- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

APAC Pharmaceutical Membrane Filtration Market Size

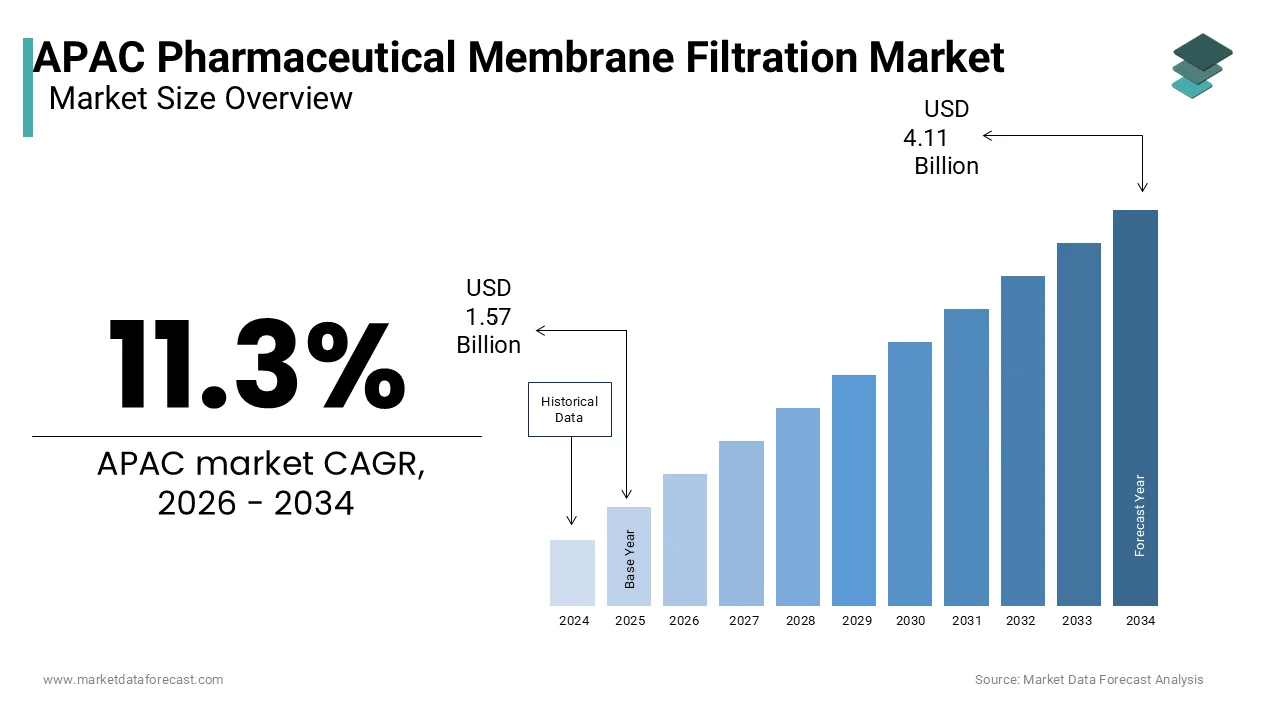

The APAC pharmaceutical membrane filtration market was valued at USD 1.57 billion in 2025 and increased to USD 1.75 billion in 2026. The market is projected to reach USD 4.11 billion by 2034, growing at a CAGR of 11.3% from 2026 to 2034.

Pharmaceutical membrane filtration is a critical, pressure-driven separation technique using thin, microporous materials to remove bacteria, microorganisms, and particulates from liquids to ensure sterility and purity. These critical components, engineered from advanced polymers such as polyethersulfone, polyvinylidene fluoride, and regenerated cellulose, serve as the backbone for sterile filtration, virus removal, and buffer exchange in the production of biologics, vaccines, and small molecule drugs. The region is currently undergoing a transformative shift toward high-value biopharmaceutical manufacturing, driven by robust government initiatives and increasing healthcare expenditure. According to reports from the World Health Organization, healthcare spending across the Asia-Pacific region is increasing steadily, which is driving significant investments in modern processing facilities and health infrastructure. The regulatory landscape is also maturing, with agencies like the National Medical Products Administration in China and the Pharmaceuticals and Medical Devices Agency in Japan aligning their Good Manufacturing Practices with global standards to facilitate exports. Research indicates that the Asia-Pacific region now holds a dominant share of global vaccine production capacity, which requires strict filtration steps to maintain high product safety standards. Furthermore, the rise of contract development and manufacturing organizations in India and South Korea is creating a fertile environment for membrane integration. As per various sources, the emphasis on aseptic processing has intensified, making membrane filtration an indispensable element in ensuring patient safety and therapeutic efficacy across the rapidly evolving pharmaceutical landscape of the Asia Pacific.

