Asia Pacific Pharmaceutical Market Research Report – Segmented By Molecule Type (Conventional Drugs, Biologics & Biosimilars), Product, Disease, Type, Route of Administration, Age Group, Distribution Channel, and Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2026 to 2034

Market Size, 2025

$379.54 BnMarket Estimate, 2026

$406.94 BnMarket Forecast, 2034

$710.78 BnCAGR, 2026–2034

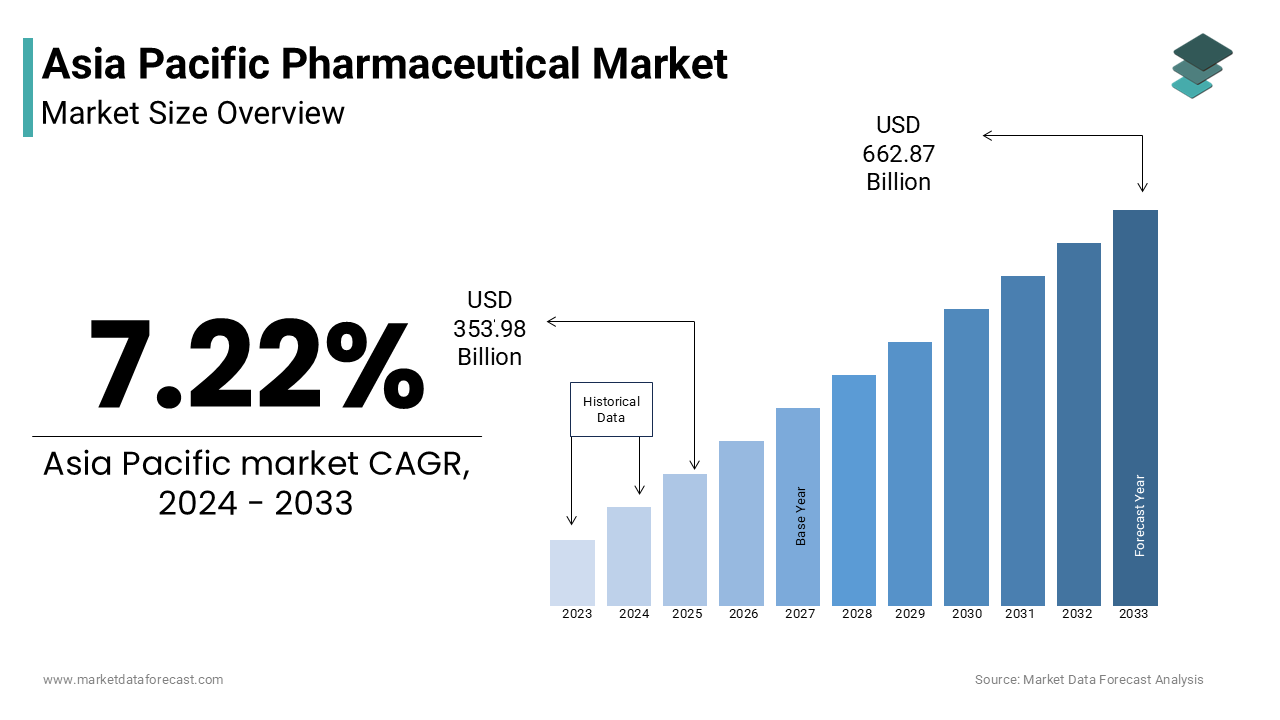

7.22%Asia Pacific Pharmaceutical Market Size

The Asia Pacific pharmaceutical market size was valued at USD 379.54 billion in 2025 and is anticipated to reach USD 406.94 billion in 2026 from USD 710.78 billion by 2034, growing at a CAGR of 7.22% during the forecast period from 2026 to 2034.

The pharmaceutical is emerged as a critical pillar of the global healthcare industry, which is driven by rapid urbanization, rising chronic disease prevalence, and increasing investments in drug development. The region encompasses a diverse landscape, ranging from highly regulated markets such as Japan and Australia to rapidly growing emerging economies like India, China, and Indonesia. Pharmaceuticals in this region include both generic and branded medicines by covering therapeutic areas such as oncology, cardiovascular diseases, diabetes, and infectious diseases. In response, governments have intensified efforts to improve healthcare access through policy reforms and public health programs. For instance, China’s National Healthcare Security Administration has expanded insurance coverage to millions, reducing out-of-pocket expenses for prescription drugs. Additionally, the rise of biopharmaceutical innovation is reshaping the market. As per the Organisation for Economic Co-operation and Development (OECD), several Asia Pacific nations are now investing heavily in biologics and biosimilars, with regulatory frameworks being updated to support faster approvals. This evolving ecosystem positions the Asia Pacific pharmaceutical sector not only as a major consumer market but also as a growing contributor to global drug discovery and manufacturing capabilities.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases

One of the primary drivers fueling the growth of the pharmaceutical market in the Asia Pacific is the escalating incidence of chronic diseases such as diabetes, hypertension, cardiovascular disorders, and cancer. According to the World Health Organization, non-communicable diseases (NCDs) account for nearly 60% of all deaths in the region, with diabetes alone affecting over 200 million individuals in China and India combined. In India, the Indian Council of Medical Research reported that the prevalence of type 2 diabetes has nearly doubled in the last decade, particularly in urban centers where lifestyle changes have led to sedentary habits and poor dietary choices. This surge has directly increased the demand for antidiabetic medications, cholesterol-lowering agents, and antihypertensives.

Expansion of Healthcare Infrastructure and Insurance Coverage

A significant factor contributing to the growth of the pharmaceutical market in the Asia Pacific is the expansion of healthcare infrastructure and the enhancement of insurance coverage across key economies. Governments in countries like Thailand, Malaysia, and the Philippines have implemented universal healthcare schemes aimed at improving access to essential medicines and treatments. In China, the National Healthcare Security Administration expanded its Essential Medicines List in 2023, adding over 90 new drugs in the fields of rare diseases and pediatric care, thereby enhancing affordability and availability. India has also made strides through initiatives like Ayushman Bharat, which provides free health insurance to over 500 million citizens.

MARKET RESTRAINTS

Regulatory Complexities and Stringent Approval Processes

A major restraint affecting the Asia Pacific pharmaceutical market is the varying levels of regulatory complexity and stringent approval processes across different countries. While some nations like Japan and Australia maintain highly structured and transparent regulatory frameworks, others such as Indonesia and Vietnam face challenges related to inconsistent policies, lengthy approval timelines, and lack of harmonization with international standards. According to the International Society for Pharmacoeconomics and Outcomes Research (ISPOR), the average time required for drug approval in certain Southeast Asian countries exceeds 18 months, compared to under 12 months in Japan and South Korea. In India, despite recent reforms by the Central Drugs Standard Control Organization (CDSCO), issues such as overlapping regulatory requirements and unpredictable pricing controls continue to hinder the timely introduction of novel pharmaceuticals. Until regulatory harmonization improves across the Asia Pacific, pharmaceutical companies will continue to face operational inefficiencies and delayed commercialization opportunities.

Counterfeit Medications and Supply Chain Vulnerabilities

Counterfeit medications pose a serious threat to the integrity and growth of the pharmaceutical market in the Asia Pacific. Despite regulatory advancements in developed markets like Japan and Australia, counterfeit drugs remain a persistent issue in countries such as India, Bangladesh, and parts of Southeast Asia. These fake medicines not only endanger patient lives but also erode trust in legitimate pharmaceutical brands. According to INTERPOL, counterfeit medicine seizures in the Asia Pacific region increased by 40% between 2021 and 2023, with online pharmacies serving as a major distribution channel. In addition, supply chain vulnerabilities such as inadequate cold chain storage, weak logistics networks, and limited traceability further exacerbate the problem. The ASEAN Common Technical Dossier (ACTD) initiative aims to standardize documentation and streamline drug registration, yet implementation remains uneven across member states.

MARKET OPPORTUNITIES

Growth of Biopharmaceutical and Biosimilar Markets

A major opportunity emerging in the Asia Pacific pharmaceutical market is the expanding biopharmaceutical and biosimilar sectors. Several countries in the region are accelerating regulatory reforms and investing in domestic manufacturing capabilities with rising demand for targeted therapies and cost-effective alternatives to patented biologics. According to the Organisation for Economic Co-operation and Development (OECD), China, South Korea, and India are among the fastest-growing biosimilar markets globally. South Korea, recognized for its strong biotechnology infrastructure, has positioned itself as a global exporter of biosimilars. Meanwhile, India’s Department of Biotechnology has launched national missions to boost indigenous biosimilar production.

Digital Health and AI-Driven Drug Discovery

The integration of digital health technologies and artificial intelligence (AI) into drug discovery and development is prompting new opportunities for the Asia Pacific pharmaceutical market growth. As traditional R&D cycles become increasingly costly and time-consuming, pharmaceutical firms are leveraging AI-driven platforms to accelerate molecule identification, clinical trials, and personalized medicine approaches. In India, AI-based platforms such as Qure.ai and SigTuple are being deployed to enhance diagnostics and drug repurposing efforts. Moreover, telemedicine and digital therapeutics are gaining traction across the region, influencing pharmaceutical companies to develop companion digital tools for treatment adherence and outcome tracking.

MARKET CHALLENGES

Pricing Pressures and Generic Competition

The intensifying pricing pressure due to aggressive generic competition and government-mandated price controls is likely to pose huge challenge for the growth of the Asia Pacific pharmaceutical market. Many governments in the region prioritize affordability and accessibility, often implementing price caps on essential medicines, which limits profitability for both multinational and domestic manufacturers. According to the Asian Development Bank, India’s National Pharmaceutical Pricing Authority (NPPA) imposed price reductions on over 1,200 drugs in 2023, impacting revenues for major pharmaceutical players. Japan, while maintaining a relatively stable pricing environment, has introduced periodic downward revisions based on comparative effectiveness assessments, affecting returns on newly launched drugs. These trends are compelling pharmaceutical firms to reassess their product portfolios, shift focus toward niche therapeutic areas, and invest in high-value specialty medicines to sustain profitability amidst relentless pricing pressures.

Intellectual Property Protection and Patent Expiry Cycles

Intellectual property (IP) protection remains a significant challenge for pharmaceutical firms operating in the Asia Pacific, particularly in markets where patent enforcement mechanisms are weak or inconsistently applied. Although developed economies like Japan and Australia maintain robust IP regimes, emerging markets such as India, Indonesia, and Vietnam struggle with effective enforcement of patent rights. According to the World Intellectual Property Organization (WIPO), disputes over patent validity and compulsory licensing have increased in recent years, particularly concerning life-saving drugs. Furthermore, the wave of patent expirations affecting blockbuster drugs has intensified competition from generics and biosimilars. The U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have approved several follow-on versions of originator drugs, which are then imported or locally manufactured in the Asia Pacific.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.22% |

| Segments Covered | By Molecule Type, Product, Disease, Type, Route of Administration, Age Group, Distribution Channel and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, the Philippines, Indonesia, Singapore, and the rest of Asia Pacific |

| Market Leaders Profiled | Pfizer, Novartis, Roche, Johnson & Johnson, Merck & Co., AstraZeneca, Sanofi, GSK, Sun Pharmaceutical Industries, Dr. Reddy’s Laboratories, Cipla, Aurobindo Pharma, Takeda Pharmaceutical Company, Daiichi Sankyo, Eisai Co., Ltd., Sumitomo Pharma, Samsung Biologics, WuXi Biologics, Catalent, Jubilant Life Sciences, Kalbe Farma, and Unilab. |

SEGMENTAL ANALYSIS

By Molecule Type Insights

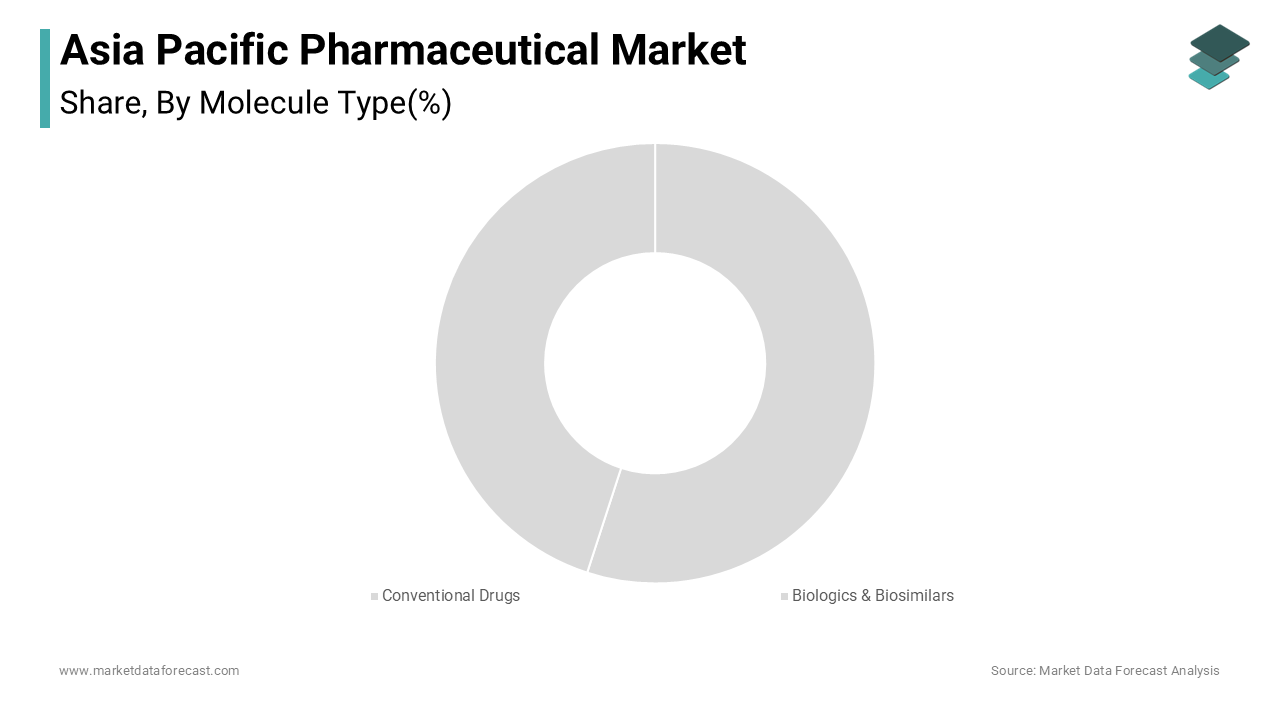

The conventional segment was the largest and held a dominant share of the Asia Pacific pharmaceutical market in 2025. In India, the Central Drugs Standard Control Organization (CDSCO) reported that over 90% of prescribed medicines in the country are small molecule generics, covering essential therapeutic areas such as cardiovascular diseases, diabetes, and respiratory illnesses. The high prevalence of non-communicable diseases across Southeast Asia has further reinforced demand for cost-effective treatments.

The biologics and biosimilars segment is likely to grow with an expected CAGR of 14.3% in the next coming years. According to the Organisation for Economic Co-operation and Development (OECD), China and South Korea have emerged as global leaders in biosimilar development, with domestic companies securing international approvals and expanding exports. Japan has also accelerated its biosimilar adoption through favorable pricing policies and physician education programs. Additionally, India is emerging as a major biosimilar manufacturing hub due to its skilled workforce and cost advantages.

By Product Type Insights

The generics segment was accounted in holding a prominent share of the Asia Pacific pharmaceutical market in 2025. India remains the cornerstone of this segment, producing over 20% of the world’s generic medicines, according to the Indian Pharmaceutical Alliance. In China, the National Healthcare Security Administration implemented volume-based procurement policies that favored generic manufacturers, resulting in increased market penetration. Similarly, Thailand and Malaysia have expanded their use of locally produced generics under national health insurance schemes.

The branded pharmaceuticals segment is likely to grow with a CAGR of 9.8% during the forecast period. According to the Asian Development Bank, per capita healthcare expenditure in Southeast Asia has risen by over 6% annually since 2018, allowing consumers to opt for premium branded medicines rather than low-cost alternatives. Japan remains a key contributor to this trend, with a highly regulated market that prioritizes quality and innovation. South Korea is also witnessing a shift toward branded medicines, supported by an aging population and higher insurance coverage.

By Disease Indication Insights

The cardiovascular diseases (CVDs) segment held 18.3% of the Asia Pacific pharmaceutical market share in 2024. According to the World Heart Federation, CVDs account for nearly 30% of all deaths in the Asia Pacific region, with India alone reporting over 2.8 million annual cardiovascular-related fatalities. In China, the Chinese Society of Cardiology estimated that over 330 million individuals suffer from some form of cardiovascular disorder, making it the leading cause of mortality in the country. Moreover, in Australia, the National Heart Foundation recorded a steady rise in prescriptions for heart failure and atrial fibrillation treatments, reflecting an aging population with complex comorbidities.

The cancer segment is expected to register a CAGR of 16.4% from 2025 to 2033. According to the International Agency for Research on Cancer (IARC), the Asia Pacific region accounts for nearly 50% of global cancer cases, with China, India, and Japan experiencing sharp increases in breast, lung, colorectal, and gastric cancers. China has witnessed a surge in demand for advanced therapies such as PD-1/PD-L1 inhibitors, with domestic biopharma firms like CSPC Pharmaceutical Group and Hengrui Medicine launching multiple oncology drugs. In India, the Indian Cancer Society noted that awareness campaigns and early screening initiatives have led to higher diagnosis rates, boosting prescription volumes.

REGIONAL ANALYSIS

China Pharmaceutical Market Insights

China was the top performer in the Asia Pacific pharmaceutical market with 30.2% of the share in 2025. According to the National Medical Products Administration, China approved over 60 new drugs in 2023, including several breakthrough therapies in oncology and rare diseases. Additionally, China’s biopharmaceutical sector has seen significant growth, with domestic firms such as CSPC Pharmaceutical Group and BeiGene playing a pivotal role in developing and exporting biosimilars and novel therapeutics.

India Pharmaceutical Market Insights

India was positioned second in the Asia Pacific pharmaceutical market by holding 18.3%the of the share in 2025. According to the Indian Pharmaceutical Alliance, India exported pharmaceutical products worth USD 24 billion in 2023, with over 50% of these exports going to regulated markets such as the U.S., Europe, and Africa. In addition, India’s domestic pharmaceutical market is growing rapidly, driven by government initiatives like Ayushman Bharat, which provides health insurance to millions of citizens.

Japan Pharmaceutical Market Insights

Japan pharmaceutical market is likely to grow with the significant CAGR during the forecast period. According to the Ministry of Health, Labour and Welfare, Japan spends nearly 11% of its GDP on healthcare, supporting the development and adoption of high-value medicines. The Pharmaceuticals and Medical Devices Agency (PMDA) has streamlined drug approval processes, allowing faster access to novel therapies, particularly in oncology and regenerative medicine. The Japanese Pharmacopoeia reported that the country launched over 15 new drugs in 2023, many of which were developed indigenously. Companies like Takeda Pharmaceutical and Daiichi Sankyo are investing heavily in next-generation therapies, including gene therapy and antibody-drug conjugates.

South Korea Pharmaceutical Market Insights

South Korea pharmaceutical market growth is likely to grow with prominent opportunities in the next coming years. According to the Ministry of Food and Drug Safety, South Korean biopharma exports surpassed USD 2.3 billion in 2023, with biosimilars being a major driver. Companies like Samsung Bioepis and Celltrion have secured multiple global approvals, positioning the country as a key exporter of biosimilar monoclonal antibodies. In addition, the Korean government has been actively promoting pharmaceutical innovation through tax incentives and public-private partnerships.

Australia Pharmaceutical Market Insights

Australia pharmaceutical market growth is to grow steadily in the next coming years. According to the Therapeutic Goods Administration (TGA), Australia approved 42 new prescription medicines in 2023, including several breakthrough therapies for rare diseases and oncology. The Pharmaceutical Benefits Scheme (PBS) played a crucial role in making these treatments accessible to the general population, subsidizing over 90% of prescribed medicines.

COMPETITIVE LANDSCAPE

The Asia Pacific pharmaceutical market is highly competitive, characterized by a mix of multinational corporations, well-established regional players, and a rapidly growing number of domestic innovators and generic manufacturers. This dynamic landscape fosters intense rivalry across various segments, from branded drugs and biosimilars to over-the-counter medications and specialty therapeutics. Multinational pharmaceutical giants leverage their global expertise and deep R&D pipelines to maintain a foothold, while local companies capitalize on cost advantages, regulatory familiarity, and agile operations to capture market share.

In addition, the rise of biotechnology and biosimilars has intensified competition, especially in countries like South Korea, China, and India, where governments actively support domestic innovation. Meanwhile, pricing pressures due to government-led procurement policies and increasing preference for generics further shape the market dynamics.

KEY MARKET PLAYERS

The key market players in the Asia Pacific Pharmaceutical Market include

- Pfizer

- Novartis

- Roche

- Johnson & Johnson

- Merck & Co.

- AstraZeneca

- Sanofi

- GSK

- Sun Pharmaceutical Industries

- Dr. Reddy’s Laboratories

- Cipla

- Aurobindo Pharma

- Takeda Pharmaceutical Company

- Daiichi Sankyo

- Eisai Co., Ltd.

- Sumitomo Pharma

- Samsung Biologics

- WuXi Biologics

- Catalent

- Jubilant Life Sciences

- Kalbe Farma

- Unilab

Top Players in the Asia Pacific Pharmaceutical Market

Takeda Pharmaceutical Company (Japan)

Takeda is a leading pharmaceutical company headquartered in Japan and a major contributor to both the Asia Pacific and global pharmaceutical markets. The company has a strong presence across multiple therapeutic areas, including oncology, gastroenterology, and rare diseases. Takeda's commitment to innovation, robust R&D capabilities, and strategic acquisitions have positioned it as a key player in developing novel therapies. Its global footprint extends beyond Japan into emerging markets in Southeast Asia and India, where it collaborates with local partners to enhance drug accessibility and expand its market reach.

Dr. Reddy’s Laboratories (India)

Dr. Reddy’s Laboratories is one of India’s most prominent pharmaceutical companies, known for its expertise in generics, biosimilars, and complex formulations. It plays a vital role in supplying affordable medicines to both domestic and international markets. The company has consistently invested in expanding its manufacturing capabilities and diversifying its product portfolio to include niche therapeutic areas. In the Asia Pacific region, Dr. Reddy’s has strengthened its brand through partnerships, regulatory compliance, and a focus on sustainable healthcare solutions, which is contributing significantly to global medicine access.

Samsung Biepis (South Korea)

Samsung Bioepis is a biopharmaceutical leader specializing in biosimilars and has emerged as a key force in the Asia Pacific pharmaceutical market. A joint venture between Samsung Biologics and Biogen, the company focuses on developing high-quality biosimilar versions of blockbuster biologics. With a strong pipeline targeting autoimmune diseases and oncology, Samsung Bioepis has expanded its influence globally by securing approvals in both developed and emerging markets. In the Asia Pacific, the company supports regional growth through advanced manufacturing infrastructure and strategic collaborations.

Top Strategies Used by Key Market Participants

One major strategy employed by key players in the Asia Pacific pharmaceutical market is expanding local manufacturing and supply chain capabilities, allowing companies to reduce costs, ensure faster delivery, and comply with regional regulations. Many firms are setting up or upgrading production facilities within the region to cater to growing demand and mitigate global supply disruptions.

Another critical approach is investing in research and development for targeted therapies and biologics in areas such as oncology, immunology, and rare diseases. Companies are forming strategic alliances with academic institutions and biotech startups to accelerate drug discovery and bring innovative treatments to market more efficiently.

RECENT MARKET DEVELOPMENTS

- In February 2024, Takeda Pharmaceutical established a new R&D center in Singapore, focusing on cell and gene therapy innovations tailored to the Asia Pacific population, which is reinforcing its dominance in next-generation therapeutics.

- In May 2024, Dr. Reddy’s Laboratories entered into a strategic partnership with a Vietnamese pharmaceutical firm, which is expanding its distribution network and enhancing access to essential generic medicines in Indochina.

- In July 2024, Samsung Bioepis announced a joint venture with an Australian biotech startup, aiming to co-develop biosimilar candidates for autoimmune diseases by strengthening its regional pipeline and commercial reach.

- In September 2024, Sun Pharmaceutical Industries acquired a niche dermatology-focused company in Thailand by broadening its specialty product offerings and reinforcing its presence in Southeast Asia.

- In November 2024, Cipla launched a dedicated digital health platform in India, which is integrating AI-powered diagnostics and medication adherence tools to improve patient outcomes and enhance engagement with healthcare professionals.

MARKET SEGMENTATION

This research report on the Asia Pacific pharmaceutical market is segmented and sub-segmented into the following categories.

By Molecule Type

- Conventional Drugs

- Biologics & Biosimilars

- Monoclonal Antibodies

- Vaccines

- Cell & Gene Therapy

- Others

By Product

- Generics

- Branded

By Disease

- Cardiovascular diseases

- Cancer

- Diabetes

- Infectious diseases

- Neurological disorders

- Respiratory diseases

- Autoimmune diseases

- Mental health disorders

- Gastrointestinal disorders

- Women’s health diseases

- Genetic and rare genetic diseases

- Dermatological conditions

- Obesity

- Renal diseases

- Liver conditions

- Hematological disorders

- Eye conditions

- Infertility conditions

- Endocrine disorders

- Allergies

- Others

By Type

- Prescription

- OTC

By Route of Administration

- Oral

- Tablets

- Capsules

- Suspensions

- Other

- Topical

- Parenteral

- Intravenous

- Intramuscular

- Inhalations

- Other

By Age Group

- Children & Adolescents

- Adults

- Geriatric

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What factors are driving the growth of the pharmaceutical market in Asia Pacific?

Key drivers include rising healthcare expenditure, a growing aging population, increasing prevalence of chronic diseases, expanding generic drug production, and supportive government policies in developing countries

What role does India play in the Asia Pacific pharmaceutical sector?

India is a global leader in the production of generic drugs and APIs, with companies like Sun Pharma, Dr. Reddy’s, Cipla, and Aurobindo dominating exports and manufacturing

What are the current trends in the Asia Pacific Pharmaceutical Market?

Emerging trends include increased focus on biosimilars, digital health integration, growth in telemedicine, contract manufacturing growth, and rising demand for personalized medicine.

What challenges does the market face?

Challenges include regulatory variations across countries, intellectual property issues, pricing pressures, and the need for strong supply chain infrastructure in less developed markets.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com