- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Asia Pacific Ring Main Unit Market Size

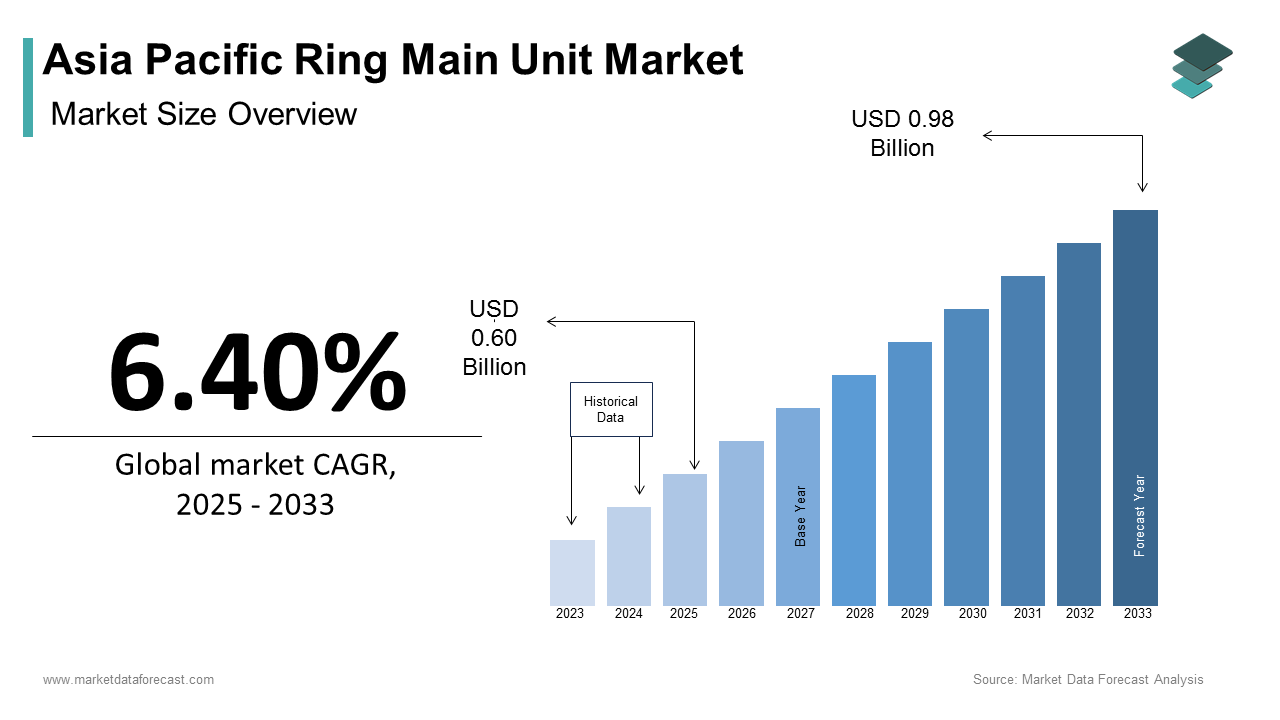

The Asia Pacific ring main unit market size was calculated to be USD 0.56 billion in 2024 and is anticipated to be worth USD 0.98 billion by 2033, from USD 0.60 billion in 2025, growing at a CAGR of 6.40% during the forecast period.

A ring main unit (RMU) is a compact, prefabricated electrical switching device used to distribute power in a closed-loop configuration, primarily within medium voltage networks. These units are widely employed in urban infrastructure, industrial complexes, commercial buildings, and renewable energy integration systems due to their reliability, space efficiency, and ease of maintenance. In the Asia Pacific region, RMUs play a critical role in enhancing grid stability and supporting the expansion of decentralized electricity distribution networks.

MARKET DRIVERS

Expansion of Smart Cities and Urban Infrastructure Projects

One of the foremost drivers of the Asia Pacific ring main unit market is the widespread push toward smart city development and modern urban infrastructure. Governments in countries like India, China, Malaysia, and Indonesia have launched large-scale smart city missions aimed at improving energy efficiency, transportation systems, and overall quality of life through digitized and resilient infrastructure. According to the World Bank, by 2050, nearly two-thirds of Asia’s population will reside in urban areas, necessitating significant upgrades to electrical distribution networks. Ring main units are integral components in these developments, enabling efficient power distribution across high-density residential and commercial zones. They provide enhanced fault tolerance, reduce downtime, and support automated control systems essential for smart grids. Similarly, in China, urbanization plans backed by the National Development and Reform Commission emphasize the deployment of intelligent distribution equipment, including vacuum circuit breaker-based RMUs that offer superior arc suppression and longer service life. These advancements align with the broader objective of creating sustainable, digitally integrated urban environments where reliable and secure energy access is non-negotiable.

Integration of Renewable Energy Sources into Distribution Networks

Another major driver propelling the growth of the Asia Pacific ring main unit (RMU) market is the increasing integration of renewable energy sources into national and regional power grids. With countries intensifying efforts to reduce carbon emissions and meet climate commitments, solar and wind energy installations are expanding rapidly across the region. According to the International Renewable Energy Agency (IRENA), Asia Pacific accounted for over 50% of global renewable energy additions in 2023, driven largely by deployments in China, India, and Japan. Renewable energy sources introduce variability and intermittency into power generation, requiring more flexible and responsive distribution systems. Ring main units play a crucial role in managing this complexity by enabling bidirectional power flow, facilitating seamless connection of distributed energy resources (DERs), and enhancing network reliability. Their modular design allows utilities to incorporate microgrid architectures and smart monitoring capabilities, which are essential for maintaining grid stability amidst fluctuating renewable inputs. In South Korea, for example, the government has mandated grid enhancements to accommodate its growing solar capacity, prompting utility companies to install intelligent RMUs equipped with real-time data analytics and remote operation features. Similarly, in Australia, DER integration strategies promoted by the Australian Energy Market Operator (AEMO) have led to increased adoption of SF6 gas-insulated RMUs in suburban distribution zones to handle decentralized generation from rooftop solar panels.

MARKET RESTRAINTS

High Capital Investment and Complex Installation Requirements

One of the primary restraints affecting the Asia Pacific ring main unit (RMU) market is the relatively high initial capital investment required for procurement and installation. While RMUs offer long-term benefits in terms of operational efficiency and reduced maintenance costs, their upfront expenses can be a deterrent, particularly for small and medium-sized enterprises (SMEs) and smaller municipalities with limited fiscal flexibility. Installation also presents logistical and technical challenges, especially in densely populated urban settings or remote rural locations where access to skilled labor and specialized equipment may be limited. In emerging economies such as Vietnam, the Philippines, and parts of Indonesia, the lack of standardized training programs for technicians capable of handling modern RMUs further complicates deployment timelines and increases dependency on external consultants. Moreover, compliance with international standards such as IEC 62271-200 adds another layer of complexity, often requiring additional engineering assessments and certification costs before commissioning.

Supply Chain Disruptions and Component Shortages

Supply chain disruptions and component shortages represent a significant challenge for the Asia Pacific ring main unit (RMU) market, impacting production schedules and project timelines. The RMU manufacturing process relies heavily on semiconductor devices, metal enclosures, insulating gases, and high-grade copper wiring—all of which have faced supply constraints in recent years due to geopolitical tensions and global logistics bottlenecks. According to McKinsey & Company, the semiconductor shortage that began in 2021 continued to affect various sectors in 2023, including industrial electronics and electrical infrastructure. Also, trade restrictions and inflationary pressures have led to extended lead times for key raw materials such as aluminum and copper, which are essential for housing and conductor fabrication. Logistical complexities have been exacerbated by container freight delays and port congestion, particularly along major shipping routes connecting Southeast Asia with Europe and North America. These disruptions have forced manufacturers to either increase pricing or reduce output, limiting accessibility for smaller buyers and delaying large-scale infrastructure projects.

MARKET OPPORTUNITIES

Growth of Microgrids and Decentralized Power Systems

An emerging opportunity for the Asia Pacific ring main unit (RMU) market lies in the expansion of microgrids and decentralized power systems, particularly in remote and off-grid communities. Governments and private energy providers are increasingly deploying microgrids to improve energy access in underserved regions, leveraging ring main units to facilitate safe, intelligent, and flexible power distribution. According to the International Energy Agency (IEA), approximately 80 million people in Asia Pacific still lacked access to electricity in 2023, primarily in rural parts of India, Indonesia, and the Philippines. Microgrid installations rely on RMUs to manage bidirectional power flows, isolate faults efficiently, and maintain system stability when integrating multiple energy sources such as solar, diesel generators, and battery storage. These units enable seamless coordination between centralized and decentralized power nodes, making them indispensable components in hybrid energy systems. In India, for instance, the Ministry of New and Renewable Energy has actively supported microgrid projects under its decentralized renewable energy initiative, mandating the use of modular RMUs for efficient load management. Similarly,

Adoption of Gas-Insulated Switchgear (GIS) Technology in RMUs

A promising opportunity in the Asia Pacific ring main unit (RMU) market is the rising adoption of gas-insulated switchgear (GIS) technology, particularly sulfur hexafluoride (SF6) and dry-air alternatives. GIS-based RMUs offer distinct advantages such as compact footprint, enhanced safety, and superior performance in harsh environmental conditions—making them ideal for urban centers, industrial parks, and coastal installations. The shift toward GIS RMUs is being driven by space constraints in metropolitan areas, stricter fire-safety regulations, and the need for low-maintenance electrical infrastructure. Japan has been at the forefront of this transition, with Tokyo Electric Power Company (TEPCO) mandating the use of GIS-based RMUs in new substation constructions to enhance reliability and disaster preparedness. Similarly, in Singapore, the Land Transport Authority (LTA) has integrated GIS RMUs into underground metro stations and transport hubs to optimize space utilization while maintaining high electrical integrity.

MARKET CHALLENGES

Technological Obsolescence Due to Rapid Innovation

A pressing challenge confronting the Asia Pacific ring main unit (RMU) market is the risk of technological obsolescence posed by rapid innovation in electrical distribution systems. The sector is witnessing a shift toward digital substations, smart grid technologies, and IoT-enabled asset monitoring solutions, which are gradually replacing conventional RMUs with more advanced, adaptive configurations. Legacy RMU designs, particularly those lacking remote monitoring, self-diagnostic capabilities, or modularity, are becoming less competitive in environments where predictive maintenance and real-time data analytics are prioritized. This trend is evident in countries like South Korea and Australia, where utility companies are retrofitting existing RMUs with digital sensors and communication modules to align with smart grid objectives set forth by respective energy regulators. Meanwhile, manufacturers unable to keep pace with evolving product expectations face declining market relevance, forcing them to invest heavily in research and development to offer next-generation RMUs with embedded intelligence and compatibility with cloud-based management platforms.

Regulatory Variability Across Regional Jurisdictions

Regulatory variability across different jurisdictions in the Asia Pacific region poses a major challenge to the standardization and scalability of ring main unit (RMU) deployment. Each country enforces its own set of electrical safety codes, compliance requirements, and certification procedures for power distribution equipment, leading to inconsistencies that complicate cross-border procurement and implementation. According to the Asian Development Bank (ADB), differences in grid standards among ASEAN nations create barriers to interoperability, affecting the ease with which RMU manufacturers and integrators can operate across markets. In some cases, local regulations require RMUs to undergo extensive testing and approval processes before deployment, prolonging project timelines and increasing administrative costs. Furthermore, shifting environmental policies, such as bans on SF6 gas usage due to its high global warming potential, are compelling manufacturers to adapt to alternative insulation mediums like dry air or vacuum interrupters. However, such modifications must be implemented by varying national guidelines, adding layers of complexity to product design and regulatory approvals.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.40% |

| Segments Covered | By Insulation type, Voltage rating, Installation type, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of Asia-Pacific |

| Market Leaders Profiled | ABB, Siemens, Schneider Electric, Eaton, Larsen & Toubro, Toshiba Corporation, LS Electric, Hyundai Electric & Energy Systems, CG Power and Industrial Solutions, Lucy Electric |

SEGMENTAL ANALYSIS

By Insulation Type Insights

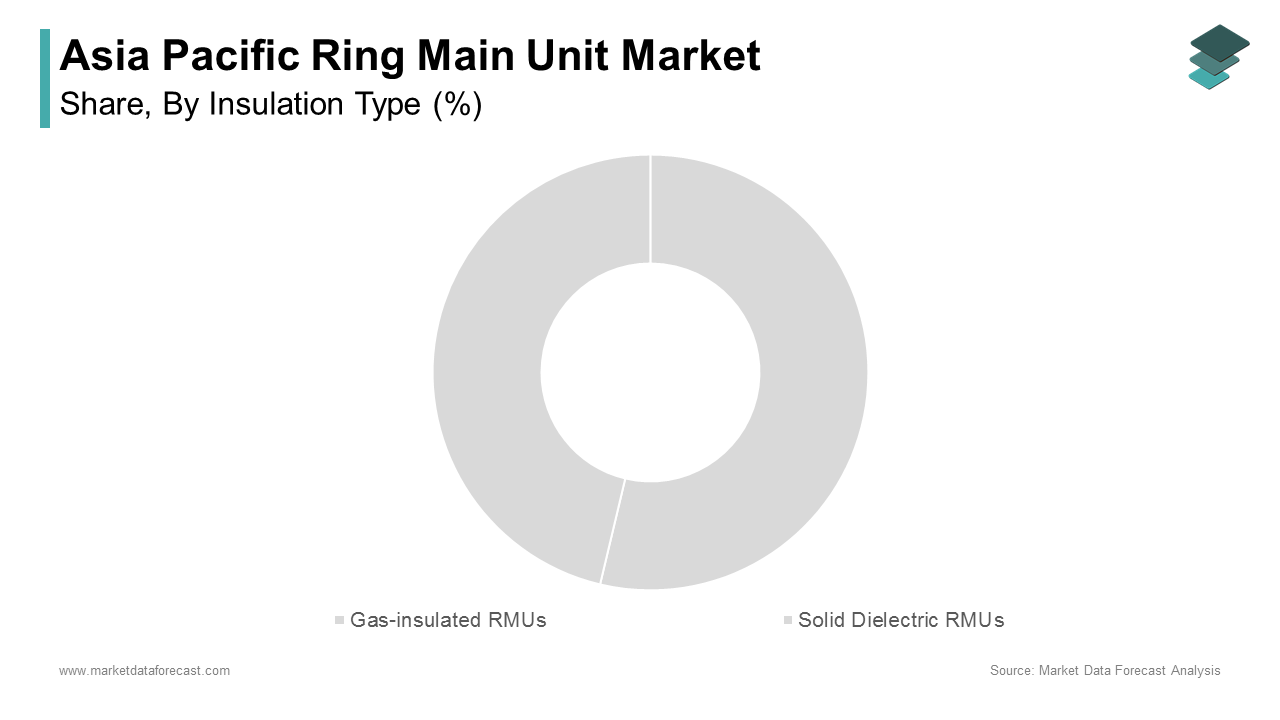

The Gas-insulated ring main units (RMUs) dominated the Asia Pacific market by capturing 45.6% of total demand in 2024. This dominance is driven by their superior performance in space-constrained environments and high reliability in urban electrical infrastructure. In densely populated cities like Tokyo, Shanghai, and Mumbai, network operators prioritize SF6-based RMUs for underground substations and commercial complexes where fire risks and physical footprints are critical concerns. China has also been a major consumer of gas-insulated RMUs, particularly in new metro rail projects and industrial parks where uninterrupted power supply is crucial. The country's State Grid Corporation has mandated the use of GIS-compatible RMUs in smart grid upgrades to improve fault detection and remote monitoring capabilities.

The solid dielectric ring main units are emerging as the fastest-growing segment in the Asia Pacific RMU market, projected to expand at a CAGR of 9.3%. This surge is primarily fueled by environmental concerns surrounding traditional insulation gases such as sulfur hexafluoride (SF6), which contributes significantly to greenhouse gas emissions. According to the International Energy Agency (IEA), SF6 is one of the most potent greenhouse gases, prompting regulators and utility companies across Asia to seek greener alternatives. Solid dielectric technology offers an eco-friendly solution without compromising on performance, making it increasingly attractive among environmentally conscious governments and private sector players. In India, for example, the Bureau of Indian Standards (BIS) has encouraged the deployment of solid insulation RMUs in new smart city projects to align with national climate action plans. Besides, solid dielectric RMUs require lower maintenance and eliminate the need for periodic gas refilling, reducing operational costs. South Korea’s Ministry of Trade, Industry, and Energy has incentivized the adoption of this technology through energy efficiency grants and green procurement policies.

By Voltage Rating Insights

The "Up to 15 kV" voltage rating segment held the largest share of the Asia Pacific ring main unit (RMU) market i.e. 60% of total sales in 2024. This dominance is attributed to the widespread use of low-to-medium voltage distribution networks in urban and rural electrification projects. According to the International Energy Agency (IEA), a large majority of electricity distribution in the Asia Pacific region occurs at voltages below 20 kV, reinforcing the relevance of RMUs within this range. These RMUs are extensively deployed in residential townships, commercial complexes, and industrial estates that require reliable and modular power distribution solutions. Countries like India and Indonesia have incorporated 12 kV RMUs into their rural electrification programs under initiatives such as India’s Deendayal Upadhyaya Gram Jyoti Yojana (DDUGJY) and Indonesia’s Electrification Acceleration Program. Moreover, the rapid expansion of smart grid deployments and microgrids has further increased the demand for RMUs operating at or below 15 kV. In China, the State Grid Corporation has standardized 12 kV RMUs for secondary distribution systems, ensuring compatibility with automated control mechanisms used in intelligent substations.

The "Above 25 kV" RMU category is currently the rapidly advancing segment in the Asia Pacific market, expected to expand at a CAGR of 8.7% through 2033. This rise is due to the increasing deployment of high-capacity transmission and sub-transmission systems to support large-scale renewable energy integration and industrial megaprojects. These RMUs facilitate seamless power injection into primary grids while maintaining system stability. Australia’s National Electricity Market (NEM) has witnessed a surge in above-25 kV RMU installations to support the integration of renewable energy zones (REZs) being developed in New South Wales and Queensland. Similarly, in South Korea, the government-backed Green Growth Strategy mandates higher voltage-rated RMUs for interconnecting new hydrogen production facilities and industrial parks. Furthermore, oil and gas companies in Malaysia and Vietnam are adopting high-voltage RMUs to manage power distribution in offshore drilling platforms and processing plants, where reliability under harsh conditions is essential.

By Installation Type

The indoor ring main units accounted for the majority of the Asia Pacific RMU market by capturing 65.6% of total installations in 2024. This preference is credited to the advantages offered by indoor RMUs in terms of protection against environmental elements, reduced maintenance requirements, and improved longevity in controlled settings. In highly urbanized markets such as Singapore and Hong Kong, building codes mandate the use of indoor RMUs to ensure compliance with fire safety and electromagnetic interference standards. The Indian Electrical and Electronics Manufacturers’ Association (IEEMA) notes that indoor RMUs are easier to integrate with SCADA systems and digital monitoring tools, enhancing grid surveillance capabilities. Similarly, in Japan, utility providers prefer indoor RMUs for retrofitting aging electrical infrastructure due to their compatibility with seismic-resistant designs and space optimization strategies.

Outdoor RMUs are witnessing the highest growth in the Asia Pacific ring main unit market, projected to expand at a CAGR of 8.2% from 2024 to 2030. This is mainly caused by the rising deployment of RMUs in rural electrification, agriculture pump sets, and renewable energy projects where grid extension into remote locations is required. Governments and independent power producers are deploying outdoor RMUs equipped with weather-resistant enclosures to support off-grid and mini-grid electrification efforts. In Vietnam, state-owned utility EVN has integrated outdoor RMUs into its solar farm clusters situated in open fields, where exposure to dust and extreme temperatures necessitates durable power management equipment. In addition, outdoor RMUs are gaining traction in irrigation networks in India, where they provide efficient load management for agricultural pumps powered by solar inverters.

REGIONAL ANALYSIS

China dominated the Asia Pacific ring main unit market by holding 30.7% of total capacity in 2024. As the world’s largest electricity consumer with a rapidly modernizing grid infrastructure, China has prioritized the deployment of RMUs to enhance distribution efficiency and support its transition toward smart grid technologies. According to the China Electricity Council, the country added a substantial number of gigawatts of new distribution infrastructure in 2023, much of which integrated RMUs to enable automation and fault tolerance. The State Grid Corporation of China has mandated the use of SF6 gas-insulated RMUs in urban substations to reduce footprint while improving reliability. Besides, the expansion of electric vehicle charging networks and renewable energy integration projects has further boosted RMU demand.

India is another key player in the market. The country’s aggressive push for electrification, smart city development, and renewable energy integration has made RMUs a core component of its electrical infrastructure expansion. According to the Central Electricity Authority (CEA), India added a significant amount of new distribution capacity in fiscal year 2024, requiring thousands of RMUs for grid segmentation and load balancing. Government programs such as the Integrated Power Development Scheme (IPDS) and Smart Metering National Programme (SMNP) have spurred utility investments in RMUs with built-in automation features for improved billing accuracy and outage management. Manufacturers including Siemens India, CG Power and Industrial Solutions, and Schneider Electric have ramped up local production to meet the surge in demand from both public and private sectors. Furthermore, the rise in rooftop solar installations and decentralized microgrids has increased the adoption of compact RMUs tailored for bidirectional power flow.

Japan is a technologically advanced market with strong adoption, driven by its advanced electrical infrastructure and emphasis on reliability and safety. The country’s aging grid requires extensive modernization, prompting utilities to invest in high-efficiency RMUs that support disaster resilience and smart grid functionality. Japanese manufacturers such as Toshiba Energy Systems and Mitsubishi Electric have introduced digitally enhanced RMUs compatible with AI-driven predictive maintenance systems. These innovations align with the nation’s broader commitment to integrating renewable energy sources and promoting energy-efficient grid operations.

South Korea's rapid digitalization driving RMU demand which is distinguished by its early adoption of smart grid technologies and digital substations. The country’s Ministry of Trade, Industry, and Energy (MOTIE) has mandated nationwide grid digitization, requiring RMUs to be embedded with IoT-enabled controls for real-time diagnostics and remote operation. Additionally, South Korea’s hydrogen economy roadmap has led to increased RMU usage in fuel cell power plants and electrolysis units. The industry is also transitioning towards solid-dielectric RMUs to align with environmental regulations restricting SF6 gas usage.

Australia contributes majorly to the Asia Pacific RMU market, with growth primarily driven by the expansion of renewable energy infrastructure and grid modernization initiatives. According to the Australian Energy Market Operator (AEMO), renewable energy sources accounted for over 35% of total electricity generation in 2023, necessitating upgraded distribution equipment such as RMUs to manage variable input flows. State governments in New South Wales and Victoria have launched multi-billion-dollar investments in renewable energy zones (REZs), which incorporate RMUs for localized power routing and grid balancing. These units help integrate distributed solar and wind farms into the national grid efficiently. In addition, Western Australia’s resource-rich regions are adopting RMUs for mining and mineral processing operations, where electrical reliability directly impacts productivity and safety. Australian utilities are also favoring gas-insulated RMUs for underground urban substations, aligning with land-use constraints and fire prevention protocols.

LEADING PLAYERS IN THE ASIA PACIFIC RING MAIN UNIT MARKET

Siemens Energy

Siemens Energy is a global leader in electrical infrastructure and holds a strong presence in the Asia Pacific ring main unit (RMU) market. The company’s portfolio includes advanced gas-insulated and solid-dielectric RMUs tailored for smart grid applications, urban distribution networks, and renewable energy integration. Siemens has been instrumental in setting industry benchmarks with its environmentally friendly Blue RMU series that eliminates SF6 usage. In Asia Pacific, Siemens collaborates with utilities and governments to modernize aging power systems, contributing significantly to the region's transition toward intelligent and sustainable electrical grids.

Schneider Electric

Schneider Electric is a key player shaping RMU deployments across commercial, industrial, and utility sectors in Asia Pacific. Known for its EcoStruxure platform, the company integrates digital monitoring and control features into RMUs, enabling real-time asset management and predictive maintenance. Schneider actively supports decentralized energy projects by supplying modular RMUs suited for microgrids and solar parks. Its localized manufacturing and strategic partnerships with regional utilities enhance accessibility and customization. With a focus on sustainability and electrification equity, Schneider plays a pivotal role in expanding reliable power access across both urban and rural Asia Pacific markets.

ABB Ltd.

ABB is a globally recognized innovator in power technologies and maintains a dominant position in the Asia Pacific RMU landscape. The company offers a comprehensive range of RMUs designed for high reliability in harsh environments, including compact GIS-based units ideal for confined urban settings. ABB’s solutions support smart city initiatives, industrial automation, and large-scale renewable energy projects. Through continuous R&D investments, ABB develops RMUs with enhanced connectivity, cybersecurity features, and environmental compliance. In Asia Pacific, ABB works closely with national grid operators and private developers to ensure grid resilience and future readiness amid evolving energy demands.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies employed by leading players in the Asia Pacific RMU market is product innovation combined with environmental compliance. Companies are increasingly introducing RMUs based on solid dielectric and clean air insulation to align with global sustainability goals and regulatory shifts away from SF6-based equipment. This shift not only reduces environmental impact but also enhances brand positioning in eco-conscious markets.

Another significant approach is expanding the regional footprint through localized production and strategic collaborations. Major manufacturers are establishing or expanding manufacturing facilities within the Asia Pacific region to reduce costs, shorten delivery cycles, and meet local regulatory requirements. Collaborations with government bodies, state-owned utilities, and engineering firms enable them to tailor products to specific national needs while ensuring long-term project engagements.

A third crucial strategy involves integrating digital technologies into RMU systems. Companies are embedding IoT-enabled sensors, remote monitoring capabilities, and predictive analytics tools into RMUs to support smart grid initiatives.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the Asia Pacific ring main unit market include ABB, Siemens, Schneider Electric, Eaton, Larsen & Toubro, Toshiba Corporation, LS Electric, Hyundai Electric & Energy Systems, CG Power and Industrial Solutions, and Lucy Electric.

The competition in the Asia Pacific ring main unit market is shaped by a dynamic mix of multinational giants and emerging regional players striving to capture market share through differentiation and localization. Established global brands such as Siemens, ABB, and Schneider Electric leverage their technological expertise, extensive R&D capabilities, and global supply chains to maintain dominance. Their focus lies on delivering innovative, eco-friendly, and digitally enabled RMUs that cater to evolving grid demands. Meanwhile, regional manufacturers are gaining traction by offering cost-effective solutions tailored to local infrastructure needs, particularly in rural and semi-urban areas.

Collaboration with public sector utilities remains a key battleground, with companies competing for tenders linked to smart city missions, rural electrification programs, and renewable energy infrastructure projects. Product differentiation is increasingly driven by energy efficiency, modularity, and compatibility with digital grid ecosystems. As regulatory standards tighten and environmental concerns grow, vendors are under pressure to adapt quickly to changing norms, further intensifying the competitive environment.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Siemens Energy launched a new line of SF6-free ring main units specifically designed for the Asia Pacific market, aiming to meet growing demand for eco-friendly electrical infrastructure while supporting regional decarbonization goals.

- In May 2024, Schneider Electric expanded its manufacturing facility in Pune, India, to increase the local production capacity of modular RMUs, enabling faster deployment in smart city and industrial projects across South and Southeast Asia.

- In July 2024, ABB formed a joint venture with a leading Japanese electrical systems integrator to develop customized RMU solutions for Japan’s aging grid infrastructure, focusing on seismic resilience and digital monitoring capabilities.

- In September 2024, Hyundai Heavy Industries entered the RMU market in Vietnam by acquiring a local switchgear manufacturer, strengthening its foothold in Southeast Asia’s rapidly growing distribution equipment sector.

- In November 2024, Eaton Corporation introduced an IoT-enabled RMU solution in Australia, designed to integrate seamlessly with smart grid platforms and support renewable energy zone developments in New South Wales and Queensland.

MARKET SEGMENTATION

This research report on the Asia Pacific ring main unit market has been segmented and sub-segmented based on insulation type, voltage rating, installation type, and region.

By Insulation Type

- Gas-insulated RMUs

- Solid Dielectric RMUs

By Voltage Rating

- Up to 15 kV RMUs

- Above 25 kV RMUs

By Installation Type

- Indoor RMUs

- Outdoor RMUs

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific