- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

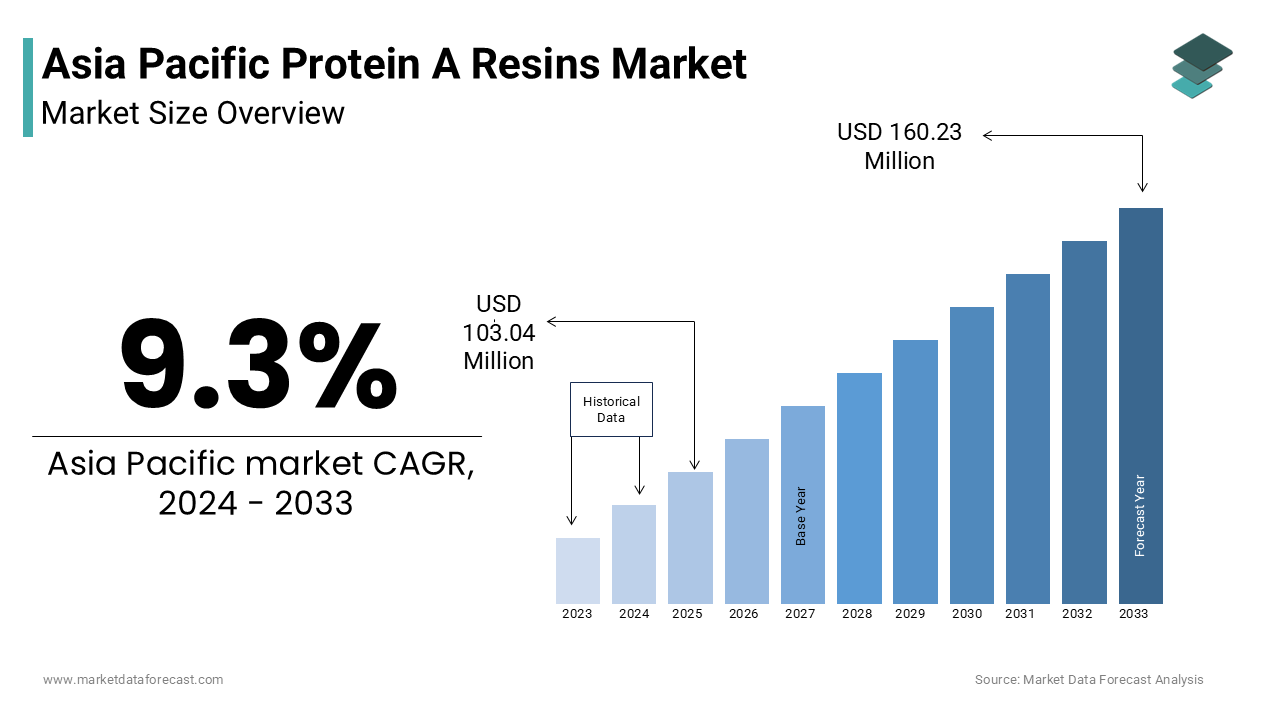

Market Size, 2025

$112.63 MnMarket Estimate, 2026

$123.1 MnMarket Forecast, 2034

$250.74 MnCAGR, 2026–2034

9.3%Executive Summary: Asia Pacific Protein A Resins Market

- Market Scope: Comprehensive regional protein A resins market analysis covering matrix bases, product types, application verticals, regional leadership frameworks, and adoption metrics.

- Market Valuation: Valued at USD 112.63 million (2025), estimated at USD 123.10 million (2026), and projected to reach USD 250.74 million by 2034, registering a robust CAGR of 9.3% (2026–2034).

- Primary Growth Drivers: Rapid expansion of biopharmaceutical manufacturing capacity in China and India, rising demand for monoclonal antibodies and biosimilars, and increasing government funding for life sciences. Key trends include the proliferation of CDMOs, technological advancements in high-flow agarose matrices and alkaline-stable ligands, and growing adoption of single-use chromatography systems, though high resin costs, supply chain volatility, and fragmented regulatory landscapes present ongoing challenges.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

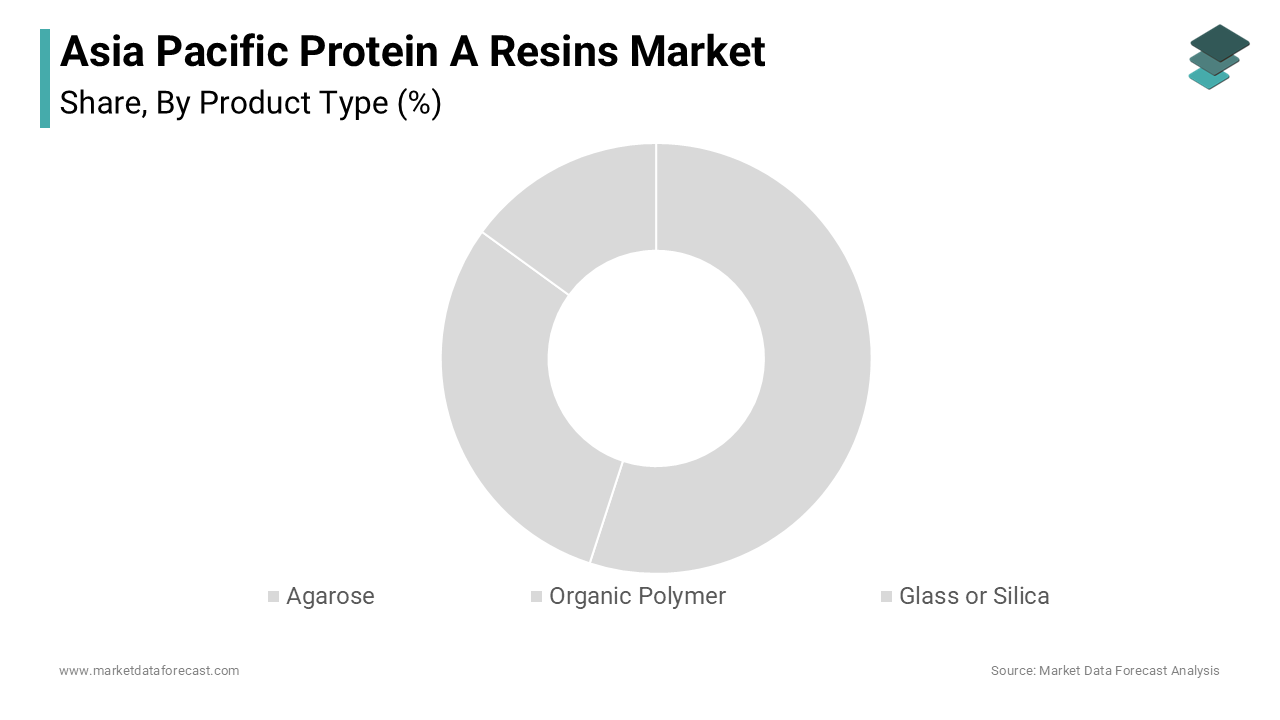

| By Matrix Base | Agarose-based Resins (dominated with a 59.1% share in 2024) | Organic Polymer-based Resins (projected to grow at a CAGR of 14.6%) |

| By Product Type | Recombinant Protein A Resins (held the largest share by type in 2024) | Natural Protein A Resins (expected to grow at a CAGR of 9.8%) |

| By Application | Antibody Purification (established as the largest application segment) | Immunoprecipitation (likely to grow at a CAGR of 12.4%) |

| By Region / Country | China (led regionally with a 35.3% share in 2024, followed by India at 18.3%) | Emerging APAC biomanufacturing hubs and specialized research sectors |

Major Market Players & Market Structure

Market Structure: Highly competitive Asia-Pacific bioprocessing landscape characterized by strategic regional expansions and partnerships, including Cytiva’s Shanghai facility expansion, Thermo Fisher’s Bangalore technical support center launch, Repligen’s South Korean CDMO collaboration, Bio-Rad’s agarose-based resin line introduction, and Pall Corporation’s Chinese biopharma incubator partnership.

Key Companies: GE Healthcare (Cytiva), Thermo Fisher Scientific, Repligen Corporation, Novasep, Tosoh Bioscience, GenScript, EMD Millipore, Expedeon Ltd., Bio-Rad Laboratories, and Pall Corporation.

Asia Pacific Protein A Resins Market Size

The Asia Pacific Protein A Resins Market size was valued at USD 112.63 million in 2025 and is anticipated to reach USD 123.1 million in 2026 from USD 250.74 million by 2034, growing at a CAGR of 9.3% during the forecast period from 2026 to 2034.

