety regulations are a key driver. As per the Federation of Indian Chambers of Commerce & Industry, fire incidents in refineries have risen over the past decade, prompting companies to invest in advanced fireproofing technologies. A further key element is the expansion of liquefied natural gas (LNG) terminals.

COUNTRY LEVEL ANALYSIS

China dominated the Asia Pacific passive fireproofing system market by commanding a market share of a 35.8%. This dominance is underpinned by the country's status as the world's largest construction hub and its focus on fire safety regulations. Like, the construction sector majorly contributed to the nation's GDP in 2022, with fireproofing systems being a critical element in urban development.

A crucial determinant is the government's push for safer infrastructure. The Ministry of Housing and Urban-Rural Development mandates the use of fire-resistant materials in all public buildings. Additionally, the Belt and Road Initiative has spurred infrastructure projects in neighboring countries, creating export opportunities for Chinese fireproofing manufacturers.

Japan marks a key progress with a notable market share. The country's advanced manufacturing capabilities and emphasis on earthquake-resistant structures drive demand for passive fireproofing systems. According to the Japan Fire Protection Association, fireproofing measures are mandatory in over 90% of industrial facilities, reflecting the nation's commitment to safety. The prevalence of natural disasters further amplifies demand. As per the Japan Meteorological Agency, the country experiences over 1,500 earthquakes annually, necessitating fireproofing solutions that can withstand seismic activity. This has led to innovations in materials like intumescent coatings, which offer dual protection against fire and structural damage.

Australia is also contributing majorly to the market. The nation's stringent building codes and focus on sustainability are key drivers of passive fireproofing adoption. According to the Building Codes of Australia, all new constructions must incorporate fire-resistant materials, ensuring compliance with international standards. The rise of smart cities is another significant factor. Also, the growing number of bushfires has underscored the importance of fire containment measures in residential and commercial buildings.

India is emerging as a key player. The country's rapid urbanization and industrialization are driving demand for fireproofing solutions. According to the Confederation of Indian Industries, the construction sector grew majorly, creating a vast market for passive fireproofing technologies. Government initiatives like "Smart Cities Mission" are also propelling growth. As per the Ministry of Housing and Urban Affairs, over 100 cities are undergoing transformation, with fire safety being a priority. This has led to increased adoption of cementitious materials and intumescent coatings in both residential and industrial projects.

South Korea accounts for a smaller share of the market and is driven by its advanced manufacturing sector and focus on fire safety. The Korea Occupational Safety and Health Agency (KOSHA) does mandate fireproofing measures in many industrial facilities, and these measures are often designed to meet or exceed global standards. Also, the country's emphasis on innovation is a key factor.

KEY MARKET PLAYERS

Some of the noteworthy companies in the APAC passive fireproofing system market profiled in this report are Lloyd Insulations (India) Limited, Illbruck, Sharpfibre Limited, Hempel A/S, Rudolf Hensel GmbH, HILTI, Carboline, Morgan Advanced Materials plc, Contego International Inc, Tecresa Protección Pasiva, S.L., Isolatek International, 3M, PPG Industries, Inc., Etex Group, and others.

TOP LEADING PLAYERS IN THE MARKET

Hilti Corporation

Hilti Corporation is a global leader in fireproofing solutions and a dominant player in the Asia Pacific passive fireproofing system market. The company specializes in innovative firestop systems, including sealants, coatings, and cladding materials, which are widely used in high-rise buildings and industrial facilities. Hilti’s commitment to sustainability and safety has positioned it as a trusted partner for architects, builders, and contractors.

AkzoNobel

AkzoNobel is a key contributor to the passive fireproofing market, renowned for its high-performance intumescent coatings. The company’s expertise lies in developing eco-friendly and durable fireproofing solutions that cater to diverse industries, including oil and gas, construction, and warehousing. AkzoNobel’s focus on R&D has enabled it to introduce cutting-edge products that align with green building standards, making it a preferred choice for sustainable infrastructure projects across the region. Its global presence further strengthens its ability to meet regional demands effectively.

PPG Industries

PPG Industries is a major player in the Asia Pacific passive fireproofing system market, offering a wide range of fire-resistant coatings and materials. The company’s products are designed to provide superior protection against fire hazards while maintaining aesthetic appeal, making them ideal for modern architectural designs. PPG’s strong distribution network and emphasis on customer-centric solutions have solidified its position in the market. Besides, its collaborations with local governments and industry stakeholders ensure compliance with evolving safety standards, reinforcing its global leadership.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Product Innovation and Customization

Leading companies in the Asia Pacific passive fireproofing system market are heavily investing in product innovation to address specific regional challenges. By developing customized solutions tailored to industries like oil and gas or construction, these firms can meet unique fire safety requirements. For instance, introducing eco-friendly coatings that comply with green building certifications not only enhances brand reputation but also aligns with sustainability goals.

Strategic Partnerships and Collaborations

To strengthen their market presence, key players are forming strategic partnerships with construction firms, government agencies, and research institutions. These collaborations enable companies to co-develop advanced fireproofing solutions and expand their reach in untapped markets. For example, partnering with local developers allows firms to integrate fireproofing systems into large-scale infrastructure projects, fostering long-term relationships and ensuring consistent demand for their products.

Focus on Training and Awareness Programs

Promoting awareness about fire safety and the importance of passive fireproofing systems is another critical strategy adopted by market leaders. By organizing training sessions and workshops for architects, contractors, and end-users, companies aim to bridge the knowledge gap and drive adoption.

COMPETITION OVERVIEW

The Asia Pacific passive fireproofing system market is characterized by intense competition, driven by the presence of both multinational corporations and regional players striving to capture market share. Leading companies are leveraging their technological expertise and extensive distribution networks to maintain their dominance, while smaller firms focus on niche applications to carve out a foothold. The market’s competitive landscape is shaped by the growing emphasis on fire safety regulations, which necessitates continuous innovation and compliance with international standards. In addition, the rise of green building initiatives has created opportunities for firms offering eco-friendly solutions, intensifying rivalry among competitors.

RECENT MARKET DEVELOPMENTS

- In March 2023, Hilti Corporation launched a new line of firestop sealants specifically designed for high-rise residential buildings in Singapore. This move aimed to address the growing demand for fireproofing solutions in urban infrastructure projects.

- In June 2023, AkzoNobel partnered with a leading construction firm in India to supply intumescent coatings for a large-scale smart city project. This collaboration was intended to enhance the company’s presence in the rapidly expanding Indian market.

- In August 2023, PPG Industries established a regional training center in Thailand to educate architects and contractors on the latest advancements in passive fireproofing technologies. This initiative underscored the company’s commitment to promoting awareness and adoption in Southeast Asia.

- In November 2023, Sherwin-Williams acquired a local fireproofing materials manufacturer in Vietnam to expand its product portfolio and strengthen its supply chain in the region. This acquisition enabled Sherwin-Williams to tap into the growing demand for affordable fireproofing solutions.

- In January 2024, 3M introduced a new range of eco-friendly fireproofing coatings compliant with green building standards in Australia. This launch positioned 3M as a leader in sustainable fireproofing solutions for the construction sector.

MARKET SEGMENTATION

This Asia Pacific passive fireproofing system market research report is segmented and sub-segmented into the following categories.

By Product

- Cementitious Materials

- Intumescent Coating

- Fireproofing Cladding

- Others

By Application

- Oil & Gas

- Construction

- Industrial

- Warehousing

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC