Asia Pacific Semiconductor Manufacturing Equipment Market Research Report – Segmented By Equipment Type( Front-end Equipment , Back-end Equipment) Dimension, Application and Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis on Size, Share, Trends& Growth Forecast from 2025 to 2033

Asia Pacific Semiconductor Manufacturing Equipment Market Size

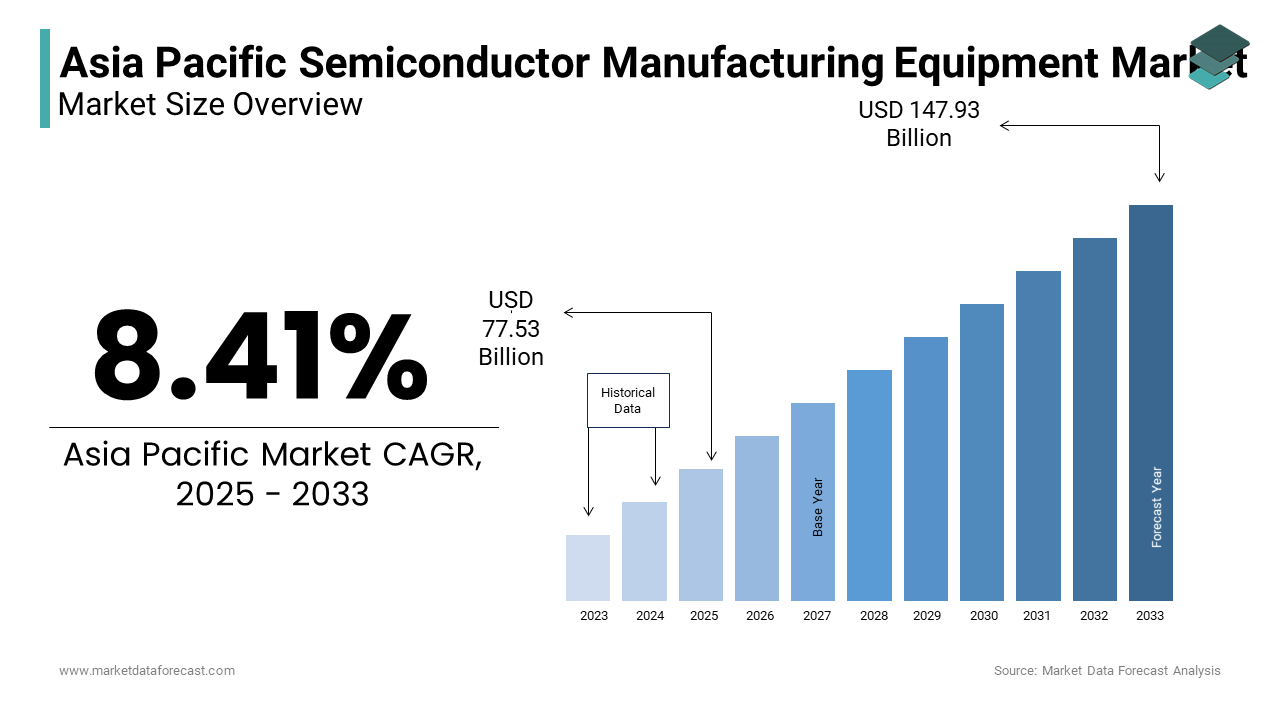

The Asia Pacific Semiconductor Manufacturing Equipment Market Size was valued at USD 71.52 billion in 2024. The Asia Pacific Semiconductor Manufacturing Equipment Market size is expected to have 8.41% CAGR from 2025 to 2033 and be worth USD 147.93 billion by 2033 from USD 77.53 billion in 2025.

The Asia Pacific semiconductor manufacturing equipment market has cemented its position as a cornerstone of global technological advancement, driven by the region's dominance in semiconductor production. Like, Asia Pacific accounts for a significant majority of global semiconductor fabrication capacity, with countries like Taiwan, South Korea, and China leading the charge. Taiwan’s TSMC alone commands substantial share of the global foundry market, showing the region's critical role in semiconductor innovation. The demand for advanced manufacturing equipment is further fueled by the proliferation of 5G, artificial intelligence, and IoT technologies.

