Asia Pacific Probiotics Market Research Report Segmented By Application (Food & Beverages, Dairy Products, Non-Dairy Beverages, Infant Formula, Cereals, Dietary Supplements, Feed), Ingredient (Bacteria, Yeast), Form (Dry, Liquid), End-User (Human And Animal), & Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore & Rest Of APAC) - Industry Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Asia Pacific Probiotics Market Size

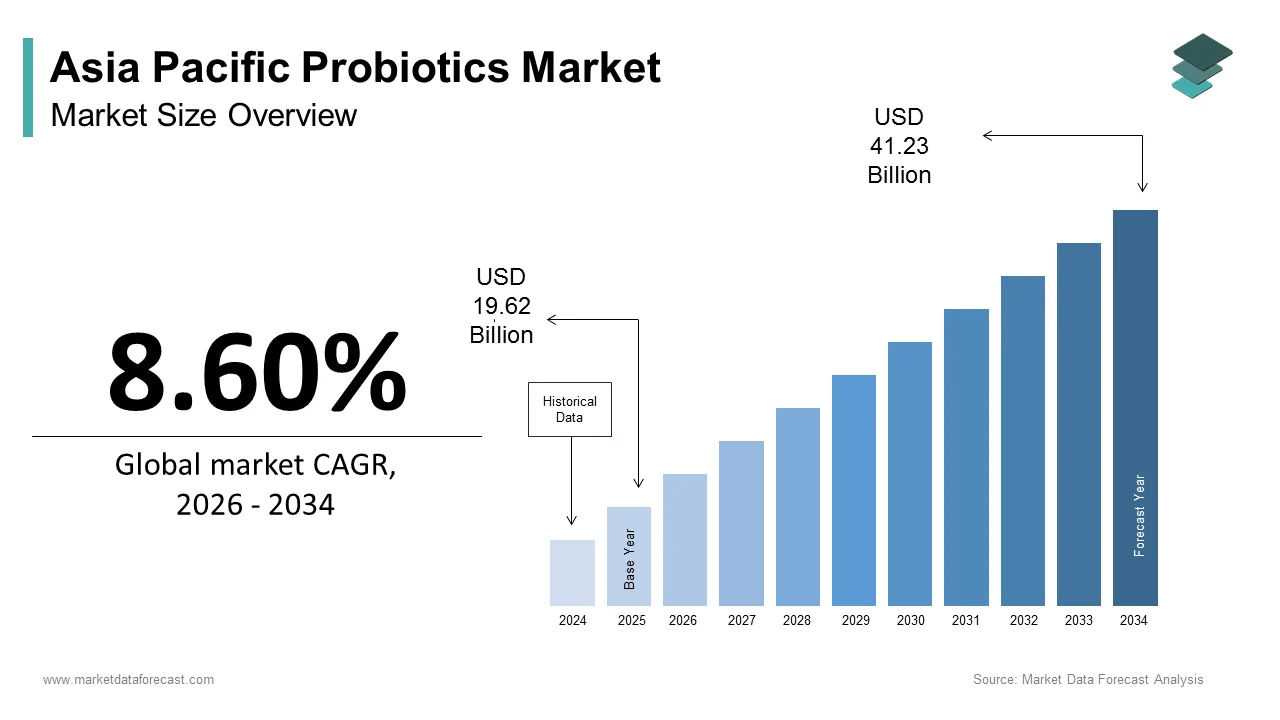

The Asia Pacific probiotics market size was calculated to be USD 19.62 billion in 2025 and is anticipated to be worth USD 41.23 billion by 2034, from USD 21.31 billion in 2026, growing at a CAGR of 8.60% during the forecast period.

The Asia Pacific probiotics market growth is driven by increasing awareness of gut health and its impact on overall well-being. The growing middle-class population, coupled with rising disposable incomes, has fueled demand for functional foods and dietary supplements containing probiotics. For instance, as per the Food Safety and Standards Authority of India, probiotic-rich yogurt and fermented beverages increased by 20% annually between 2018 and 2022. Additionally, urbanization and lifestyle changes, including high-stress levels and poor dietary habits, have exacerbated digestive disorders by prompting consumers to seek preventive healthcare solutions.

MARKET DRIVERS

Rising Awareness About Gut Health

A significant driver of the Asia Pacific probiotics market is the growing awareness about the role of gut health in maintaining overall wellness. Scientific advancements have linked gut microbiota to various health conditions, including obesity, diabetes, and mental health disorders. According to research published in the Journal of Gastroenterology and Hepatology, over 60% of adults in urban areas of the region now recognize the importance of probiotics in improving digestion and boosting immunity. This heightened awareness has led to a surge in demand for probiotic-infused products, such as fortified dairy items, supplements, and even skincare formulations. For instance, Nestlé reported a 25% increase in sales of its probiotic yogurt range in Southeast Asia during 2022. Furthermore, social media influencers and wellness bloggers have played a pivotal role in educating consumers about the benefits of probiotics, which is creating a culture of preventive healthcare.

Increasing Prevalence of Lifestyle Diseases

Another key driver is the rising prevalence of lifestyle-related diseases, which has enhanced the need for preventive healthcare solutions. According to the World Health Organization, non-communicable diseases (NCDs) account for over 70% of deaths in the Asia Pacific region, with poor dietary habits being a major contributing factor. Probiotics are increasingly seen as a natural remedy to combat issues like irritable bowel syndrome (IBS), bloating, and constipation, which are common among individuals with sedentary lifestyles. This has fueled the demand for convenient probiotic supplements and functional foods. For example, Yakult, a popular probiotic drink brand, witnessed a 30% rise in consumption in urban centers like Shanghai and Tokyo.

MARKET RESTRAINTS

High Product Costs

One of the primary restraints hindering the growth of the Asia Pacific probiotics market is the relatively high cost of probiotic products, which limits accessibility for low-income populations. According to a report by the Confederation of Indian Industry, premium probiotic supplements can cost up to 50% more than conventional vitamins, making them unaffordable for a significant portion of rural consumers. In emerging economies like Indonesia and Vietnam, where healthcare spending heavily relies on out-of-pocket expenses, affordability remains a critical barrier. Even in urban areas, where income levels are higher, the perception of probiotics as a luxury product deters widespread adoption. Additionally, the lack of insurance coverage for dietary supplements exacerbates the issue, forcing consumers to bear the full cost. This economic disparity restricts market penetration and slows the adoption of innovative formulations in tier-2 and tier-3 cities where purchasing power is lower.

Limited Awareness in Rural Areas

Another significant restraint is the limited awareness and misconceptions about probiotics in rural and semi-urban regions. According to a survey conducted by the Asian Rural Development Association, less than 20% of rural households in countries like Bangladesh and Nepal are familiar with the concept of probiotics or their health benefits. Traditional beliefs often overshadow scientific evidence, with many individuals relying on home remedies rather than embracing modern solutions. For instance, fermented foods like kimchi and miso are widely consumed in urban areas but remain underutilized in rural settings due to a lack of understanding about their probiotic content. Moreover, inadequate marketing efforts and distribution networks in remote areas further compound the issue.

MARKET OPPORTUNITIES

Integration with Functional Foods and Beverages

The integration of probiotics into functional foods and beverages presents a lucrative opportunity for the Asia Pacific probiotics market. Consumers are increasingly seeking convenient and tasty ways to incorporate health-promoting ingredients into their diets. For instance, Australian brands like Vaalia have successfully launched probiotic-rich smoothies targeting fitness enthusiasts. Similarly, Japanese companies are experimenting with kombucha and other fermented drinks to appeal to younger demographics. The versatility of probiotics allows manufacturers to cater to diverse preferences, from lactose-free options to vegan-friendly formulations.

Expansion into Pediatric and Geriatric Markets

Another promising opportunity lies in tailoring probiotic products for pediatric and geriatric populations, two demographic groups with distinct health needs. According to the United Nations Department of Economic and Social Affairs, the aging population in the Asia Pacific region is expected to reach 535 million by 2030, which is creating a robust market for age-specific probiotics. Elderly individuals often suffer from compromised gut health, making them prime candidates for products designed to enhance digestion and immunity. Simultaneously, the pediatric segment is gaining traction, with parents increasingly prioritizing gut health for their children. Companies like BioGaia have capitalized on this trend by launching kid-friendly formulations in chewable tablets and flavored drops.

MARKET CHALLENGES

Regulatory Hurdles Across Countries

Navigating complex regulatory frameworks poses a significant challenge for the Asia Pacific probiotics market in emerging economies. Each country has its own set of approval processes, labeling requirements, and quality standard creating barriers for multinational companies seeking to introduce innovative products. For example, in India, the Food Safety and Standards Authority mandates extensive clinical trials and documentation for probiotic supplements, delaying market entry by up to two years, according to Deloitte Insights. Similarly, in Indonesia, bureaucratic inefficiencies often prolong the registration process for functional foods and beverages. These delays stifle innovation and limit patient access to cutting-edge formulations. Furthermore, inconsistent enforcement of intellectual property laws in some regions discourages investment in research and development. Companies must allocate additional resources to comply with diverse regulations, increasing operational costs and complicating market strategies.

Misinformation and Consumer Skepticism

Misinformation and consumer skepticism present another pressing challenge for the probiotics market in the Asia Pacific region. Despite growing awareness, misconceptions about the efficacy and safety of probiotics persist, particularly among older generations. According to a study by the Malaysian Medical Association, over 35% of consumers harbor doubts about the scientific validity of probiotic claims, citing conflicting information online and in traditional media. This skepticism is exacerbated by exaggerated marketing tactics used by some brands, which undermine trust in the broader category. For instance, certain products marketed as “miracle cures” fail to deliver tangible results, leading to dissatisfaction and negative reviews. Additionally, cultural beliefs in herbal remedies and alternative medicine often overshadow the adoption of probiotics in rural areas.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.60% |

| Segments Covered | By Form, Ingredient, End User, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of Asia-Pacific |

| Market Leaders Profiled | Yakult Honsha Co. Ltd, Nestle S.A., Groupe Danone, PepsiCo Inc. (Kevita), Lifeway Foods Inc., Actimel, Activia, Bright Dairy, BioGaia, CHR Hansen |

SEGMENTAL ANALYSIS

By Form Insights

The dry probiotics segment accounted for 60.2% of the Asia Pacific probiotics market share in 2025 due to its superior shelf stability and ease of incorporation into various products ranging from supplements to functional foods. Dry probiotic powders have a shelf life of up to two years, compared to liquid forms that degrade faster under improper storage conditions. This durability makes them particularly appealing in regions with inconsistent cold chain infrastructure, such as rural India and Southeast Asia. Additionally, the growing demand for portable and convenient formats, such as capsules and sachets, has further bolstered the segment's growth. As per a report by the Confederation of Indian Industry, over 70% of dietary supplement manufacturers in the region prefer dry probiotics due to their cost-effectiveness and compatibility with high-temperature processing techniques.

Liquid probiotics are projected to grow at the fastest compound annual growth rate (CAGR) of 9.8%, according to data from the Asian Nutrition Society. This rapid expansion is attributed to the rising popularity of fermented beverages like kombucha, kefir, and probiotic-infused juices, which resonate with health-conscious urban consumers. For instance, a survey by Nielsen revealed that over 55% of millennials in metropolitan cities like Tokyo and Sydney prefer ready-to-drink probiotic beverages for their convenience and refreshing taste. Moreover, advancements in encapsulation technologies have enhanced the stability of liquid probiotics, addressing previous concerns about short shelf life. South Korea’s Ministry of Food and Drug Safety reports that innovations such as microencapsulation have increased the viability of live cultures in liquid formats by 40%. The growing emphasis on clean-label products and natural ingredients further fuels demand, positioning liquid probiotics as a dynamic and rapidly evolving segment in the market.

By Ingredients Insights

The bacteria-based probiotics segment held a dominant share of the Asia Pacific probiotics market in 2025 due to the extensive research supporting bacterial strains like Lactobacillus and Bifidobacterium, which are widely recognized for their role in improving gut health and boosting immunity. According to a study published in the Journal of Applied Microbiology, over 80% of commercially available probiotic products contain bacterial strains, underscoring their widespread adoption. Additionally, the versatility of bacteria-based formulations allows for easy integration into a variety of products, including dairy items, supplements, and infant formulas. For instance, Yakult, a leading probiotic drink brand, relies exclusively on Lactobacillus casei Shirota, which has been clinically proven to enhance digestive health. The affordability and scalability of bacterial production further contribute to its prominence by ensuring consistent supply and accessibility across diverse markets.

The yeast-based probiotics segment is swiftly emerging with a CAGR of 11.2% in the coming years. The growth of the segment is attributed to be fueled by increasing consumer interest in alternative probiotic sources among individuals seeking non-dairy options or those with lactose intolerance. Saccharomyces boulardii, a widely used yeast strain, has gained traction due to its efficacy in treating conditions like diarrhea and irritable bowel syndrome (IBS). A clinical trial conducted by the Chinese Academy of Sciences demonstrated that S. boulardii reduced IBS symptoms by 35% in patients within three months of use. Furthermore, the rise of veganism and plant-based diets has amplified demand for yeast-based formulations, as they align with ethical and dietary preferences. Companies like BioCare in Australia have capitalized on this trend by launching yeast-based supplements targeting niche demographics.

By End-User Insights

The human probiotics segment was the largest in holding a significant share of the Asia Pacific probiotics market in 2025 owing to the growing awareness of gut health and its impact on overall well-being, particularly among urban populations. According to the International Probiotics Association, over 60% of adults in metropolitan areas now incorporate probiotic-rich foods or supplements into their daily routines. The aging population also plays a pivotal role; a study by the Japanese Geriatrics Society reveals that elderly individuals account for nearly 30% of probiotic consumers due to their higher susceptibility to digestive disorders. Additionally, targeted marketing campaigns by brands like Yakult and Amul have successfully positioned probiotics as essential components of preventive healthcare.

The animal probiotics segment is expected to hit a CAGR of 10.5% during the foreseen years. The growth of the segment can be driven by the increasing focus on animal health and nutrition with the rising pet ownership and the commercialization of livestock farming. For instance, a survey by the Australian Pet Welfare Foundation found that over 70% of pet owners prioritize gut health when selecting food products, which is creating a robust market for probiotic-infused pet foods. Similarly, in countries like China and India, where livestock contributes significantly to GDP, farmers are adopting probiotics to enhance feed efficiency and reduce antibiotic usage. As per a report by the Indian Veterinary Research Institute, probiotic supplementation in poultry improved weight gain by 20% while reducing mortality rates.

By Application Insights

The food and beverages segment led the Asia Pacific probiotics market by capturing 45.4% of the share in 2025 due to the widespread consumption of probiotic-rich products like yogurt, fermented drinks, and functional snacks. Urbanization and lifestyle changes have further propelled this trend, with busy professionals opting for convenient yet health-promoting options. For example, Nestlé reported a 30% increase in sales of its probiotic yogurt range in Southeast Asia during 2022. Additionally, government initiatives promoting healthy eating habits, such as South Korea’s “Probiotic Awareness Campaign,” have bolstered adoption. The versatility and accessibility of food and beverage applications ensure their continued dominance in the market.

The dietary supplements segment is lucratively growing with an estimated CAGR of 12.3% in the next coming years owing to the rising prevalence of lifestyle diseases and the increasing preference for preventive healthcare solutions. For instance, a study by the Malaysian Medical Association found that over 65% of consumers view dietary supplements as essential for maintaining gut health. The convenience of probiotic capsules, tablets, and powders appeals to health-conscious individuals seeking precise dosages and portability. Additionally, the growing popularity of e-commerce platforms has expanded access to premium supplements in urban centers. Innovations such as delayed-release capsules and synbiotic formulations further enhance efficacy, enhancing dietary supplements as a dynamic and rapidly expanding segment.

REGIONAL ANALYSIS

China was the top performer in the Asia Pacific probiotics market with a 30.4% share in 2025 the country’s massive population, coupled with rising disposable incomes, drives demand for functional foods and dietary supplements. According to the National Health Commission, over 70% of urban households now include probiotic products in their grocery baskets, reflecting a cultural shift towards preventive healthcare. The government’s "Healthy China 2030" initiative has further accelerated adoption by promoting gut health awareness through public campaigns. Additionally, domestic brands like Bright Dairy have capitalized on local preferences, offering affordable and culturally relevant probiotic options.

India's probiotics market was witnessed in holding 20.5% of the share in 2025 owing to its increasing middle-class population and rising awareness of gut health, as per the Confederation of Indian Industry. The country’s rich tradition of fermented foods, such as curd and idli, provides a natural foundation for probiotic adoption. According to the Food Safety and Standards Authority of India, the consumption of probiotic-rich yogurt increased by 20% annually between 2018 and 2022 with strong consumer interest. Multinational companies like Amul and Mother Dairy have introduced innovative products tailored to local tastes, while startups focus on affordable supplements. Government-backed initiatives, such as mass health screenings, have also played a pivotal role in educating rural populations about the benefits of probiotics by ensuring sustained market growth.

Japan's probiotics market growth is driven by its advanced healthcare infrastructure and aging population. The country’s emphasis on longevity and preventive care has made probiotics a staple in daily diets. For instance, Yakult, a globally recognized probiotic drink, originated in Japan and remains a household name. According to the Ministry of Health, Labour and Welfare, over 60% of elderly individuals consume probiotics regularly to address digestive issues and boost immunity. Additionally, the integration of probiotics into traditional foods like miso and natto enhances their appeal.

The South Korean probiotics market is likely to have significant growth opportunities in next coming years. The country’s focus on beauty-from-within trends has popularized probiotics as tools for enhancing skin health and overall wellness. According to Nielsen, over 55% of millennials in Seoul prefer probiotic-infused skincare products and beverages, reflecting a unique blend of health and aesthetics. Brands like CJ CheilJedang have capitalized on this trend by launching kombucha and other fermented drinks targeting younger demographics. Additionally, the government’s support for biotech research has spurred advancements in probiotic formulations by ensuring consistent innovation and consumer trust.

Australia's probiotics market growth is driven by its robust regulatory framework and emphasis on clean-label products. The country’s health-conscious population prioritizes natural and organic formulations by creating a fertile ground for premium probiotic brands. Local companies like BioCeuticals have gained traction by offering science-backed probiotic solutions tailored to specific health needs. The growing popularity of plant-based diets and veganism further amplifies demand, which is positioning Australia as a hub for high-quality probiotic innovations.

LEADING PLAYERS IN THE ASIA PACIFIC PROBIOTICS MARKET

Yakult Honsha Co., Ltd.

Yakult Honsha Co., Ltd. is a global leader in the probiotics market, renowned for its flagship product, Yakult, a fermented milk drink containing Lactobacillus casei Shirota. The company’s contributions extend beyond the Asia Pacific region, shaping global standards for probiotic beverages. Its focus on scientific research and clinical trials has established its products as trusted solutions for digestive health. By leveraging localized marketing strategies, Yakult has successfully penetrated diverse markets, from Japan to India. Collaborations with healthcare professionals and participation in public health campaigns further reinforce its brand equity. Its commitment to quality and innovation ensures its position as a pioneer in promoting gut health worldwide.

Nestlé S.A.

Nestlé S.A., a Swiss multinational, has made significant strides in the Asia Pacific probiotics market through its innovative product portfolio. Brands like Nestlé A+ Milk and NESTLÉ ACTICOR are fortified with probiotics, catering to both children and adults. The company’s emphasis on functional foods aligns with consumer preferences for convenient health solutions. By investing in cutting-edge research and development, Nestlé has introduced products that combine taste with nutritional benefits. Its global supply chain and strong distribution networks enable it to reach urban and rural consumers alike.

Amul Dairy (GCMMF)

Amul Dairy is part of the Gujarat Cooperative Milk Marketing Federation (GCMMF), which is a dominant player in India’s probiotics market, offering affordable and high-quality dairy-based products. Its probiotic yogurt and buttermilk variants have gained widespread popularity due to their accessibility and cultural relevance. Amul’s success lies in its deep understanding of local tastes and preferences, enabling it to innovate while maintaining affordability. Through strategic partnerships with farmers and government initiatives, Amul ensures consistent supply and quality. Its efforts not only strengthen its domestic presence but also position it as a key contributor to the global probiotics landscape.

TOP STRATEGIES USED BY KEY PLAYERS IN THE ASIA PACIFIC PROBIOTICS MARKET

Product Innovation and Diversification

Key players in the market are increasingly focusing on product innovation to cater to evolving consumer preferences. The companies can appeal to niche demographics such as health-conscious millennials and environmentally aware consumers by diversifying their portfolios to include plant-based, vegan-friendly, and clean-label probiotic options. For instance, introducing synbiotic formulations that combine prebiotics and probiotics enhances product efficacy, by addressing specific health concerns like immunity and gut health. This strategy not only differentiates brands but also fosters customer loyalty by meeting unmet needs. R&D investments ensure that products remain scientifically validated and aligned with global health trends.

Strategic Partnerships and Collaborations

Strategic partnerships with local distributors, healthcare providers, and research institutions are pivotal for strengthening market presence. Additionally, alliances with e-commerce platforms expand reach, particularly in urban centers where online shopping is prevalent. These collaborations also enable players to navigate regulatory challenges more effectively, ensuring compliance with regional standards. Joint ventures with local firms further facilitate entry into underserved markets by creating a win-win scenario for all stakeholders involved.

Consumer Education and Awareness Campaigns

Educating consumers about the benefits of probiotics is another critical strategy employed by industry leaders. Through targeted marketing campaigns, social media engagement, and partnerships with influencers, companies aim to dispel misconceptions and build trust. Hosting workshops, webinars, and public health events helps create a deeper understanding of gut health and its impact on overall wellness. For example, emphasizing the role of probiotics in managing lifestyle diseases resonates with urban populations seeking preventive healthcare solutions.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the Asia Pacific probiotics market include Yakult Honsha Co. Ltd, Nestle S.A., Groupe Danone, PepsiCo Inc. (Kevita), Lifeway Foods Inc., Actimel, Activia, Bright Dairy, BioGaia, CHR Hansen.

The Asia Pacific probiotics market is characterized by intense competition, driven by the presence of both global giants and regional players striving to capture a larger share of the burgeoning health-conscious consumer base. Multinational corporations like Nestlé and Yakult bring technological expertise and extensive R&D capabilities, enabling them to introduce breakthrough formulations that set industry benchmarks. Simultaneously, domestic players leverage their understanding of local preferences and cost-effective manufacturing to carve out significant market shares. This dynamic creates a dual-layered competitive landscape where innovation and affordability coexist. The market is further fueled by rising consumer awareness and the growing prevalence of lifestyle-related disorders, prompting companies to adopt aggressive marketing strategies and expand their distribution networks. Additionally, the emergence of e-commerce platforms has intensified competition, as players vie to capitalize on digital trends. Regulatory challenges and cultural factors add complexity, requiring firms to balance compliance with innovation.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, Yakult Honsha launched a new line of plant-based probiotic beverages targeting vegan consumers in Japan and South Korea. This initiative aimed to address the growing demand for sustainable and inclusive health solutions by strengthening its appeal among environmentally conscious buyers.

- In June 2023, Nestlé partnered with a leading Indian e-commerce platform to offer exclusive discounts on its probiotic-enriched dairy products during the festive season. This collaboration expanded its reach in tier-2 and tier-3 cities by enhancing accessibility for first-time users.

- In September 2023, Amul Dairy introduced a low-cost probiotic yogurt variant specifically designed for rural markets in India. The product was marketed through local cooperatives by ensuring affordability and cultural relevance while boosting penetration in underserved areas.

- In November 2023, BioGaia collaborated with a Malaysian biotech firm to develop synbiotic supplements tailored for pediatric use. This partnership focused on addressing gut health issues in children by aligning with the rising trend of family-centric healthcare solutions.

- In January 2025, Yakult organized a series of gut health awareness campaigns across Southeast Asia, partnering with local health ministries to educate consumers about the benefits of probiotics. These initiatives included free sampling events and expert-led seminars by reinforced brand trust and the driving adoption.

MARKET SEGMENTATION

This research report on the Asia Pacific probiotics market has been segmented and sub-segmented based on form, ingredient, end user, application, and region.

By Form

- Dry

- Liquid

By Ingredient

- Bacteria

- Yeast

By End User

- Human

- Animal

By Application

- Food & Beverages

- Dairy Products

- Non-Dairy Beverages

- Infant Formula

- Cereals

- Dietary Supplements

- Feed

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

1. What is driving the growth of the Asia Pacific probiotics market?

Market growth is mainly driven by rising consumer awareness of gut health, increasing disposable income, and growing demand for functional foods and dietary supplements

2. Which product segment dominates the Asia Pacific probiotics market?

Probiotic food and beverage products dominate the market due to high consumption of yogurt, fermented dairy products, and probiotic drinks.

3. Which segment is expected to grow rapidly?

Probiotic dietary supplements are expected to grow at the fastest rate due to increasing health consciousness among consumers.

4. Which ingredient type holds a major market share?

Bacterial probiotics such as Lactobacillus and Bifidobacterium dominate the market due to their proven effectiveness in digestive and immune health.

5. What trends are shaping the Asia Pacific probiotics market?

Key trends include increasing demand for personalized nutrition, plant-based probiotic products, and innovations in probiotic strain formulations.

6. How does urbanization influence the Asia Pacific probiotics market?

Rapid urbanization increases demand for functional foods and preventive healthcare products, thereby boosting probiotic consumption.

7. What challenges are faced by the Asia Pacific probiotics market?

Stringent regulatory requirements and high production costs may restrain market growth.

8. How is the infant nutrition sector impacting the market?

Probiotics are increasingly used in infant formula and child nutrition products to improve digestive health.

9. How does health awareness impact market growth?

Growing awareness regarding digestive health and immunity is encouraging consumers to adopt probiotic-enriched foods and supplements.

10. What is the future outlook of the Asia Pacific probiotics market?

The market is expected to witness steady growth due to rising adoption of preventive healthcare and increasing awareness of gut-immune system benefits.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com