- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$3.53 BnMarket Estimate, 2026

$3.80 BnMarket Forecast, 2034

$6.78 BnCAGR, 2026–2034

7.53%Executive Summary: Asia Pacific Rubber Hose Market

- Market Scope: Comprehensive regional rubber hose market analysis covering material types, end-use industries, country-specific leadership frameworks, and key strategic developments.

- Market Valuation: Valued at USD 3.53 billion (2025), estimated at USD 3.80 billion (2026), and projected to reach USD 6.78 billion by 2034, registering a robust CAGR of 7.53% (2026–2034).

- Primary Growth Drivers: Rapid expansion of industrial machinery, hydraulics, and automotive manufacturing, alongside government-backed infrastructure initiatives (Belt and Road, National Infrastructure Pipeline) and agricultural irrigation demand. Opportunities include advanced synthetic materials, oil & gas LNG expansion, and EV/renewable energy supply partnerships.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Material Type & End-Use | Natural rubber segment (held ~58.3% share for agriculture/mining); Hydraulic industry (led end-use with 33.3% share) | Synthetic rubber segment (highest CAGR of 7.9% for temperature/chemical resistance); Oil & gas segment (fastest CAGR of 9.6% for LNG/offshore expansion) |

| By Region / Country | China (dominated regional market with a 32.3% share in 2025 due to manufacturing and infrastructure) | India (17.2% share) and Japan acting as key high-growth industrial manufacturing contributors |

Major Market Players & Market Structure

Market Structure: Highly competitive Asia-Pacific industrial hose and fluid power landscape featuring global and regional manufacturing leaders competing intensely on advanced material science, regional supply chain capabilities, and OEM partnerships.

Key Companies: Parker Hannifin Corp., Lomoflex Company Limited, Abbott Rubber Company Inc., Goodall Hoses, Anchor Rubber Products LLC, NewAge Industries Inc., Harrison Hose & Tubing Inc., Teknikum Oy, Kuriyama Holdings Corporation, and Goodflex Rubber Co. Ltd.

Asia Pacific Rubber Hose Market Size

In 2025, the Asia Pacific rubber rose market size was valued at USD 3.53 billion in 2025 and is anticipated to reach a valuation of USD 3.80 billion in 2026 and USD 6.78 billion by 2034, growing at a CAGR of 7.53%, from 2026 to 2034.

The rubber hose is made from natural and synthetic rubber, designed for the conveyance of fluids, gases, and semi-solids across industrial, automotive, construction, and agricultural applications. These hoses vary in composition and structure depending on their intended use, ranging from high-pressure hydraulic hoses used in machinery to lightweight irrigation and garden hoses used in domestic settings. Additionally, government-backed infrastructure initiatives such as China’s Belt and Road Program and India’s National Infrastructure Pipeline have further stimulated demand for construction equipment and heavy-duty machinery that incorporate rubber hoses for hydraulic and cooling functions.

MARKET DRIVERS

Expansion of Industrial Machinery and Hydraulic Equipment

The growing production and usage of industrial machinery and hydraulic equipment across the manufacturing, construction, and logistics sectors is propelling the growth of the Asia Pacific rubber hose market. Rubber hoses play an essential role in these machines by enabling fluid transfer under high pressure while maintaining flexibility and durability. In China, where the government has been promoting smart manufacturing and factory automation, the China Machinery Industry Federation noted a 22% increase in sales of industrial robots and automated assembly units in 2023. These machines often rely on rubber hoses for pneumatic and hydraulic actuation, reinforcing the sector's influence on hose demand.

Growth of the Automotive Sector and Aftermarket Demand

The rapid expansion of the automotive industry, both in terms of original equipment manufacturing and aftermarket replacement services, is also expected to fuel the growth of the Asia Pacific rubber hose market. Rubber hoses are integral components in vehicles, used in cooling systems, brake lines, fuel delivery, and air conditioning, making them indispensable in both traditional internal combustion engine (ICE) and hybrid electric vehicles (HEVs).

MARKET RESTRAINTS

Environmental Regulations and Shift Toward Synthetic Alternatives

The tightening regulatory environment concerning emissions, waste management, and material sustainability is slightly restraining the growth of the Asia Pacific rubber hose market. Governments across the region are implementing stricter environmental policies aimed at reducing reliance on fossil-fuel-derived materials and encouraging the adoption of recyclable or bio-based alternatives. According to the United Nations Environment Programme (UNEP), several Asia Pacific nations, including South Korea, Japan, and Australia, have introduced new directives mandating the reduction of non-recyclable content in industrial and consumer goods packaging. While rubber hoses are primarily used in mechanical applications rather than packaging, these regulations have indirectly influenced material sourcing decisions in manufacturing sectors.

Volatility in Raw Material Prices and Supply Chain Disruptions

Another significant constraint on the Asia Pacific rubber hose market is the fluctuation in prices of raw materials such as natural rubber, synthetic rubber, carbon black, and textile reinforcements. These commodities are subject to global supply chain dynamics, geopolitical tensions, and energy price movements, making cost forecasting and budgeting challenging for manufacturers. According to the International Energy Agency (IEA), crude oil prices experienced sharp volatility between 2021 and 2023, peaking above USD 120 per barrel before dropping below USD 70. Since synthetic rubber is derived from petrochemical feedstocks, these fluctuations directly affect production costs. In addition, disruptions in global shipping routes and container shortages have impacted the availability of imported raw materials.

MARKET OPPORTUNITIES

Increasing Demand for High-Performance Hoses in Renewable Energy Projects

The expanding renewable energy sector, particularly in solar thermal and wind power installations that require durable, heat-resistant, and flexible hose systems, is posing huge growth opportunities for the Asia Pacific rubber hose market. According to the International Renewable Energy Agency (IRENA), the Asia Pacific accounted for over 55% of global renewable energy investments in 2023, with countries like India, China, and Australia leading large-scale solar and wind projects.

Rising Need for Agricultural Irrigation Systems

The increasing demand for agricultural irrigation systems in countries facing water scarcity and erratic rainfall patterns is additionally to create new opportunities for the Asia Pacific rubber hose market. Rubber hoses are widely used in drip irrigation, sprinkler systems, and portable water distribution setups due to their flexibility, durability, and resistance to UV degradation. According to the Food and Agriculture Organization (FAO), over 60% of farmland in South and Southeast Asia relies on rain-fed irrigation, necessitating the deployment of efficient water distribution networks. In Indonesia, the Directorate General of Estate Crops encouraged farmers to adopt precision irrigation techniques, resulting in increased procurement of rubber-lined pipes and connectors. The Indonesian Agricultural Research Institute found that farms using rubber hose-based irrigation saw a 17% improvement in water efficiency compared to conventional methods.

MARKET CHALLENGES

Competition from Thermoplastic and Composite Hose Solutions

The increasing competition from thermoplastic and composite hose alternatives, which offer advantages such as lighter weight, greater flexibility, and enhanced resistance to extreme temperatures and abrasion, is certainly a challenging factor for the Asia Pacific rubber hose market growth. These materials are gaining traction in applications traditionally dominated by rubber, including automotive cooling systems, hydraulic circuits, and industrial fluid transfer. According to the American Chemistry Council, thermoplastic hoses accounted for nearly 30% of new industrial hose installations in Japan and South Korea in 2023, particularly in mobile equipment and robotics, cs where weight reduction is a key consideration.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.53% |

| Segments Covered | By Type, Pressure Rating, Application, End-Use, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of APAC |

| Market Leaders Profiled | Parker Hannifin Corp., Lomoflex Company Limited, Abbott Rubber Company Inc., Goodall Hoses, Anchor Rubber Products LLC, NewAge Industries Inc., Harrison Hose & Tubing Inc., Teknikum Oy, Kuriyama Holdings Corporation, Goodflex Rubber Co. Ltd. |

SEGMENTAL ANALYSIS

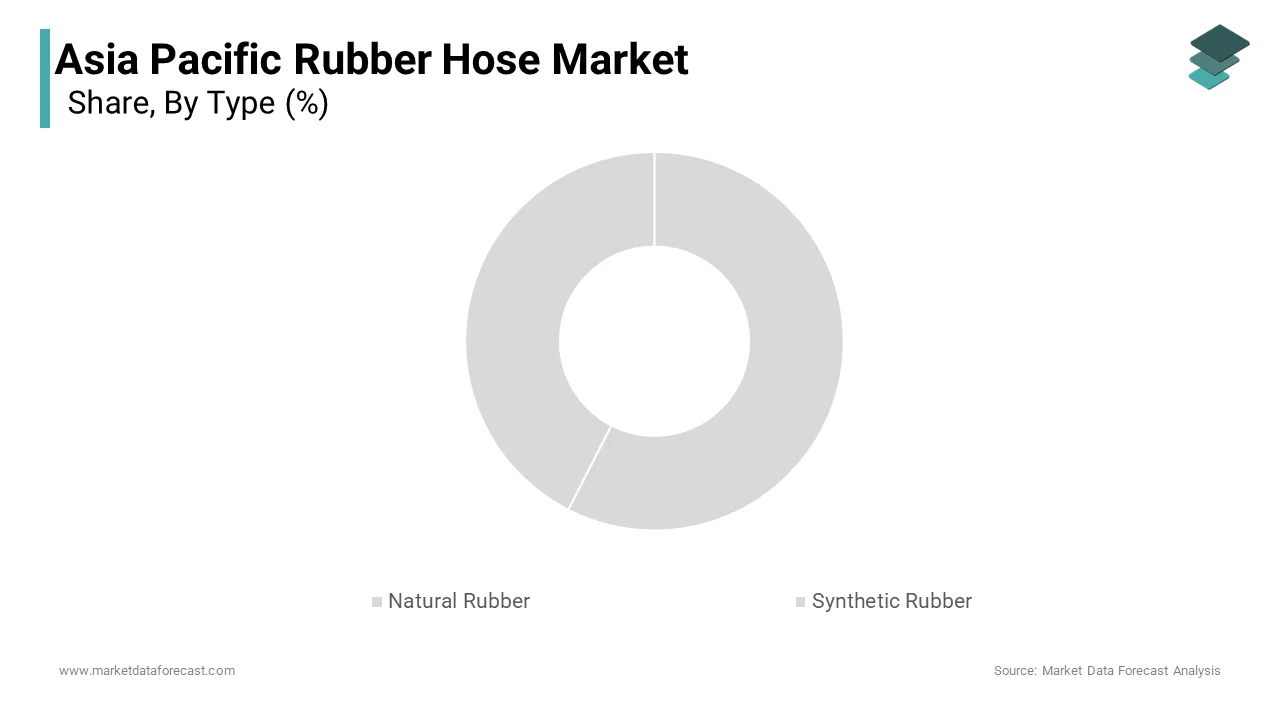

By Type Insights

The natural rubber segment dominated the Asia Pacific rubber hose market by accounting for 58.3% of the share in 2025, with the largest producer and consumer of natural rubber, particularly in countries like Thailand, Indonesia, and Vietnam. According to the International Rubber Study Group (IRSG), these three countries together accounted for over 65% of global natural rubber production in 2023. The proximity of raw material sources allows manufacturers in the region to maintain cost efficiency and supply chain resilience. Another contributing factor is the deep integration of natural rubber hoses in traditional industries such as agriculture and mining, where durability and elasticity are crucial. As per the ASEAN Rubber Producers’ Association, nearly 40% of all irrigation systems installed in Southeast Asia between 2021 and 2023 used natural rubber-based hoses due to their resistance to abrasion and moderate temperatures.

The synthetic rubber segment is swiftly emerging with an expected CAGR of 7.9% from 2025 to 2033, owing to the increasing demand for hoses that can withstand extreme temperatures, chemical exposure, and high-pressure environments, particularly in automotive, oil & gas, and heavy industrial sectors. Additionally, China’s growing investment in petrochemical infrastructure has led to increased consumption of synthetic rubber hoses in refinery and chemical processing plants. As reported by the China Petroleum and Chemical Industry Federation, new pipeline installations in western China required over 12 million meters of synthetic rubber-lined hoses in 2023 alone.