Government initiatives, such as China’s "Made in China 2025" policy, which allocates $150 billion to boost domestic semiconductor capabilities, amplify this growth. Additionally, the rise of electric vehicles and smart devices necessitates more sophisticated chips, driving investments in next-generation equipment. Despite geopolitical tensions and supply chain disruptions, the region remains a hub of innovation, supported by strong collaboration between equipment manufacturers and semiconductor fabs.

MARKET DRIVERS

Surging Demand for Advanced Electronics

The escalating demand for advanced electronics serves as a primary driver for the Asia Pacific semiconductor manufacturing equipment market. According to projections, global shipments of smartphones, laptops, and IoT devices are expected to exceed 2 billion units annually by 2025, with Asia Pacific accounting for over 60% of this consumption. This surge is propelled by rising disposable incomes and urbanization, particularly in emerging economies like India and Vietnam. Moreover, the advent of 5G technology amplifies this trend. Plus, the number of 5G subscriptions in Asia Pacific is expected to surpass 1 billion by 2026, necessitating advanced chips for network infrastructure and consumer devices. This demand drives investments in state-of-the-art lithography and etching tools, enabling manufacturers to produce smaller, faster, and more efficient semiconductors.

Government Initiatives and Localization Efforts

Government initiatives aimed at boosting domestic semiconductor capabilities significantly drive the Asia Pacific semiconductor manufacturing equipment market. Localization efforts also gain momentum amid geopolitical uncertainties. As per Boston Consulting Group, over 50% of global semiconductor companies are reassessing their supply chains, prioritizing regional hubs. This shift necessitates the procurement of cutting-edge tools like deposition and inspection systems. Furthermore, partnerships between governments and private players, such as Taiwan’s collaboration with ASML, showcasing the strategic importance of securing advanced equipment. These initiatives not only bolster regional manufacturing capabilities but also ensure long-term resilience, positioning the Asia Pacific market as a global leader in semiconductor innovation.

MARKET RESTRAINTS

Geopolitical Tensions and Export Restrictions

Geopolitical tensions and export restrictions pose significant challenges to the Asia Pacific semiconductor manufacturing equipment market, disrupting supply chains and stifling growth. Like, escalating trade disputes between the U.S. and China have led to stringent export controls on advanced semiconductor technologies. For instance, restrictions on the sale of extreme ultraviolet (EUV) lithography machines to Chinese fabs have severely impacted their ability to produce cutting-edge chips. These measures create bottlenecks, forcing manufacturers to seek alternative suppliers or delay production timelines. Further, the weaponization of technology trade exacerbates uncertainty. This instability deters investments in new equipment, particularly in countries like China, where reliance on imported tools remains high. Moreover, the lack of indigenous alternatives limits flexibility, further straining the market. While some nations attempt to localize production, the time and cost required to develop competitive equipment hinder progress, leaving the region vulnerable to external pressures.

High Costs of Equipment and R&D Investments

The prohibitively high costs of semiconductor manufacturing equipment and the associated R&D investments act as a major restraint for the Asia Pacific market. This financial barrier limits participation in advanced chip production, particularly in developing economies like India and Southeast Asia. In addition, the rapid pace of technological advancements necessitates continuous upgrades, further straining budgets. This expenditure is often beyond the reach of regional players, forcing them to rely on foreign manufacturers for cutting-edge tools. Furthermore, the complexity of equipment installation and maintenance increases operational costs, deterring new entrants.

MARKET OPPORTUNITIES

Expansion of Electric Vehicle Production

The rapid expansion of electric vehicle (EV) production presents a transformative opportunity for the Asia Pacific semiconductor manufacturing equipment market. According to BloombergNEF, EV sales in the region are projected to reach 20 million units annually by 2030, accounting for over 50% of global EV sales. This surge is driven by government incentives and environmental regulations, particularly in China, which aims to phase out internal combustion engines by 2040. For instance, silicon carbide (SiC) and gallium nitride (GaN) semiconductors, critical for EV efficiency, require cutting-edge epitaxy and deposition tools. Manufacturers investing in these technologies can capitalize on partnerships with automotive giants like BYD and Hyundai.

Growth of AI and Data Centers

The proliferation of artificial intelligence (AI) and data centers offers another significant opportunity for the Asia Pacific semiconductor manufacturing equipment market. Countries like Japan and South Korea are at the forefront of AI innovation, necessitating advanced chips for machine learning and data processing. Data centers, too, play a pivotal role. This trend fuels demand for precision tools like chemical vapor deposition (CVD) and atomic layer deposition (ALD) systems. Additionally, the rise of edge computing amplifies semiconductor needs, creating opportunities for equipment manufacturers.

MARKET CHALLENGES

Supply Chain Vulnerabilities

Supply chain vulnerabilities represent a significant challenge for the Asia Pacific semiconductor manufacturing equipment market, exacerbated by the complexity and globalization of the industry. Also, a significant majority of semiconductor materials and components are sourced from a limited number of suppliers, primarily concentrated in East Asia. This dependency creates risks, as demonstrated by the 2021 global chip shortage, which disrupted industries ranging from automotive to consumer electronics. For instance, Toyota and Hyundai faced production halts due to insufficient chip supplies, highlighting the cascading effects of supply chain disruptions. Natural disasters further compound these vulnerabilities. As per the Asian Development Bank, typhoons and earthquakes in Taiwan and Japan frequently disrupt semiconductor fabs, delaying equipment deliveries and increasing lead times. Additionally, logistical bottlenecks, such as port congestion and shipping delays, inflate costs and reduce efficiency.

Talent Shortages in High-Tech Roles

Talent shortages in high-tech roles pose another critical challenge for the Asia Pacific semiconductor manufacturing equipment market, hindering innovation and operational efficiency. Similarly, the semiconductor industry requires over 1 million skilled professionals annually, yet the current workforce falls short by approximately 30%. This gap is particularly pronounced in emerging economies like Vietnam and Indonesia, where educational infrastructure struggles to keep pace with technological advancements. Specialized roles, such as process engineers and equipment technicians, are in acute demand. Additionally, the rapid evolution of semiconductor technologies necessitates continuous upskilling, which many organizations fail to address adequately. This scarcity not only slows down equipment deployment but also increases labor costs, as companies compete for limited talent.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 8.41 % |

| Segments Covered | By Equipment Type,Dimension,Application and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | China, India, Japan, South Korea, Australia, New Zealand, Thailand, Indonesia, Philippines, Vietnam, Singapore, Rest of APAC. |

| Market Leader Profiled | Lam Research Corp, KLA Corp, ASML Holding NV ADR, Tokyo Electron Ltd, Advantest Corp. |

SEGMENTAL ANALYSIS

By Equipment Type Insights

The segment of Front-end equipment segment dominated the Asia Pacific semiconductor manufacturing equipment market by holding a commanding 65.5% market share in 2024. This dominance is driven by the critical role of front-end processes in semiconductor fabrication, including wafer production, lithography, etching, and deposition. Like, a considerable portion of semiconductor manufacturing costs are attributed to front-end processes, underscoring their importance. One key factor fueling this segment’s growth is the surging demand for advanced chips used in AI, 5G, and IoT applications. For instance, TSMC, a global leader in semiconductor manufacturing, invests substantial amount annually in front-end equipment to produce cutting-edge 3nm and 2nm chips. Additionally, the rise of electric vehicles (EVs) amplifies demand for silicon carbide (SiC) wafers, which require specialized front-end tools. Another driving factor is government initiatives aimed at boosting domestic semiconductor capabilities. China’s "Made in China 2025" policy allocates $150 billion to enhance local semiconductor fabs, necessitating extensive investments in front-end equipment.

The Back-end equipment is the fastest-growing segment in the Asia Pacific semiconductor manufacturing equipment market, with a projected CAGR of 9.5% through 2033. This is fueled by the increasing complexity of semiconductor packaging, particularly in advanced applications like 2.5D and 3D integration. For example, the rise of high-performance computing (HPC) chips, which require sophisticated packaging solutions, drives demand for back-end tools such as die bonders and wire bonders. Another major point is the proliferation of consumer electronics, including smartphones and wearables. These devices rely on compact and efficient semiconductor packages, necessitating advanced back-end equipment. Also, the shift toward heterogeneous integration, where multiple chips are combined into a single package, further accelerates adoption.

By Dimension Insights

The 2D semiconductor manufacturing segment held the largest share of the Asia Pacific semiconductor manufacturing equipment market i.e. 55.3% in 2024. This segment's prominence is due to its widespread application in traditional semiconductor devices, such as microprocessors and memory chips. According to PwC, over 80% of semiconductors produced globally still rely on 2D architectures, ensuring sustained demand for related equipment. One driving factor is the massive scale of semiconductor production in the region. For instance, South Korea’s Samsung and SK Hynix dominate the global memory chip market, producing DRAM and NAND flash chips using 2D technologies. These companies invest heavily in photolithography and etching tools, which are essential for 2D manufacturing. Additionally, the ongoing demand for consumer electronics, such as laptops and TVs, sustains the need for 2D chips. Government support also plays a crucial role. China’s push for self-sufficiency in semiconductor production prioritizes 2D technologies due to their established manufacturing processes.

The 3D semiconductor manufacturing is the quickest one to expand in the Asia Pacific semiconductor manufacturing equipment market, with a projected CAGR of 12.3%. This rapid growth is driven by the increasing adoption of 3D integration in high-performance applications, such as AI accelerators and advanced memory chips. For instance, Samsung’s 3D V-NAND technology has revolutionized storage solutions, requiring specialized equipment for vertical stacking. Another key driver is the rise of heterogeneous integration, where multiple chips are stacked to enhance performance and reduce power consumption. This trend is particularly evident in Taiwan, where TSMC leverages 3D packaging for its CoWoS (Chip on Wafer on Substrate) technology. Also, the proliferation of 5G and IoT devices, which demand compact and efficient designs, further amplifies demand for 3D manufacturing tools.

By Application Insights

The segment of semiconductor fabrication plants, or foundries, represented the largest application in the Asia Pacific semiconductor manufacturing equipment market i.e. 50.4% share in 2024. This dominance is driven by the region’s leadership in semiconductor production, with countries like Taiwan, South Korea, and China hosting the world’s most advanced fabs. One crucial factor is the surge in demand for advanced chips used in AI, 5G, and automotive applications. For example, TSMC’s expansion of its 3nm fab in Taiwan required substantial investment in state-of-the-art equipment. Similarly, South Korea’s Samsung and SK Hynix dominate the memory chip market, relying heavily on cutting-edge lithography and deposition tools. Further, government initiatives, such as China’s "Made in China 2025" policy, prioritize the establishment of local fabs, further boosting equipment demand.

The test home segment is the quickly moving application in the Asia Pacific semiconductor manufacturing equipment market, with a projected CAGR of 10.8%. This is backed by the increasing complexity of semiconductor testing, particularly for advanced chips used in AI, IoT, and automotive applications. For instance, the rise of autonomous vehicles necessitates rigorous testing of safety-critical chips, driving demand for advanced testing equipment. Another key aspect is the proliferation of consumer electronics, which require comprehensive testing to ensure reliability and performance. These devices rely on sophisticated testing solutions to validate functionality. Additionally, the adoption of automated testing systems enhances efficiency, further propelling growth.

COUNTRY LEVEL ANALYSIS

Taiwan stood as the undisputed leader in the Asia Pacific semiconductor manufacturing equipment market by holding a 30% market share in 2024. The country’s leading position is underpinned by its status as a global hub for semiconductor fabrication, with TSMC commanding a significant share of the global foundry market. Taiwan’s strategic investments in advanced technologies, such as EUV lithography, ensure its leadership in producing cutting-edge chips. Government support further amplifies Taiwan’s position. According to the Ministry of Economic Affairs, Taiwan plans to invest over $100 billion in semiconductor manufacturing by 2025, focusing on expanding 3nm and 2nm production capabilities. Additionally, collaborations with global players like ASML strengthen its technological edge. The concentration of world-class fabs and equipment suppliers positions Taiwan as a cornerstone of the regional market.

China is trailing in the Asia Pacific semiconductor manufacturing equipment market and has made major strides. The country’s aggressive push for self-sufficiency, driven by its "Made in China 2025" policy, fuels demand for advanced equipment. Localization efforts are gaining momentum. For instance, SMIC, China’s largest semiconductor manufacturer, recently achieved breakthroughs in 7nm production, reducing dependence on imported chips. Additionally, partnerships with domestic equipment manufacturers, such as NAURA Technology, bolster supply chain resilience.

South Korea commands a notable share of the Asia Pacific semiconductor manufacturing equipment market. The country’s position is driven by its dominance in memory chip production, with Samsung and SK Hynix leading the charge. Government initiatives further amplify growth. For example, South Korea’s K-Semiconductor Strategy plans to invest $450 billion by 2030 to strengthen its place in memory and logic chips. Further, collaborations with global equipment suppliers, such as Applied Materials, ensure access to cutting-edge tools.

Japan is another key player in the Asia Pacific semiconductor manufacturing equipment market. The country’s strength lies in its expertise in semiconductor materials and equipment manufacturing. For instance, Tokyo Electron Limited (TEL) is a global leader in deposition and etching tools, catering to both domestic and international markets. Government support plays a pivotal role. Additionally, partnerships with global players like TSMC and Intel strengthen its technological capabilities.

Singapore commands a smaller share of the Asia Pacific semiconductor manufacturing equipment market. The country’s business is driven by its role as a regional hub for semiconductor R&D and manufacturing. For example, GlobalFoundries operates one of its largest fabs in Singapore, producing chips for automotive and IoT applications. Government incentives further amplify growth. Also, Singapore offers tax breaks and grants to attract semiconductor investments, with a focus on advanced packaging and testing. Additionally, collaborations with global players like Micron and STMicroelectronics bolster its technological edge.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the Asia Pacific semiconductor manufacturing equipment market are Applied Materials Inc, Lam Research Corp, KLA Corp, ASML Holding NV ADR, Tokyo Electron Ltd, Advantest Corp, Screen Holdings Co Ltd, Cohu Inc, ACM Research Inc Class A, Nordson Corp, EV Short Duration Diversified, Ferrotec Holdings Corp, Tokyo Seimitsu, Modutek.

The Asia Pacific semiconductor manufacturing equipment market is characterized by intense competition, driven by the presence of global giants and regional players vying for dominance. Established companies like Applied Materials, Tokyo Electron, and ASML leverage their technological expertise and extensive distribution networks to maintain leadership. Meanwhile, local manufacturers compete aggressively on pricing, offering cost-effective solutions tailored to budget-conscious customers. The market’s competitive landscape is further shaped by rapid technological advancements and government initiatives aimed at boosting domestic semiconductor capabilities. To differentiate themselves, players focus on innovation, introducing cutting-edge tools for advanced nodes and packaging applications. Sustainability initiatives, such as low-emission designs, are also gaining traction amid stricter environmental regulations. Collaborations with governments and participation in mega-projects further underscore the strategic maneuvers undertaken by key participants.

Top Players in the Market

Applied Materials

Applied Materials is a key player in the Asia Pacific semiconductor manufacturing equipment market, renowned for its innovative solutions in deposition, etching, and inspection systems. The company’s focus on enabling advanced nodes, such as 3nm and below, has strengthened its appeal among regional fabs. In recent years, Applied Materials launched its "AI-Driven Process Control" platform, enhancing precision and efficiency in semiconductor production. To bolster its presence, the company expanded its R&D centers in Taiwan and South Korea, fostering closer collaborations with leading manufacturers like TSMC and Samsung. Additionally, partnerships with local universities ensure a steady pipeline of skilled talent, reinforcing its leadership in the region.

Tokyo Electron Limited (TEL)

Tokyo Electron Limited (TEL) plays a pivotal role in the Asia Pacific semiconductor manufacturing equipment market, specializing in lithography, deposition, and etching tools. TEL’s commitment to sustainability is evident in its development of eco-friendly equipment, aligning with regional environmental regulations. Recently, TEL introduced its next-generation deposition systems, designed for 2.5D and 3D packaging applications. The company also established a new manufacturing facility in China to cater to rising demand. Collaborations with domestic players, such as SMIC, further solidify its position.

ASML Holding

ASML Holding is a dominant force in the Asia Pacific semiconductor manufacturing equipment market, particularly in lithography systems. Its EUV (Extreme Ultraviolet) technology is critical for producing advanced chips used in AI, 5G, and automotive applications. ASML’s strategic partnerships with regional leaders, such as TSMC and Samsung, ensure the adoption of its cutting-edge tools. Additionally, the company invested in expanding its supply chain network across Asia to mitigate logistical challenges.

Top Strategies Used by Key Market Participants

Key players in the Asia Pacific semiconductor manufacturing equipment market employ diverse strategies to maintain their competitive edge. Innovation and R&D investments rank among the most prominent approaches, with companies developing advanced technologies like EUV lithography and 3D packaging solutions. Strategic partnerships and collaborations are also widely adopted, enabling firms to tap into emerging markets and secure contracts for large-scale projects. Localization efforts, such as establishing regional manufacturing hubs, reduce costs and improve supply chain resilience. Sustainability-focused measures, such as developing energy-efficient equipment, further strengthen market positioning. Lastly, after-sales services, including predictive maintenance and operator training, play a pivotal role in fostering customer loyalty and driving repeat business.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, Applied Materials launched its "AI-Driven Process Control" platform in Taiwan, enhancing precision and efficiency in semiconductor fabrication.

- In May 2023, Tokyo Electron Limited inaugurated a new manufacturing facility in China, increasing its production capacity for advanced deposition systems.

- In July 2023, ASML Holding opened a training center in South Korea to provide expertise in EUV lithography systems, strengthening its regional presence.

- In September 2023, Lam Research partnered with SMIC to develop next-generation etching tools, targeting 3nm chip production in China.

- In November 2023, KLA Corporation expanded its inspection tool portfolio in Japan, catering to growing demand for defect detection in advanced nodes.

MARKET SEGMENTATION

This research report on the asia pacific semiconductor manufacturing equipment market has been segmented and sub-segmented into the following.

By Equipment Type

- Front-end Equipment

- Back-end Equipment

By Dimension

- 2D Semiconductor Manufacturing

- 3D Semiconductor Manufacturing

By Application

- Semiconductor Fabrication Plant/Foundry

- Test Home

By Country

- China

- India

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Indonesia

- Philippines

- Vietnam

- Singapore

- Rest of APAC

Frequently Asked Questions

Which countries are leading the market in the Asia Pacific region?

Taiwan, South Korea, China, and Japan are the top contributors due to their strong presence of foundries like TSMC, Samsung, and SMIC, as well as investments in research and development.

How is China impacting the Asia Pacific semiconductor equipment market?

China is heavily investing in self-sufficiency through initiatives like "Made in China 2025," which has led to increased domestic production and higher demand for semiconductor equipment.

How are governments in the Asia Pacific region supporting the semiconductor sector?

Governments are offering subsidies, tax incentives, and public-private partnerships to boost semiconductor manufacturing and reduce reliance on imports.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com