Asia Pacific Rotomoulding Powder Market Size, Share, Trends & Growth Forecast Report By Product (Polyethylene, Polyurethane), Machining Type, Application, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore And Rest Of Asia-Pacific), Industry Analysis From 2025 To 2033

Asia Pacific Rotomoulding Powder Market Size

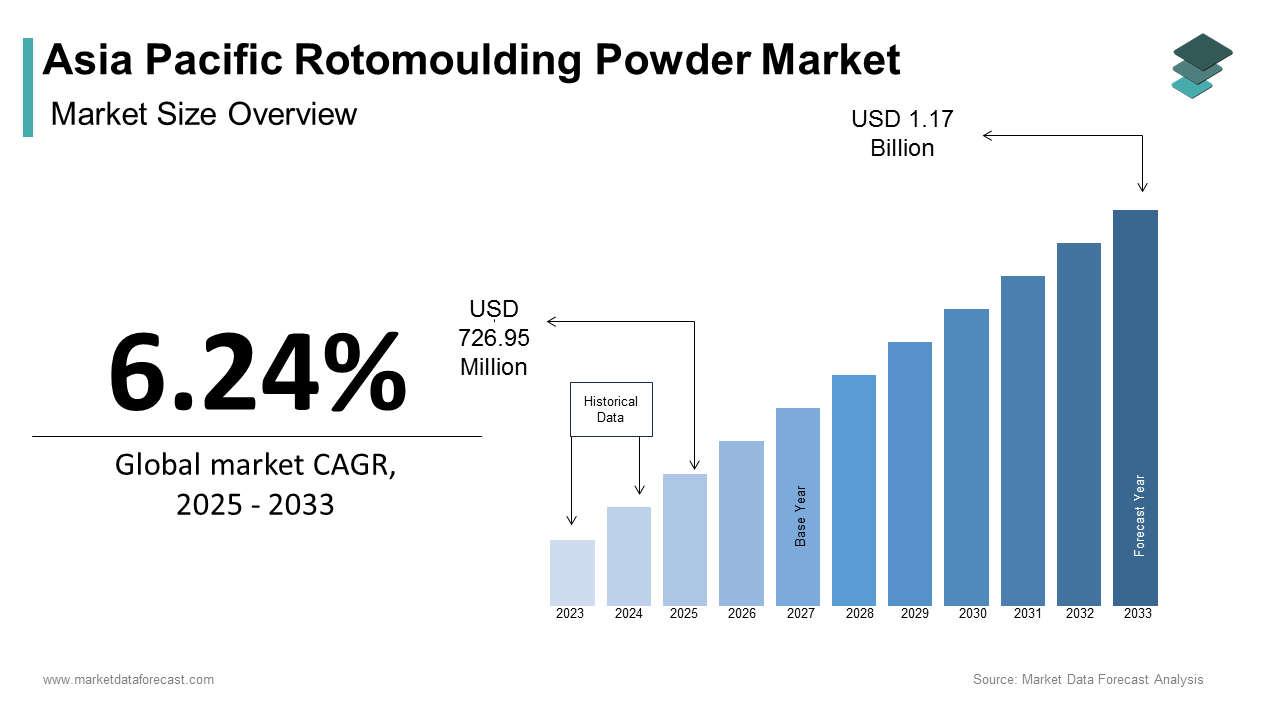

The Asia Pacific Rotomoulding Powder Market size was calculated to be USD 684.25 million in 2024 and is anticipated to be worth USD 1.17 billion by 2033, from USD 726.95 million in 2025, growing at a CAGR of 6.24% during the forecast period.

The rotomoulding powder technique is widely employed in industries such as automotive, construction, agriculture, and consumer goods for fabricating large, stress-free components like water tanks, playground equipment, industrial containers, and marine buoys. The primary materials involved are polyethylene (PE), polypropylene (PP), and nylon-based powders, each offering distinct advantages in durability, chemical resistance, and thermal stability. In recent years, the Asia Pacific region has emerged as a key growth hub for this market, driven by rapid industrialization, infrastructure expansion, and rising disposable incomes. Countries such as China, India, and Indonesia have seen an uptick in demand for rotomoulded products due to their cost-effectiveness and scalability.

MARKET DRIVERS

Expansion of the Water Storage and Irrigation Sector in Developing Economies

One of the most significant drivers of the Asia Pacific rotomoulding powder market is the increasing demand for durable and lightweight water storage solutions in rural and semi-urban areas. With rapid population growth and uneven rainfall distribution, countries like India, Vietnam, and the Philippines are investing heavily in irrigation and rainwater harvesting systems. Rotomoulded water tanks, produced using high-density polyethylene (HDPE) powders, offer superior corrosion resistance, UV stability, and cost-efficiency compared to traditional concrete or metal alternatives.

According to the Food and Agriculture Organization (FAO), over 60% of agricultural land in South and Southeast Asia relies on rain-fed irrigation, necessitating the deployment of efficient water storage systems. In India alone, the Ministry of Jal Shakti reported the installation of more than 10 million HDPE-based water tanks between 2020 and 2023 under its Jal Jeevan Mission. These tanks are predominantly manufactured using rotomoulding techniques, directly boosting demand for rotomoulding powders. Furthermore, the Indian Plastics Institute noted that domestic production of HDPE resin increased by 9.4% annually during this period, underscoring the strong link between agricultural modernization and polymer consumption.

Surge in Demand for Recreational and Leisure Products

Another critical driver of the Asia Pacific rotomoulding powder market is the growing recreational and leisure industry in urban centers and tourist destinations. Rotomoulded products such as playground equipment, kayaks, outdoor furniture, and floating pontoons are gaining popularity due to their durability, weather resistance, and design flexibility. The rise in disposable incomes and the expansion of the middle class in countries like Thailand, Malaysia, and Australia have spurred investments in tourism infrastructure and public amenities, which often incorporate rotomoulded components.

As per the World Travel & Tourism Council (WTTC), the travel and tourism sector in the Asia Pacific accounted for nearly 10% of total employment and contributed approximately USD 1.8 trillion to the regional GDP in 2023. This economic activity has led to increased public and private investment in parks, resorts, marinas, and recreational facilities. The expanding leisure economy thus presents a consistent and growing market for roto moulding powder producers across the Asia Pacific.

MARKET RESTRAINTS

Volatility in Raw Material Prices

A major restraint affecting the Asia Pacific rotomoulding powder market is the fluctuation in prices of key raw materials, primarily derived from crude oil. Polyethylene resins, which constitute the bulk of rotomoulding powders, are petrochemical derivatives whose costs are closely tied to global oil markets. Price instability can significantly impact production budgets for manufacturers and lead to inconsistent pricing for end-users, thereby hampering market growth.

According to the International Energy Agency (IEA), crude oil prices experienced sharp volatility between 2021 and 2023, peaking at over USD 120 per barrel in mid-2022 before dropping below USD 70 in late 2023. Such fluctuations create uncertainty for polymer producers, who must adjust their pricing strategies frequently. This surge forced many small and medium-sized enterprises (SMEs) to either absorb the cost or pass it on to customers, both of which negatively affected profit margins and slowed order growth.

Limited Awareness and Technical Expertise in Emerging Markets

The lack of technical knowledge and awareness regarding advanced rotomoulding techniques continues to hinder market growth in several emerging economies across the Asia Pacific. Many local manufacturers, especially in countries like Bangladesh, Cambodia, and Papua New Guinea, still rely on outdated production methods or alternative fabrication processes due to a limited understanding of the benefits offered by rotomoulding technology.

As per the United Nations Industrial Development Organization (UNIDO), only 23% of SMEs in Southeast Asia had access to formal training programs related to polymer processing technologies in 2023. This gap in skill development restricts the adoption of rotomoulding, despite its advantages such as lower tooling costs and the ability to produce complex shapes. Moreover, the absence of localized technical support services exacerbates the issue, making maintenance and troubleshooting difficult for new adopters.

MARKET OPPORTUNITIES

Growth of the Renewable Energy Sector and Off-grid Infrastructure

The expansion of renewable energy infrastructure, particularly off-grid solar and wind power installations, presents a substantial opportunity for the Asia Pacific rotomoulding powder market. Rotomoulded components are increasingly being used in the housing, mounting, and protective structures for solar panels, battery enclosures, and wind turbine components due to their lightweight nature, durability, and resistance to environmental stressors.

According to the International Renewable Energy Agency (IRENA), Asia Pacific accounted for nearly 60% of global renewable energy capacity additions in 2023, with countries like India, Vietnam, and the Philippines leading the charge in decentralized solar projects. In India, the Ministry of New and Renewable Energy reported that off-grid solar installations surpassed 2.5 GW in cumulative capacity by the end of 2023 by supporting millions of rural households and small businesses. Rotomoulded battery housings and solar panel mounts made from UV-stabilized polyethylene powders are becoming integral to these deployments due to their corrosion resistance and ease of transport. In Australia, where rooftop solar penetration exceeds 30%, manufacturers such as Rotoplas have introduced modular rotomoulded battery enclosures designed specifically for residential energy storage systems. The Australian Solar Council noted a 22% year-over-year increase in orders for such enclosures in 2023.

Rise of Modular Construction and Prefabricated Housing

The increasing adoption of modular and prefabricated construction methods in the Asia Pacific region offers another promising avenue for the rotomoulding powder market. Modular construction involves assembling pre-manufactured building components off-site by enabling faster project completion and reduced labor costs. Rotomoulded elements such as septic tanks, plumbing conduits, insulation panels, and utility boxes are well-suited for integration into prefabricated structures due to their durability, ease of customization, and lightweight properties.

As per the McKinsey Global Institute, the prefabricated construction market in the Asia Pacific is projected to grow at a compound annual rate of 11.3% through 2030, driven by urbanization and housing shortages in countries like China, Indonesia, and the Philippines. In Singapore, where land scarcity and labor constraints have accelerated the shift toward modular construction, the Building and Construction Authority (BCA) mandated that at least 70% of new public housing projects incorporate prefabricated elements by 2025. Rotomoulded components are increasingly being used in these projects for waste management and utility integration. The Japan Prefabricated Housing Association recorded a 17% increase in the use of rotomoulded parts in prefabricated homes in 2023.

MARKET CHALLENGES

Environmental Regulations and Plastic Waste Management Pressures

One of the foremost challenges facing the Asia Pacific rotomoulding powder market is the tightening regulatory environment concerning plastic waste and environmental sustainability. Governments across the region are enacting stringent policies aimed at reducing single-use plastics and promoting circular economy principles, which can inadvertently affect the perception and usage of polymeric materials even those used in durable, long-life applications like rotomoulding.

According to the United Nations Environment Programme (UNEP), 18 out of 25 Asia Pacific countries have implemented bans or restrictions on certain plastic products since 2020. While rotomoulded items are typically long-lasting and not classified as single-use plastics, negative public sentiment around plastics as a whole poses a reputational risk. In Thailand, for example, the Pollution Control Department launched a national roadmap in 2022 aiming to reduce plastic waste by 50% by 2027 by encouraging industries to adopt biodegradable alternatives. Although rotomoulding powders are largely recyclable, the lack of widespread recycling infrastructure in many parts of the region hampers effective material recovery. Moreover, environmental NGOs have been vocal in advocating for extended producer responsibility (EPR) schemes, which could impose additional compliance costs on manufacturers.

High Initial Investment and Limited Access to Advanced Machinery

Another significant challenge confronting the Asia Pacific rotomoulding powder market is the high capital expenditure required to set up and operate rotational moulding facilities, particularly in smaller economies. Unlike injection or blow moulding, rotomoulding requires specialized ovens, cooling chambers, and mould-handling equipment, which can be prohibitively expensive for small-scale manufacturers. This financial barrier limits market entry and slows down the adoption of rotomoulding technology in regions where traditional fabrication methods dominate.

In countries like Nepal and Laos, where industrial infrastructure is still developing, the lack of local suppliers and after-sales service for rotomoulding machines further discourage investment. Additionally, the limited availability of locally engineered moulds and the need to import precision tools from Europe or North America add to the overall complexity and expense. The Philippine Plastics Institute reported that nearly 40% of surveyed manufacturers cited equipment costs as the primary reason for not adopting rotomoulding, despite recognizing its long-term benefits.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.24% |

| Segments Covered | By Product, Machining Type, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of Asia-Pacific |

| Market Leaders Profiled | BASF SE, Dow Inc., Reliance Industries Limited, Matrix Polymers, ExxonMobil Corporation, LyondellBasell Industries, SABIC, GreenAge Industries, Pacific Poly Plast, Centro Incorporated |

SEGMENTAL ANALYSIS

By Product Insights

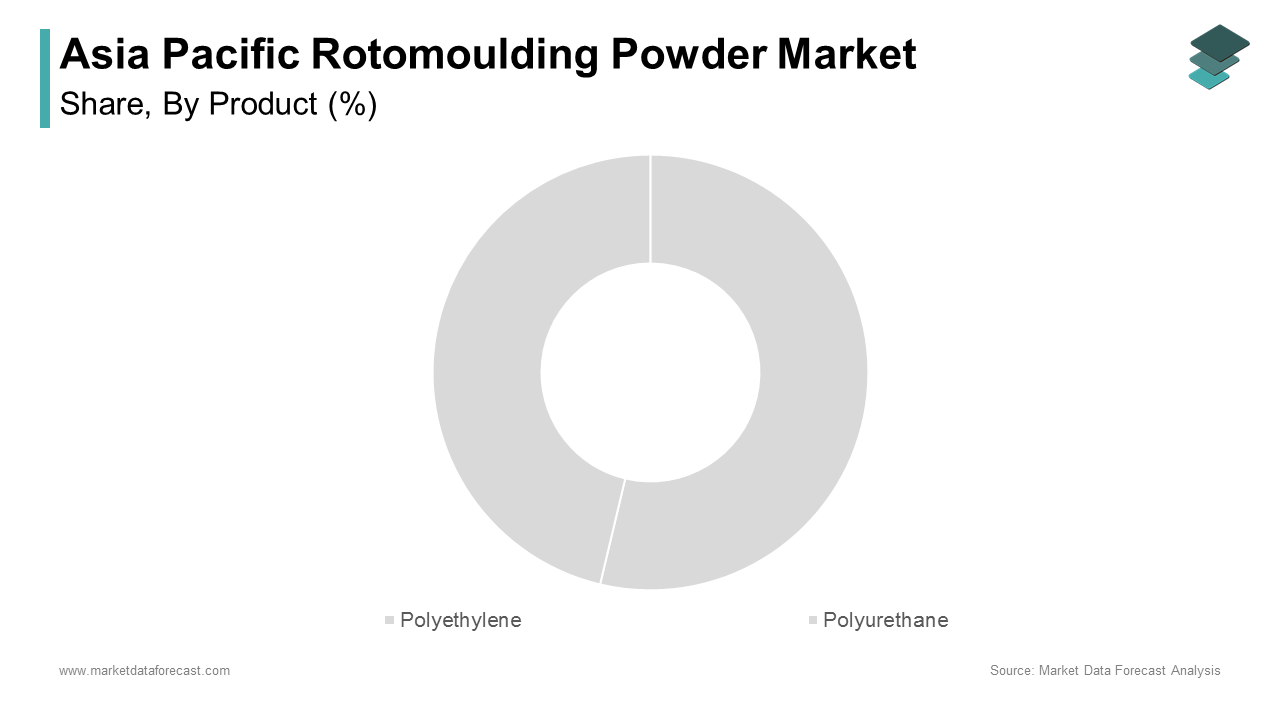

The polyethylene segment held 58.1% of the Asia Pacific rotomoulding powder market share in 2024. One of the key drivers behind polyethylene's leading position is its extensive adoption in agricultural water storage solutions , especially in countries like India, Vietnam, and Indonesia where irrigation infrastructure is rapidly expanding. Additionally, polyethylene’s compatibility with UV stabilizers makes it ideal for outdoor applications, further boosting its usage in playground equipment, septic tanks, and industrial containers.

Another contributing factor is the availability and scalability of HDPE and LLDPE resins in the region. As per the China Petroleum and Chemical Industry Federation, China alone accounted for nearly 45% of polyethylene resin consumption in the Asia Pacific, with domestic production growing at an annual rate of 7.3% from 2020 to 2023. The presence of large-scale polymer manufacturers and importers has ensured a steady supply chain, which is reinforcing polyethylene’s stronghold on the market.

The polyurethane segment is projected to grow with a CAGR of 9.8% during the forecast period. This rapid growth is driven by its increasing application in high-performance sectors such as automotive interiors, industrial rollers, and customized furniture components that demand superior resilience and design versatility.

One major driver is the expansion of the automotive industry in emerging economies like India, Thailand, and Indonesia, where there is a rising need for lightweight, durable materials that reduce vehicle weight without compromising structural integrity. According to the International Organization of Motor Vehicle Manufacturers (OICA), passenger car production in the Asia Pacific increased by 6.4% in 2023 compared to the previous year, with a significant portion incorporating polyurethane-based interior parts fabricated through rotational moulding. Additionally, the growing consumer preference for premium, customizable furniture in urban centers such as Singapore, Sydney, and Seoul has fueled demand for polyurethane powders.

By Machining Type Insights

The carousel machine segment accounted for 32.2% of the Asia Pacific rotomoulding powder market share in 2024. A primary reason for the carousel machine’s dominance is its multi-station design, which allows simultaneous heating, cooling, and loading operations, significantly improving throughput. According to the Japan Rotational Moulding Association, manufacturers using carousel machines reported up to 30% higher productivity compared to those operating shuttle or swing arm systems. In South Korea, where automation and precision are prioritized, the Korea Machinery Importers Association noted that over 60% of new rotomoulding units installed in 2023 were carousel-based systems in the automotive and construction sectors.

Another contributing factor is the rising investment in industrial automation in countries like China and India, where labor costs are increasing and manufacturers seek more efficient alternatives. The Chinese Ministry of Industry and Information Technology recorded a 12% rise in automated machinery adoption in the plastics sector in 2023, with carousel machines playing a central role in this transition. Their modular design also facilitates easy integration into smart manufacturing setups, further strengthening their market position.

The vertical or rotational machine segment is expected to expand at a CAGR of 10.4% from 2025 to 2033 due to its compact footprint and suitability for small-scale and startup manufacturers who require flexible and cost-effective production solutions. Additionally, the adoption of vertical machines in niche applications such as custom playground equipment, medical devices, and specialized containers is accelerating. As per the Australian Plastics Processing Institute, vertical machines have gained popularity in Australia for producing bespoke rotomoulded products tailored for remote communities and mining camps. Their ease of operation and adaptability to diverse product designs make them a compelling choice, especially for companies aiming to innovate without heavy capital outlay.

By Application Insights

The building & construction segment was the top performer in the Asia Pacific rotomoulding powder market with 28.4% of the share in 2024. This strong foothold is largely due to the increasing reliance on rotomoulded components in infrastructure development, including drainage systems, insulation panels, portable sanitation units, and utility enclosures.

The rapid urbanization and housing expansion taking place across emerging economies like India, Indonesia, and the Philippines is also fueling the growth of the market. According to the Asian Development Bank, urban populations in the Asia Pacific grew by an average of 2.1% annually between 2020 and 2023, which necessitates scalable and cost-effective construction solutions. Rotomoulded septic tanks, rainwater harvesting modules, and modular plumbing conduits made from polyethylene powders have become integral to affordable housing and public sanitation projects. For instance, India’s Ministry of Housing and Urban Affairs reported that over 15 million low-cost homes constructed under the Pradhan Mantri Awas Yojana (PMAY) incorporated rotomoulded components between 2021 and 2023.

The automotive segment is projected to grow with a CAGR of 11.6% from 2025 to 2033. This surge is driven by the increasing demand for lightweight, impact-resistant components that enhance fuel efficiency and reduce emissions, aligning with regional environmental regulations and evolving vehicle design trends.

Also, the expansion of electric vehicle (EV) production across the region, particularly in China, South Korea, and Thailand is prompting the growth of this segment. EV manufacturers are increasingly adopting rotomoulded battery housings, charge port covers, and interior trims made from polyethylene and polypropylene powders due to their thermal insulation properties and corrosion resistance. Another contributing factor is the shift towards modular and customizable vehicle interiors, especially in commercial and recreational vehicles. This trend is mirrored across Southeast Asia, where van conversions and mobile retail vehicles are gaining traction. With continued innovation in automotive design and sustainability goals, the automotive application segment is poised for sustained high-growth momentum.

REGIONAL ANALYSIS

China was the top performer in the Asia Pacific rotomoulding powder market with 32.1% of the share in 2024. One of the key drivers of this dominance is the high volume of plastic goods production, supported by government-backed initiatives such as "Made in China 2025," which emphasizes advanced manufacturing technologies. According to the National Bureau of Statistics of China, the country produced over 60 million metric tons of synthetic resins in 2023, with a significant portion allocated to rotational moulding applications. Another contributing factor is the growth of the automotive sector in electric vehicle (EV) manufacturing. This convergence of industrial policy, infrastructure development, and technological advancement ensures China remains the leading market for rotomoulding powders in the Asia Pacific.

India was positioned second in the Asia Pacific rotomoulding powder market by capturing 14.3% of the hare in 2024. A major driver behind India’s strong market position is the large-scale deployment of rotomoulded water tanks in rural and semi-urban areas. Under the Jal Jeevan Mission, the Government of India installed over 10 million HDPE-based household water connections between 2020 and 2023, many of which involved rotomoulded tank systems. According to the Ministry of Jal Shakti, this initiative has not only improved access to clean drinking water but also created a consistent demand for rotomoulding powders across the country.

Japan is likely to showcase huge growth opportunities for the Asia Pacific rotomoulding powder market in the coming years driven by its advanced industrial infrastructure and high adoption of precision manufacturing techniques. One of the primary reasons for Japan’s strong market presence is its focus on high-value industrial applications, particularly in the automotive and electronics sectors. Japanese automakers, known for their emphasis on quality and efficiency, extensively use rotomoulded parts for battery enclosures, air ducts, and interior trim components. Another contributing factor is the country’s commitment to disaster-resilient infrastructure, especially in coastal regions prone to typhoons and flooding.

Australia's rotomoulding powder market growth is anticipated to have a significant growth rate during the forecast period because of its strong presence in niche applications such as marine equipment, agricultural storage, and off-grid infrastructure. The country’s relatively small population belies its high per capita consumption of specialty plastics, particularly in sectors requiring durability and environmental resilience.

South Korea's rotomoulding powder market growth is likely to be driven by technological innovation, industrial automation, and the increasing use of engineered plastics in high-performance sectors. The country’s advanced manufacturing capabilities and focus on R&D have enabled it to carve out a unique position in the market.

Additionally, the expansion of the electric vehicle (EV) and hydrogen fuel cell industries has led to increased demand for rotomoulded components such as battery trays, coolant reservoirs, and lightweight interior parts. As per the Korea Automobile Manufacturers Association, EV production in the country rose by 28% in 2023, with major brands like Hyundai and Kia incorporating more polymer-based parts to meet emission targets and improve energy efficiency.

LEADING PLAYERS IN THE ASIA PACIFIC ROTOMOULDING POWDER MARKET

One of the leading companies in the Asia Pacific rotomoulding powder market is LyondellBasell Industries, a global chemical manufacturer with a strong regional presence. The company supplies high-quality polyethylene and polypropylene powders tailored for rotational moulding applications. LyondellBasell has consistently invested in product innovation and sustainable manufacturing, supporting diverse industries such as automotive, construction, and agriculture. Its focus on developing advanced polymer formulations enhances performance characteristics, making its products a preferred choice among manufacturers across the region.

Another key player is SABIC, a Saudi-based multinational corporation with a significant footprint in the Asia Pacific. SABIC offers a wide range of engineering thermoplastics and specialty polymers used in rotomoulding processes. The company leverages its extensive R&D capabilities to develop customized solutions that meet evolving industry demands. With strategic partnerships and localized production facilities, SABIC supports the growing needs of infrastructure, consumer goods, and industrial sectors, reinforcing its prominent position in the regional market.

Formosa Plastics Corporation, based in Taiwan, is also a major contributor to the Asia Pacific rotomoulding powder market. Known for its broad portfolio of PVC and polyolefin-based materials, Formosa serves multiple end-use sectors including water storage, packaging, and transportation. The company emphasizes vertical integration and operational efficiency to ensure reliable supply and cost-effectiveness.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies employed by key players in the Asia Pacific rotomoulding powder market is product innovation and customization Companies are focusing on developing advanced polymer blends that offer enhanced durability, UV resistance, and recyclability. By tailoring their offerings to specific industry requirements, manufacturers can address niche applications in the automotive, marine, and renewable energy sectors, thereby strengthening their competitive edge.

Another critical approach is expanding regional presence through localized production and partnerships. Leading firms are setting up dedicated manufacturing units and collaborating with local distributors to ensure faster delivery and better customer support. These efforts help them cater to the rising demand from emerging economies while reducing logistics costs and improving supply chain resilience.

Investing in sustainability initiatives has become a core strategy for major players. With increasing regulatory pressure and consumer awareness regarding environmental impact, companies are shifting toward eco-friendly raw materials and energy-efficient production methods. This not only aligns with global sustainability goals but also enhances brand reputation and long-term market positioning.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players of the Asia Pacific root moulding powder market include BASF SE, Dow Inc., Reliance Industries Limited, Matrix Polymers, ExxonMobil Corporation, LyondellBasell Industries, SABIC, GreenAge Industries, Pacific Poly Plast, Centro Incorporated.

The competition in the Asia Pacific roto moulding powder market is characterized by a mix of established global chemical producers and emerging regional players striving to capture market share through differentiation and strategic expansion. While large international firms leverage their technological expertise and extensive distribution networks, domestic manufacturers in countries like China, India, and South Korea are gaining traction by offering cost-effective and locally adapted solutions. The market landscape is further shaped by continuous advancements in polymer formulations and processing techniques, which enable companies to meet the evolving demands of various industries. As demand grows across sectors such as construction, agriculture, and automotive, firms are increasingly focusing on innovation, sustainability, and localized service offerings to maintain a competitive advantage. Additionally, partnerships, joint ventures, and investments in research and development play a crucial role in enhancing product portfolios and securing long-term contracts with key industry clients. This dynamic environment fosters both collaboration and rivalry, ensuring a constantly evolving market structure where adaptability and responsiveness to regional trends determine success.

RECENT HAPPENINGS IN THE MARKET

- In March 2024, LyondellBasell launched a new line of UV-stabilized polyethylene powders specifically designed for outdoor agricultural and water storage applications in Southeast Asia. This move was aimed at addressing the region’s growing need for durable, weather-resistant materials and enhancing the company’s foothold in key markets such as Vietnam and Indonesia.

- In February 2024, SABIC announced a strategic collaboration with a leading Japanese machinery manufacturer to co-develop next-generation rotomoulding systems optimized for high-performance thermoplastics. This partnership is intended to improve process efficiency and expand the adoption of SABIC’s polymers in precision-driven industries such as electronics and medical equipment.

- In January 2024, Formosa Plastics Corporation expanded its manufacturing facility in Kaohsiung, Taiwan, dedicating additional capacity to produce PVC-based rotomoulding powders. This investment reflects the company’s commitment to meet rising demand in the packaging and industrial sectors across the Asia Pacific.

- In May 2024, Mitsui Chemicals entered into a joint venture with an Indian polymer distributor to strengthen its supply chain and enhance customer reach in South Asia. This initiative supports Mitsui’s broader objective of increasing its presence in high-growth emerging markets.

- In June 2024, BASF SE opened a regional innovation center in Shanghai focused on polymer compounding and formulation technologies for rotational moulding applications. The center aims to accelerate product development and provide tailored material solutions to local manufacturers in the automotive and construction sectors.

MARKET SEGMENTATION

This research report on the Asia Pacific Rotomoulding Powder Market has been segmented and sub-segmented based on product, machining type, application, and region.

By Product

- Polyethylene

- Polyurethane

By Machine Type

- Carousel Machine

- Vertical or Rotational Machine

By Application

- Building & Construction

- Automotive

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What is the Asia Pacific Rotomoulding Powder Market?

The Asia Pacific Rotomoulding Powder Market refers to the regional industry involved in the production, distribution, and application of powdered resins used in the rotational moulding process to manufacture hollow plastic products.

2. Who are the key players in the Asia Pacific Rotomoulding Powder Market?

Major players include BASF SE, Dow Inc., Reliance Industries Limited, Matrix Polymers, ExxonMobil Corporation, LyondellBasell Industries, SABIC, GreenAge Industries, Pacific Poly Plast, and Centro Incorporated.

3. How is rotomoulding powder used in manufacturing?

Rotomoulding powder is heated inside a rotating mold where it melts and forms a uniform coating along the mold’s walls, creating seamless and hollow plastic products such as tanks, containers, and playground equipment.

4. Which factors are driving the growth of the Asia Pacific Rotomoulding Powder Market?

Growth is driven by rising demand for lightweight and durable plastic products, increased urbanization, industrialization, and growing usage in sectors like agriculture, water storage, and construction.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com