Protein A resins are specialized affinity chromatography media primarily used in the purification of monoclonal antibodies (mAbs) and other immunoglobulins. These resins contain immobilized Protein A, a surface protein originally derived from Staphylococcus aureus, which exhibits high binding specificity to the Fc region of immunoglobulin G (IgG). This growth trajectory is further supported by increasing government funding for life sciences and a growing focus on developing biosimilars.

MARKET DRIVERS

Expansion of Biopharmaceutical Manufacturing Capacity in Asia Pacific

The rapid expansion of biopharmaceutical manufacturing infrastructure. Countries like China, India, and South Korea are increasingly investing in large-scale biomanufacturing facilities to meet rising domestic and global demand for biologics, including monoclonal antibodies (mAbs), vaccines, and biosimilars. According to the Centre for Innovation in Healthcare (CIH), China alone added more than 30 new biopharma production sites between 2020 and 2023. This surge in manufacturing activity directly increases the consumption of Protein A resins, which are essential for purifying mAbs during downstream processing. The Indian Biotechnology Industry Research Assistance Council (BIRAC) reported that India’s biopharma sector witnessed a 20% increase in production volume in 2023 compared to the previous year, with over 70% of this output relying on Protein A-based purification methods. Additionally, regulatory reforms such as the introduction of fast-track approvals for biosimilars in Japan have further encouraged investment in biologics production, reinforcing the need for high-efficiency purification technologies.

Rising Demand for Monoclonal Antibodies and Biosimilars

The escalating global demand for monoclonal antibodies (mAbs) and biosimilars is another critical driver influencing the growth of the Protein A resins market in the Asia Pacific region. mAbs constitute a major segment of modern therapeutics, particularly in oncology, autoimmune diseases, and infectious disease treatment. As per the World Health Organization (WHO), over 100 mAb-based drugs were approved globally by the end of 2023, with more than 40% of these therapies being developed or manufactured in Asia Pacific countries. China and India have emerged as key players in biosimilar development, which is leveraging cost-effective manufacturing capabilities and streamlined regulatory pathways.

MARKET RESTRAINTS

High Cost and Limited Reusability of Protein A Resins

The high acquisition and operational costs associated with these purification materials is slowly restraining the growth of the Asia Pacific Protein A resins market. Protein A resins are among the most expensive consumables in biopharmaceutical downstream processing, often accounting for up to 60% of the total purification costs in monoclonal antibody (mAb) manufacturing, as reported by McKinsey & Company in 2023. This financial burden is particularly pronounced for small and medium-sized enterprises (SMEs) and emerging biotech firms in the region, which may lack the capital to invest in premium-grade resins. Additionally, the limited reusability of Protein A resins poses a major economic challenge. While some advanced resin variants can be reused up to 50 cycles without significant loss of binding capacity, many conventional types degrade after 10–20 cycles due to harsh cleaning-in-place (CIP) protocols involving low pH or strong detergents. In countries like India and Indonesia, where cost sensitivity is high and reimbursement systems are still evolving, this factor discourages widespread adoption of high-end Protein A resins.

Supply Chain Constraints and Raw Material Shortages

The ongoing volatility in supply chains and raw material availability is also hindering the growth of the Asia Pacific Protein A resins market. Protein A resins are typically composed of agarose or synthetic matrices coupled with recombinant Protein A ligands. According to the Global Biotech Outlook 2023 published by BioPlan Associates, over 70% of Protein A resin manufacturers in the Asia Pacific region depend on imported base matrices and ligands, making them vulnerable to geopolitical disruptions, freight delays, and customs bottlenecks. Moreover, the production of recombinant Protein A involves fermentation and purification steps that require high-purity reagents and enzymes many of which faced shortages due to factory shutdowns and logistical constraints.

MARKET OPPORTUNITIES

Growth of Contract Development and Manufacturing Organizations (CDMOs)

The proliferation of contract development and manufacturing organizations (CDMOs) in the Asia Pacific region presents a substantial opportunity for the Protein A resins market. CDMOs play a pivotal role in accelerating the development and commercialization of biologics by offering end-to-end services, including process development, clinical trial manufacturing, and large-scale commercial production. These organizations rely heavily on standardized, high-efficiency purification platforms, where Protein A resins serve as the cornerstone technology. As per the Center for Biopharmaceutical Services (CBS), approximately 85% of all monoclonal antibody (mAb) purification processes outsourced to CDMOs in the region utilize Protein A chromatography. The shift toward outsourcing in biopharma, driven by cost optimization and faster time-to-market, has led to increased resin consumption across CDMO facilities. Furthermore, the rise of flexible manufacturing models, such as multi-product bioreactors and modular purification skids, enhances the adaptability of CDMOs to handle diverse client pipelines.

Technological Advancements in Resin Design and Single-Use Technologies

Advancements in resin engineering and the integration of single-use technologies are opening new avenues for growth in the Asia Pacific Protein A resins market. Manufacturers are increasingly focusing on improving resin performance through innovations such as high-flow agarose matrices, alkaline-stable ligands, and smaller particle sizes that enhance binding capacity and reduce cycle times. According to the European Federation for Pharmaceutical Sciences (EUFEPS), next-generation Protein A resins introduced in 2023 offer up to 25% higher dynamic binding capacities compared to earlier versions by enabling more efficient purification processes. Additionally, the adoption of single-use chromatography systems is gaining momentum in the region, particularly among CDMOs and biotech startups seeking to minimize cross-contamination risks and reduce cleaning validation requirements. South Korea and Singapore have been early adopters of these technologies, with government-backed initiatives promoting green biomanufacturing practices and waste reduction. The Korea Biomedical Review reported that Korean biopharma firms reduced resin-related waste by 18% in 2023 through the implementation of single-use resin systems.

MARKET CHALLENGES

Regulatory Complexity and Compliance Burden Across Diverse Markets

A major challenge facing the Asia Pacific Protein A resins market is the fragmented regulatory landscape across the region. Asia Pacific comprises multiple jurisdictions with varying regulatory standards, approval timelines, and documentation requirements. This diversity complicates compliance for both resin manufacturers and biopharma companies integrating these products into their workflows. For example, China’s National Medical Products Administration (NMPA) enforces stringent Good Manufacturing Practice (GMP) audits and local testing mandates for imported bioprocessing materials. In contrast, Australia’s Therapeutic Goods Administration (TGA) follows an approach closer to the EU’s EudraLex guidelines, creating inconsistencies in quality expectations. Moreover, the requirement for extensive documentation, including batch-specific certificates of analysis and traceability records, increases administrative overhead.

Environmental Impact and Waste Management Concerns

Environmental sustainability has emerged as a growing concern in the Protein A resins market, particularly in the Asia Pacific region where waste management infrastructure varies widely. The production and disposal of Protein A resins generate significant environmental footprints due to the use of hazardous chemicals in resin synthesis, ligand coupling, and cleaning-in-place (CIP) procedures. As per the United Nations Environment Programme (UNEP), the biopharma industry contributes approximately 15% of pharmaceutical sector waste, with chromatography resins accounting for a notable portion. In countries like India and Vietnam, where wastewater treatment facilities are often inadequate, improper disposal of spent resins and cleaning agents can lead to soil and water contamination. The Indian Central Pollution Control Board (CPCB) issued stricter discharge norms in 2023, requiring biopharma companies to treat effluents containing residual Protein A ligands before release. Additionally, the non-biodegradable nature of agarose and synthetic resin matrices poses long-term disposal challenges. Some resin manufacturers are exploring recyclable or bio-based alternatives, but adoption remains limited due to technical and economic barriers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.3% |

| Segments Covered | By Product Type , Type, Application, End Users and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, the Philippines, Indonesia, Singapore, and the Rest of APAC. |

| Market Leaders Profiled | GE Healthcare, Repligen Corporation, Novasep, Tosoh Bioscience, GenScript, Thermo Fisher Scientific, EMD Millipore, and Expedeon Ltd |

SEGMENTAL ANALYSIS

By Product Type Insights

The agarose-based Protein A resins was accounted in holding 59.1% of the Asia Pacific protein A resins market share in 2024. The growth of the segment is attributed to the preference for agarose-based resins due to their high binding capacity and compatibility with large-scale chromatography systems, which are increasingly being deployed in China, India, and South Korea. According to the International Society for Pharmaceutical Engineering (ISPE), more than 70% of commercial mAb production facilities in the region utilize agarose-based matrices for initial purification steps. Additionally, the well-established supply chain and availability of cost-effective variants from local manufacturers have further reinforced their dominance. The Chinese Biopharma Association reported that domestic resin producers supplied nearly 45% of the agarose-based Protein A resin demand in 2023, significantly reducing import dependency and lowering overall process costs.

The organic polymer-based Protein A resins segment is likely to grow with a CAGR of 14.6% from 2025 to 2033 as these resins offer superior chemical and mechanical resistance compared to traditional agarose matrices, enabling longer column life and increased reuse cycles. As per the American Chemical Society (ACS), organic polymer-based resins can withstand up to 100 purification cycles without significant loss of binding efficiency by making them ideal for continuous manufacturing setups gaining traction in countries like Japan and Singapore.

By Type Insights

The recombinant Protein A resins segment held a dominant share of the Asia Pacific Protein A resins market in 2024 with its superior batch-to-batch consistency and reduced risk of microbial contamination, both of which are crucial for regulatory compliance in pharmaceutical manufacturing. According to the U.S. Food and Drug Administration (FDA) guidelines adapted by several Asian regulators, recombinant versions are preferred due to their defined genetic origin and absence of pathogenic elements associated with Staphylococcus aureus. Furthermore, the expansion of biologics manufacturing hubs in China and India has led to greater demand for high-performance purification media.

The natural protein A resins segment is expected to grow with an expected CAGR of 9.8% during the forecast period. The growth of the segment can be driven by the cost-effectiveness of natural Protein A, which makes it an attractive option for budget-constrained laboratories and early-stage biotech startups in countries like Indonesia, Thailand, and Vietnam. Another key driver is the increased utilizationofn immunoassay development in diagnostic kits targeting autoimmune diseases and infectious agents. The Japanese Ministry of Health, Labour and Welfare (MHLW) reported a 15% increase in diagnostic assay production in 2023, with many relying on natural Protein A for IgG capture.

By Application Insights

The antibody purification segment was the largest by capturing a prominent share of the Asia Pacific Protein A resins market share in 2024. The core reason for the continued reliance on Protein A resins in antibody purification lies in their high specificity towards the Fc region of IgG antibodies, ensuring efficient and selective capture during downstream processing. China’s National Medical Products Administration (NMPA) approved 15 new biosimilars in 2023 alone, all of which required Protein A-based purification steps.

The immunoprecipitation segment is likely to grow with an anticipated CAGR of 12.4% in the next coming years due to the rising investment in academic and translational research in countries like Japan, Australia, and Singapore. The University Grants Committee of Hong Kong reported a 22% increase in life sciences funding in 2023 with a significant portion allocated to proteomics and cell signaling research utilizing immunoprecipitation techniques. Additionally, the integration of Protein A resins into automated immunoassay platforms has improved workflow efficiency in clinical diagnostics and biomedical research centers. The Australian Government’s Department of Health indicated that diagnostic labs in the country adopted immunoprecipitation-based assays for autoimmune disease detection in 40% of new test protocols introduced in 2023.

REGIONAL ANALYSIS

China Protein A Resins Market Insights

China was the top performer in the Asia Pacific Protein A resins market with 35.3% of share in 2024. As per the Chinese Biopharma Association, the country added more than 25 new biologics manufacturing plants between 2021 and 2023, each requiring extensive use of Protein A resins for monoclonal antibody (mAb) purification. In addition, China’s growing participation in global contract development and manufacturing organization (CDMO) networks has amplified resin consumption. The Shanghai Center for Industrial Pharmacy reported that outsourced biologics manufacturing in China grew by 28% in 2023, with nearly all projects involving Protein A-based purification steps.

India Protein A Resins Market Insights

India ranked second in the Asia Pacific Protein A resins market with 18.3% of the share in 2024. India’s Central Drugs Standard Control Organization (CDSCO) has streamlined biosimilar approval processes, leading to a 35% increase in mAb-based drug submissions in 2023, according to the Indian Biotechnology Industry Research Assistance Council (BIRAC). This regulatory momentum has encouraged domestic firms to scale up production, directly boosting Protein A resin usage.

South Korea Protein A Resins Market Insights

South Korea Protein A resins market growth is esteemed to gain huge opportunities throughout the forecast period due to the government-backed "Bio Korea 2030" strategy, which aims to elevate the nation’s biopharma exports.

Japan Protein A Resins Market Insights

Japan Protein A resins market growth is likely to grow with its well-established biopharmaceutical ecosystem, stringent quality standards, and advanced healthcare infrastructure, as per a 2023 report by the Japan Bioindustry Association (JBA). The country’s emphasis on innovative therapies and precision medicine continues to drive consistent demand for high-quality purification materials. Additionally, the country’s expanding contract manufacturing sector has reinforced resin consumption. Moreover, the adoption of next-generation Protein A resins with enhanced alkaline stability has gained traction among top-tier firms such as Daiichi Sankyo and Takeda, which is aligning with sustainability goals and improving process efficiency.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific Protein A resins market is marked by a blend of established global players and emerging regional suppliers striving to capture a larger share of the expanding biopharmaceutical landscape. The market is witnessing increased investment in advanced resin engineering, aiming to improve performance metrics such as binding capacity, chemical stability, and reusability. At the same time, strategic moves like joint ventures, regional expansions, and integration with downstream processing platforms are shaping the competitive dynamics. While multinational corporations maintain a dominant presence, local manufacturers are gaining traction by offering cost-effective alternatives and agile service models.

KEY MARKET PLAYERS

The companies dominating the APAC Protein A Resins Market include

Top Players in the Asia Pacific Protein A Resins Market

GE Healthcare (Cytiva) Insights

GE Healthcare, operating under the Cytiva brand, is a global leader in life sciences tools and biopharma solutions. In the Asia Pacific region, Cytiva plays a pivotal role in supplying high-performance Protein A resins for monoclonal antibody purification. The company’s extensive distribution network and strong partnerships with biopharma firms and CDMOs support its dominance. Cytiva's innovative resin technologies are widely adopted across China, India, Japan, and South Korea due to their reliability and compatibility with large-scale bioprocessing workflows.

Thermo Fisher Scientific

Thermo Fisher Scientific is a key player known for offering a broad portfolio of chromatography media, including Protein A resins tailored for diverse purification needs. The company has strengthened its presence through localized manufacturing, strategic collaborations, and technical support services. Thermo Fisher’s ability to integrate its resins with automated systems and single-use technologies has made them a preferred choice among contract manufacturers and research institutions across the region.

Repligen Corporation

Repligen has emerged as a major supplier of high-capacity Protein A resins, particularly favored for their efficiency in continuous and high-throughput bioprocessing. The company has expanded its customer base by focusing on cost-effective, scalable purification solutions with a growing footprint in the Asia Pacific region. Repligen collaborates closely with leading biopharma companies and CDMOs in Asia Pacific by providing customized resin formats that align with evolving manufacturing standards and regulatory expectations.

Top Strategies Used by Key Market Participants

Key players in the Asia Pacific Protein A resins market employ several strategic initiatives to reinforce their market position. One of the most prevalent strategies is technology innovation, where companies focus on developing next-generation resins with enhanced binding capacity, longer lifespan, and compatibility with modern bioprocessing techniques such as continuous chromatography and disposable systems. Another crucial approach is strategic partnerships and collaborations, wherein market leaders engage with regional biopharma firms, academic institutions, and government bodies to align with local R&D and manufacturing goals.

RECENT MARKET DEVELOPMENTS

- In May 2023, Cytiva (GE Healthcare) expanded its manufacturing facility in Shanghai, China, to increase local production of Protein A resins by enhancing supply chain resilience and reducing lead times for biopharma customers in the region.

- In July 2023, Thermo Fisher Scientific launched a dedicated technical support center in Bangalore, India, to provide end-to-end assistance for chromatography-based purification processes, which is strengthening its foothold in the country’s booming biosimilars sector.

- In October 2023, Repligen Corporation entered into a strategic collaboration with a leading South Korean CDMO to co-develop custom Protein A resin formats optimized for high-throughput monoclonal antibody purification by aligning with regional manufacturing trends.

- In February 2024, Bio-Rad Laboratories introduced a new line of agarose-based Protein A resins designed for small-scale and academic research applications by targeting the growing immunoprecipitation segment in Japanese and Australian research institutions.

- In June 2024, Pall Corporation (part of Danaher) announced a partnership with a Chinese biopharma incubator to offer integrated resin and filtration solutions by supporting early-stage companies in streamlining their purification workflows and accelerating development timelines.

MARKET SEGMENTATION

This research report on the APAC Protein A Resins market has been segmented and sub-segmented into the following categories.

By Product Type

- Agarose

- Organic Polymer

- Glass or Silica

By Type

- Natural Protein A Resin

- Recombinant Protein A Resin

By Application

- Immunoprecipitation

- Antibody Purification

By End Users

- Biopharmaceutical Manufacturers

- Clinical Research Laboratories

- Academic Institutions

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC