Asia Pacific Radar Sensor Market Size, Share, Trends & Growth Forecast Report By Type (Imaging, Non-Imaging), Range, Application, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore And Rest Of Asia-Pacific), Industry Analysis From 2025 To 2033

Asia Pacific Radar Sensor Market Size

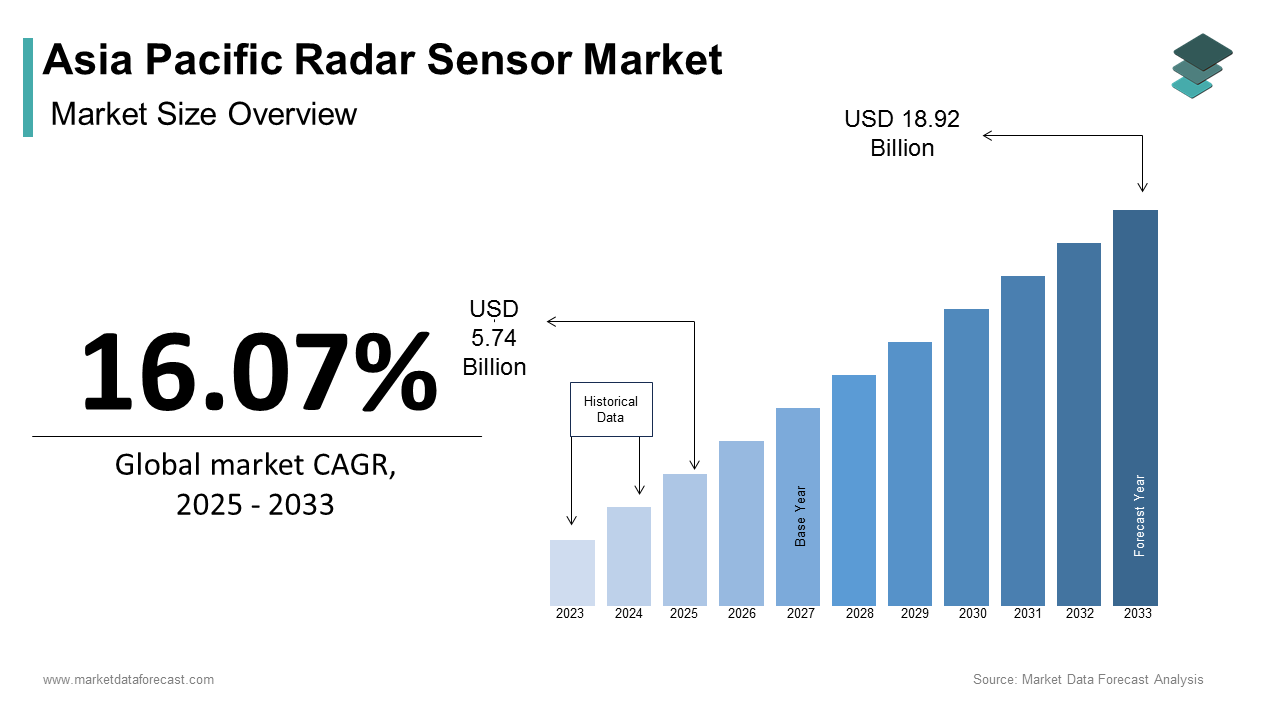

The Asia Pacific radar sensor market size was calculated to be USD 4.95 billion in 2024 and is anticipated to be worth USD 18.92 billion by 2033, from USD 5.74 billion in 2025, growing at a CAGR of 16.07% during the forecast period.

The Asia Pacific radar sensor utilizes electromagnetic waves to detect objects, measure speed, and determine distance with high precision by making them integral to modern safety, navigation, and monitoring systems. According to the International Telecommunication Union, over 65% of new passenger vehicles in Japan now include some form of radar-based driver assistance system with the growing integration of these sensors in automotive applications. In China, as per the Ministry of Industry and Information Technology, more than 10 million drones equipped with radar sensors were registered for commercial use in 2023, indicating a strong adoption rate in unmanned aerial systems. Additionally, India’s Department of Science and Technology reported that radar-based security systems are increasingly being deployed at critical infrastructure sites such as airports and power plants to enhance situational awareness and threat detection.

MARKET DRIVERS

Expansion of Autonomous and Advanced Driver Assistance Systems (ADAS)

One of the most significant drivers of the Asia Pacific radar sensor market is the rapid expansion of autonomous vehicles and Advanced Driver Assistance Systems (ADAS). Radar sensors play a crucial role in enabling features such as adaptive cruise control, blind-spot detection, automatic emergency braking, and parking assistance by providing real-time object detection and distance measurement. In South Korea, the Korea Automotive Technology Institute reports that over 70% of mid to high-end passenger vehicles launched since 2022 include multiple radar sensors for enhanced road safety. Similarly, in Japan, the Society of Automotive Engineers notes that major automakers like Toyota and Honda have increased their average radar sensor count per vehicle from two in 2020 to five in 2023. The Chinese government's push toward intelligent transportation systems, supported by subsidies for electric and autonomous vehicles, has further accelerated this trend.

Rising Demand for Surveillance and Security Applications

Another major driver fueling the growth of the radar sensor market in the Asia Pacific is the increasing demand for surveillance and security applications across both public and private sectors. Governments and enterprises are investing heavily in advanced radar-based monitoring systems to enhance national security, border control, airport surveillance, and critical infrastructure protection. According to the United Nations Office on Drugs and Crime, regional defense spending in the Asia Pacific exceeded USD 600 billion in 2023, with a significant portion allocated to modernizing radar-based command and control systems. In India, the Ministry of Home Affairs has mandated the installation of radar-equipped surveillance systems along international borders to detect unauthorized movements. Additionally, as per Deloitte, the number of commercial buildings integrating radar-enhanced perimeter security systems in Singapore grew by 35% in 2023 compared to the previous year.

MARKET RESTRAINTS

High Cost of Advanced Radar Sensor Integration

One of the primary restraints affecting the Asia Pacific radar sensor market is the high cost associated with the development, manufacturing, and integration of advanced radar systems. High-performance radar sensors, particularly those operating in millimeter-wave frequencies used in automotive and defense applications, require complex semiconductor materials, precision components, and extensive calibration, all of which contribute to elevated production costs. According to McKinsey & Company, the bill of materials for a mid-range automotive radar sensor exceeds USD 150, making it a significant component of overall vehicle electronics expenditure. Additionally, as per PwC, small and medium-sized enterprises involved in drone technology or industrial automation frequently opt for alternative sensing technologies such as LiDAR or ultrasonic sensors due to lower upfront investment requirements. These economic barriers hinder widespread adoption and limit market penetration in price-sensitive segments across the Asia Pacific.

Regulatory and Spectrum Allocation Challenges

A significant restraint impacting the Asia Pacific radar sensor market is the complexity surrounding regulatory compliance and spectrum allocation policies across different countries. Radar sensors operate within specific frequency bands, and regulatory authorities impose strict licensing conditions to prevent interference with other communication systems such as aviation radars, weather forecasting systems, and military operations. According to the International Telecommunication Union, spectrum regulations vary widely across the region creating challenges for manufacturers seeking to deploy standardized radar solutions.

In India, the Telecom Regulatory Authority mandates that companies using radar sensors above certain frequency thresholds must obtain spectrum usage licenses, which can take up to six months to process. As per the Confederation of Indian Industry, delays in regulatory approvals have caused project setbacks for firms developing autonomous vehicle testing facilities. Moreover, as per GSMA Intelligence, inconsistent spectrum policies across ASEAN nations complicate cross-border scalability for radar-based applications such as smart transportation and drone logistics.

MARKET OPPORTUNITIES

Adoption of Radar Sensors in Industrial Automation and Robotics

A promising opportunity emerging in the Asia Pacific radar sensor market is the increasing adoption of radar-based sensing technologies in industrial automation and robotics. The need for reliable, real-time object detection and motion tracking has surged as industries shift toward smart manufacturing, automated guided vehicles (AGVs), and robotic process automation. According to McKinsey Global Institute, the industrial automation market in the Asia Pacific is projected to expand at a compound annual growth rate of 12% through 2028, which is driven primarily by investments in robotics and AI-driven control systems. In Japan, the Robot Revolution Initiative Council reports that over 90% of newly deployed AGVs in automotive and electronics manufacturing facilities now incorporate radar-based obstacle detection mechanisms.

Integration of Radar Sensors in Smart Cities and Intelligent Transportation Systems

An emerging opportunity in the Asia Pacific radar sensor market is the integration of radar-based sensing systems into smart city initiatives and intelligent transportation networks. Governments across the region are investing heavily in urban digitization projects aimed at improving traffic management, reducing congestion, and enhancing road safety through real-time data collection and analytics. Radar sensors, known for their ability to accurately track movement and speed, are playing a pivotal role in these developments.

According to the World Bank, over 40 cities in the Asia Pacific have implemented intelligent transport systems incorporating radar-based traffic monitoring solutions since 2021. In Singapore, the Land Transport Authority has deployed Doppler radar sensors at major intersections to optimize signal timing based on real-time traffic flow, resulting in a 20% improvement in peak-hour efficiency. Similarly, in China, the Ministry of Transport reports that more than 200 smart highways now utilize roadside radar units to monitor vehicle speeds, detect anomalies, and support autonomous vehicle navigation. Additionally, as per JTC Corporation in Malaysia, radar-based pedestrian detection systems have been installed in Kuala Lumpur’s central business district to enhance crosswalk safety.

MARKET CHALLENGES

Technological Limitations in Miniaturization and Power Efficiency

One of the foremost challenges facing the Asia Pacific radar sensor market is the difficulty in achieving optimal miniaturization and power efficiency without compromising performance. While there is growing demand for compact, energy-efficient radar sensors in applications such as wearables, drones, and Internet of Things (IoT) devices, current technological limitations make it challenging to scale down radar modules while maintaining high-resolution detection and long-range capabilities. In Japan, the Semiconductor Business Unit of Renesas Electronics notes that developers working on compact radar sensors for wearable health monitoring face significant trade-offs between battery life and sensing resolution. Moreover, as per IEEE Spectrum, the thermal dissipation issues associated with high-frequency radar chips pose additional design complexities, especially in densely packed electronic systems.

Interference and Signal Noise in Dense Urban Environments

Another critical challenge confronting the Asia Pacific radar sensor market is the issue of interference and signal noise in densely populated urban environments. The likelihood of electromagnetic interference affecting radar sensor performance increases significantly as the number of wireless communication systems including Wi-Fi, Bluetooth, 5G, and satellite networks continues to rise. According to the International Telecommunication Union, co-channel interference and multipath propagation are becoming more pronounced in metropolitan areas, leading to degraded radar accuracy and reliability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 16.07% |

| Segments Covered | By Type, Range, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of Asia-Pacific |

| Market Leaders Profiled | NXP Semiconductors, Infineon Technologies, Texas Instruments, Robert Bosch GmbH, Denso Corporation, Continental AG, Autoliv Inc., Aptiv PLC, ZF Friedrichshafen AG, Mitsubishi Electric Corporation |

SEGMENTAL ANALYSIS

By Type Insights

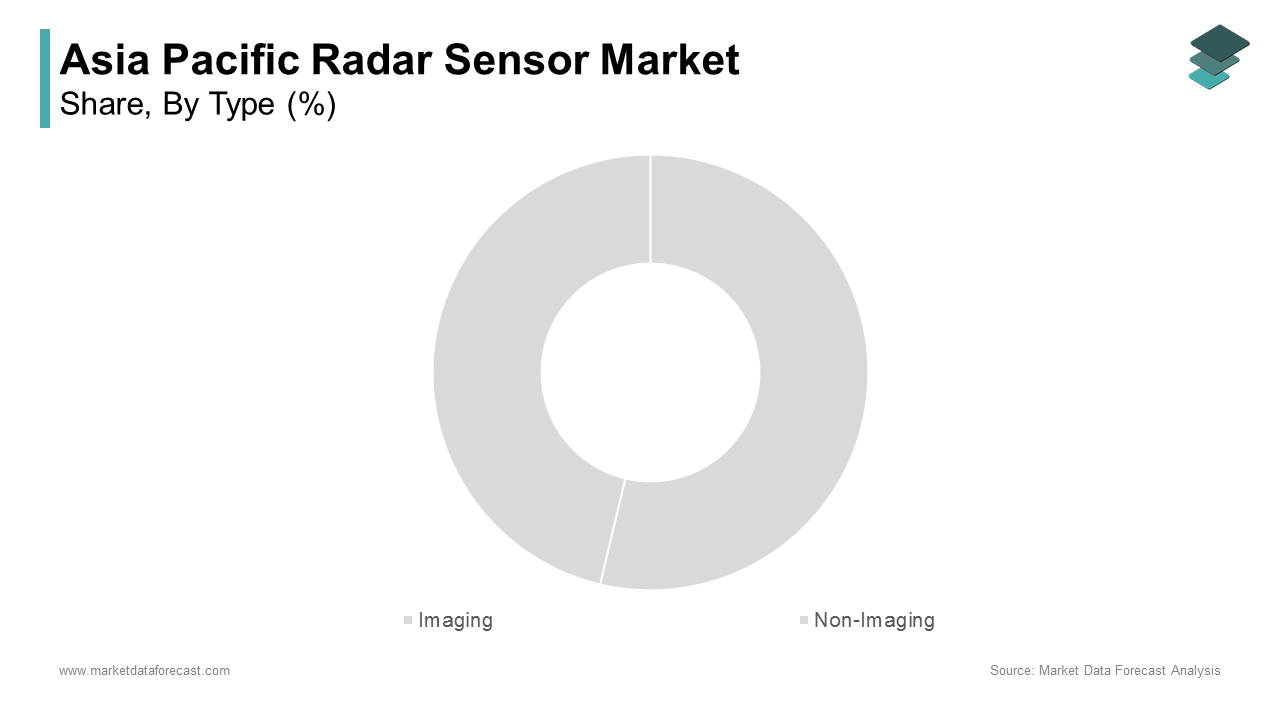

The non-imaging radar sensor segment dominated the Asia Pacific market by accounting for 58.4% of share in 2024 with the widespread use of non-imaging radar systems in automotive applications such as adaptive cruise control, blind spot detection, and automatic emergency braking. These sensors offer cost-effective solutions with high reliability by making them a preferred choice for mass-market vehicle models.

According to McKinsey Global Institute, over 60% of new passenger vehicles produced in Japan now include at least four non-imaging radar sensors per unit. In China, the Ministry of Industry and Information Technology reported that domestic automakers integrated more than 45 million non-imaging radar units into new vehicles in 2023 alone. Additionally, South Korea’s Automotive Technology Association noted that local manufacturers have increasingly adopted 24 GHz and 77 GHz short-range radars due to their compatibility with existing ADAS architectures.

The imaging radar sensor segment is swiftly emerging with a CAGR of 14.6% from 2025 to 2033. Unlike traditional non-imaging counterparts, imaging radar sensors provide higher resolution, enabling detailed object classification and enhanced situational awareness, which is crucial for autonomous driving and advanced driver assistance systems (ADAS). According to Frost & Sullivan, demand for imaging radar has surged in India and Southeast Asia due to rising investments in intelligent transportation infrastructure and vehicle electrification. As reported by the Korea Electronics Technology Institute, South Korean automakers are accelerating the integration of 4D imaging radar into premium electric vehicles to support Level 3 autonomy.

By Range Insights

The range radar (SRR) sensors segment was the largest capturing 53.1% of the Asia Pacific radar sensor market share in 2024 with the extensive use of SRR sensors in automotive safety systems such as parking assistance, lane change detection, and collision avoidance. Their compact size, lower cost, and ability to operate effectively in congested urban environments make them highly suitable for mass-market applications. According to the Japan Automobile Manufacturers Association, over 90% of newly launched compact and mid-sized cars in Japan now feature multiple SRR units for enhanced road safety. Similarly, in China, the Society of Automotive Engineers of China reported that domestic automakers installed more than 60 million short-range radar units in 2023, primarily for entry-level and mid-tier vehicles. In India, the Automotive Research Association notes that regulatory mandates requiring rear parking sensors in all new passenger vehicles have significantly boosted SRR adoption.

The Long-range radar (LRR) sensors segment is likely to grow with an anticipated CAGR of 13.9% from 2025 to 2033. LRR sensors are critical components in highway driving scenarios, where accurate detection of distant objects is essential for features like adaptive cruise control and forward collision warning systems. In addition, the Indian Ministry of Defence has deployed long-range radar systems along key border regions to enhance surveillance capabilities. According to Deloitte, commercial aviation and maritime sectors in Australia are also adopting LRR for real-time tracking of

By Application Insights

The automotive sector was the largest in the Asia Pacific radar sensor market with 47.4% of share in 2024 with the increasing integration of radar sensors in Advanced Driver Assistance Systems (ADAS) and autonomous vehicles. Governments across the region are enforcing stricter vehicle safety regulations by compelling automakers to adopt radar-based sensing solutions for features such as blind spot detection, adaptive cruise control, and automatic emergency braking.

According to the Japan Automobile Manufacturers Association, over 85% of new vehicles sold in Japan now include factory-fitted radar-based safety systems. In China, the Ministry of Industry and Information Technology reports that domestic automakers incorporated more than 70 million radar sensors into new car models in 2023 alone.

The traffic management and monitoring applications segment is likely to experience a CAGR of 15.2% from 2025 to 2033 with the increasing government investments in smart city initiatives and intelligent transportation systems aimed at reducing congestion, improving road safety, and enhancing traffic flow efficiency. In China, the Ministry of Transport reports that more than 200 smart highways now utilize roadside radar units to monitor vehicle speeds and detect anomalies. Similarly, in Malaysia, the Kuala Lumpur Smart City initiative has installed radar-based pedestrian detection systems to improve crosswalk safety.

REGIONAL ANALYSIS

China held the largest share in the Asia Pacific radar sensor market with 31.3% of share in 2024. The country’s dominant position stems from its robust automotive manufacturing base, aggressive push toward autonomous vehicle development, and extensive investment in defense modernization programs. According to the China Association of Automobile Manufacturers, domestic automakers integrated over 80 million radar sensors into new vehicles in 2023, reflecting the rapid adoption of ADAS features.

Japan was ranked second in the Asia Pacific radar sensor market with 18.3% of its share in 2024. The country maintains a strong presence due to its early adoption of advanced automotive radar systems, deep integration of radar in aerospace applications, and well-established electronics manufacturing ecosystem. According to the Japan Automobile Manufacturers Association, over 90% of new passenger vehicles sold in Japan in 2023 included multiple radar sensors for functions such as adaptive cruise control and autonomous parking. Companies such as Denso, Toyota, and Mitsubishi Electric have been pioneers in integrating high-resolution radar into next-generation autonomous vehicles.

South Korea is likely to have prominent growth opportunities throughout the forecast period owing to its cutting-edge automotive industry, active defense modernization programs, and early adoption of smart transportation infrastructure. A major growth catalyst is the collaboration between automotive giants like Hyundai and Samsung Electronics to develop next-generation radar solutions for autonomous driving.

India's radar sensor market is growing with the increasing government focus on digital infrastructure, vehicular safety regulations, and defense modernization. According to the Ministry of Road Transport and Highways, India mandated the inclusion of front and rear radar sensors in all new passenger vehicles starting in October 2023, which is boosting sensor adoption.

In the defense sector, the Ministry of Defence has been expanding its radar surveillance capabilities along international borders. As reported by the Defence Research and Development Organisation, over 150 mobile radar units were deployed in border areas between 2021 and 2023. Additionally, the rise of electric and connected vehicles is creating new demand for radar-based safety features. The Indian automotive industry, supported by policies under the Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme, is increasingly integrating radar sensors into both internal combustion engines and electric vehicles.

Australia's radar sensor market is gearing up with significant investments in defense infrastructure and intelligent transportation systems. A key factor behind the market expansion is the growing integration of radar sensors in traffic monitoring and road safety applications. As reported by the Australian Road Research Board, several state governments have implemented radar-based traffic flow optimization systems in major cities such as Sydney and Melbourne. These systems help reduce congestion and enhance road safety through real-time data analytics. Additionally, the mining and logistics sectors are adopting radar-enabled automation solutions to improve operational efficiency and worker safety.

LEADING PLAYERS IN THE ASIA PACIFIC RADAR SENSOR MARKET

Robert Bosch GmbH

Bosch is a leading force in the Asia Pacific radar sensor market in automotive applications. The company has been at the forefront of developing high-performance radar solutions for Advanced Driver Assistance Systems (ADAS) and autonomous driving technologies. Bosch plays a crucial role in shaping vehicle safety standards, with strong partnerships across the region’s automotive industry, Its innovation in millimeter-wave radar technology has enabled precise object detection and enhanced road safety. The company's continuous R&D efforts and localized manufacturing facilities have strengthened its presence in key markets like China, Japan, and India.

Denso Corporation

Denso has established itself as a dominant player in the Asia Pacific radar sensor landscape, especially within the automotive sector. Known for integrating radar systems into next-generation mobility platforms, the company collaborates closely with major automakers to deliver cutting-edge ADAS features. Denso's expertise lies in designing compact, high-resolution radar units that support autonomous driving functions.

Mitsubishi Electric Corporation

Mitsubishi Electric is a key participant in the radar sensor market, offering advanced solutions for both defense and civilian applications. The company specializes in high-precision radar systems used in air traffic control, maritime navigation, and urban security monitoring. In addition to its aerospace and defense contributions, Mitsubishi Electric has expanded into automotive radar technologies, aligning with evolving mobility trends. Its focus on system integration and AI-driven signal processing has positioned it as a trusted provider of radar-based infrastructure solutions across the Asia Pacific.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies adopted by key players in the Asia Pacific radar sensor market is technology innovation and product differentiation, where companies continuously develop advanced radar systems with higher accuracy, lower latency, and improved environmental adaptability. Another significant approach is strategic collaborations and joint ventures with local manufacturers, research institutions, and government agencies to accelerate the adoption of emerging applications such as autonomous vehicles and smart infrastructure. Additionally, market localization and supply chain optimization are widely pursued by allowing firms to tailor products to regional regulatory requirements while enhancing distribution efficiency and reducing time-to-market.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the Asia Pacific radar sensor market include NXP Semiconductors, Infineon Technologies, Texas Instruments, Robert Bosch GmbH, Denso Corporation, Continental AG, Autoliv Inc., Aptiv PLC, ZF Friedrichshafen AG, Mitsubishi Electric Corporation.

The competition in the Asia Pacific radar sensor market is highly dynamic, driven by rapid technological advancements, increasing demand from automotive and defense sectors, and growing investments in intelligent infrastructure. A mix of global leaders and regional specialists coexists, each striving to capture market share through innovation, strategic partnerships, and localized offerings. Automotive OEMs and Tier-1 suppliers are aggressively integrating radar sensors into new vehicle models to meet rising consumer expectations for safety and autonomy. At the same time, defense and aerospace organizations are expanding their use of radar-based surveillance and tracking systems to enhance national security. Emerging economies are witnessing increased participation from domestic electronics manufacturers seeking to develop indigenous radar capabilities. This competitive environment fosters continuous evolution, pushing companies to differentiate through technical excellence, application-specific customization, and end-to-end system integration.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Bosch announced a collaboration with NIO, a leading Chinese electric vehicle manufacturer, to integrate Bosch’s latest generation of long-range radar sensors into upcoming EV models. This partnership aims to enhance autonomous driving capabilities and strengthen Bosch’s foothold in China’s rapidly expanding ADAS market.

- In June 2023, Denso launched a new line of compact 4D imaging radar systems designed specifically for urban autonomous mobility applications in Japan. This initiative was intended to support the deployment of self-driving taxis and advanced driver assistance features tailored to dense city environments.

- In November 2023, Mitsubishi Electric partnered with the Indian Space Research Organisation (ISRO) to supply high-precision radar equipment for satellite tracking and space situational awareness. The collaboration aimed to bolster India’s indigenous radar capabilities in aerospace and defense domains.

- In March 2024, Hyundai Mobis introduced an integrated radar-camera fusion system developed in-house for deployment in South Korean-made premium vehicles. This move was aimed at enhancing ADAS performance and reducing reliance on foreign suppliers for critical sensor technologies.

- In August 2023, Infineon Technologies expanded its semiconductor manufacturing facility in Singapore to increase production capacity for radar sensor chips used in automotive and industrial applications. This investment was intended to support the rising demand for radar-based systems across the Asia Pacific region.

MARKET SEGMENTATION

This research report on the Asia Pacific Radar Sensor Market has been segmented and sub-segmented based on type, range, application, and region.

By Type

- Imaging

- Non-Imaging

By Range

- Short Range

- Medium Range

- Long Range

By Application

- Automotive

- Aerospace and Defense

- Environment and Weather Monitoring

- Traffic Management and Monitoring

- Others

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. How are radar sensors used in automotive applications?

Radar sensors support collision avoidance, adaptive cruise control, lane change assistance, and parking assistance in modern vehicles.

2. What is driving the growth of the radar sensor market in Asia Pacific?

The growth is driven by rising demand for advanced driver-assistance systems (ADAS), increasing focus on vehicle safety, industrial automation, and expanding defense applications.

3. Who are the key market players in the Asia Pacific radar sensor market?

Key players include NXP Semiconductors, Infineon Technologies, Texas Instruments, Robert Bosch GmbH, and Denso Corporation.

4. Which countries are major contributors to the Asia Pacific radar sensor market?

China, Japan, South Korea, and India are the leading contributors due to their growing automotive, electronics, and defense sectors.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com