MARKET DRIVERS

Exponential Growth in Biologics and Biosimilar Production

The explosive expansion of biologics and biosimilar manufacturing across the region serves as a key factor for the surging demand for advanced membrane filtration systems and the overall growth of the APAC pharmaceutical membrane filtration market. Unlike traditional small molecule drugs, biological products such as monoclonal antibodies, recombinant proteins, and cell therapies require highly sophisticated purification processes to remove host cell proteins, DNA, and viruses while preserving structural integrity. According to studies, the number of biopharmaceutical facilities in Asia has grown significantly over the last several years, with China and India leading a rapid expansion in manufacturing capacity. These facilities rely heavily on tangential flow filtration and depth filtration membranes to achieve the purity levels mandated by international regulatory bodies. Research shows that China’s domestic market for biosimilars is expanding at a rapid annual rate, fueled by government initiatives designed to lower healthcare costs by prioritizing locally developed medical alternatives. This surge in production volume directly correlates with an escalated consumption of single-use membrane capsules and cassettes, which offer flexibility and minimized cross-contamination risks. Furthermore, the complexity of biological molecules necessitates precise pore size distributions and specific surface chemistries that only advanced membrane technologies can provide. Sources indicate that a vast majority of new bioprocessing lines in the Asia-Pacific region are adopting single-use membrane systems to reduce the time required to bring new drugs to market. The strategic focus on self-sufficiency in critical therapeutics ensures a sustained and growing demand for high-performance filtration solutions tailored to the nuances of biological manufacturing.

Stringent Regulatory Harmonization and Export Orientation

The rigorous alignment of Asia Pacific regulatory frameworks with international Good Manufacturing Practices acts as a significant driver for the uptake of premium membrane filtration technologies within the APAC pharmaceutical membrane filtration market. Regulatory agencies across the region, including the Therapeutic Goods Administration in Australia, the Ministry of Food and Drug Safety in South Korea, and the Health Sciences Authority in Singapore, have progressively tightened their requirements for sterility assurance and viral clearance in pharmaceutical production. As per guidelines issued by the International Council for Harmonisation, member states in the region are increasingly adopting standards comparable to those of the United States and European Union to facilitate drug exports and ensure public safety. This regulatory convergence compels pharmaceutical manufacturers to upgrade their existing filtration infrastructure, replacing older, less reliable methods with validated membrane systems that offer consistent performance and documented integrity. According to quality standards promoted by the World Health Organization, manufacturing facilities that implement advanced filtration technologies experience fewer issues with batch contamination and improved overall product quality. The necessity for comprehensive validation protocols, including bubble point testing and diffusion tests, further favors advanced membrane solutions that come with extensive supplier documentation and support. Studies show that the financial consequences of product recalls and facility closures have increased, leading companies to invest more heavily in advanced filtration systems to ensure continuous regulatory compliance. Moreover, the push for data integrity and traceability in manufacturing processes encourages the adoption of smart filtration systems capable of real-time monitoring. This regulatory pressure creates a mandatory market environment where high-quality membrane filtration is not merely an option but a fundamental prerequisite for operational continuity and access to lucrative global export markets.

MARKET RESTRAINTS

High Capital Investment and Operational Cost Barriers

The substantial capital investment required for acquiring and maintaining these advanced systems poses a significant barrier to the APAC pharmaceutical membrane filtration market growth. This issue is particularly critical for small and medium-sized enterprises in developing Asia Pacific nations. The initial cost of high-performance membrane modules, along with the associated hardware such as skids, pumps, and sensors, can be prohibitive for emerging pharmaceutical companies operating on thin margins. The Asian Development Bank indicates that trade costs and non-tariff measures in Southeast Asian nations like Vietnam and Indonesia remain higher than in advanced regional economies, which can elevate the landed cost of imported industrial technologies. This financial burden forces many local manufacturers to delay critical upgrades or opt for lower-cost, less efficient alternatives that may compromise product quality and regulatory compliance. Research suggests that while small-scale pharmaceutical producers face financial pressures, the primary challenges to scaling infrastructure are often regulatory complexity and talent shortages rather than a widespread postponement of capital projects. Furthermore, the ongoing operational costs, including the frequent replacement of single-use membranes and the energy required for high-pressure filtration processes, add to the financial strain. The reliance on imported raw materials for membrane production also exposes buyers to currency fluctuations and supply chain disruptions, which can suddenly escalate operational expenses. Additionally, the lack of localized financing options for technology upgrades limits the ability of smaller players to compete with multinational corporations. Consequently, high entry and operational costs act as a potent brake on market penetration, preventing widespread adoption of cutting-edge filtration technologies across the diverse economic landscape ofthe Asia Pacific.

Scarcity of Skilled Technical Workforce and Expertise

The acute shortage of highly skilled technical personnel capable of operating and maintaining complex filtration systems is a critical constraint hindering the optimal utilization and expansion of the APAC pharmaceutical membrane filtration market. The successful implementation of advanced membrane technologies requires specialized knowledge in fluid dynamics, membrane chemistry, process validation, and troubleshooting, areas where the regional workforce often lacks sufficient depth. The International Labour Organization highlights a notable regional gap in general STEM education and vocational training, which industry experts identify as a key factor contributing to the shortage of skilled labor in the biopharmaceutical manufacturing sector. This skills deficit leads to suboptimal operation of filtration equipment, resulting in premature membrane fouling, reduced throughput, and increased downtime. Case studies from major pharmaceutical firms in the region indicate that a significant portion of process inefficienciesise attributed to operator error and manual handling inconsistency, driving the adoption of automated filtration systems. The lack of localized training programs and certified expertise further exacerbates the issue, forcing companies to rely on expensive expatriate consultants or extensive overseas training for their staff. Research emphasizes that the shortage of qualified engineers and technicians is a primary bottleneck in scaling up bioprocessing operations. Additionally, the rapid evolution of filtration technologies means that continuous professional development is essential, yet resources for such training are often limited. This human capital challenge restricts the ability of manufacturers to fully leverage the capabilities of modern membrane systems, thereby slowing down the overall adoption rate and market penetration of advanced filtration solutions across the region.

MARKET OPPORTUNITIES

Surge in Contract Manufacturing and Outsourcing Trends

The accelerating trend toward contract development and manufacturing organizations offers a transformative opportunity for the Asia Pacific Pharmaceutical Membrane Filtration Market. As global pharmaceutical giants seek to diversify their supply chains and reduce production costs, they are increasingly turning to Asia Pacific CDMOs for the manufacturing of generic drugs, biosimilars, and sterile formulations. According to industry analysis, the CDMO sector in the Asia-Pacific is projected to expand significantly over the next decade, with certain major markets growing at double-digit annual rates. This trend is driven by competitive labor costs, supportive government policies, and strong intellectual property protections in leading hubs like Singapore and India. These contract manufacturers must adhere to the highest international quality standards, necessitating the installation of robust and versatile membrane filtration systems to handle diverse client portfolios. As per sources, there is a substantial influx of foreign investment into local manufacturing hubs, which has triggered a major surge in the construction of new cleanroom facilities equipped with advanced filtration technologies. The flexibility of single-use membrane systems makes them particularly attractive for CDMOs that need to switch between different products rapidly without the risk of cross-contamination. Furthermore, the establishment of regional centers of excellence for biologics production creates a sustained demand for high-performance filtration consumables. Industry observers note that CDMOs are often early adopters of new technologies to maintain their competitive edge, thereby driving innovation in the membrane sector. This shift toward outsourcing not only expands the customer base for membrane suppliers but also fosters a culture of quality and efficiency that permeates the broader regional pharmaceutical landscape, offering lucrative growth avenues for technology providers.

Government Initiatives for Local Vaccine and Essential Medicine Production

Strategic government initiatives aimed at achieving self-sufficiency in vaccine and essential medicine production provide a lucrative avenue for growth in the APAC pharmaceutical membrane filtration market. In the wake of global health crises, several Asia Pacific governments have launched ambitious programs to bolster domestic manufacturing capabilities and reduce reliance on imports. Announcements from Chinese science and technology authorities confirm that significant funding has been dedicated to increasing the production capacity of both state-owned and private laboratories, with a particular emphasis on vaccine development and final-stage processing. These expansions inherently require advanced membrane filtration systems for virus removal, buffer exchange, and sterile filtration to meet international potency and safety standards. The World Health Organization Regional Office for South-East Asia emphasizes that regional collaboration is vital for technology transfer, facilitating the local production of complex biological medicines through the adoption of modern manufacturing processes. The push for localizing the supply chain for critical care medications also drives demand for reliable filtration solutions in small molecule manufacturing. The ASEAN Pharmaceutical Federationhighlightst that public-private partnerships are facilitating the acquisition of modern equipment, including high-capacity membrane skids. Furthermore, regulatory incentives for locally produced vaccines encourage private sector participation, further amplifying the need for filtration infrastructure. This concerted political will and financial backing create a stable and growing market segment for membrane suppliers who can align their offerings with national health security objectives and contribute to the region's resilience against future pandemics.

MARKET CHALLENGES

Complex Supply Chain Logistics and Import Dependencies

Complex supply chain logistics and a heavy dependence on imported raw materials and finished productlimitts the growth of the APAC pharmaceutical membrane filtration market. A significant portion of high-performance membrane polymers and specialized filtration hardware is sourced from North America, Europe, and Japan, making the regional market vulnerable to global shipping disruptions and customs delays. A study indicates that transit times for imported goods into Asia-Pacific ports vary significantly, with administrative hurdles and infrastructure limitations in certain developing nations occasionally leading to extended delays that disrupt the supply of critical industrial components. These logistical uncertainties complicate inventory management for manufacturers who rely on just-in-time delivery models for critical filtration consumables. Sources emphasize that gaps in specialized transport infrastructure in certain areas can pose risks to the integrity of sensitive pharmaceutical supplies, necessitating more robust handling protocols during transit. The reliance on imports also exposes buyers to fluctuating freight costs and potential trade barriers, which can suddenly escalate operational expenses. Additionally, the fragmentation of customs regulations across different Asia Pacific countries creates a cumbersome environment for distributors attempting to serve the entire region efficiently. Case studies from major filtration suppliers indicate that supply chain interruptions have led to production stoppages in several facilities, highlighting the fragility of the current logistics network. Significant improvements in regional infrastructure and the harmonization of trade procedures are required. Until these are achieved, supply chain volatility will remain a formidable obstacle to market stability and growth.

High Operational Costs and Maintenance Complexity

High operational costs associated with the maintenance and validation of advanced membrane filtration systems are also an impediment for the pharmaceutical manufacturers within the APAC pharmaceutical membrane filtration market. The deployment of sophisticated filtration technologies requires not only substantial initial capital investment but also ongoing expenditures for cleaning agents, integrity testing equipment, and skilled labor. Sources suggest that the long-term operational costs for advanced manufacturing systems in certain regional markets are influenced by the availability of local technical support and the reliance on imported components for maintenance. The complexity of maintaining sterile conditions and performing regular validation tests adds to the operational burden, particularly for smaller manufacturers with limited resources. Research shows that the frequency of filter replacement due to damage or build-up is often higher in areas with poor water quality, which significantly increases the cost of necessary consumables. Additionally, the lack of standardized protocols for maintenance across different facilities leads to inefficiencies and increased downtime. Surveys reveal that unplanned maintenance events account for a significant portion of production losses in the regional biopharmaceutical sector. The financial strain of adhering to rigorous validation requirements while managing high operational expenses discourages some players from upgrading to newer, more efficient technologies. This economic barrier limits the widespread adoption of advanced filtration solutions and hampers the overall modernization of the pharmaceutical manufacturing landscape inthe Asia Pacific, requiring targeted interventions to alleviate cost pressures.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Technique, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Merck KGaA (Germany), General Healthcare Company (U.K.), Pall Corporation (U.S.), Sartorius Stedim Biotech Group (France), Alfa Laval (Sweden), Graver Technologies, LLC (U.S.), Koch Membrane Systems Inc. (U.S.), GEA Group (Germany), and Novasep (U.S.)

|

SEGMENTAL ANALYSIS

By Product Insights

The Polyvinylidene Fluoride (PVDF) membrane segment dominated the APAC pharmaceutical membrane filtration market and accounted for a 42.5% share in 2025. This dominance of the segment is driven by the material's exceptional chemical resistance and thermal stability, which are critical for the harsh cleaning and sterilization protocols required in modern biopharmaceutical manufacturing across the region. A key force behind for the dominance of PVDF membranes is their unparalleled ability to withstand aggressive cleaning agents and repeated sterilization cycles without degradation, a necessity for complying with stringent Good Manufacturing Practices in Asia Pacific. Unlike other polymers, PVDF exhibits high resistance to strong acids, bases, and organic solvents, allowing manufacturers to use rigorous Clean-in-Place procedures that ensure absolute sterility. The material can endure steam sterilization at temperatures up to 140 degrees Celsius, which is essential for eliminating endotoxins and viruses in vaccine production. As per studies, filtration systems must demonstrate consistent integrity after multiple autoclave cycles, a standard that PVDF meets more reliably than cellulose-based alternatives. Furthermore, the hydrophobic nature of PVDF makes it ideal for venting applications in fermenters and storage tanks, preventing microbial ingress while allowing gas exchange. The operational reliability reduces the risk of batch failures and product loss, making PVDF the preferred choice for high-value biological manufacturing across the continent. PVDF membranes dominate the market due to their low protein binding characteristics and broad compatibility with diverse biological fluids, which is crucial for maximizing yield in the production of monoclonal antibodies and recombinant proteins. In the Asia Pacific market, where the biosimilar sector is expanding rapidly, maintaining high product recovery rates is economically vital. According to research, PVDF membranes exhibit significantly lower nonspecific adsorption of proteins compared to nylon or uncoated cellulose acetate, resulting in yield improvements of up to 18 percent in critical purification steps. This efficiency is particularly important for expensive biologic drugs where even minor losses translate to substantial financial impacts. The material's inherent stability also ensures that it does not leach extractables into the product stream, a key concern for regulatory compliance. Additionally, the versatility of PVDF allows it to be used in both aqueous and organic solvent applications, providing a unified solution for complex multi-step processes. This adaptability supports the growing trend of integrated continuous manufacturing in the region, further solidifying the segment's market leadership.

The Nylon membrane segment is expected to exhibit a noteworthy CAGR of 9.8% from 2026 to 2034 owing to its unique affinity for polar solvents and its increasing application in specific analytical and preparative processes within the pharmaceutical sector. Moreover, the accelerated growth of this segment is primarily driven by its superior performance in filtering polar solvents and its widespread adoption in quality control laboratories across Asia Pacific. Nylon membranes possess excellent wettability and high tensile strength, making them ideal for sample preparation and sterilization of solvent-based drug formulations that other materials cannot handle effectively. The material's ability to retain fine particulates without significant flow restriction makes it indispensable for High Performance Liquid Chromatography sample filtration, a routine procedure in drug development. Furthermore, Nylon's compatibility with a wide pH range allows it to be used in diverse extraction processes for active pharmaceutical ingredients derived from natural sources, a growing niche in Asia Pacific. The cost-effectiveness of Nylon compared to fluoropolymer alternatives also appeals to mid-sized pharmaceutical companies looking to optimize operational expenses without compromising quality. This combination of technical superiority in specific applications and economic viability propels the Nylon segment forward at a remarkable pace. The booming generic drug sector in Asia Pacific serves as a significant catalyst for the rapid adoption of Nylon membranes in various formulation and clarification steps. Generic manufacturers often deal with a wide array of chemical entities that require robust filtration solutions capable of handling diverse solvent systems used in crystallization and precipitation processes. Nylon membranes are increasingly preferred for clarifying fermentation broths and filtering intermediate solutions where high mechanical strength is required to withstand pressure fluctuations. The material's hydrophilic nature allows for immediate wetting without the need for pre-treatment solvents, streamlining workflow in high-volume production environments. Additionally, the rise of fixed-dose combination drugs, which often involve complex solvent mixtures, further boosts the demand for Nylon's broad chemical compatibility. The ability of Nylon to provide consistent retention ratings across different batches ensures product uniformity, a critical factor for regulatory approval. These factors collectively drive the Nylon segment to become the fastest-growing category in the product landscape.

By Technique Insights

The Microfiltration segment led the APAC pharmaceutical membrane filtration market and captured a share of 48.4% in 2025. This position of the segment is attributed to its fundamental role as the primary step for sterile filtration and clarification in almost all pharmaceutical manufacturing processes. Microfiltration dominates the market also because it is the mandatory final barrier for ensuring the sterility of injectable drugs, ophthalmic solutions, and vaccines, a requirement strictly enforced by regional health authorities. The technique utilizes membranes with pore sizes typically ranging from 0.1 to 0.45 micrometers to physically remove bacteria and fungi without altering the chemical composition of the drug. The ubiquity of this technique across small molecule and large molecule manufacturing ensures a consistent and high volume of demand. Furthermore, the technique is essential for clarifying cell culture harvests and buffer solutions, serving as a pre-treatment for more advanced filtration stages. The critical nature of this step means that manufacturers prioritize reliability and validation support, fostering strong loyalty to established microfiltration providers. This universal application and regulatory necessity cement Microfiltration as the undisputed leader in the technique segment. Beyond sterile filtration, the dominance of Microfiltration is reinforced by its extensive use in clarification and pre-filtration applications, which protect downstream equipment and extend the life of more expensive ultrafiltration membranes. In the complex manufacturing of biologics and vaccines, removing coarse particulates and cell debris is a crucial first step that relies heavily on microfiltration technology. The technique's ability to handle high turbidity feeds makes it suitable for processing herbal extracts and traditional medicines, a growing sector in Asia Pacific. The flexibility of microfiltration allows it to be configured in various formats, including cartridge filters, plate and frame systems, and hollow fiber modules, adapting to diverse scale requirements from pilot plants to commercial production. The cost-effectiveness of microfiltration compared to other techniques also drives its widespread adoption in the generic drug sector, where margin optimization is critical. According to studies, the low operational cost of microfiltration makes it accessible for small and medium-sized enterprises, further expanding its market footprint. This broad applicability across multiple process stages ensures its continued leadership.

The Ultra Filtration segment is predicted to witness the highest CAGR of 11.2% over the forecast period, owing to the exponential rise in biopharmaceutical production, where concentration and diafiltration of proteins and viruses are essential steps that only ultrafiltration can perform efficiently. The primary engine for the rapid growth of this segment is the expanding biopharmaceutical sector inthe Asia Pacific, which relies on this technique for the concentration and purification of large biomolecules like monoclonal antibodies and vaccines. Unlike microfiltration, ultrafiltration separates components based on molecular weight, making it indispensable for isolating therapeutic proteins from fermentation broths. The technique allows manufacturers to concentrate dilute protein solutions without thermal denaturation, preserving product efficacy. The shift toward single-use ultrafiltration cassettes further accelerates adoption, as it reduces cross-contamination risks and cleaning validation burdens. The complexity of biological drugs necessitates precise molecular weight cutoffs that ultrafiltration membranes provide, making it a non-substitutable technology. This alignment with the high-growth biotech sector ensures that Ultra Filtration remains the fastest-expanding technique segment. Ultra Filtration is experiencing rapid growth due to the industry-wide shift toward continuous manufacturing and process intensification, where it plays a central role in integrating upstream and downstream operations. Traditional batch processing is being replaced by continuous flows that utilize ultrafiltration for real-time concentration and buffer exchange, significantly reducing facility footprints and production times. Ultrafiltration enables the recycling of perfusion media in cell culture processes, enhancing cell density and product yield. The technology's scalability allows seamless transition from clinical trial volumes to commercial production, accelerating time to market for new drugs. Furthermore, the development of high-flux ultrafiltration membranes has improved throughput, making the technique more attractive for large-scale operations. This technological evolution positions Ultra Filtration as the dynamic growth leader in the market.

By Application Insights

The Final Product application segment occupied the majority share of the APAC pharmaceutical membrane filtration market in 2025 because of the critical regulatory requirement to ensure the sterility and safety of the finished pharmaceutical dosage form before it reaches the patient. Apart from these, a growth enabler for the Final Product segment is fundamentally underpinned by the non-negotiable regulatory mandate for sterile filtration of all injectable and ophthalmic preparations before filling. This final barrier step is the last line of defense against microbial contamination, making it the most critical application of membrane filtration in the pharmaceutical value chain. The sheer volume of injectable drugs produced in the region, including vaccines, antibiotics, and analgesics, ensures a massive and consistent demand for filtration systems in this application. Furthermore, the trend toward prefilled syringes and auto-injectors, which have zero tolerance for particulates, has heightened the importance of this step. The critical nature of this application means that manufacturers invest heavily in high-quality membranes and redundant systems to guarantee safety. This regulatory and safety imperative secures the Final Product segment as the largest consumer of membrane filtration technology. Beyond sterility, the Final Product segment leads the market due to the extensive use of membrane filtration for removing particulates and ensuring clarity in liquid oral and topical formulations. Regulatory agencies require that all liquid drugs be free from visible and sub-visible particles that could affect patient safety or drug stability. According to pharmacopeia standards adopted by Asia Pacific countries, membrane filtration is the preferred method for clarifying syrups, elixirs, and injectable solutions before packaging. The technique is also crucial for removing precipitates that may form during storage, ensuring shelf-life stability. Moreover, the versatility of membrane filtration allows it to handle viscous solutions and complex emulsions common in pediatric and geriatric medicines. Furthermore, the move toward preservative-free formulations increases the reliance on sterile filtration as the sole method of preservation, amplifying the demand in this segment. The direct link between final filtration and product release makes this application the cornerstone of the pharmaceutical filtration market.

The Raw Material application segment is estimated to register the fastest CAGR of 9.5% from 2026 to 2034 due to the increasing complexity of Active Pharmaceutical Ingredient synthesis and the need for high-purity inputs in biopharmaceutical manufacturing. Besides these, the rapid growth of the Raw Material segment is fuelled by the escalating complexity of Active Pharmaceutical Ingredient synthesis, which increasingly relies on membrane filtration for purification and separation steps. Modern drug discovery involves complex chemical reactions and biocatalytic processes that generate intricate mixtures requiring precise separation to isolate the desired API. Membrane filtration is used to remove catalysts, by-products, and unreacted starting materials, ensuring high purity levels before crystallization. The shift toward enzymatic synthesis, which operates in aqueous environments, further boosts the demand for membrane-based separation in raw material processing. In addition, the need to comply with international impurity limits, such as those for genotoxic impurities, forces manufacturers to incorporate multiple filtration steps in their raw material workflows. This trend toward higher purity standards and more complex synthesis routes propels the Raw Material segment to the forefront of market growth. The burgeoning biopharmaceutical sector is a key driver for the fast growth of the Raw Material segment, specifically in upstream processing, where membrane filtration is used for media preparation and feed clarification. The production of biologics requires vast quantities of highly purified buffers and culture media, which must be filtered to remove contaminants before contacting living cells. Tangential flow filtration is increasingly used to concentrate and diafilter cell culture media components, optimizing nutrient delivery and cell growth. The sensitivity of cell lines to trace impurities necessitates rigorous filtration of all input materials, creating a high-volume demand for membranes in this application. Furthermore, the trend toward single-use upstream technologies relies heavily on disposable membrane filters for media and feed streams. Industry analysts note that the raw material application is becoming more technology-intensive, driving the adoption of advanced membrane solutions. This alignment with the high-growth biotech upstream sector ensures rapid expansion for this segment.

COUNTRY LEVEL ANALYSIS

China Pharmaceutical Membrane Filtration Market Analysis

China outperformed other countries in the APAC pharmaceutical membrane filtration market and held a 38.1% share in 2025. The demand for these systems in China is supported by its massive domestic pharmaceutical industry and aggressive biotechnology expansion. The country serves as the regional hub for drug manufacturing, hosting the highest number of pharmaceutical plants and research centers inthe Asia Pacific. The presence of global giants alongside state-owned entities like Sinopharm ensures continuous investment in advanced manufacturing infrastructure. The regulatory framework is among the strictest in the region, mandating high standards of sterility and purity that drive the adoption of premium filtration solutions. Furthermore, China's leadership in bioethanol and renewable chemicals has spurred cross-industry innovation in membrane technologies that benefit the pharmaceutical sector. The country's extensive network of universities and research institutes fosters innovation in membrane materials, supporting local adaptation and customization. This combination of scale, regulatory rigor, and strategic investment cements China's position as the primary market force.

Japan Pharmaceutical Membrane Filtration Market Analysis

Japan was the next prominent country in the APAC Pharmaceutical Membrane Filtration Market and accounted for a 20.2% share in 2025. This expansion of the Japanese market is credited to its advanced technological capabilities and aging population, driving high pharmaceutical consumption. The country benefits from a highly sophisticated healthcare system and a strong focus on innovation in biopharmaceuticals and regenerative medicine. According to sources, the pharmaceutical sector contributes substantially to the national GDP, with a strong focus on producing high-quality originator drugs and advanced biologics. The presence of numerous global research and development centers drives the demand for world-class filtration systems that meet the standards of the Pharmaceuticals and Medical Devices Agency. Moreover, the government's commitment to health innovation has also led to increased public investment in vaccine production and cell therapy, which expands the market for sterile filtration. The robust regulatory oversight ensures that local manufacturers maintain high-quality standards, further stimulating the demand for advanced filtration. Additionally, the growing prevalence of chronic diseases in Japan is driving domestic consumption of pharmaceuticals, reinforcing the need for efficient manufacturing processes. This strategic focus on quality and innovation propels Japan's significant market standing.

India Pharmaceutical Membrane Filtration Market Analysis

India maintains a significant position in the APAC Pharmaceutical Membrane Filtration Market due to its status as the "Pharmacy of the World" and a leading producer of generic drugs and vaccines. Despite challenges, the country maintains a sophisticated pharmaceutical industry capable of developing and manufacturing complex drugs, including biosimilars and oncology treatments. The presence of renowned research institutions fosters innovation in biotechnology, leading to the development of indigenous vaccines and therapies that require specialized membrane filtration. Also, the regulatory agency CDSCO enforces rigorous quality standards, compelling manufacturers to adopt state-of-the-art filtration systems to ensure product safety. Industry observers note that India is a leader in the production of biosimilars in the region, a segment that heavily utilizes ultrafiltration and tangential flow filtration. The country's focus on high-volume production and cost efficiency drives the demand for reliable and scalable filtration solutions. This emphasis on volume and export orientation sustains India's important role in the regional market landscape.

South Korea Pharmaceutical Membrane Filtration Market Analysis

South Korea is moving ahead steadfastly in the APAC pharmaceutical membrane filtration market by leveraging its strong biotechnology sector and government support for innovation. The country's pharmaceutical sector is characterized by a high degree of modernization and adherence to international standards, attracting multinational corporations to establish regional headquarters and manufacturing bases. According to sources, the country has seen a steady increase in the localization of biopharmaceutical production, which drives demand for sterile filtration equipment. The government's proactive support for the life sciences sector, through agencies like the Ministry of Health and Welfare, has facilitated investments in biotechnology parks and innovation clusters. As per research, the life sciences sector is one of the fastest-growing industries, benefiting from a skilled workforce and robust intellectual property protection. The country's rigorous regulatory framework, managed by the Ministry of Food and Drug Safety, aligns closely with international norms, encouraging the adoption of advanced membrane technologies. Furthermore, the country's stability makes it a preferred location for regional training centers and technical support hubs for filtration suppliers. Data from the Korea Biotech Venture Association shows a rising number of startups focusing on novel drug delivery systems, further diversifying the demand for filtration. This combination of innovation, stability, and strategic positioning supports South Korea's steady market growth.

Australia Pharmaceutical Membrane Filtration Market Analysis

Australia is predicted to grow notably in the APAC market between 2026 and 2034 owing to its high regulatory standards, strong research ecosystem, and focus on specialized therapeutics. The Australian lifestyle and healthcare system revolve around high-quality medical care, leading to a dense network of advanced pharmaceutical manufacturing and research facilities. The custom of rigorous quality assurance ensures a high turnover of advanced membrane technologies, particularly in urban centers like Sydney and Melbourne. The research sector acts as a powerful multiplier, with universities and research institutes conducting cutting-edge clinical trials that require precise filtration solutions. The rise of local biotech startups, although smaller in number, is gaining momentum, with local companies challenging the dominance of imported drugs. In addition, the warm climate in some regions also favors cold chain logistics, making advanced filtration with superior retention highly desirable. As per equipment sales data, the demand for glycol-cooled systems has risen to cope with varying temperatures, indirectly boosting filtration utilization. The cultural ingrainedness of high-quality healthcare ensures that Australia remains a critical and resilient market for filtration suppliers.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific Pharmaceutical Membrane Filtration Market is characterized by a dynamic interplay between established multinational corporations and emerging regional distributors who compete on technology and service quality. The landscape is moderately consolidated, with global leaders leveraging their extensive portfolios and technical expertise to dominate the high-end biopharmaceutical segment. Intense rivalry exists in the area of product innovation, where companies strive to offer higher flux membranes and integrated single-use systems to attract cost-conscious manufacturers. Price sensitivity remains a factor, particularly in the generic drug sector,r but is often outweighed by the need for regulatory compliance and validated performance. New entrants face significant barriers due to the high capital investment required for research and development and the strict validation processes mandated by local health authorities. However,er the growing demand for biosimilars and vaccines creates opportunities for niche players to thrive by offering specialized solutions for specific applications. Oveall the market dynamics favor those who can combine operational efficiency with strong local support networks while adapting quickly to shifting regulatory requirements and economic conditions in the region.

KEY MARKET PLAYERS

Prominent Companies leading the Asia Pacific Pharmaceutical Membrane Filtration Market profiled in this report are

- Merck KGaA

- GE Healthcare

- Pall Corporation

- Sartorius Stedim Biotech

- Alfa Laval

- Graver Technologies LLC

- Koch Membrane Systems Inc.

- GEA Group

- Novasep

TOP LEADING PLAYERS IN THE MARKET

- Merck KGaA operates as a global science and technology leader with a profound impact on the Asia Pacific Pharmaceutical Membrane Filtration Market through its extensive portfolio of process solutions. The company provides advanced membrane technologies, including Pellicon cassettes and Millipore filter,s that are essential for biopharmaceutical purification and sterile filtration across the region. Their contribution to the global market involves setting benchmarks fosingle-usese processing and continuous manufacturing efficiency. Recently, Merck has expanded its technical support centers in China and India to offer localized training and rapid service delivery to pharmaceutical clients. The firm also launched new high flux ultrafiltration membranes designed specifically for the complex biosimilar formulation,s gaining traction ithe n Asia Pacific. By partnering with local contract manufacturers Merck ensures seamless technology transfer and compliance with regional regulatory standards. These strategic initiatives reinforce their commitment to advancing bioprocessing capabilities and supporting the growing demand forhigh-qualityy medicines throughout the Asia Pacific while maintaining their status as a preferred innovation partner globally.

- Danaher Corporation stands as a pivotal innovator in the life sciences sector with a robust presence in the Asia Pacific Pharmaceutical Membrane Filtration Market via its Cytiva and Pall brands. The company delivers comprehensive filtration solutions ranging from depth filters to sterilizing-grade membranes that cater to diverse pharmaceutical applications. Their global contribution centers on integrating digital tools with hardware to enable smart manufacturing and real-time process monitoring. In recent developments, Danaher has strengthened its supply chain resilience in the region by establishing strategic warehousing hubs in Japan and Singapore to ensure consistent product availability. The firm also introducednext-generationn tangential flow filtration systems that reduce processing time and enhance yield for vaccine producers. By focusing on sustainability, Danaher promotes reusable andsingle-usee options that align with the environmental goals of Asian manufacturers. These efforts demonstrate their dedication to providing reliable, efficien,t aneco-friendlyly filtration technologies that empower customers to accelerate drug development and production scales effectively across the continent.

- Sartorius AG is a renowned German supplier specializing in biopharmaceutical manufacturing equipment with a significant footprint in the Asia Pacific Pharmaceutical Membrane Filtration Market. The company offers a wide array of membrane products, including virus filtration modules and sterile filter capsules that are critical for ensuring product safety and purity. Their contribution to the global market is defined by engineering excellence and a strong focus onsingle-usee bioprocessing technologies. Recently, Sartorius has expanded its manufacturing capacity for disposable bag systems and filters in facilities serving the Asia Pacific region to reduce lead times. The firm also enhanced its digital ecosystem by launchingcloud-basedd software for monitoring filtration performance and predicting maintenance needs. By collaborating with regional biotech clusters, Sartorius facilitates knowledge exchange and skill development among local scientists and engineers. Additionall,y the company actively supports sustainability initiatives by optimizing material usage and promoting circular economy practices in packaging. These strategic actions underscore their position as a trusted partner dedicated to supporting the evolving needs of modern pharmaceutical manufacturers and driving innovation in the Asian market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Asia Pacific Pharmaceutical Membrane Filtration Market primarily employ strategies focused on localization and technological advancement to secure competitive advantages. Companies are increasingly establishing regional manufacturing and distribution centers to mitigate supply chain disruptions and reduce delivery times for critical filtration products. Another major strategy involves investing in research and development to create specialized membranes tailored for the unique requirements of biosimilars and vaccines produced in the region. Strategic partnerships with local contract manufacturing organizations help firms expand their customer base and facilitate technology transfer initiatives. Manufacturers are also deploying digital solutions such as Internet of Things sensors and predictive analytics to enhance process efficiency and providvalue-addeded services to clients. Furthermore, firms are prioritizing sustainability by developingeco-friendly single-usee systems and reducing plastic waste through innovative design. These collective efforts aim to deliver superior reliability and performance while adapting to the specific regulatory and economic landscapes of Asia Pacific countries.

MARKET SEGMENTATION

This research report on the Asia Pacific Pharmaceutical Membrane Filtration Market has been segmented and sub-segmented into the following categories:

By Product

- MCE

- Coated Cellulose Acetate

- Nylon

- PVDF Membrane

By Technique

- Microfiltration

- Ultra-Filtration

- Nanofiltration

By Application

- Final Product

- Raw Material

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC