Asia Pacific Semiconductor Materials Market Size, Share, Trends & Growth Forecast Report By Material (Silicon Carbide, Molybdenum Disulfide (MoS₂)), Application, End User, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore And Rest Of Asia-Pacific), Industry Analysis From 2025 To 2033

Asia Pacific Semiconductor Materials Market Size

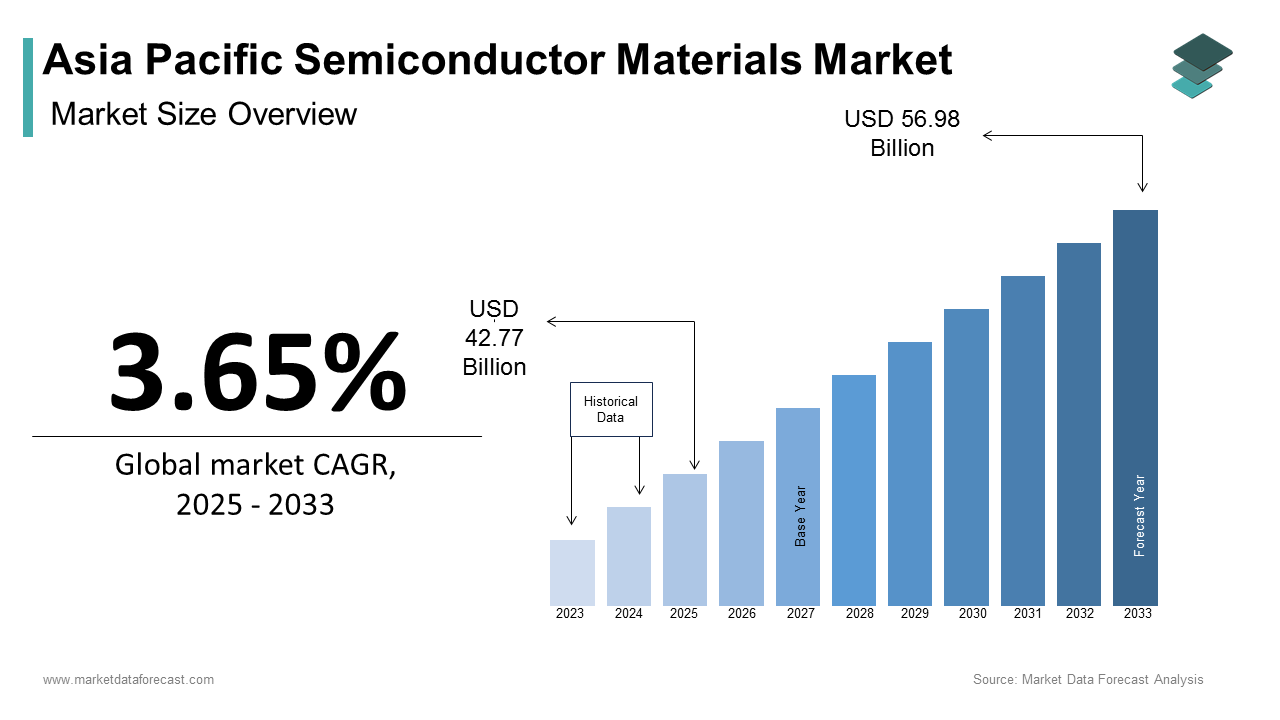

The Asia Pacific semiconductor materials market size was calculated to be USD 41.26 billion in 2024 and is anticipated to be worth USD 56.98 billion by 2033, from USD 42.77 billion in 2025, growing at a CAGR of 3.65% during the forecast period.

The Asia Pacific semiconductor materials market includes a broad spectrum of raw materials essential for the fabrication and packaging of semiconductors, including silicon wafers, photoresists, gases, polishing materials, and chemical mechanical planarization (CMP) slurries. These materials serve as the foundational components in the production of integrated circuits (ICs), memory chips, and other electronic devices that power modern technology. The region has emerged as a global hub for semiconductor manufacturing, driven by the presence of key industry players, government-led technological initiatives, and increasing investments in electronics infrastructure.

Countries such as China, South Korea, Japan, and Taiwan are at the forefront of semiconductor material consumption, reflecting their dominant roles in global chip fabrication. According to SIA (Semiconductor Industry Association), as of 2023, the Asia Pacific region accounted for over 65% of global semiconductor manufacturing capacity, with China alone contributing substantially to total global wafer fabrication facilities (fabs) under construction. This growing infrastructure is directly influencing demand for semiconductor-grade materials. Also, India’s recent push into indigenous semiconductor manufacturing, backed by a $10 billion incentive package, further signals the region's long-term commitment to building local supply chains.

MARKET DRIVERS

Expansion of Semiconductor Manufacturing Capacity Across APAC

One of the primary drivers fueling growth in the Asia Pacific semiconductor materials market is the expansion of semiconductor manufacturing facilities across the region, particularly in response to global supply chain disruptions and increased domestic demand. Countries like China, India, and Vietnam are investing heavily in establishing new fabrication units, which significantly increases the consumption of semiconductor materials such as silicon wafers, photoresist chemicals, and process gases. Each of these facilities will require vast quantities of copper electroplating solutions, CMP slurries, and etching gases to support mass production. Moreover, countries like Malaysia and Thailand are also positioning themselves as secondary hubs for semiconductor assembly and testing, which necessitates a continuous flow of packaging materials such as epoxy mold compounds and gold wire.

Rising Demand for Advanced Packaging and Chiplet Technologies

Another significant driver of the Asia Pacific semiconductor materials market is the growing adoption of advanced packaging technologies and chipset-based designs, which require specialized materials not traditionally used in conventional packaging. As device miniaturization accelerates and Moore’s Law slows down, companies are increasingly turning to 2.5D/3D packaging, fan-out wafer-level packaging (FOWLP), and system-in-package (SiP) solutions to enhance performance and reduce latency. These advanced packaging methods rely heavily on novel materials such as underfill resins, thermal interface materials, redistribution layer (RDL) polymers, and low-k dielectrics. According to SEMI, the global market for advanced packaging materials is projected to exceed $16 billion by 2027, with APAC accounting for a major share of this demand, driven by foundries in South Korea, Japan, and Taiwan.

MARKET RESTRAINTS

Supply Chain Disruptions and Raw Material Shortages

A major restraint affecting the Asia Pacific semiconductor materials market is the persistent instability in the global supply chain, particularly concerning the sourcing of rare and high-purity raw materials required for semiconductor fabrication. Materials such as gallium arsenide, germanium, and high-purity quartz are crucial for wafer production, but geopolitical tensions and export restrictions have created bottlenecks in availability. China, which dominates global gallium production, has imposed export quotas on several critical metals due to environmental concerns and domestic industrial needs. According to the U.S. Geological Survey, in 2023, global gallium prices surged due to reduced exports from China, directly impacting semiconductor manufacturers across South Korea, Japan, and Taiwan, which rely heavily on imported raw materials. Also, Japan and South Korea have faced challenges in securing stable supplies of fluorinated gases and hydrogen fluoride, both essential for etching and cleaning processes. Following export restrictions during the Japan–South Korea trade dispute, companies had to seek alternative sources, often at higher costs and lower purity levels. Furthermore, natural disasters and logistical delays have compounded these issues. Typhoon-induced floods in Thailand in late 2023 disrupted transportation networks, delaying shipments of silicon wafers and photoresist chemicals from Japanese suppliers.

Environmental Regulations and Waste Management Challenges

Environmental regulations and waste management requirements are emerging as significant restraints on the growth of the Asia Pacific semiconductor materials market. The production of semiconductor materials involves the use of highly toxic substances such as hydrofluoric acid, phosphine gas, and various heavy metals which pose severe risks to human health and the environment if not handled properly. Governments in Japan, South Korea, and Singapore have implemented stringent emission norms and waste disposal mandates that increase the operational costs for semiconductor material producers. For example, the Ministry of Environment in Japan mandated stricter monitoring of per- and polyfluoroalkyl substances (PFAS) emissions in 2023, compelling manufacturers to invest in more expensive filtration and purification systems. In one case, a major silicon wafer plant near Shanghai was fined over $2 million for illegal discharge of hazardous waste, causing production delays lasting more than three months. Besides, the EU’s Restriction of Hazardous Substances (RoHS) Directive has influenced multinational companies operating in APAC to adopt cleaner alternatives, even though not legally required locally. This compliance requirement forces material manufacturers to reformulate or replace certain chemicals, adding time and cost to product development cycles.

MARKET OPPORTUNITIES

Growth in EV and Power Electronics Driving Wide Bandgap Semiconductor Adoption

A significant opportunity in the Asia Pacific semiconductor materials market lies in the rising demand for wide bandgap (WBG) semiconductors, particularly silicon carbide (SiC) and gallium nitride (GaN), driven by their superior efficiency and thermal properties over traditional silicon-based devices. These materials are becoming indispensable in electric vehicles (EVs), renewable energy systems, and industrial power electronics. Many of these vehicles now incorporate SiC-based power modules in inverters and onboard chargers, offering improved energy efficiency and longer driving ranges. Japan and South Korea are home to several material suppliers specializing in SiC and GaN substrates, epitaxial layers, and deposition equipment. Moreover, governments across the region are promoting green technologies. In India, the Production-Linked Incentive (PLI) Scheme for Advanced Chemistry Cell Battery Storage includes provisions for WBG semiconductor development, encouraging domestic startups and manufacturers to enter the space.

Indigenous Semiconductor Ecosystem Development in Emerging APAC Economies

Another transformative opportunity for the Asia Pacific semiconductor materials market is the emergence of national semiconductor strategies in countries like India, Vietnam, and Indonesia, aimed at reducing dependency on foreign suppliers and fostering local manufacturing ecosystems. These efforts are opening up new demand channels for semiconductor materials previously dominated by established hubs like South Korea, Japan, and Taiwan. India, for instance, launched its Semiconductor Mission in 2022, backed by a $10 billion fiscal incentive package, to attract investment in semiconductor fabrication, packaging, and display manufacturing. As of 2023, six semiconductor projects totaling over $15 billion in planned investment have been announced, including joint ventures between global firms and Indian partners. Each of these projects requires extensive procurement of silicon wafers, deposition materials, and photolithography chemicals. Similarly, Vietnam is positioning itself as an electronics manufacturing center, particularly for assembly and testing operations. According to the Vietnam Chamber of Commerce and Industry (VCCI), as of mid-2023, foreign direct investment (FDI) in Vietnamese semiconductor and electronics sectors grew notably YoY, signaling expanding opportunities for material suppliers.

MARKET CHALLENGES

Intense Global Competition and Pricing Pressures

A major challenge facing the Asia Pacific semiconductor materials market is the intensifying global competition, especially from North America and Europe, which are aggressively investing in domestic semiconductor industries. This has led to price pressure on APAC-based material suppliers trying to maintain margins while competing with subsidized international rivals. The United States’ CHIPS and Science Act, providing over $52 billion in funding for domestic semiconductor manufacturing, has enabled American companies to invest in cutting-edge materials and production techniques. Similarly, the European Union’s Chips Act, allocating €43 billion (~$47 billion), supports the revival of semiconductor manufacturing within Europe, including advanced materials development. These subsidies allow Western firms to offer competitive pricing, squeezing smaller APAC suppliers out of global contracts. Japanese and South Korean companies, although technologically advanced, also face pressure from Chinese firms offering lower-cost alternatives. This price sensitivity makes it difficult for premium APAC material providers to retain market share without compromising profitability. Apart from these, large semiconductor foundries in the region are increasingly negotiating bulk discounts and long-term fixed-price contracts, limiting revenue flexibility for material suppliers.

Talent Shortage and High R&D Costs in Material Innovation

Another pressing challenge in the Asia Pacific semiconductor materials market is the scarcity of skilled professionals and the high cost of research and development (R&D) required to keep pace with rapidly evolving semiconductor technologies. Developing next-generation materials—such as extreme ultraviolet (EUV) lithography-compatible resists, atomic-layer deposition precursors, and quantum dot materials —requires deep technical expertise and capital-intensive innovation. According to the Semiconductor Industry Association (SIA), as of 2023, the global shortage of semiconductor engineers exceeded 300,000, with the Asia Pacific region being particularly affected despite its educational infrastructure. Although countries like South Korea and Japan produce a large number of engineering graduates, the attrition rate in semiconductor R&D remains high, with many professionals shifting to software and AI fields for better compensation and work-life balance. Moreover, R&D in semiconductor materials is extremely costly. Developing a single new photoresist formulation can require over $50 million in investment and take up to five years, as per data from Tokyo Electron’s internal research division. Smaller firms in the APAC region often lack the financial muscle to compete with global giants like JSR, Shin-Etsu Chemical, and BASF, which dominate the high-end material space. Collaborative research initiatives between universities and corporations are somewhat alleviating the burden, but limited IP-sharing agreements and fragmented innovation ecosystems in the region hinder broader progress.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.65% |

| Segments Covered | By Material, Application, End User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of Asia-Pacific |

| Market Leaders Profiled | Tokyo Ohka Kogyo Co., Ltd., DuPont de Nemours, Inc., BASF SE, Hitachi Chemical Co., Ltd., JSR Corporation, Shin-Etsu Chemical Co., Ltd., Sumitomo Chemical Co., Ltd., LG Chem Ltd., Samsung SDI Co., Ltd., Showa Denko K.K. |

SEGMENTAL ANALYSIS

By Material Insights

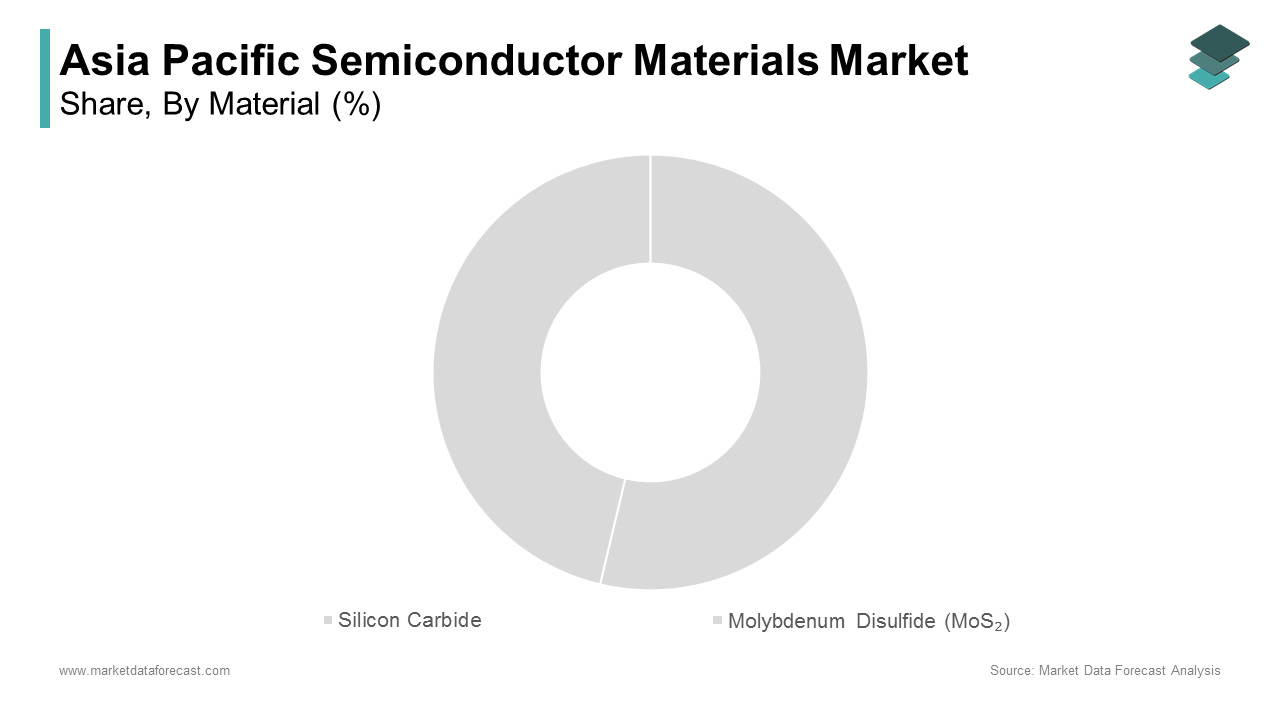

The silicon Carbide (SiC) is the largest segment in the Asia Pacific semiconductor materials market accounting for 34.6% of total consumption in 2024. As a wide bandgap (WBG) material, SiC outperforms traditional silicon in high-power, high-temperature, and high-frequency applications, making it indispensable across modern electronics manufacturing. One of the primary factors driving the dominance of SiC is its widespread adoption of electric vehicles (EVs). SiC-based power modules offer higher energy efficiency and reduced system size, which are critical for extending EV battery life. Many automakers including BYD, XPeng, and NIO have integrated SiC inverters into their EV platforms, directly boosting demand for this material. Another key driver is the expansion of renewable energy infrastructure, particularly solar power inverters. Countries like Japan and South Korea are investing heavily in smart grids and energy storage systems that rely on SiC components for better electrical conversion efficiency. The International Renewable Energy Agency (IRENA) reported that Asia Pacific contributed majorly to global solar capacity additions in 2023, reinforcing the growth trajectory of SiC-based semiconductors. Moreover, leading manufacturers such as ROHM Semiconductor and Mitsubishi Electric have ramped up SiC wafer production in APAC facilities to meet growing demand from the industrial and automotive sectors.

Molybdenum Disulfide (MoS₂) is the fastest-growing material segment in the Asia Pacific semiconductor materials market, projected to expand at a CAGR of 18.7%. This rapid surge is primarily attributed to MoS₂’s emerging role in next-generation nanoelectronics and flexible electronics, where conventional silicon-based materials struggle to perform efficiently. One major driver is the surge in research and development activities related to 2D materials for transistor design and optoelectronic devices. MoS₂ exhibits excellent electron mobility and can be fabricated into ultrathin layers, making it ideal for use in field-effect transistors (FETs) and photodetectors. Besides, the flexible display and wearable electronics industry in APAC has created new opportunities for MoS₂ integration. South Korean companies such as Samsung Display and LG Display are experimenting with this material for ultra-thin, bendable screens used in smartphones and AR/VR headsets. In 2023, Samsung filed three new patents related to MoS₂-based display technologies, signaling strong commercial interest. Governments in the region are also funding advanced materials research.

By Application Insights

The fabrication application segment dominated the Asia Pacific semiconductor materials market by capturing 62.5% of the total market share in 2024. This dominance is because semiconductor fabrication involves a complex and resource-intensive process requiring a vast array of raw materials from silicon wafers and chemical etchants to photoresists and deposition precursors. One of the key drivers behind this segment's leadership is the massive expansion of semiconductor fabrication plants (fabs) in China, India, and Southeast Asia. Each of these fabs requires continuous procurement of ultra-pure silicon, copper interconnect materials, and polishing slurries to maintain high-volume production. In addition, South Korea and Taiwan remain global leaders in advanced node manufacturing, particularly in memory chips and foundry services. TSMC invested a substantial amount in capital expenditures in 2023, much of which was directed toward securing next-generation materials needed for 3nm and 2nm processes. These include extreme ultraviolet (EUV) resists and cobalt alloys, both of which are integral to maintaining yield rates and performance standards. Furthermore, Japanese companies such as Shin-Etsu Chemical and JSR Corporation continue to supply the world's photoresist chemicals, which are essential during photolithography steps in chipmaking.

The packaging application segment is gaining momentum in the Asia Pacific semiconductor materials market and is expected to grow at the highest CAGR of 11.3%. This acceleration is driven by the increasing complexity of semiconductor packaging techniques, particularly in response to advancements in AI, high-performance computing (HPC), and 5G telecommunications. Advanced packaging methods such as fan-out wafer-level packaging (FOWLP), 2.5D packaging, and system-in-package (SiP) require a new class of materials beyond those used in traditional wire bonding. A major contributing factor is the widespread adoption of co-packaged optics (CPO) and chipsets, which are being deployed in data centers and cloud infrastructure. Companies like NVIDIA and AMD are increasingly relying on multi-die packaging solutions, which in turn drive demand for underfill materials, thermal interface materials (TIMs), and redistribution layer (RDL) polymers. According to TechInsights, in 2023, over 60% of high-end processors shipped globally utilized some form of chipset architecture, most of them manufactured in APAC-based foundries. In addition, governments in countries like Malaysia and Thailand are positioning themselves as secondary hubs for semiconductor assembly, testing, and packaging (ATMP), offering tax incentives and infrastructure support.

By End Use Industry Insights

The consumer electronics sector held the largest share of the Asia Pacific semiconductor materials market accounting for 39% in 2024. This control over the market is mainly due to the region’s status as the global epicenter of consumer electronics manufacturing, encompassing smartphones, laptops, tablets, wearables, and home appliances. Each of these devices contains multiple semiconductor components, from logic chips and memory modules to image sensors and power management units—all requiring significant volumes of silicon wafers, gallium arsenide substrates, and chemical mechanical planarization (CMP) slurries. Another key driver is the proliferation of IoT-enabled devices, including smart home systems, connected wearables, and edge computing gadgets. Smart TVs, digital cameras, and gaming consoles further contribute to sustained demand for high-purity electronic materials. Besides, governments in the region are promoting indigenous chipset development programs, especially in India and China, to reduce reliance on foreign suppliers.

The automotive industry is the fastest-growing end-use segment in the Asia Pacific semiconductor materials market, projected to expand at a CAGR of 14.8%. This surge is closely linked to the electrification of transport, autonomous driving technologies, and the integration of infotainment and connectivity systems in modern vehicles. One of the primary catalysts is the rapid adoption of electric vehicles (EVs) in the region, particularly in China. Unlike internal combustion engine vehicles, EVs incorporate two to five times more semiconductor content, including silicon carbide (SiC) and gallium nitride (GaN) power devices, which enhance battery efficiency and charging performance. Major automakers like BYD, Geely, and XPeng have transitioned to SiC-based inverters, significantly increasing demand for associated semiconductor materials. Another major growth vector is the deployment of advanced driver-assistance systems (ADAS) and vehicle-to-everything (V2X) communication modules. These features rely on radar, lidar, and vision processing chips, many of which utilize indium phosphide (InP) and compound semiconductor materials. According to McKinsey & Company, automotive semiconductor revenue in APAC is expected to surpass $35 billion by 2027, driven largely by ADAS and autonomous technology investments. In addition, Japanese and South Korean auto manufacturers are collaborating with semiconductor firms to co-develop custom chips tailored for electric and smart vehicles.

REGIONAL ANALYSIS

China commanded the largest share of the Asia Pacific semiconductor materials market by holding 32.4% in 2024. The country’s strategic investments in semiconductor self-sufficiency, coupled with its dominant position in electronics manufacturing, make it a critical player in the supply and consumption of semiconductor materials. The Chinese government has prioritized semiconductor independence through initiatives such as the "Made in China 2025" policy and the National Integrated Circuit Industry Investment Fund, which has injected over $40 billion into the sector since its inception. According to the Ministry of Industry and Information Technology (MIIT), China plans to increase its domestic chip production to 70% of domestic demand by 2025, necessitating a substantial increase in semiconductor material imports and local sourcing. This includes expansions by SMIC, YMTC, and Huahong Semiconductor, all of whom are heavily reliant on imported silicon wafers, photoresists, and CMP slurries. Moreover, China is the world’s largest producer of electric vehicles, with over 9 million EVs sold in 2023, many of which use silicon carbide (SiC) and gallium nitride (GaN) components. Companies like BYD and Gotion High-Tech are working closely with material suppliers to ensure a stable supply chain for wide bandgap semiconductors.

Japan occupies a strategic position in the Asia Pacific semiconductor materials market. Known for its leadership in high-purity semiconductor chemicals and precision materials, Japan plays a critical role in supplying essential inputs for global semiconductor manufacturing. Key Japanese companies such as JSR Corporation, Shin-Etsu Chemical, and Tokyo Ohka Kogyo dominate the production of photoresists, spin-on-glass materials, and CMP slurries, which are indispensable in advanced lithography and polishing processes. In addition, Japan continues to advance its capabilities in silicon wafer production, with companies like SUMCO and Siltronic AG (with joint ventures in Japan) supplying a major share of the world’s 300mm silicon wafers required for leading-edge chip manufacturing. Furthermore, the Japanese government has launched the "Semiconductor Strategy for the New Era", allocating ¥1.2 trillion (~$8.4 billion) to strengthen domestic supply chains. This includes partnerships with U.S. and European semiconductor firms to secure access to front-line materials and advanced packaging solutions.

South Korea is home to global giants like Samsung Electronics and SK Hynix, the country is a powerhouse in memory chip production, which drives massive demand for high-purity silicon, noble gases, and advanced interconnect materials. Samsung and SK Hynix together account for a key share of global DRAM and NAND flash memory production. Their combined investments in next-generation memory technologies—including DDR5, GDDR7, and 3D NAND —require cutting-edge materials such as cobalt, ruthenium, and atomic-layer deposition (ALD) precursors. The Korean government has also played a proactive role in bolstering the semiconductor supply chain. This initiative includes support for startups developing high-k dielectrics, EUV-compatible resists, and specialized gases. Also, South Korea is emerging as a leader in chipset integration and hybrid bonding technologies, which require novel underfill materials and redistribution layer (RDL) polymers.

India is emerging as a noteworthy participant in the Asia Pacific semiconductor materials market. This growth has been driven by the Indian government’s ambitious push to build a domestic semiconductor ecosystem, supported by financial incentives and infrastructure development. These developments are creating a new demand center for semiconductor materials, including silicon wafers, deposition chemicals, and cleaning agents. Moreover, India is witnessing a booming electronics manufacturing sector, with smartphone and EV production expanding rapidly. Domestic EV startups such as Ola Electric and Ather Energy are increasingly adopting power semiconductors, which in turn boosts demand for wide bandgap (WBG) materials like silicon carbide (SiC).

Taiwan holds a critical but compact share of the Asia Pacific semiconductor materials market. As the global leader in contract chip manufacturing, Taiwan serves as a linchpin in the semiconductor supply chain, hosting the world’s most advanced foundries such as TSMC, UMC, and PSMC, all of which consume vast quantities of high-performance materials. TSMC alone accounts for a major share of global foundry revenue and its continued investment in leading-edge technologies such as 3nm, 2nm, and gate-all-around (GAA) architectures has intensified demand for extreme ultraviolet (EUV) resists, cobalt alloys, and low-k dielectrics. In 2023, TSMC allocated over $30 billion toward capital expenditure, a significant portion of which was dedicated to securing next-generation materials from Japanese and U.S. suppliers. Beyond foundry operations, Taiwan is also a major hub for advanced packaging, particularly in the development of CoWoS and 2.5D packaging solutions for AI accelerators and high-performance graphics cards. The Industrial Technology Research Institute (ITRI) has also been instrumental in advancing local material development, focusing on carbon nanotube interconnects and quantum well structures for future chip designs. Government-backed initiatives aim to reduce dependency on external suppliers, encouraging domestic firms to participate in the semiconductor materials supply chain.

LEADING PLAYERS IN THE ASIA PACIFIC SEMICONDUCTOR MATERIALS MARKET

JSR Corporation (Japan)

JSR Corporation is a leading player in the semiconductor materials sector, particularly known for its advanced photoresist solutions used in photolithography. The company plays a vital role in supplying high-performance materials essential for manufacturing cutting-edge semiconductors. JSR’s continuous investment in R&D and strategic partnerships with global tech firms have solidified its position as a key supplier in the semiconductor supply chain. Its focus on innovation and quality ensures that it remains integral to both domestic and international semiconductor production.

Shin-Etsu Chemical Co., Ltd. (Japan)

Shin-Etsu Chemical is one of the world’s largest producers of silicon wafers, which form the foundation of most semiconductor devices. With an emphasis on ultra-pure materials and precision manufacturing, the company supplies critical substrates to major foundries and memory chip manufacturers globally. Shin-Etsu's dominance in the silicon wafer market makes it indispensable to the industry, supporting advancements in logic chips, DRAM, and NAND flash memory. Its long-standing expertise and forward-looking investments reinforce its leadership in semiconductor materials.

Sumitomo Metal Mining Co., Ltd. (Japan)

Sumitomo Metal Mining is a key supplier of copper and precious metals used in semiconductor interconnects and packaging. The company provides essential materials such as copper wire bonding and lead frames, enabling the miniaturization and performance enhancement of electronic components. Its vertically integrated operations ensure consistent quality and reliability, making it a preferred partner for semiconductor manufacturers across Asia and beyond. Sumitomo continues to innovate in response to evolving material demands from next-generation electronics.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies employed by leading companies in the Asia Pacific semiconductor materials market is aggressive investment in research and development. Firms are prioritizing innovation in material science to support emerging technologies like extreme ultraviolet (EUV) lithography, wide bandgap semiconductors, and advanced packaging techniques. By developing next-generation materials tailored for AI, IoT, and electric vehicles, companies aim to secure long-term contracts with major semiconductor manufacturers.

Another significant strategy is forming strategic partnerships and joint ventures with other industry players, academic institutions, and government bodies. These collaborations help accelerate technology transfer, reduce R&D risks, and enhance production capabilities. Companies are also engaging in co-development initiatives with equipment makers and end-users to align material innovations with fabrication process requirements.

Lastly, expanding manufacturing and supply chain infrastructure within the region has become a priority. With geopolitical uncertainties affecting global trade, semiconductor material suppliers are increasing local production capacities, especially in countries like Japan, South Korea, and India. This localization effort ensures greater resilience and responsiveness to regional demand fluctuations while reducing dependency on external sources.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the Asia Pacific Semiconductor materials market include Tokyo Ohka Kogyo Co., Ltd., DuPont de Nemours, Inc., BASF SE, Hitachi Chemical Co., Ltd., JSR Corporation, Shin-Etsu Chemical Co., Ltd., Sumitomo Chemical Co., Ltd., LG Chem Ltd., Samsung SDI Co., Ltd., Showa Denko K.K.

The competition in the Asia Pacific semiconductor materials market is characterized by intense technological rivalry, deep-rooted supplier relationships, and strategic positioning among global and regional players. Japanese companies hold a dominant presence due to their long-standing expertise in high-purity materials and precision manufacturing. However, South Korean and Chinese firms are rapidly catching up by leveraging state-backed incentives and expanding domestic production capabilities. The rise of indigenous semiconductor ecosystems in countries like India and Malaysia is also reshaping competitive dynamics, creating new opportunities for local and international material suppliers. As demand for specialized materials grows alongside advancements in chip design, companies are increasingly focusing on differentiation through innovation, vertical integration, and localized supply chains. The market is witnessing a shift toward collaboration as firms seek to align material development with emerging fabrication processes, ensuring compatibility and performance optimization. While established players continue to set industry benchmarks, smaller firms are entering niche segments, offering customized solutions for specific applications such as flexible electronics and quantum computing. This evolving landscape underscores the growing complexity and strategic importance of semiconductor materials in shaping the future of the global electronics industry.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, JSR Corporation announced a strategic partnership with ASML to develop next-generation EUV photoresists tailored for sub-3nm chip manufacturing. This collaboration aims to enhance lithography performance and yield rates, reinforcing JSR’s position as a critical supplier in the advanced semiconductor ecosystem.

- In May 2024, Shin-Etsu Chemical expanded its silicon wafer production facility in Yamagata, Japan, to meet rising demand from global foundries. This expansion supports the increased output of 300mm wafers required for high-performance computing and automotive semiconductor applications.

- In July 2024, Sumitomo Metal Mining entered into a joint venture with a South Korean materials firm to boost supply chain resilience for copper bonding wires and lead frames. This move strengthens Sumitomo’s footprint in the APAC region and ensures stable delivery of critical interconnect materials.

- In September 2024, SK Materials, a South Korean specialty gas supplier, acquired a Singapore-based semiconductor chemical company to broaden its portfolio and enhance its capability to serve the growing ASEAN semiconductor manufacturing base.

- In November 2024, Tokyo Ohka Kogyo (TOK) launched a new line of advanced CMP slurries designed specifically for gate-all-around (GAA) transistor architectures. This product launch positions TOK as a key enabler of next-generation logic chip manufacturing in the Asia Pacific region.

MARKET SEGMENTATION

This research report on the Asia Pacific semiconductor materials market has been segmented and sub-segmented based on material, application, end-user, and region.

By Material

- Silicon Carbide

- Molybdenum Disulfide (MoS₂)

By Application

- Fabrication

- Packaging

By End User

- Consumer Electronics

- Automotive

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What is driving the growth of the Asia Pacific semiconductor materials market?

The growth is driven by increasing demand for consumer electronics, rising adoption of advanced technologies like AI and IoT, and expanding semiconductor manufacturing capabilities in countries like China, Taiwan, South Korea, and Japan.

2. Who are the major consumers of semiconductor materials in the Asia Pacific region?

Major consumers include semiconductor foundries, integrated device manufacturers (IDMs), and electronics manufacturers operating in countries like Taiwan, South Korea, and China.

3. Which country holds the largest market share in the region?

Taiwan and South Korea lead the market due to their advanced semiconductor manufacturing ecosystems and the presence of global giants like TSMC and Samsung.

4. How is the market expected to evolve in the coming years?

The market is expected to witness significant growth due to increased R&D investments, technological advancements in chip production, and government initiatives supporting local manufacturing.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com