By Pressure Rating Insights

The medium-pressure hose segment accounted in holding 47.6% of the Asia Pacific rubber hose market in 2025 due to its extensive use in farm mechanization and rural water distribution systems, particularly in India, Indonesia, and the Philippines. According to the Food and Agriculture Organization (FAO), over 60 million hectares of farmland in South and Southeast Asia were equipped with low-to-medium pressure irrigation systems in 2023, each requiring durable rubber hoses for fluid transfer. Another contributing factor is the adoption of medium-pressure hoses in urban utility services, including drainage, sewage handling, and municipal cleaning equipment. In Australia, local authorities reported an increase in the deployment of mobile cleaning units using medium-pressure rubber hoses for stormwater drain maintenance.

The high-pressure hose segment is expected to grow with an expected CAGR of 8.4% from 2025 to 2033. This surge is fueled by increasing demand from energy-intensive industries such as oil & gas, mining, and hydraulic engineering, where reliability under extreme conditions is paramount. Another major factor is the modernization of construction and mining equipment, which increasingly uses high-pressure hoses for excavators, loaders, and underground drilling rigs. In India, the Ministry of Mines reported that coal and mineral extraction activities saw a 14% year-on-year increase in 2023, prompting greater demand for hydraulic hoses rated for pressures above 3,000 psi.

By Application Insights

The industrial application segment was the largest by capturing 41.2% of the Asia Pacific rubber hose market share in 2025, with the massive scale of manufacturing activity in countries like China, India, and South Korea, where production lines rely on rubber hoses for coolant circulation, pneumatic controls, and hydraulic power transmission. According to the United Nations Industrial Development Organization (UNIDO), manufacturing output in the Asia Pacific grew by 6.7% annually between 2019 and 2023, which is reinforcing the need for durable hose solutions in factory settings. Another contributing factor is the growing number of large-scale infrastructure projects, including steel mills, cement plants, and shipyards, which require specialized hoses for heavy-duty operations.

The municipal application segment is projected to expand with a CAGR of 9.1% in the coming years due to the intensifying focus on flood mitigation and wastewater treatment across coastal cities, particularly in the Philippines, Thailand, and Vietnam. Another significant factor is the expansion of smart city initiatives where municipalities are upgrading fire suppression systems, street cleaning vehicles, and waste collection mechanisms with high-efficiency hose components. In India, the Ministry of Housing and Urban Affairs reported that over 100 Smart Cities introduced new water jetting machines using high-durability rubber hoses for road and sewer cleaning in 2023.

By End-Use Industry Insights

The hydraulic industry was the largest by holding 33.3% of the Asia Pacific rubber hose market share in 2025, with the widespread deployment of hydraulic-powered construction and earthmoving equipment in China, India, and Indonesia, where infrastructure development remains a priority. Another contributing factor is the integration of hydraulic hose systems in factory automation and robotics, especially in South Korea and Japan, where precision and durability are critical. The Korea Institute of Industrial Technology reported a 17% rise in the use of reinforced rubber hoses in robotic arms and automated assembly lines in 2023.

The oil & gas segment is likely to register an anticipated CAGR of 9.6% from 2025 to 2033, owing to the expansion of liquefied natural gas (LNG) terminals and refining capacity, particularly in Australia, Malaysia, and China. Another key factor is the deployment of deep-sea drilling rigs and floating production, storage, and offloading (FPSO) vessels, which extensively use rubber hoses for subsea hydraulic connections and fluid transportation. The Australian Offshore Energy Report noted that the country’s offshore oil and gas sector commissioned five new FPSO units in 2023 alone, significantly boosting the sector's demand.

COUNTRY ANALYSIS

China Rubber Rose Market Analysis

China was the largest contributor in the Asia Pacific rubber hose market with 32.3% of share in 2025, owing to the scale of its construction and infrastructure development in second-tier cities and border regions, where government-backed projects continue to expand. Another contributing factor is the country’s role as a leading exporter of industrial and agricultural machinery, which requires standardized hose fittings and performance-grade materials. The China Chamber of Commerce for Import and Export of Machinery and Electronic Products reported a 16% increase in machinery exports in 2023.

India Rubber Rose Market Analysis

India was positioned next with 17.2% of the Asia Pacific rubber hose market share in 2025 due to the rapid industrialization, agricultural modernization, and increasing domestic vehicle production.

The booming automotive and commercial vehicle sector, which directly influences hose demand for engine cooling, braking, and transmissionsystemss is also expected to influence the growth of the market in this country. The Society of Indian Automobile Manufacturers (SIAM) reported that domestic vehicle production surpassed 28 million units in 2023, with OEMs sourcing millions of rubber hoses from local suppliers.

Japan's rubber hose market growth is driven by its emphasis on high-quality, engineered hose solutions tailored for automotive, aerospace, and precision manufacturing applications. Additionally, the heavy reliance on imported rubber hoses by Japanese automotive OEMs and Tier 1 suppliers, who prioritize product safety, longevity, and compliance with JIS standards, will also boost the growth of the market. The Japan Automobile Manufacturers Association noted that nearly 45% of all domestically produced cars featured rubber hose assemblies sourced from specialized domestic producers.

South Korea Rubber Rose Market Analysis

South Korea's rubber hose market is expected to grow with its well-developed industrial base, automotive sector, and growing investments in renewable energy infrastructure. A significant driver of South Korea’s market position is the expansion of its shipbuilding and heavy engineering industries, which rely on durable rubber hoses for hydraulic and marine applications.

Australia Rubber Rose Market Analysis

Australia's rubber hose market growth is likely to grow with its strategic emphasis on mining, resource extraction, and infrastructure development. The continued expansion of open-pit and underground mining operations, which require high-pressure rubber hoses for slurry transfer, dewatering, and hydraulic support systems, is also expected to fuel. According to the Minerals Council of Australia, the country’s mining output increased by 7.4% in 2023, with iron ore and coal mines being the primary consumers of industrial hoses. The government-backed push for disaster-resilient infrastructure in remote and arid regions, where firefighting and emergency water supply systems rely on durable rubber hoses. Indonesia's rubber hose market growth is driven by its dual role as a major natural rubber producer and a rapidly industrializing economy. Another key factor is the rising mechanization of agriculture and forestry, where irrigation, harvesting, and land preparation equipment rely on rubber hoses for hydraulic and cooling applications. The Indonesian Directorate General of Estate Crops reported that the number of mechanized palm oil estates rose by 19% in 2023, indicating a shift toward modern, hose-dependent equipment.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific rubber hose market is shaped by a mix of global conglomerates, regional manufacturers, and local suppliers vying for dominance in a rapidly expanding industrial landscape. Multinational firms leverage their technological expertise, extensive distribution networks, and brand recognition to maintain dominant positions in premium and regulated applications such as aerospace, offshore drilling, and high-pressure hydraulics.

Regional and domestic players are gaining traction by offering cost-effective, locally adapted hose solutions tailored to specific machinery and climate conditions. Their agility allows them to respond swiftly to changing market demands and regulatory shifts, making them formidable competitors in price-sensitive segments. Additionally, the market is witnessing increased collaboration between hose manufacturers and end-use industries to co-develop specialized products aligned with evolving operational requirements.

Regulatory pressures, raw material volatility, and rising consumer awareness are reshaping competitive priorities. Increasingly defined by innovation, environmental responsibility, and the ability to deliver scalable, high-quality hose solutions across diverse industrial platforms, is prompting the growth of the Asia Pacific rubber hose market.

KEY MARKET PLAYERS

These are the market players that are dominating the Asia Pacific rubber hose market.

- Parker Hannifin Corp.

- Lomoflex Company Limited

- Abbott Rubber Company Inc.

- Goodall Hoses

- Anchor Rubber Products LLC

- NewAge Industries Inc.

- Harrison Hose & Tubing Inc.

- Teknikum Oy

- Kuriyama Holdings Corporation

- Goodflex Rubber Co. Ltd.

