Asia Pacific Robot Sensor Market Size, Share, Trends & Growth Forecast Report By Type (Light Sensors, Navigation and Positioning Sensors), End User Industry And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore And Rest Of Asia-Pacific), Industry Analysis From 2025 To 2033

Asia Pacific Robot Sensor Market Size

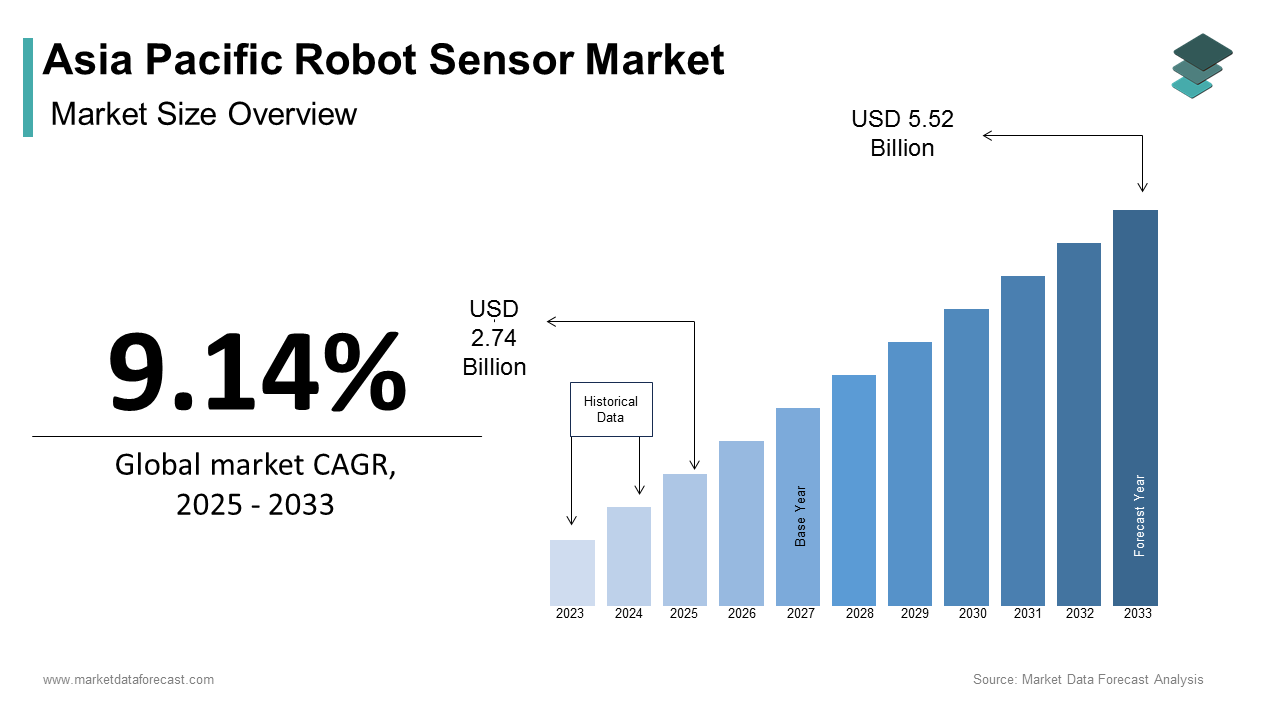

The Asia Pacific robot sensor market size was calculated to be USD 2.51 billion in 2024 and is anticipated to be worth USD 5.52 billion by 2033, from USD 2.74 billion in 2025, growing at a CAGR of 9.14% during the forecast period.

The robot sensor market represents a dynamic segment within the broader robotics industry, characterized by its integration of advanced sensory technologies to enhance automation processes. These sensors are pivotal in enabling robots to interact with their environment effectively, ensuring precision and efficiency in tasks ranging from manufacturing to healthcare. The region’s rapid industrialization, coupled with advancements in artificial intelligence and machine learning, has positioned it as a hotspot for innovation in robotics.

MARKET DRIVERS

Surge in Automation Across Manufacturing Industries

The proliferation of automation in manufacturing industries serves as a cornerstone for the growth of the robot sensor market in the Asia Pacific region. With labor costs rising and a growing emphasis on precision manufacturing, companies are increasingly turning to robotics to optimize production lines. Sensors play a critical role in this transition, as they enable robots to perform complex tasks such as quality control, assembly line coordination, and predictive maintenance. As per a study conducted by the Federation of Indian Chambers of Commerce & Industry (FICCI), robotic adoption in India's automotive sector alone surged by 30% in 2022, showing the cascading effect on sensor demand. Moreover, collaborative robots (cobots) equipped with vision sensors are gaining traction in small-scale enterprises, particularly in Southeast Asia.

Expansion of E-commerce and Logistics Operations

Another significant driver is the exponential growth of e-commerce and logistics operations in the Asia Pacific region. This surge has necessitated the deployment of automated warehouses and fulfillment centers, where robots equipped with proximity, LiDAR, and vision sensors streamline inventory management and order processing. For example, Alibaba's automated warehouse in Hangzhou utilizes over 700 robots, each embedded with multiple sensors, to handle up to one million packages daily. Furthermore, DHL Supply Chain reports that sensor-equipped autonomous mobile robots (AMRs) have reduced operational costs by up to 40% in its regional facilities. The rise of same-day delivery services has also amplified the need for high-speed sorting systems, where sensors ensure accurate routing and minimize errors. Notably, Singapore’s government initiative to establish itself as a regional logistics hub has spurred investments in sensor-based technologies.

MARKET RESTRAINTS

High Initial Costs and Limited Budgets

One of the primary restraints impacting the Asia Pacific robot sensor market is the substantial upfront investment required for deploying advanced robotic systems. While developed nations like Japan and South Korea can absorb these costs, smaller enterprises and emerging economies face financial constraints. This issue is exacerbated by the lack of accessible financing options tailored specifically for SMEs. A survey conducted by the Confederation of Indian Industry revealed that only a small fraction of Indian SMEs had access to affordable credit for technological upgrades in 2022. Also, the complexity of integrating sensors into existing systems often requires specialized expertise, further inflating costs.

Technical Challenges in Harsh Environmental Conditions

Another significant restraint is the operational challenges posed by harsh environmental conditions prevalent in certain parts of the Asia Pacific region. As per the United Nations Environment Programme, extreme weather patterns, including typhoons and monsoons, affect over 30% of the region’s landmass annually. Such conditions can impair the functionality of sensitive sensors, leading to frequent malfunctions or inaccurate readings. Moreover, the mining and construction sectors, which rely heavily on ruggedized robotic systems, encounter additional hurdles due to dust and debris interfering with sensor accuracy.

MARKET OPPORTUNITIES

Advancements in Artificial Intelligence and Machine Learning

The convergence of artificial intelligence (AI) and machine learning (ML) with robot sensors presents a transformative opportunity for the Asia Pacific market. By leveraging AI-driven algorithms, sensors can process vast amounts of real-time data to improve decision-making and operational efficiency. For instance, smart cameras equipped with AI-enabled image recognition are revolutionizing quality inspections in electronics manufacturing hubs. Besides, ML-enhanced predictive maintenance systems, powered by vibration and temperature sensors, are reducing unplanned downtime. This capability is particularly valuable in capital-intensive industries such as aerospace and semiconductor fabrication. Furthermore, governments across the region are investing heavily in AI research. Singapore’s National AI Strategy aims to allocate $500 million annually toward developing intelligent automation solutions, creating a fertile ecosystem for sensor innovation.

Growing Demand for Healthcare Robotics

The healthcare sector offers another promising avenue for the robot sensor market in the Asia Pacific. As per the World Health Organization, the region accounts for a large share of the global geriatric population, driving demand for assistive robotic devices. Sensors embedded in medical robots facilitate precise surgical procedures, patient monitoring, and rehabilitation therapies. Telemedicine platforms, bolstered by sensor technologies, are also gaining prominence amid the post-pandemic era.

MARKET OPPORTUNITIES

Stringent Regulatory Standards

Navigating stringent regulatory standards poses a formidable challenge for the Asia Pacific robot sensor market. Governments across the region have implemented rigorous compliance requirements to ensure safety and reliability, particularly in industries like pharmaceuticals and food processing. For instance, as per the Food Safety and Standards Authority of India, many of the automated systems in food manufacturing must adhere to ISO 22000 standards, which mandate extensive testing and certification of sensory components. These regulations not only increase development timelines but also inflate costs, making it difficult for startups and smaller firms to compete. Moreover, the lack of harmonization between national standards creates additional hurdles for multinational companies seeking to standardize their offerings across the region.

Cybersecurity Vulnerabilities

Another pressing concern is the vulnerability of robot sensors to cyberattacks, given their increasing connectivity to IoT networks. As per Kaspersky Lab, the Asia Pacific region experienced a 30% rise in cyber threats targeting industrial systems in 2022, with robotic devices being prime targets. Compromised sensors can lead to catastrophic outcomes, such as disrupted supply chains or compromised patient safety in healthcare settings. Despite these risks, many organizations lag in implementing robust cybersecurity measures. This gap shows the urgent need for enhanced security frameworks and awareness campaigns to safeguard sensor-dependent operations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.14% |

| Segments Covered | By Type, Industry, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of Asia-Pacific |

| Market Leaders Profiled | ATI Industrial Automation, Baumer Group, Honeywell International Inc., IFM Electronic GmbH, Keyence Corporation, Omron Corporation, Panasonic Corporation, Rockwell Automation, SICK AG, Teledyne FLIR LLC, TE Connectivity Ltd., Infineon Technologies AG, FANUC Corporation, Sensata Technologies Holdings PLC, Tekscan Inc., FUTEK Advanced Sensor Technology Inc., ABB Ltd., Cognex Corporation, Hokuyo Automatic Co. Ltd., KUKA AG, Pepperl+Fuchs AG, Roboception GmbH, Yaskawa Electric Corporation, Zebra Technologies Corporation |

SEGMENTAL ANALYSIS

By Type Insights

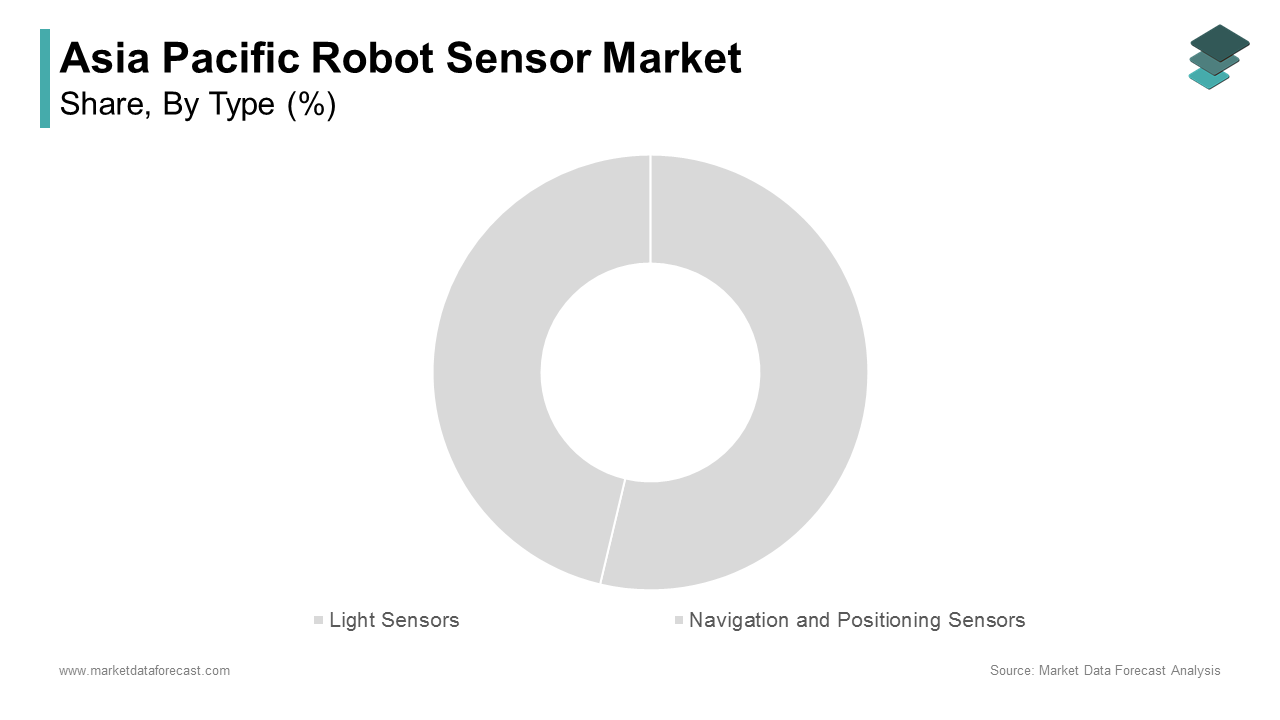

The light sensors segment dominated the Asia Pacific robot sensor market by holding a market share of 25.1% in 2024. This dominance is driven by their widespread application across various industries, including consumer electronics, automotive, and healthcare. For instance, in consumer electronics, light sensors are integral to smartphones, tablets, and smart home devices, enabling features like automatic brightness adjustment and proximity detection. A key factor propelling this segment is the rapid adoption of smart city initiatives across the region. These sensors optimize energy consumption by adjusting illumination based on ambient light levels, reducing electricity costs. Also, the growing emphasis on energy-efficient solutions aligns with regional sustainability goals, further amplifying demand. Another driving force is the expansion of autonomous vehicles, where light sensors play a critical role in LiDAR systems for navigation and obstacle detection.

The navigation and positioning sensors segment is the fastest-growing in the Asia Pacific robot sensor market, with a CAGR of 18.5% as per industry forecasts. This development is fueled by advancements in robotics and automation, particularly in logistics, manufacturing, and agriculture. For example, autonomous mobile robots (AMRs) equipped with navigation sensors are transforming warehouse operations, enabling precise movement and inventory tracking. DHL Supply Chain reports that AMR adoption has reduced operational costs by 30% in its regional facilities. Furthermore, the rise of precision agriculture is boosting demand for GPS-enabled positioning sensors. According to the Food and Agriculture Organization, the adoption of smart farming technologies in the Asia Pacific grew notably between 2020 and 2022, with sensors enabling accurate mapping and resource allocation.

By Industry Insights

The consumer electronics industry held the largest share of the Asia Pacific robot sensor market by accounting for 30.5% of the total revenue in 2024. This leading position is due to the region's position as a global hub for electronics manufacturing, with countries like China, South Korea, and Japan leading the charge. A primary driver is the proliferation of IoT-enabled devices, which rely heavily on sensors for connectivity and functionality. For instance, wearable devices such as smartwatches and fitness trackers utilize multiple sensors to monitor health metrics, driving innovation and adoption. Another factor is the increasing focus on miniaturization and energy efficiency. The Semiconductor Industry Association notes that advancements in MEMS (Micro-Electro-Mechanical Systems) technology have enabled the development of compact, low-power sensors, making them ideal for portable electronics.

The healthcare sector is the quickest-expanding end-use industry in the Asia Pacific robot sensor market, with a CAGR of 20%. This is driven by the rising geriatric population and the increasing adoption of medical robotics. Robotic surgical systems, equipped with force-torque and vision sensors, are revolutionizing procedures by enhancing precision and reducing recovery times. Besides, the post-pandemic surge in telemedicine has amplified the need for remote diagnostic tools, many of which rely on biosensors. The Indian Ministry of Health reports that telemedicine consultations utilizing sensor-based diagnostics exceeded 10 million in 2022, showcasing the technology's potential. Government initiatives are also playing a pivotal role.

REGIONAL ANALYSIS

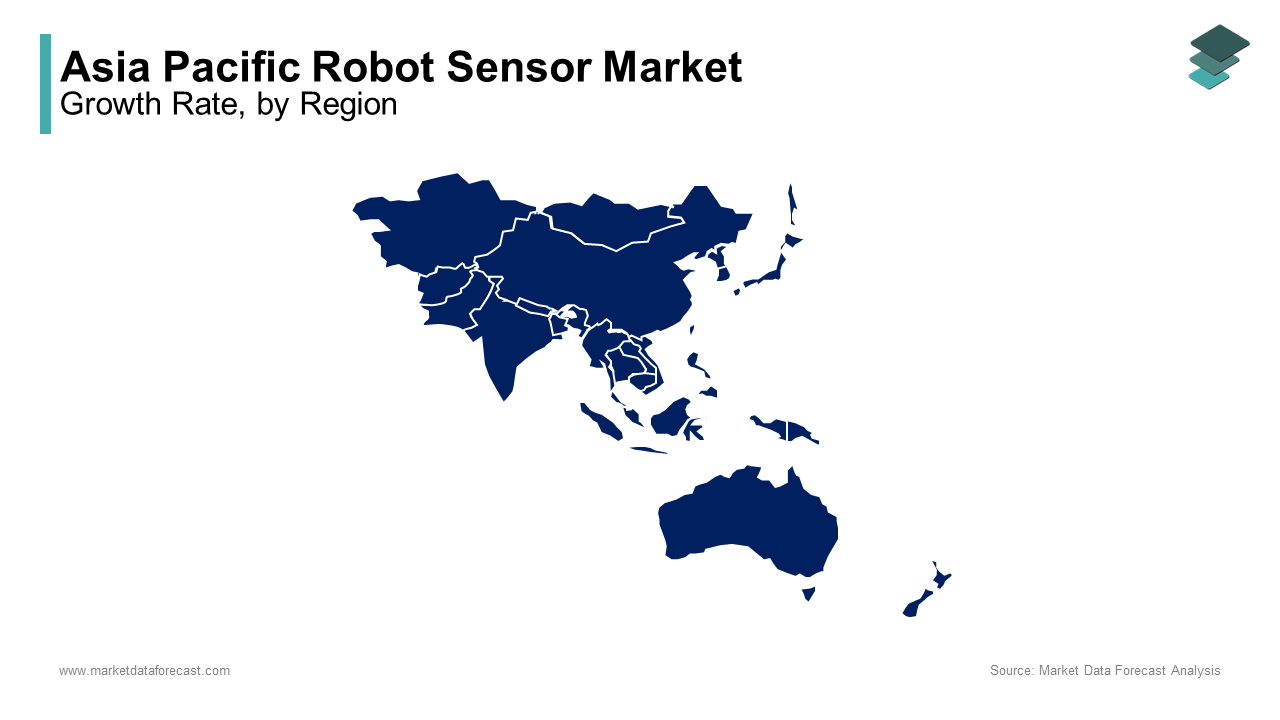

China stood as the leader in the Asia Pacific robot sensor market by commanding a market share of 40.7%. This control over the market is underpinned by the country's status as the world's largest manufacturing hub and its aggressive push toward automation. This massive deployment has created a steady demand for sensors, particularly in sectors like automotive and electronics. A key driving factor is the Made in China 2025 initiative, which prioritizes technological self-reliance and innovation. Moreover, the proliferation of smart factories is accelerating sensor adoption.

Japan is a major player in the regional market. Renowned for its technological prowess, Japan is a pioneer in robotics, with companies like Fanuc and Yaskawa Electric leading the charge. The aging population is a significant driver, with the Japanese Ministry of Health estimating that over 28% of the population is aged 65 or above. This demographic shift has spurred demand for assistive robots equipped with tactile and pressure sensors, enabling elderly care and rehabilitation. In addition, the government's Society 5.0 initiative aims to integrate AI and IoT into daily life, further propelling sensor innovation.

South Korea holds a significant position. The country's robust semiconductor and electronics industries are major contributors to sensor demand. Another driving factor is the rapid adoption of autonomous vehicles. Furthermore, the government's Green New Deal emphasizes sustainable practices, encouraging the use of energy-efficient sensors in industrial and residential settings.

India is emerging as a key player. The country's growing manufacturing base and favorable government policies are driving sensor adoption. According to the Confederation of Indian Industry, the "Make in India" campaign has attracted a substantial amount of foreign direct investment for robotics and automation projects. The expansion of e-commerce is another significant factor. Flipkart and Amazon India have established large-scale automated warehouses, utilizing sensors for inventory management and order fulfillment. In addition, the healthcare sector is witnessing increased sensor usage.

Australia and New Zealand collectively account for a small share of the market which is driven by their focus on advanced technologies in agriculture and mining. In mining, autonomous drilling and haulage systems equipped with sensors are transforming operations. Additionally, New Zealand's strong emphasis on renewable energy has spurred demand for temperature and pressure sensors in utility projects.

LEADING PLAYERS IN THE ASIA PACIFIC ROBOT SENSOR MARKET

Omron Corporation

Omron Corporation is a global leader in automation solutions and a key player in the Asia Pacific robot sensor market. The company specializes in advanced sensor technologies, including vision and tactile sensors, which are widely used in manufacturing and industrial automation. Omron’s innovation-driven approach has enabled it to develop highly precise sensors that cater to diverse industries such as automotive and consumer electronics.

Keyence Corporation

Keyence Corporation is renowned for its high-performance sensors and measurement systems, playing a pivotal role in the Asia Pacific market. The company’s focus on research and development has resulted in innovative products like laser displacement sensors and vision systems, which are integral to robotics applications. Keyence’s ability to provide customized solutions tailored to specific industry needs has strengthened its position globally.

Panasonic Corporation

Panasonic Corporation is a major contributor to the Asia Pacific robot sensor market, leveraging its expertise in electronics and automation. The company offers a wide range of sensors, including temperature and pressure sensors, which are critical for industrial and healthcare applications. Panasonic’s strong regional presence and partnerships with local manufacturers have enabled it to expand its footprint significantly.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Strategic Collaborations and Partnerships

Key players in the Asia Pacific robot sensor market are increasingly forming collaborations with technology firms and academic institutions to enhance their R&D capabilities. These partnerships allow companies to co-develop innovative sensor solutions that address specific regional challenges, such as harsh environmental conditions or unique industrial requirements.

Focus on Product Diversification

To cater to the diverse needs of end-use industries, leading companies are expanding their product portfolios by introducing specialized sensors. For instance, developing sensors tailored for healthcare robotics or autonomous vehicles ensures broader market penetration.

Investment in Localization

Recognizing the importance of regional adaptation, key players are investing in localized production and service centers. By establishing facilities closer to customers, they can reduce lead times, improve after-sales support, and better understand local market dynamics.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the Asia Pacific robot sensor market include ATI Industrial Automation, Baumer Group, Honeywell International Inc., IFM Electronic GmbH, Keyence Corporation, Omron Corporation, Panasonic Corporation, Rockwell Automation, SICK AG, Teledyne FLIR LLC, TE Connectivity Ltd., Infineon Technologies AG, FANUC Corporation, Sensata Technologies Holdings PLC, Tekscan Inc., FUTEK Advanced Sensor Technology Inc., ABB Ltd., Cognex Corporation, Hokuyo Automatic Co. Ltd., KUKA AG, Pepperl+Fuchs AG, Roboception GmbH, Yaskawa Electric Corporation, Zebra Technologies Corporation.

The Asia Pacific robot sensor market is characterized by intense competition, driven by the presence of both global giants and regional players striving to capture market share. Leading companies are heavily focused on innovation, consistently introducing advanced sensor technologies to meet the evolving demands of industries such as manufacturing, healthcare, and logistics. The market’s competitive landscape is shaped by the rapid adoption of Industry 4.0 practices, which emphasize connectivity, precision, and efficiency. Players are also prioritizing customer-centric strategies, offering tailored solutions to address specific operational challenges. Additionally, the rise of startups specializing in niche applications, such as AI-enabled sensors, adds another layer of complexity to the market.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, Omron Corporation launched a new series of vision sensors designed specifically for use in collaborative robots (cobots). This move aimed to enhance precision in assembly line operations and strengthen its position in the industrial automation segment.

- In June 2023, Keyence Corporation announced a partnership with a leading robotics manufacturer in Japan to integrate its laser displacement sensors into next-generation autonomous mobile robots (AMRs). This collaboration was intended to improve navigation accuracy and expand its application base.

- In August 2023, Panasonic Corporation established a regional R&D center in Singapore focused on developing IoT-enabled sensors for smart city applications. This initiative underscored its commitment to addressing urbanization challenges in the Asia Pacific region.

- In November 2023, Honeywell International acquired a local sensor technology startup in India to bolster its portfolio of environmental monitoring sensors. This acquisition enabled Honeywell to tap into the growing demand for sustainable solutions in the region.

- In January 2024, Sick AG introduced a new line of safety sensors compliant with international standards, targeting the aerospace and defense sectors in Australia. This launch positioned Sick AG as a leader in high-reliability sensor solutions for critical industries.

MARKET SEGMENTATION

This research report on the Asia Pacific robot sensor market has been segmented and sub-segmented based on type, industry,y, and region.

By Type

- Light Sensors

- Navigation and Positioning Sensors

By Industry

- Consumer Electronics

- Healthcare

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What are the key types of sensors used in robots?

Common types include proximity sensors, vision sensors, force/torque sensors, temperature sensors, ultrasonic sensors, and motion sensors.

2. Who are the key players in the Asia Pacific robot sensor market?

Major players include Panasonic Corporation, Omron Corporation, Keyence Corporation, SICK AG, Honeywell International Inc., and TE Connectivity Ltd.

3. How is AI impacting robot sensors in the region?

AI is enhancing sensor performance by enabling real-time data analysis, adaptive learning, and improved decision-making capabilities in robotic systems.

4. Which countries are driving the growth of this market in Asia Pacific?

China, Japan, South Korea, and India are the major countries driving growth due to their large manufacturing bases, high investment in automation, and increasing adoption of robotics in various sectors.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com