Asia Pacific Pet Packaging in Pharmaceutical Market Size, Share, Growth, Trends, and Forecast Report – Segmented By product type (tablet bottles, syrup bottles, dropper bottles, vials, mouthwash bottles, handwash and hand sanitizer bottles), Color, and Region (India, China, Japan, South Korea, Australia & New Zealand, Thailand) - Industry Analysis from 2026 to 2034

Market Size, 2025

$4.12 BnMarket Estimate, 2026

$4.40 BnMarket Forecast, 2034

$7.45 BnCAGR, 2026–2034

6.81%Executive Summary: Asia Pacific PET Packaging in Pharmaceutical Market

- Market Scope: Comprehensive regional analysis of the Asia-Pacific polyethylene terephthalate (PET) packaging market in the pharmaceutical sector, covering product types, packaging color variants, country-level leadership, and manufacturing dynamics.

- Market Valuation: Valued at USD 4.12 billion (2025 base year), estimated at USD 4.40 billion (2026), and projected to reach USD 7.45 billion by 2034, registering a robust CAGR of 6.81% (2026–2034).

- Primary Growth Drivers: Expansion of generic drug manufacturing, rising regional healthcare investments, and the structural shift toward lightweight, shatter-resistant plastic containers. Key operational, financial, and logistical highlights include tablet bottles representing 28% of initial volume demand, transparent packaging capturing a 43.1% color market share, and major pharmaceutical hubs across China and India driving massive export-oriented packaging throughput.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Product Type | Tablet Bottles (accounted for approximately 28% of total volume demand) | Handwash & Sanitizer Bottles / Specialized Vials (projected at a 13.6% CAGR) |

| By Packaging Color | Transparent Packaging (dominated with a 43.1% market share in 2025) | Amber-Colored Packaging (forecasted to register a strong 9.8% CAGR) |

| By Material & Technology | Standard PET Resin Formulations & Stretch Blow Molding Infrastructure | Recycled PET (rPET) Blends & Advanced UV-Barrier Technologies |

| By Country / Region | China (led geographically with 31.3% of the market in 2025), followed by India (14.3%) | Emerging Southeast Asian Pharma & Packaging Conversion Hubs |

Major Market Players & Market Structure

Market Structure: Highly competitive Asia-Pacific medical packaging landscape featuring specialized polymer processors and multinational container manufacturers competing intensely on design localization, strict regulatory compliance, sustainable recycled content integration, and cost-effective high-volume production.

Key Companies: Senpet Polymers LLP, Total PET (Radico Khaitan Ltd), Ganesh PET, ALPHA GROUP, and Gerresheimer AG.

Asia Pacific Pet Packaging in Pharmaceutical Market Size

The Asia Pacific pet packaging in pharmaceutical market size was valued at USD 4.12 billion in 2025, and the market size is expected to reach USD 7.45 billion by 2034 from USD 4.40 billion in 2026. The market's promising CAGR for the predicted period is 6.81%.

The Asia Pacific Pet Packaging in Pharmaceutical market encompasses the design, production, and distribution of specialized packaging solutions tailored for pet food, treats, accessories, and healthcare products. This sector includes flexible and rigid packaging formats such as pouches, bags, containers, and cans that prioritize functionality, freshness preservation, convenience, and branding appeal.

According to the World Animal Protection Organization, pet ownership in Southeast Asia has increased by nearly 20% over the past five years, driven by rising disposable incomes and shifting lifestyle preferences. In Japan, where pet ownership rates are among the highest globally, companies like Maruha Nichiro and Orijen have introduced resealable stand-up pouches and vacuum-sealed trays to enhance shelf life and consumer experience. Additionally, Australia's Department of Agriculture has strengthened labeling and hygiene regulations for pet food packaging, which is prompting manufacturers to adopt tamper-evident and recyclable materials.

MARKET DRIVERS

Rising Pet Humanization and Premiumization Trends

One of the most significant drivers of the Asia Pacific Pet Packaging in Pharmaceutical market is the increasing trend of pet humanization, wherein pet owners treat their animals as family members and seek out premium products that reflect this emotional bond. This shift has led to greater investment in high-quality, aesthetically appealing packaging that mirrors human food presentation and branding strategies.

In countries like South Korea and China, younger demographics view pets as companions rather than just animals, influencing purchasing decisions toward premium pet foods and accessories. According to NielsenIQ, more than 60% of urban pet owners in these markets prefer branded pet food packaged in resealable pouches or eco-friendly materials, reflecting a desire for both quality and environmental consciousness.

Expansion of E-Commerce and Direct-to-Consumer Pet Brands

Another key driver shaping the Asia Pacific Pet Packaging in Pharmaceutical market is the rapid expansion of e-commerce and the rise of direct-to-consumer (DTC) pet brands. Online retail platforms have become a primary channel for pet product distribution, necessitating packaging solutions that ensure durability during transit while maintaining product integrity and brand identity.

Moreover, logistics challenges in densely populated cities like Bangkok and Mumbai have prompted the use of compact, space-efficient packaging to reduce shipping costs and carbon footprints. As per the Federation of Indian Chambers of Commerce and Industry (FICCI), e-commerce logistics providers reported a 40% increase in inquiries related to pet product packaging optimization in 2023 alone.

MARKET RESTRAINTS

Regulatory Hurdles and Compliance Costs

A major restraint affecting the Asia Pacific Pet Packaging in Pharmaceutical market is the complex and evolving regulatory landscape governing pet food safety, labeling, and environmental compliance. Governments across the region are implementing stricter packaging standards to ensure consumer transparency and animal health protection, which increases compliance burdens for manufacturers.

For instance, in Australia, the Department of Agriculture and Fisheries has mandated detailed nutritional labeling and traceability requirements for all commercial pet food packaging, which is leading to higher design and printing costs. Similarly, in India, the Food Safety and Standards Authority of India (FSSAI) has introduced stringent migration limits for packaging materials used in contact with pet food, requiring extensive testing before market entry.

Furthermore, environmental regulations targeting single-use plastics are impacting traditional flexible packaging formats. As per the Ministry of Environment of Japan, new restrictions on non-recyclable films and laminates have forced many small and mid-sized pet food brands to redesign their packaging at considerable expense. These regulatory pressures, though beneficial for long-term sustainability, pose short-term financial and operational constraints that can hinder market expansion, especially for smaller players.

High Cost of Sustainable Packaging Materials

Another significant challenge restraining the Asia Pacific Pet Packaging in Pharmaceutical market is the elevated cost associated with sustainable packaging materials. While there is a growing consumer preference for eco-friendly options such as compostable films, biodegradable pouches, and recyclable containers, these alternatives often come at a premium compared to conventional plastic-based solutions.

According to Frost & Sullivan, bio-based packaging materials can be up to 30% more expensive than petroleum-derived counterparts, which is making them less accessible for budget-conscious brands and retailers. This cost differential is particularly pronounced in emerging markets like Vietnam and the Philippines, where price sensitivity remains a dominant purchasing factor.

MARKET OPPORTUNITIES

Growth of Functional and Smart Packaging Solutions

An emerging opportunity in the Asia Pacific Pet Packaging in Pharmaceutical market is the development and adoption of functional and smart packaging solutions designed to enhance product performance, convenience, and consumer engagement. As pet owners increasingly seek convenience and freshness assurance, packaging innovations such as oxygen scavengers, freshness indicators, and resealable closures are gaining traction.

Smart packaging, which integrates QR codes, NFC tags, or temperature-sensitive labels, allows consumers to access real-time product information, track ingredient sources, and verify authenticity. According to the Singapore Packaging Centre, over 50 new pet product launches in 2023 featured scannable packaging elements that linked to nutritional data, feeding guidelines, and veterinary certifications.

Increasing Demand for Customized and Private Label Pet Packaging in Pharmaceutical

The rise of private label and custom-branded Pet Packaging in Pharmaceutical presents a lucrative opportunity for the Asia Pacific market. Retailers, online pet stores, and veterinary clinics are increasingly opting for co-packed or white-label products that allow them to maintain brand consistency while catering to niche customer segments.

According to Euromonitor International, private label pet food accounted for nearly 25% of total sales in Australia and New Zealand in 2023, with major chains like Woolworths and Petco launching exclusive packaging lines. These products require highly customizable packaging formats that support unique branding, ingredient storytelling, and targeted marketing.

MARKET CHALLENGES

Technological Complexity in Developing Recyclable Multi-Layer Films

One of the foremost challenges confronting the Asia Pacific Pet Packaging in Pharmaceutical market is the technological complexity involved in developing recyclable multi-layer films that balance performance with sustainability. Traditional flexible pet food packaging often consists of multiple polymer layers to provide barrier protection against moisture, oxygen, and light, but these structures are difficult to recycle due to material incompatibility.

Moreover, converting existing manufacturing lines to accommodate recyclable film compositions requires significant capital investment. As per the Malaysian Plastics Manufacturers Association, retrofitting extrusion and lamination equipment to produce mono-polymer films could cost up to USD 500,000 per line, deterring smaller converters from transitioning. These technical and financial barriers hinder widespread adoption of truly circular packaging solutions in the pet care sector.

Fragmented Supply Chain and Logistics Constraints

The Asia Pacific Pet Packaging in Pharmaceutical market faces logistical and supply chain fragmentation in rural and semi-urban areas where distribution networks are underdeveloped. Unlike other consumer goods sectors with well-established cold chains and warehousing infrastructure, pet product packaging must navigate diverse climatic conditions, last-mile delivery inefficiencies, and inconsistent storage facilities.

According to the Thailand Logistics Association, approximately 30% of perishable pet food spoilage incidents in 2023 were attributed to inadequate packaging protection during transit. In countries like Indonesia and the Philippines, where island geography complicates transportation, brands face additional costs in ensuring packaging resilience against humidity, vibration, and temperature fluctuations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.81% |

| Segments Covered | By Product Type, Color, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of Asia-Pacific |

| Market Leaders Profiled | Senpet Polymers LLP, Total PET (Radico Khaitan Ltd), Ganesh PET, ALPHA GROUP, and Gerresheimer AG, and others |

SEGMENTAL ANALYSIS

By Product Type Insights

The tablet bottles segment was the largest and held represent the largest segment in the Asia Pacific Pet Packaging in Pharmaceutical market, accounting for approximately 28% of total volume demand in 2023. This dominance is primarily attributed to the rising consumption of veterinary supplements, prescription medications, and functional pet health products that require secure, child-resistant, and moisture-proof packaging. The growing emphasis on preventive pet healthcare across urban centers is substantially to fuel the growth of the segment. According to the Petcare Federation of India, over 45% of pet owners in Tier-1 Indian cities now regularly administer joint care, digestive support, and immunity boosters to their pets, necessitating durable tablet packaging. Additionally, regulatory requirements in countries like Australia and Japan mandate tamper-evident closures and clear dosage instructions on medication bottles, further reinforcing the use of rigid plastic containers.

The handwash and hand sanitizer bottles segment is swiftly emerging with a CAGR of 13.6% from 2026 to 2034. This rapid expansion is driven by heightened hygiene awareness among pet owners and the increasing need for post-petting sanitation solutions in households and commercial pet facilities. A primary growth catalyst is the surge in pet grooming salons and veterinary clinics adopting hygiene-focused protocols. Moreover, manufacturers are introducing dual-purpose bottles that combine pet-safe disinfectants with moisturizing agents, appealing to eco-conscious consumers. Segmental Analysis: By Color (Transparent, Green, Amber)

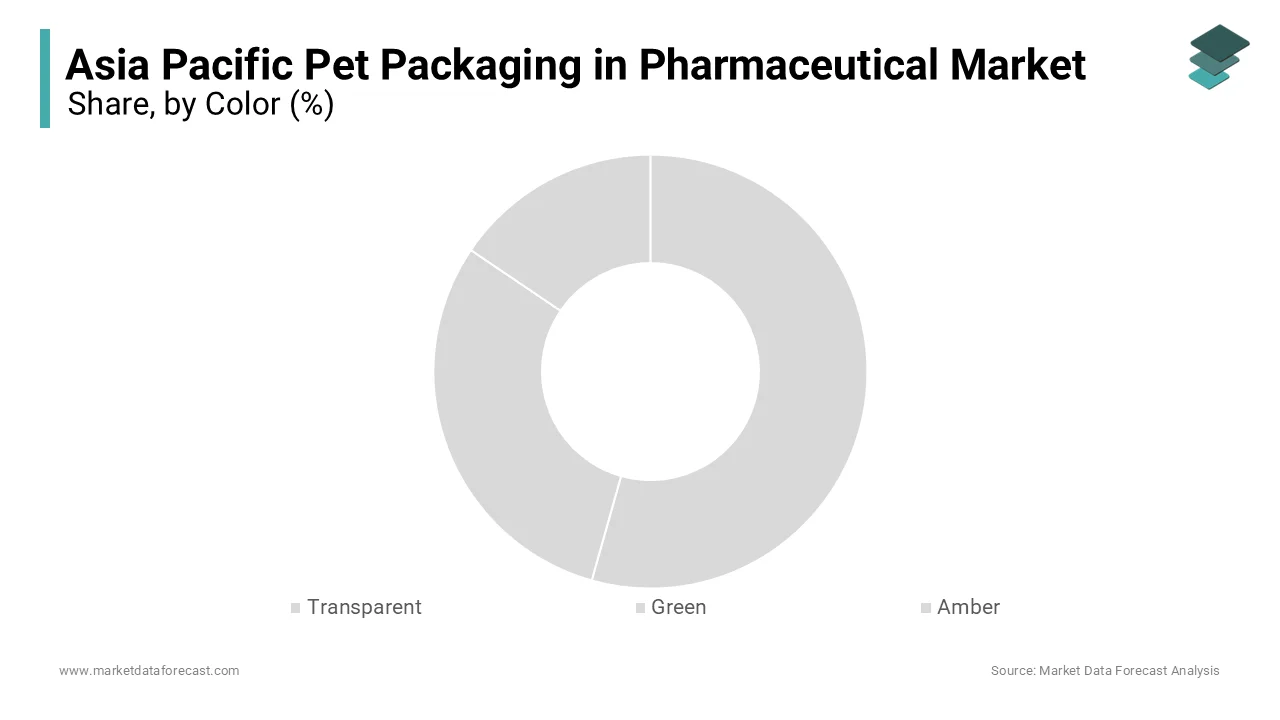

By Color Insights

Transparent packaging was accounted in holding 43.1% of the Asia Pacific Pet Packaging in Pharmaceutical market share in 2025. One major driver behind this trend is the rise of e-commerce platforms where product visibility plays a crucial role in decision-making. Additionally, transparency supports brand authenticity and ingredient storytelling for natural and organic pet food segments. In Japan, the Ministry of Agriculture, Forestry and Fisheries reported that 70% of surveyed pet owners preferred transparent packaging for high-end freeze-dried raw diets, citing freshness perception as a key factor.

The amber-colored packaging segment is likely to register a CAGR of 9.8% throughout the forecast period. This growth is driven by its functional advantages, particularly in protecting light-sensitive formulations such as liquid vitamins, probiotics, and CBD-infused pet oils.

A key growth driver is the increasing use of amber glass and plastic bottles in veterinary supplement packaging. Furthermore, amber packaging aligns with the clean-label movement, often associated with natural and holistic wellness brands.

REGIONAL ANALYSIS

China was the top performer in the Asia Pacific Pet Packaging in Pharmaceutical market with 31.3% of share in 2025. The country's dominance is supported by its booming pet care industry, rising disposable incomes, and expanding middle-class population that increasingly treats pets as family members. One of the main growth drivers is the rapid expansion of the domestic pet food manufacturing sector. Additionally, e-commerce has become a critical distribution channel, prompting brands to invest in visually appealing and logistics-friendly packaging. As per Alibaba Group, pet product sales on Tmall and Taobao grew by 28% in 2023, with custom-designed packaging playing a significant role in customer retention and repeat purchases.

India was positioned second with 14.3% of Asia Pacific Pet Packaging in Pharmaceutical market share in 2025. The country’s market expansion is fueled by a combination of rising pet ownership, urbanization, and increasing investment in organized pet care infrastructure.

Additionally, government initiatives promoting food safety and traceability have led to stricter labeling norms for pet food packaging. As per the Food Safety and Standards Authority of India (FSSAI), new regulations introduced in 2023 require detailed nutritional information and batch tracking, encouraging manufacturers to adopt digitally printed and compliant packaging solutions.

Japan is likely to showcase a healthy CAGR in the next coming years with its advanced packaging technologies and high consumer expectations, Japan remains a key innovator in sustainable and premium Pet Packaging in Pharmaceutical solutions. One of the key strengths of Japan’s market is its focus on functional and eco-friendly packaging. Moreover, Japanese pet owners exhibit a strong preference for convenience-driven packaging features such as zip-lock closures, tear notches, and portion-controlled packs. As per the Japan Pet Food Association, nearly 40% of surveyed consumers cited packaging ease-of-use as a decisive factor in repurchasing decisions.

South Korea Pet Packaging in Pharmaceutical market growth is driven by strong demand from premium pet brands and an expanding pet service ecosystem. The country’s compact urban lifestyle and digital-savvy consumers make it a hotspot for innovative and visually striking packaging designs.

Additionally, South Korean retailers are pushing for private label pet food lines with customized packaging to cater to niche dietary preferences such as grain-free, hypoallergenic, and senior pet formulas.

Australia was likely to grow with the distinguished by its strong regulatory environment and commitment to environmental responsibility. Though not the largest in terms of volume, Australia plays a pivotal role in setting sustainability benchmarks that influence broader regional packaging strategies. In addition, Australian pet owners show a strong preference for eco-conscious packaging choices. As per Roy Morgan Research, over 55% of surveyed pet owners indicated willingness to pay a premium for biodegradable or recycled-content packaging in 2023.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Senpet Polymers LLP, Total PET (Radico Khaitan Ltd), Ganesh PET, ALPHA GROUP, and Gerresheimer AG are the key players in the Asia Pacific Pet Packaging in Pharmaceutical market.

The competition in the Asia Pacific Pet Packaging in Pharmaceutical market is shaped by a mix of global packaging giants and agile regional manufacturers striving to capture market share through innovation, localization, and sustainability initiatives. As pet ownership rises and consumers become more discerning about product quality and packaging aesthetics, companies are under pressure to offer differentiated, functional, and environmentally responsible packaging solutions. The market sees intense rivalry not only in pricing but also in design, material sourcing, and performance features, particularly among flexible packaging providers. Regulatory changes related to food safety and recyclability are further influencing competitive strategies, pushing firms to invest heavily in R&D and compliance measures. Additionally, the growth of e-commerce and private label pet brands is altering traditional supplier-buyer dynamics, encouraging packaging companies to engage directly with retailers and online platforms.

TOP PLAYERS IN THE MARKET

Amcor plc

One of the leading players in the Asia Pacific Pet Packaging in Pharmaceutical market is Amcor plc, a global leader in responsible packaging solutions. The company has a strong presence across the region, offering sustainable and innovative packaging formats tailored for pet food and veterinary products. Amcor focuses on developing recyclable flexible packaging that aligns with evolving consumer expectations around environmental responsibility while ensuring product freshness and durability.

Sonoco Products Company

Another major player is Sonoco Products Company, known for its diverse portfolio of rigid and flexible packaging solutions designed for the pet care industry. In Asia Pacific, Sonoco has been actively expanding its footprint through localized production units and strategic partnerships with regional pet food manufacturers to meet rising demand for premium packaging formats such as resealable pouches and stackable containers.

Bemis Company Inc

Bemis Company Inc., now part of Amcor following its acquisition in 2019, continues to play a significant role in shaping the Pet Packaging in Pharmaceutical landscape in the region. Prioritizing advanced barrier films and stand-up pouches, Bemis brought expertise in high-performance flexible packaging that enhances shelf appeal and extends product life. Its legacy continues to influence Amcor’s innovation strategy in pet food and treat packaging across Asia Pacific.

TOP STRATEGIES USED BY KEY PLAYERS

A primary strategy adopted by leading companies in the Asia Pacific Pet Packaging in Pharmaceutical market is product innovation and customization by focusing on developing specialized packaging formats that cater to evolving consumer preferences such as convenience, sustainability, and brand differentiation. Another key approach is expanding regional manufacturing capabilities and forming strategic alliances with local pet food brands by allowing global players to better serve diverse markets and respond quickly to changing regulatory and logistical demands.

RECENT HAPPENINGS IN THE MARKET

- In March 2025, Amcor launched a new line of fully recyclable stand-up pouches specifically designed for premium pet food brands in Japan and South Korea, aiming to support regional sustainability commitments while enhancing shelf appeal and consumer convenience.

- In July 2023, Sonoco expanded its production facility in Shanghai to include a dedicated line for multi-layer flexible pet food packaging by reinforcing its ability to serve China’s growing demand for high-barrier, durable packaging solutions tailored for wet and dry pet foods.

- In November 2025, Huhtamaki, a major global packaging provider, entered into a joint venture with an Indian pet food manufacturer to co-develop compostable sachets for single-serve pet treats, aligning with the country’s increasing focus on plastic waste reduction and eco-conscious branding.

- In February 2023, UFlex established a new research and development center in Singapore focused on flexible Pet Packaging in Pharmaceutical innovations, including oxygen barriers, resealable closures, and digital printing technologies aimed at improving product longevity and visual appeal.

- In September 2025, Constantia Flexibles introduced a range of lightweight, tamper-evident aluminum-laminated pouches for pet supplements in Australia, targeting the growing demand for secure and visually appealing packaging formats in the premium wellness pet segment.

MARKET SEGMENTATION

This research report on the Asia Pacific pet packaging in pharmaceutical market has been segmented and sub-segmented based on the following categories.

By Product Type

- Tablet bottles

- Syrup bottles

- Dropper bottles

- Vials

- Mouthwash bottles

- Handwash bottles

- Hand sanitizer bottles

By Color

- Transparent

- Green

- Amber

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What are the key opportunities in the Asia Pacific PET packaging in pharmaceutical market?

The growing demand for cost-effective, lightweight, and shatter-resistant packaging in pharmaceuticals presents key growth opportunities, especially in emerging economies like India and China.

2. What trends are shaping the Asia Pacific PET packaging market?

Trends include increasing use of recyclable PET materials, rising adoption of dropper and vial packaging formats, and growing investments in pharmaceutical manufacturing across the region.

3. What challenges does the Asia Pacific PET packaging market face?

Key challenges include fluctuating raw material costs, regulatory compliance across different countries, and competition from alternative packaging materials like glass and HDPE.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com