Top Players In The Market

One of the leading players in the Asia Pacific rubber hose market is Continental AG, a German multinational with a strong regional presence. The company specializes in high-performance hydraulic, industrial, and automotive hoses tailored for extreme conditions. Continental contributes significantly to global standards by offering technologically advanced hose systems that integrate seamlessly into machinery, vehicles, and energy infrastructure across multiple industries. Another key player is Parker Hannifin Corporation, an American firm with extensive operations in Asia. Parker is known for its broad portfolio of engineered hose solutions used in aerospace, mobile hydraulics, and process industries. In the Asia Pacific, it supports critical sectors such as mining, oil & gas, and construction by delivering reliable, high-pressure hose assemblies designed for durability and safety.

Fujikura Rubber Ltd., based in Japan, is also a major contributor to the regional rubber hose landscape. Fujikura specializes in industrial and automotive hoses with a focus on precision engineering and thermal resistance. The company plays a crucial role in supporting Japanese automakers and industrial equipment manufacturers by supplying customized hose systems that meet rigorous quality and environmental performance criteria.

Top Strategies Used by Key Market Participants

A core strategy employed by leading companies in the Asia Pacific rubber hose market is product innovation through material science and application-specific design enhancements. Firms are investing heavily in R&D to develop hoses that offer superior resistance to heat, abrasion, and chemical exposure by ensuring longer service life and compliance with evolving industry standards.

Another major approach is expanding regional manufacturing capabilities and forming strategic partnerships with local distributors and OEMs. Companies can reduce lead times, comply with regional regulations, and better serve domestic demand by establishing production hubs closer to high-growth markets in India, Southeast Asia, and Australia.

Adopting digitalization and predictive maintenance technologies in hose assembly systems has become a priority for industry leaders. Companies are integrating smart sensors and condition-monitoring features into their products to enhance reliability and support Industry 4.0 trends, positioning themselves as providers of not just components but complete fluid transfer solutions.

RECENT MARKET NEWS

- In March 2025, Continental AG launched a new line of ultra-durable synthetic rubber hoses specifically engineered for use in hydrogen refueling stations. This initiative was aimed at supporting the growing green mobility sector in South Korea and Japan, which is reinforcing Continental’s dominance in high-performance hose technology.

- In February 2025, Parker Hannifin announced a joint venture with a leading Indian industrial equipment manufacturer to establish a dedicated hose assembly facility in Pune. This move was intended to strengthen Parker’s supply chain and improve responsiveness to the booming demand from the construction and agricultural sectors.

- In January 2025, Fujikura Rubber Ltd. commissioned a state-of-the-art testing center in Yokohama focused on validating hose performance under extreme pressure and temperature conditions. This investment aligns with Fujikura’s commitment to quality assurance and enhances its credibility among Japanese and international OEM clients.

- In May 2025, Goodyear Engineered Products, now part of EnPro Industries, expanded its distribution network in Thailand to cater to the increasing demand for hydraulic and agricultural hoses in Southeast Asia. This expansion was designed to improve customer access and after-sales support for industrial clients.

- In June 2025, Trelleborg AB, a Swedish manufacturer specializing in engineered polymer solutions, introduced a new range of fire-resistant rubber hoses at an industrial trade fair in Singapore. These hoses were developed in collaboration with Australian emergency services and maritime operators to meet stringent safety and durability standards in harsh environments.

MARKET SEGMENTATION

This research report on the Asia Pacific rubber rose market is segmented and sub-segmented into the following categories.

By Type

- Natural Rubber

- Synthetic Rubber

- Ethylene Propylene

- Fluoroelastomer

- Isobutylene Isoprene Butyl

- Isoprene

- Polyurethane

- Vinyl

- Silicone Rubber

- Others (Nitrile Rubber, Polychloroprene)

By Pressure Rating

- Low

- Medium

- High

By Application

- Home

- Commercial

- Industrial

- Municipal

By End-User

- Oil & Gas

- Automotive

- Hydraulic

- Agriculture

- Food & Beverages

- Chemicals

- Infrastructure

- Mining

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC