Asia Pacific Radiation Hardened Electronics Market Size, Share, Growth, Trends, and Forecast Report – Segmented By Component (Mixed Signal ICs, Processors & Controllers, Memory, Power Management), Manufacturing Techniques, and Region (India, China, Japan, South Korea, Australia & New Zealand, Thailand) - Industry Analysis from 2026 to 2034

Market Size, 2025

$313 MnMarket Estimate, 2026

$331 MnMarket Forecast, 2034

$517 MnCAGR, 2026–2034

5.71%Asia Pacific Radiation Hardened Electronics Market Size

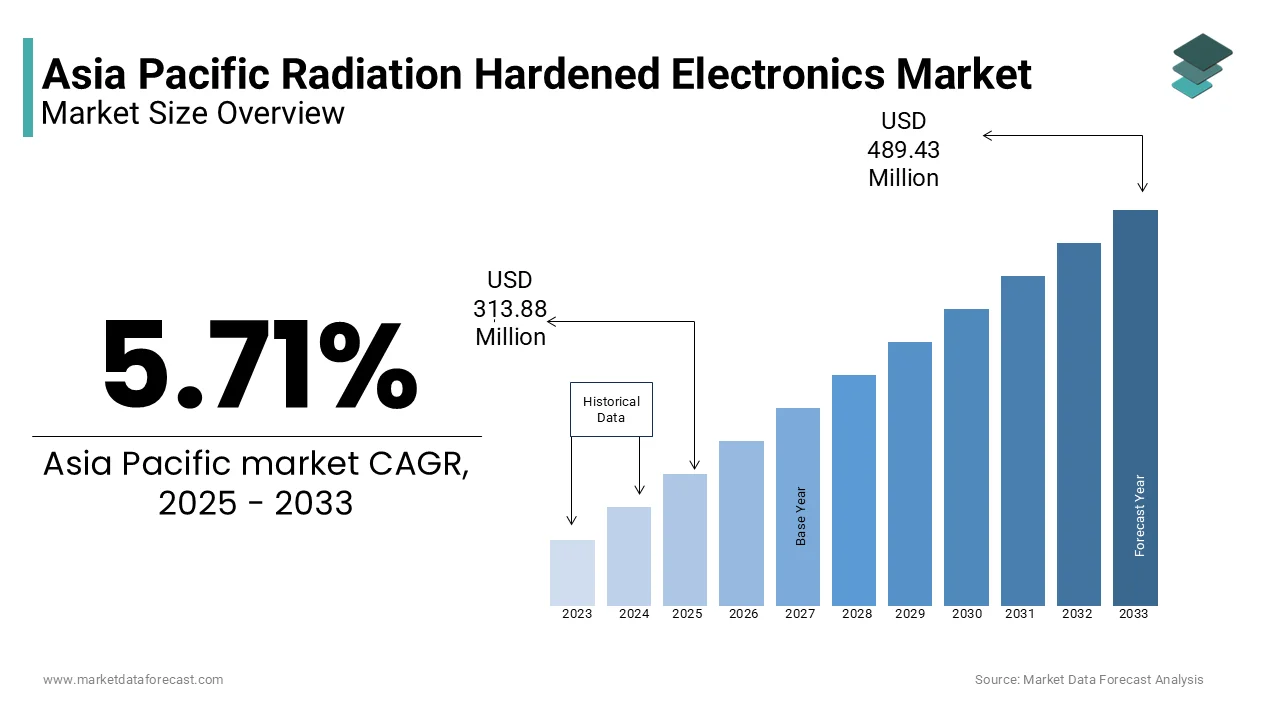

Asia Pacific radiation hardened electronics market size was valued at USD 313.88 million in 2025, and is expected to reach USD 517.37 billion by 2034 from USD 331.80 million in 2026. The market's promising CAGR for the predicted period is 5.71%.

The Asia Pacific radiation hardened electronics market encompasses electronic components and systems designed to withstand extreme radiation environments without performance degradation. These specialized electronics are critical for applications in space exploration, satellite communication, nuclear power plants, defense systems, and high-altitude aviation—sectors where exposure to ionizing radiation can cause data corruption, circuit disruption, or total device failure. Radiation hardening techniques include material engineering, shielding, redundancy design, and advanced semiconductor processing.

MARKET DRIVERS

Expansion of Space Exploration Programs Across the Region

One of the primary drivers of the Asia Pacific radiation hardened electronics market is the significant expansion of space exploration initiatives undertaken by both government agencies and private enterprises. Countries like China, India, and Japan are increasingly investing in satellite constellations, lunar missions, and deep-space research, all of which require highly reliable electronic systems capable of functioning in high-radiation environments. According to Euroconsult, in 2023, Asia Pacific accounted for nearly one-third of all satellite launches worldwide, highlighting the rapid pace of space activity in the region. China’s Tiangong space station program and its planned Mars sample return mission have spurred demand for advanced radiation-tolerant microprocessors and memory units. Similarly, India's Chandrayaan-3 lunar mission and upcoming Aditya-L1 solar observatory required extensive integration of radiation-hardened components to withstand harsh extraterrestrial conditions. As per the Indian Space Research Organisation, over 80% of onboard electronics used in recent interplanetary missions were sourced from domestic or regional suppliers specializing in radiation-hardened technologies. Furthermore, the rise of commercial space startups in South Korea and Singapore is contributing to this trend, fostering innovation in compact, cost-effective hardened solutions.

Increasing Defense Modernization and Missile Program Development

Increasing Defense Modernization and Missile Program Development

A crucial driver fueling the Asia Pacific radiation hardened electronics market is the ongoing modernization of defense systems, particularly in missile guidance, radar technology, and electronic warfare platforms. Radiation-hardened components play a vital role in ensuring operational integrity under extreme electromagnetic pulses (EMPs) and nuclear threat scenarios. India's Agni-V intercontinental ballistic missile and China's DF-41 long-range missile systems incorporate hardened electronics to ensure reliability during high-altitude flight and potential EMP exposure. Japan and South Korea are also enhancing their missile defense capabilities through partnerships with U.S.-based defense contractors, integrating ruggedized components into early-warning systems and airborne surveillance platforms. As per the Asian Defense Review, approximately 60% of newly deployed missile systems in the region since 2022 have embedded radiation-resistant processors for command and control functions. Moreover, defense forces in Australia and Indonesia are upgrading electronic warfare suites in naval and aerial fleets, further driving demand for hardened microelectronics.

MARKET RESTRAINTS

High Cost and Long Development Cycles of Radiation-Hardened Components

One of the most significant restraints affecting the Asia Pacific radiation hardened electronics market is the prohibitively high cost and extended development timelines associated with these components. Unlike standard semiconductors, radiation-hardened devices require specialized manufacturing processes, including silicon-on-insulator (SOI) substrates, triple-well isolation, and redundant logic circuits—all of which significantly increase production complexity and unit costs. According to McKinsey & Company, the average development cycle for a radiation-hardened integrated circuit extends beyond three years, compared to less than a year for commercial-grade chips. In addition, testing and qualification procedures for radiation tolerance add further delays and expenses. Military and aerospace standards such as MIL-STD-883 and ECSS-Q-ST-60-15 mandate rigorous environmental simulations, including neutron and gamma-ray exposure tests, which must be conducted in specialized laboratories. This financial and temporal burden deters smaller manufacturers and startups from entering the market, limiting competition and slowing down innovation cycles.

Limited Local Manufacturing Capabilities and Technology Transfer Barriers

Another pressing constraint in the Asia Pacific radiation hardened electronics market is the limited availability of indigenous manufacturing infrastructure and the challenges surrounding technology transfer. While countries like China and Japan possess advanced semiconductor fabrication facilities, many other nations in the region lack the necessary cleanrooms, wafer-processing equipment, and technical expertise to produce radiation-resistant components at scale. Moreover, export controls imposed by Western governments on dual-use technologies restrict access to cutting-edge radiation-hardening methodologies, limiting regional players' ability to develop competitive products independently.

MARKET OPPORTUNITIES

Growth in Commercial Satellite and LEO Constellation Deployments

An expanding opportunity within the Asia Pacific radiation hardened electronics market is the surge in commercial satellite launches and the development of Low Earth Orbit (LEO) mega-constellations. Private space firms and government-backed entities are deploying large-scale satellite networks for global broadband internet, remote sensing, and IoT connectivity, all of which require radiation-tolerant electronics to maintain operational stability in orbit. Furthermore, governments in Malaysia and Thailand are exploring satellite-based disaster monitoring networks, requiring robust electronics to function reliably in the Van Allen belts’ radiation zones.

Rising Demand for Radiation-Tolerant Electronics in Nuclear Power Plants

Another significant opportunity in the Asia Pacific radiation hardened electronics market comes from the expanding nuclear energy sector, which requires highly resilient electronic components for reactor control, instrumentation, and safety systems. With numerous new nuclear power plants under construction across China, India, South Korea, and Pakistan, there is a growing need for electronic systems capable of operating in high-dose radiation environments without compromising functionality. According to the International Atomic Energy Agency, Asia Pacific accounted for a significant share of all new nuclear reactors under construction globally in 2023. These reactors rely extensively on radiation-hardened programmable logic controllers (PLCs), digital protection relays, and sensor interfaces to manage core operations and emergency shutdown protocols. For instance, China’s CAP1400 reactor projects integrate hardened microcontrollers to ensure fail-safe operation under extreme conditions. As per the World Nuclear Association, India alone plans to deploy 21 new reactors by 2031, each requiring extensive use of hardened electronics in monitoring and automation systems. Also, aging nuclear facilities in Japan and South Korea undergoing modernization are retrofitting their control rooms with solid-state, hardened instrumentation panels.

MARKET CHALLENGES

Rapid Evolution of Radiation Tolerance Requirements

One of the foremost challenges facing the Asia Pacific radiation hardened electronics market is the continuously evolving nature of radiation tolerance requirements driven by advancements in aerospace, defense, and nuclear technologies. As spacecraft operate at higher altitudes and in deeper orbits, they encounter increased levels of cosmic rays, solar flares, and single-event effects (SEEs), necessitating constant updates to radiation mitigation strategies. According to NASA’s Jet Propulsion Laboratory, newer radiation-induced failure modes such as latch-up and bit flips are becoming more prevalent in nanoscale CMOS technologies, challenging traditional hardening approaches. Manufacturers must therefore invest heavily in adaptive design methodologies, predictive modeling, and simulation software to stay ahead of these changing benchmarks.

Talent Shortage and Specialized Knowledge Gaps

A critical challenge confronting the Asia Pacific radiation hardened electronics market is the scarcity of skilled professionals equipped to design, fabricate, and validate radiation-resistant components. The niche nature of radiation hardening—requiring expertise in physics, materials science, semiconductor engineering, and aerospace systems—makes it difficult to attract and retain qualified personnel. According to the IEEE, as of 2023, less number of electrical engineering graduates in the Asia Pacific region had exposure to radiation effects in electronics, creating a skills gap that hinders industry growth. Universities and research institutions in Japan and South Korea have made strides in offering specialized courses in radiation-tolerant design, but similar programs remain limited in other parts of the region. Large corporations like Mitsubishi Electric and Renesas have established internal training programs to address the shortage, yet the reliance on a small pool of experts constrains scalability. Moreover, defense and space agencies struggle to compete with commercial tech firms for talent, exacerbating recruitment challenges.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.71% |

| Segments Covered | By Component, Manufacturing Techniques, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of Asia-Pacific |

| Market Leaders Profiled | Renesas Electronics Corporation, STMicroelectronics N.V., Infineon Technologies AG, Texas Instruments, Inc., Microchip Technology, Inc., Teledyne Technologies, Inc., Honeywell International, Inc., BAE Systems PLC, Xilinx, Inc., and TTM Technologies, Inc, and others |

SEGMENTAL ANALYSIS

By Component Insights

The processors and controllers segment represent the largest category in the Asia Pacific radiation hardened electronics market by accounting for a 38.6% of total revenue in 2025. These components serve as the central processing units in critical aerospace and defense systems, responsible for executing commands, managing data flow, and ensuring system reliability even under high-radiation conditions. According to Yole Développement, more than 60% of newly launched satellites in 2023 integrated advanced radiation-hardened microprocessors to support autonomous decision-making capabilities. The increasing complexity of onboard computing in space missions is a major driver. China’s Tiangong space station and India’s Chandrayaan-3 lunar mission both required robust processors to manage navigation, communication, and scientific instrumentation in harsh extraterrestrial environments. As per the Indian Space Research Organisation, over 75% of onboard control systems in recent interplanetary probes relied on indigenous or regionally sourced radiation-hardened processors. In addition, military applications such as missile guidance, radar processing, and electronic warfare further amplify demand.

Power management ICs are emerging as the fastest-growing segment within the Asia Pacific radiation hardened electronics market, projected to expand at a compound annual growth rate (CAGR) of 14.9%. This rapid progress is attributed to the rising need for efficient energy regulation in small satellites, CubeSats, and long-duration space missions where power conservation is paramount. Modern spacecraft increasingly rely on solar arrays and battery-based energy storage, requiring sophisticated voltage regulators, DC/DC converters, and thermal protection circuits that can withstand ionizing radiation. Japanese firm Mitsubishi Electric has developed hardened power ICs specifically for use in JAXA’s upcoming lunar exploration modules, aiming to improve energy efficiency while maintaining operational stability.

Moreover, defense forces across the region are adopting hardened power management units in unmanned aerial vehicles (UAVs) and hypersonic weapons, where compact, resilient electronics are essential. As per the Asian Defense Review, around 45% of UAVs deployed by Southeast Asian militaries since 2022 incorporated hardened power ICs, underscoring the sector's growing strategic importance in regional security architectures.

By Manufacturing Techniques Insights

The radiation-Hardened by Design (RHBD) segment accounted for the largest share of the Asia Pacific radiation hardened electronics market by capturing 62.5% of total revenue in 2025. Unlike post-fabrication hardening techniques, RHBD integrates protective measures directly into the semiconductor design phase, offering superior resilience against single-event upsets (SEUs), latch-up, and total ionizing dose (TID) effects. One key driver of RHBD’s dominance is its widespread adoption in modern spacecraft and launch vehicles where miniaturization and weight reduction are crucial. China’s Long March rocket series and India’s GSLV Mk III launchers utilize RHBD-based processors and memory units to ensure reliable performance in high-altitude radiation zones. Furthermore, defense manufacturing centers in Japan and South Korea have embraced RHBD for next-generation fighter jets, stealth drones, and missile guidance systems, which require real-time processing in high-radiation battlefield scenarios.

The Radiation-Hardened by Process (RHBP) is the fastest-growing segment in the Asia Pacific radiation hardened electronics market, anticipated to grow at a CAGR of 13.6%. This technique involves modifying semiconductor fabrication processes—such as using silicon-on-insulator (SOI), deep trench isolation, and epitaxial layers—to inherently enhance resistance to radiation-induced failures. A primary catalyst driving RHBP adoption is the rise in commercial satellite constellations, including those used for broadband internet and Earth observation. As per the Asia-Pacific Space Cooperation Organization, nearly 50% of new low-Earth orbit (LEO) satellites launched in 2023 featured RHBP-integrated subsystems for improved durability. Also, nuclear power plants in India and South Korea are incorporating RHBP logic circuits into reactor control and monitoring systems to prevent signal corruption caused by gamma radiation.

REGIONAL ANALYSIS

China held the largest share of the Asia Pacific radiation hardened electronics market by contributing a 34.6% of total revenue in 2025. As a global leader in space exploration and defense modernization, the country benefits from a well-established aerospace industry, substantial government funding, and state-backed semiconductor development initiatives. The Chinese Ministry of Industry and Information Technology has prioritized self-reliance in strategic electronics through its Made in China 2026 program, encouraging domestic firms to develop radiation-resistant components for military and civil space applications. In 2023 alone, China launched over 60 orbital rockets, including multiple missions to Low Earth Orbit and Geostationary Transfer Orbit, all requiring hardened processors and memory units.

India is positioning itself as a rapidly growing participant due to its expanding space program and indigenous defense electronics development. The Indian Space Research Organisation (ISRO) plays a central role in driving demand, with recent interplanetary missions such as Chandrayaan-3 and Aditya-L1 relying heavily on domestically manufactured radiation-tolerant components. The Indian government has also intensified its focus on self-reliance in defense electronics under the Atmanirbhar Bharat initiative, leading to increased procurement of hardened components for missile systems like Agni-V and BrahMos. The Defence Research and Development Organisation (DRDO) has established specialized laboratories focused on radiation effects testing, accelerating product validation and deployment cycles.

Japan is a technological innovation leader in the Asia Pacific radiation hardened electronics market which is distinguished by its strong industrial base and leadership in semiconductor innovation. The country excels in developing high-performance radiation-tolerant components tailored for aerospace, robotics, and nuclear energy applications. According to the Japan Aerospace Exploration Agency (JAXA), Japanese-made radiation-hardened processors have been successfully integrated into multiple lunar and planetary exploration missions, demonstrating reliability in extreme radiation environments. Japanese firms such as Renesas Electronics and Mitsubishi Electric have pioneered RHBD and RHBP fabrication techniques that enable high-density, low-power consumption chips for space-grade applications. In 2023, Renesas partnered with JAXA to develop hardened microcontrollers for Japan’s upcoming Smart Lander for Investigating Moon (SLIM) mission, highlighting the country’s technological prowess in this niche domain. In addition to space exploration, Japan’s nuclear infrastructure relies extensively on hardened electronics for reactor control and emergency shutdown systems. As part of its broader smart manufacturing strategy, the Japanese government continues to provide incentives for companies engaged in radiation-hardened semiconductor R&D, reinforcing its position as a key innovator in the Asia Pacific market.

South Korea is leveraging its strong electronics manufacturing infrastructure and growing strategic investments in aerospace and defense. The country’s defense modernization programs, including the development of precision-guided missiles and surveillance satellites, have significantly boosted demand for hardened components. According to the South Korean Defense Acquisition Program Administration, over 40% of newly deployed missile systems since 2022 included radiation-resistant processors for improved performance in high-altitude and EMP-prone environments. South Korea is also expanding its commercial space ambitions, with the Korea Aerospace Research Institute (KARI) launching several satellites equipped with hardened electronics. The Nuri rocket program, which entered full operational capacity in 2023, incorporates domestically produced radiation-tolerant avionics to support future lunar and deep-space missions.

Australia is playing a strategic role as a partner in defense and space collaborations with the United States, Japan, and other regional allies. The country’s relatively small but highly specialized defense and aerospace sector drives demand for hardened components used in satellite communications, airborne reconnaissance, and maritime electronic warfare platforms. Australia’s participation in the U.S.-led Operation Olympic Defender and its involvement in the OneWeb satellite constellation project have reinforced the need for radiation-tolerant components in high-altitude and space-bound applications. Also, the Australian Space Agency has been actively supporting domestic startups and research institutions in developing hardened microelectronics for future space missions.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific radiation hardened electronics market is characterized by a blend of state-backed enterprises, established semiconductor manufacturers, and emerging regional players striving to secure strategic dominance. While global firms maintain strong footholds through decades of experience and technological leadership, local companies are increasingly investing in indigenous development to meet rising demand from defense and space sectors. The market is marked by intense R&D activity, with participants focusing on innovation in radiation mitigation techniques such as RHBD and RHBP to enhance device resilience. Strategic alliances between governments, academic institutions, and private firms are shaping the competitive landscape, enabling localized production and reducing reliance on imported components. Additionally, export restrictions on dual-use technologies have prompted several countries to accelerate domestic capabilities in radiation-hardened chip design and manufacturing.

KEY MARKET PLAYERS

Renesas Electronics Corporation, STMicroelectronics N.V., Infineon Technologies AG, Texas Instruments, Inc., Microchip Technology, Inc., Teledyne Technologies, Inc., Honeywell International, Inc., BAE Systems PLC, Xilinx, Inc., and TTM Technologies, Inc. are playing dominating role in the Asia Pacific radiation hardened electronics market.

TOP PLAYERS IN THE MARKET

- Toshiba plays a pivotal role in the Asia Pacific radiation hardened electronics market through its development of advanced semiconductor technologies tailored for aerospace and nuclear applications. The company’s expertise lies in designing resilient memory components and power management systems that operate reliably in high-radiation environments. Toshiba has supported numerous space missions with its specialized ICs and continues to collaborate with Japanese and international agencies on satellite and reactor safety systems.

- Mitsubishi Electric is a key player known for supplying high-performance radiation-hardened electronic modules for defense, space exploration, and industrial control systems. The company integrates cutting-edge design methodologies to ensure component durability under extreme radiation exposure. Mitsubishi Electric has been instrumental in equipping Japan's major space programs with hardened processors and communication units, contributing significantly to mission success and system longevity.

- As a leading institution within India’s space program, ISRO Satellite Centre plays a critical role in advancing domestic radiation hardened electronics. ISAC collaborates closely with Indian research bodies and semiconductor firms to develop indigenous components that reduce dependency on foreign suppliers. Its work spans processor design, memory architecture, and sensor integration for satellites and deep-space probes, positioning India as a growing force in the global radiation-hardened electronics landscape.

TOP STRATEGIES USED BY KEY PLAYERS

One major strategy employed by key players is deep collaboration with government and defense agencies to align product development with national security and space exploration priorities. Companies actively engage in joint R&D initiatives to customize radiation-hardened solutions for specific military and aerospace applications.

Another crucial approach is investment in proprietary design and fabrication technologies , including RHBD and RHBP methodologies. By enhancing in-house capabilities in radiation-tolerant chip manufacturing, firms ensure long-term competitiveness and compliance with evolving mission requirements.

Lastly, expanding partnerships across academia and emerging tech startups allows market leaders to accelerate innovation cycles and tap into new design paradigms.

RECENT HAPPENINGS IN THE MARKET

- In March 2025, Toshiba announced a collaborative initiative with JAXA to develop next-generation radiation-hardened memory modules designed specifically for use in lunar orbiters and deep-space probes. This partnership aims to improve data retention and reliability in extreme radiation conditions encountered beyond Low Earth Orbit.

- In May 2025, Mitsubishi Electric launched a new internal division focused exclusively on RHBD-based microprocessor development for future satellite constellations and hypersonic missile guidance systems, reinforcing its commitment to delivering high-reliability electronics for strategic applications.

- In August 2025, the Indian Space Research Organisation (ISRO) initiated a joint venture with Semiconductor Complex Limited (SCL) to scale up indigenous fabrication of radiation-hardened logic circuits, aiming to reduce dependence on foreign suppliers and strengthen self-reliance in mission-critical electronics.

- In October 2025, South Korea’s Hanwha Aerospace signed a technology-sharing agreement with a U.S.-based radiation-hardening firm to integrate hardened avionics into its next-generation reconnaissance satellites, enhancing operational reliability in contested electromagnetic environments.

- In December 2025, Australian startup Saber Astronautics partnered with the Australian Space Agency to establish a radiation-effects testing facility in Adelaide, aimed at supporting regional companies in validating their electronic components for space-bound and defense applications.

MARKET SEGMENTATION

This research report on the Asia Pacific Radiation Hardened Electronics market has been segmented and sub-segmented based on the following categories.

By Component

- Power Management

- Mixed Signal ICs

- Processors & Controllers

- Memory

By Manufacturing Technique

- Radiation-Hardening by Design (RHBD)

- Radiation-Hardening by Process (RHBP)

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What is the Asia Pacific radiation hardened electronics market?

The Asia Pacific radiation hardened electronics market comprises electronic components and systems designed to operate reliably in high-radiation environments such as space, defense, nuclear power, and aerospace applications.

2. What factors are driving the growth of the Asia Pacific radiation hardened electronics market?

The market is driven by increasing space exploration missions, rising defense modernization programs, expanding satellite deployments, and growing investments in nuclear energy infrastructure.

3. Which countries lead the Asia Pacific radiation hardened electronics market?

China, Japan, India, South Korea, and Australia are the leading markets due to their growing aerospace, defense, and space technology industries.

4. What are the major types of radiation hardened electronics?

The market includes radiation-hardened processors, memory devices, power management integrated circuits (PMICs), microcontrollers, field-programmable gate arrays (FPGAs), sensors, and analog components.

5. Which end-use industries generate the highest demand for radiation hardened electronics?

The aerospace, defense, satellite communications, nuclear energy, scientific research, and industrial sectors are the primary end users.

6. Why are radiation hardened electronics important?

Radiation hardened electronics are designed to withstand ionizing radiation and extreme environments, ensuring reliable performance, extended operational life, and mission-critical system safety.

7. What challenges does the Asia Pacific radiation hardened electronics market face?

The market faces challenges such as high development costs, complex manufacturing processes, stringent qualification standards, and limited production volumes.

8. How is the space industry influencing the Asia Pacific radiation hardened electronics market?

Increasing satellite launches, deep-space exploration missions, and investments in national space programs are driving demand for highly reliable radiation-resistant electronic components.

9. How are technological advancements shaping the radiation hardened electronics market?

Advancements in semiconductor fabrication, chip miniaturization, system-on-chip (SoC) technologies, and radiation-resistant design techniques are improving performance, reliability, and power efficiency.

10. What opportunities exist in the Asia Pacific radiation hardened electronics market?

Opportunities include expanding space programs, increasing defense budgets, growth in satellite communication networks, rising investments in nuclear power projects, and the development of next-generation aerospace technologies.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com