Asia Pacific Software Defined Network Market Size, Share, Growth, Trends, And Forecasts Research Report, Segmented By Component, Type, Application And By Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis From 2025 to 2033

Asia Pacific Software-Defined Network Market Size

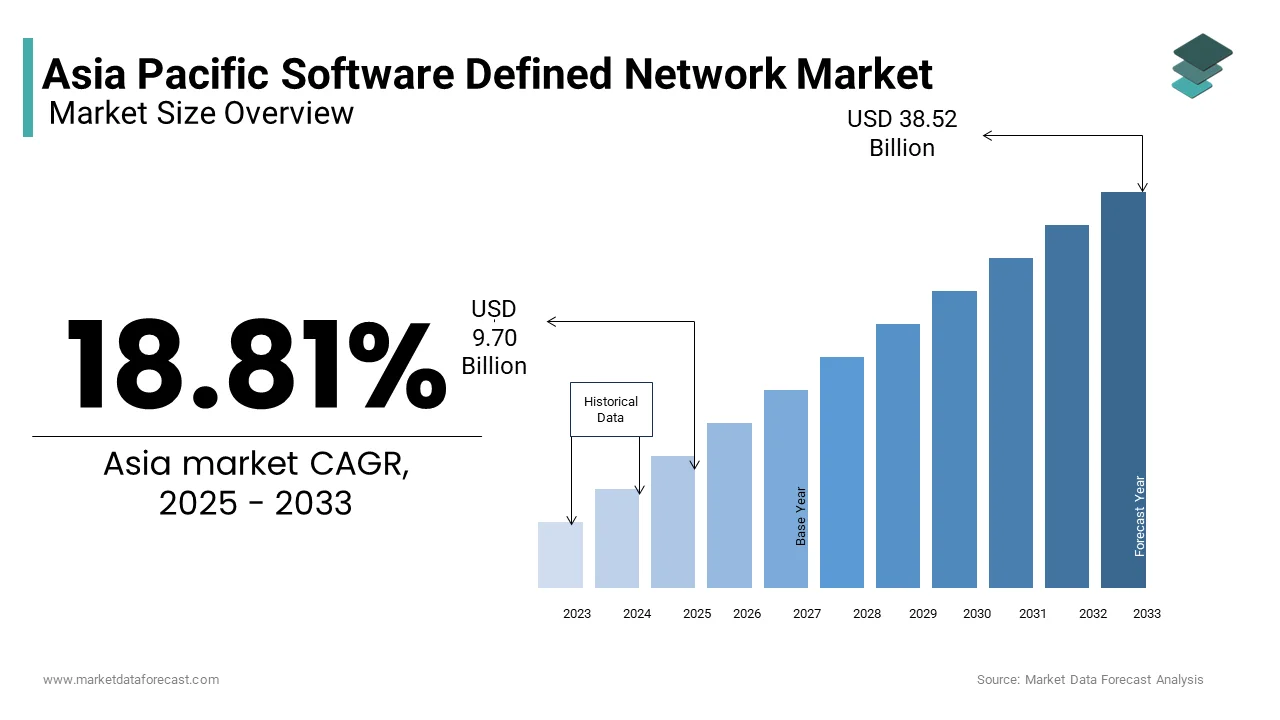

The Asia Pacific software-defined network market size was valued at USD 8.16 billion in 2025 and is anticipated to reach USD 9.70 billion in 2025 from USD 38.52 billion by 2033, growing at a CAGR of 18.81% during the forecast period from 2025 to 2033.

Software Defined Networking (SDN) in the Asia Pacific region refers to an advanced network architecture that decouples the control plane from the data plane, enabling centralized management and programmability of network resources. This model allows enterprises and service providers to dynamically manage network services through software-based automation, reducing dependency on proprietary hardware.

Also, the emergence of 5G deployment and edge computing is further pushing organizations to adopt SDN for better network orchestration. Moreover, the rise in remote work environments post-pandemic has intensified the requirement for secure and flexible networking models, reinforcing the relevance of SDN across both large enterprises and SMEs in the Asia Pacific.

MARKET DRIVERS

Surge in Digital Transformation Initiatives Across Enterprises

One of the primary drivers fueling the growth of the Asia Pacific software-defined networking market is the widespread push towards digital transformation across industries such as banking, healthcare, manufacturing, and retail. Organizations are increasingly adopting cloud-native architectures and virtualized infrastructures to streamline operations, enhance customer experiences, and improve business agility. As per a report by McKinsey, over 60% of enterprises in the Asia Pacific region have initiated or scaled their digital transformation programs in the past three years, with SDN playing a critical role in enabling seamless integration of hybrid cloud environments. In particular, countries like Singapore and South Korea are leading the charge, where government-backed smart city projects require intelligent, scalable, and secure networking frameworks. Software-defined networking offers the flexibility required to support dynamic application delivery and real-time analytics, which are essential components of digitally transformed ecosystems. Furthermore, the growing reliance on AI-driven decision-making systems and big data analytics platforms necessitates a more agile and programmable network backbone.

Expansion of Data Centers and Cloud Infrastructure Investments

The second major driver of the Asia Pacific software-defined networking market is the rapid expansion of data centers and the significant investments being made in cloud infrastructure development. With the exponential growth in data generation and consumption, companies across the region are scaling up their data center capacities to support cloud services, AI/ML models, and IoT deployments. Similarly, India has witnessed a surge in data center investments, fueled by domestic cloud service providers and international firms establishing regional hubs. Software-defined networking plays a crucial role in these data centers by simplifying network orchestration, improving interconnectivity between virtual machines, and enhancing security through policy-based automation. The integration of SDN with emerging technologies like containerization and Kubernetes also enables efficient workload management across distributed architectures.

MARKET RESTRAINTS

Lack of Skilled Professionals and Technical Expertise

A major restraint hindering the full potential of the Asia Pacific software-defined networking market is the acute shortage of skilled professionals who can effectively deploy, manage, and maintain SDN-based infrastructures. Unlike traditional networking paradigms that rely heavily on hardware configurations, SDN requires deep expertise in programming, automation, and integration with DevOps practices. Countries like Vietnam, Indonesia, and the Philippines face particular challenges due to limited access to structured training programs and certification courses focused on SDN. In addition, many enterprises hesitate to transition from legacy systems because of the steep learning curve associated with managing programmable networks. As per a whitepaper by ISACA, this skills gap leads not only to delayed implementation but also increases the risk of misconfigurations and security vulnerabilities. Educational institutions and industry bodies in the region are beginning to address this issue through collaborative initiatives; however, progress remains slow compared to the pace of technological advancement.

Interoperability Challenges Across Vendors and Legacy Systems

Another significant challenge impeding the growth of the Asia Pacific software-defined networking market is the lack of standardization and interoperability between different vendor platforms and existing legacy network infrastructures. SDN solutions often come with proprietary APIs and control mechanisms that make it difficult for enterprises to integrate them seamlessly into heterogeneous environments. This fragmentation is particularly problematic for organizations transitioning from traditional networking models to more open and programmable architectures. In countries like Thailand and Malaysia, where enterprises rely on a mix of global and local vendors, the absence of unified standards poses a serious barrier to scalability and performance optimization. Industry forums such as the Open Networking Foundation (ONF) are working toward establishing common frameworks, but widespread adoption remains inconsistent across the Asia Pacific.

MARKET OPPORTUNITY

Proliferation of Smart Cities and IoT-Based Urban Infrastructure

The rapid development of smart cities across the Asia Pacific region presents a substantial opportunity for the software-defined networking market. Governments in countries such as Japan, South Korea, and India are investing heavily in urban digitization initiatives aimed at improving public services, transportation, energy grids, and surveillance systems. These smart infrastructure projects rely extensively on interconnected IoT devices and real-time data processing, which demand highly flexible and scalable networking capabilities. Software-defined networking provides the ideal architectural framework for managing the vast volumes of data generated by sensors, cameras, and edge nodes deployed across these smart ecosystems. Its ability to dynamically allocate network resources and prioritize traffic flows ensures optimal performance and reliability in mission-critical applications such as emergency response systems and autonomous transport networks. Moreover, SDN supports secure, low-latency communication between edge computing nodes and central data centers, which is essential for maintaining uninterrupted services in densely populated urban areas.

Integration with Edge Computing and 5G Network Slicing

The evolution of 5G and the growing adoption of edge computing present another compelling opportunity for the Asia Pacific software-defined networking market. As mobile operators roll out 5G networks across countries like Australia, Singapore, and South Korea, they are increasingly relying on SDN to enable network slicing—a technique that allows the creation of multiple virtual networks tailored to specific use cases. According to GSMA Intelligence, by early 2024, over 30 mobile network operators in the Asia Pacific had launched commercial 5G services, many of which depend on SDN for dynamic service provisioning and traffic prioritization. The combination of SDN with edge computing enhances the ability to process data closer to end-users, significantly reducing latency and improving application responsiveness. This is particularly vital for applications such as industrial automation, augmented reality, and real-time analytics, which require instantaneous data handling. As per Tech Mahindra, enterprises deploying edge-SDN architectures have seen up to a 60% reduction in network downtime and improved resource utilization. Furthermore, governments in the region are promoting indigenous development of edge infrastructure, thereby encouraging telecom firms and cloud providers to invest in SDN-integrated 5G solutions.

MARKET CHALLENGE

Cybersecurity Vulnerabilities in Centralized Control Architectures

One of the foremost challenges confronting the Asia Pacific software-defined networking market is the heightened risk of cybersecurity threats due to the centralized nature of SDN control architectures. Unlike traditional decentralized networks, where breaches are typically isolated, SDN introduces a single point of failure—the controller—making it an attractive target for cyberattacks. Countries such as India and the Philippines, which are rapidly expanding their digital infrastructure, are particularly vulnerable due to insufficient cybersecurity frameworks and outdated compliance measures. The open-source nature of certain SDN implementations also exposes networks to potential vulnerabilities if not properly monitored and updated.

Regulatory and Policy Uncertainties Across Geographies

Regulatory inconsistencies and evolving policy landscapes across the Asia Pacific region present a formidable challenge for the software-defined networking market. Each country has its own set of data protection laws, network governance policies, and cybersecurity mandates, making it difficult for multinational enterprises and service providers to establish uniform SDN frameworks. According to a policy analysis by the Economic Research Institute for ASEAN and East Asia, disparate regulatory approaches across Southeast Asia have led to fragmented compliance requirements, slowing down SDN implementations in cross-border data environments. In China, stringent regulations surrounding data localization and foreign technology usage create additional barriers for global SDN vendors seeking market entry. Similarly, in India, recent amendments to the Information Technology Act have introduced stricter norms for data storage and processing, affecting how enterprises configure their SDN architectures.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 23.95% |

| Segments Covered | By Product, Application, and Region. |

|

Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Arista Networks, Inc., Cisco Systems, Inc., Ciena Corporation, Dell Inc., LM Ericsson, Extreme Networks, Fortinet, Inc., Hewlett Packard Enterprise Development LP, Huawei Technologies Co., Ltd., IBM, Juniper Networks, Inc., Nokia, Palo Alto Networks, Broadcom. |

SEGMENTAL ANALYSIS

By Component Insights

The solutions segment held the largest share of the Asia Pacific software-defined networking market by accounting for 65% in 2024. This dominance is primarily attributed to the increasing deployment of SDN controllers, virtual switches, and automation tools by enterprises and telecom providers seeking enhanced network agility and performance. In particular, financial institutions and cloud service providers are adopting SDN solutions at a rapid pace to support hybrid cloud environments and improve security postures. As noted by Gartner, organizations that have deployed SDN-based infrastructure report up to a 45% reduction in network provisioning time, significantly improving operational efficiency. Moreover, advancements in AI-driven analytics integrated within SDN platforms are enabling real-time traffic optimization and policy enforcement, further driving adoption. In addition, government-led smart city projects in India and Southeast Asia require scalable and programmable networks, which are best addressed through comprehensive SDN solution deployments.

The services segment is projected to grow at the fastest rate, registering a CAGR exceeding 18% over the next five years. This growth is driven by increasing demand for professional services such as consulting, system integration, and managed network services. Enterprises lacking internal expertise often rely on external vendors to design and implement SDN architectures effectively. Furthermore, the complexities involved in migrating from legacy systems to open-source SDN platforms necessitate expert guidance and ongoing support. Telecom operators in Australia and Singapore are also outsourcing SDN implementation to specialized service providers to ensure seamless integration with 5G and fiber-optic networks.

By Type Insights

The hybrid SDN dominated the Asia Pacific software-defined networking market by capturing 40.7% of the total revenue share in 2024. This model combines elements of OpenFlow-based control with traditional networking protocols, allowing enterprises to gradually transition toward full SDN adoption without disrupting existing operations. The banking sector, in particular, is increasingly deploying hybrid models to balance regulatory compliance with modernization needs. Additionally, telecommunications providers in Australia and India are leveraging this architecture to manage heterogeneous networks composed of both proprietary and open-source components. A whitepaper from Cisco highlights that Hybrid SDN allows for better traffic prioritization and resource allocation, making it ideal for high-traffic environments like data centers and mobile backhaul networks. Gartner emphasizes that interoperability and vendor neutrality are central to the sustained growth of this segment in the Asia Pacific market.

SDN via Overlay is emerging as the fastest-growing type segment, expected to expand at a CAGR of over 20% during the forecast period. This approach enables logical network abstraction over existing physical infrastructures, providing enterprises with greater flexibility and simplified management. Companies in the logistics and e-commerce industries in Vietnam and the Philippines are increasingly leveraging overlay technologies to support multi-cloud strategies and remote branch connectivity. According to VMware's annual cloud networking survey, a large share of enterprises in the Asia Pacific prefer overlay SDN for WAN optimization and secure application delivery. The rise of distributed workforces and edge computing use cases is further fueling interest in overlay-based virtual networks. Also, the ability to decouple network services from hardware makes overlay SDN an attractive option for organizations undergoing digital transformation.

By Application Vertical Insights

The enterprise segment led the Asia Pacific software-defined networking market in terms of revenue contribution by capturing 45.3% of the overall market in 2024. This dominance is driven by the widespread adoption of SDN solutions across large corporations in finance, manufacturing, healthcare, and retail. Banking institutions, in particular, are leveraging SDN to enhance network security and automate compliance workflows. In addition, multinational corporations are using SDN to manage global branch offices and optimize WAN performance. As noted by Gartner, the increasing reliance on artificial intelligence and machine learning applications requires agile and programmable network capabilities that SDN delivers effectively. Educational institutions and government bodies are also adopting SDN to facilitate secure and scalable digital campuses.

The telecom service providers segment is anticipated to register the highest growth rate, expanding at a CAGR surpassing 19% through 2030. This rapid expansion is fueled by the rollout of 5G networks and the need for flexible, high-performance infrastructure capable of supporting new services such as ultra-low latency applications and network slicing. In Japan and South Korea, telecom giants are utilizing SDN to streamline core network functions and reduce operational costs associated with legacy infrastructure. Moreover, the increasing deployment of fiber-based broadband and the evolution of Open RAN (Radio Access Network) architectures are further accelerating SDN adoption among telecom operators.

COUNTRY LEVEL ANALYSIS

China Software-defined Networking Market Analysis

China maintained a dominant position in the Asia Pacific software-defined networking market by accounting for 30.7% of the regional revenue share in 2024. The country's extensive investments in digital infrastructure, 5G rollout, and smart city initiatives are primary catalysts for SDN adoption. Major domestic technology firms such as Huawei, Alibaba Cloud, and Tencent are actively developing and deploying SDN solutions to support national data center expansion and cloud migration efforts. Besides, the manufacturing sector is embracing SDN to integrate industrial IoT and AI-driven analytics into production ecosystems.

India Software-Defined Networking Market Analysis

India holds a prominent place in the Asia-Pacific software-defined networking market. The country’s rapid digital transformation, coupled with aggressive government-led initiatives such as "Digital India" and "Smart Cities Mission," has created fertile ground for SDN adoption. The proliferation of hyperscale data centers operated by global and local cloud providers further amplifies the demand for programmable networking solutions. Telecommunications operators such as Bharti Airtel and Jio Infocomm are also leveraging SDN to support their 5G network launches and deliver next-generation services.

Japan Software-defined Networking Market Analysis

Japan occupies a strong presence in the Asia Pacific software-defined networking market. Known for its technological sophistication and early adoption of advanced networking solutions, Japan is leveraging SDN to support its Smart City and Industry 4.0 initiatives. According to the Ministry of Internal Affairs and Communications, the Japanese government has allocated substantial funding for next-generation communication infrastructure, including 5G and SDN-based automation frameworks. Financial institutions and automotive manufacturers are among the earliest adopters of SDN in the country, reflecting a broader trend toward digitizing mission-critical operations. Besides, telecom operators like NTT DOCOMO and SoftBank are integrating SDN with AI-driven analytics to optimize mobile network performance and support edge computing applications.

South Korea Software-defined Networking Market Analysis

South Korea commands a notable share and is driven by its world-leading 5G infrastructure and digital-first economic policies. According to the Ministry of Science and ICT, South Korea was the first country to commercially deploy standalone 5G services, leveraging SDN extensively for dynamic network slicing and intelligent traffic management.

Singapore Software-defined Networking Market Analysis

Singapore secures a significant share, owing to its status as a global financial and digital innovation hub. The country’s proactive Smart Nation initiative has fostered widespread adoption of SDN across financial services, logistics, and government sectors. According to the Infocomm Media Development Authority (IMDA), Singapore ranks among the top nations in the world for ease of doing business in the digital economy, attracting multinational corporations to establish regional headquarters equipped with SDN-based infrastructure. Apart from these, the proliferation of interlinked data centers across ASEAN makes Singapore a preferred location for deploying centralized SDN orchestrations.

COMPETITIVE LANDSCAPE

The Asia Pacific software-defined networking market is characterized by intense competition driven by rapid technological advancements and growing demand for agile, scalable, and secure network infrastructures. A mix of global technology giants and emerging regional players actively shape the market, each striving to offer differentiated SDN solutions tailored to enterprise, telecom, and cloud provider needs. While multinational firms leverage their established brand reputation and global expertise, domestic vendors capitalize on their deep understanding of regional regulatory landscapes and customer preferences. The rise of open-source SDN initiatives and hybrid deployment models further intensifies the competitive environment, pushing companies to innovate continuously. Additionally, the convergence of SDN with adjacent technologies such as artificial intelligence, 5G, and edge computing has expanded the battlefield, compelling players to invest heavily in integration capabilities and strategic alliances.

KEY MARKET PLAYERS

These are the market players that are dominating the Asia Pacific software defined networking market, including

- Arista Networks, Inc.

- Cisco Systems, Inc.

- Ciena Corporation

- Dell Inc.

- LM Ericsson

- Extreme Networks

- Fortinet, Inc.

- Hewlett Packard Enterprise Development LP

- Huawei Technologies Co., Ltd.

- IBM

- Juniper Networks, Inc.

- Nokia

- Palo Alto Networks

- Broadcom.

Top Players In the Market

- Cisco is a dominant force in the Asia Pacific software-defined networking market, known for its comprehensive SDN solutions such as Application Centric Infrastructure (ACI) and DNA Center. The company plays a pivotal role in shaping global SDN standards while offering scalable and secure network automation tools tailored to enterprise and telecom needs. Cisco's strong R&D focus and strategic collaborations with regional partners have significantly influenced the adoption of open and hybrid SDN models across the Asia Pacific.

- Huawei has emerged as a key player in the Asia Pacific SDN landscape by providing end-to-end software-defined networking solutions that integrate seamlessly with cloud computing and 5G infrastructure. Its Agile Campus and CloudFabric platforms are widely deployed across enterprises and telecom operators in China and beyond. Huawei’s emphasis on indigenous innovation and support for government digitalization programs has made it an influential contributor to the region’s SDN evolution and global export of networking technologies.

- HPE Aruba is recognized for its adaptive edge-to-cloud SDN strategies, particularly in enterprise environments. The company contributes to the Asia Pacific market through intelligent campus networks, secure Wi-Fi 6 integrations, and AI-driven analytics. HPE Aruba’s partnerships with local service providers and cloud vendors have enhanced its regional presence, making it a preferred choice for organizations transitioning to modern, flexible network architectures.

Top Strategies Used by Key Market Participants

Key players in the Asia Pacific software-defined networking market primarily rely on strategic partnerships and ecosystem collaborations to strengthen their market position. By aligning with regional telecom providers, cloud service companies, and system integrators, vendors can deliver more integrated and localized SDN offerings. These partnerships also enable better interoperability with existing infrastructure, facilitating smoother transitions for enterprises moving away from legacy systems.

Another crucial strategy involves continuous investment in research and development to drive innovation in SDN architecture. Companies are focusing on developing AI-powered orchestration tools, intent-based networking frameworks, and advanced security features tailored to the evolving digital demands of the region. This not only enhances product differentiation but also addresses emerging challenges like network complexity and cybersecurity threats.

Lastly, localized product adaptation and go-to-market strategies play a vital role in capturing diverse market segments across the Asia Pacific. Vendors are customizing their SDN solutions to meet specific regulatory requirements, business sizes, and industry verticals, ensuring higher adoption rates and stronger customer engagement throughout the region.

RECENT MARKET NEWS

- In February 2024, Cisco expanded its collaboration with SoftBank in Japan to enhance SDN integration within 5G networks. This partnership aimed at improving dynamic network slicing and automated service provisioning, reinforcing Cisco’s leadership in carrier-grade SDN solutions across the Asia Pacific.

- In May 2024, Huawei launched a new SDN-enabled cloud data center in Bangkok, Thailand, designed to support local enterprises and public sector institutions. This initiative was part of Huawei’s broader push to expand its hybrid cloud and networking footprint across Southeast Asia, offering scalable and secure digital infrastructure solutions.

- In July 2024, HPE Aruba introduced a new AI-driven SD-WAN solution tailored for mid-sized enterprises in India and Indonesia. The move was intended to help businesses transition smoothly to distributed IT models while maintaining high levels of performance and security without significant capital outlays.

- In October 2024, Juniper Networks partnered with NTT Communications in Australia to co-develop enterprise SDN services that integrate with multi-cloud environments. This alliance focused on delivering intelligent networking solutions optimized for hybrid work and real-time application delivery in the Asia Pacific region.

- In December 2024, VMware announced a joint venture with LG Uplus in South Korea to deploy next-generation SDN solutions for the smart manufacturing and logistics sectors. This initiative aimed to accelerate Industry 4.0 transformations by enabling highly responsive and programmable network infrastructures tailored to mission-critical applications.

MARKET SEGMENTATION

This research report on the Asia Pacific software-defined networking market is segmented and sub-segmented into the following categories.

By Component

- Solutions

- Physical Network Infrastructure

- Virtualization/Control Software

- SDN Application

- SDN Controllers

- Services

- Consulting

- Integration and Deployment

- Training and Maintenance

- Managed Services

By Type

- Open SDN

- SDN via API

- SDN via Overlay

- Hybrid SDN

By End-use

- Enterprise

- Telecommunication Service Providers

- Cloud Services Providers

- Managed Service Providers

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is SDN, and why is adoption accelerating across APAC?

Software-Defined Networking decouples the network control plane from the data plane, enabling centralized, programmable, and automated network management. In APAC, digital transformation, cloud migration, and 5G rollout are driving enterprises and telcos to adopt SDN for agility, scalability, and cost efficiency.

Which countries lead SDN deployment in the region?

Japan, South Korea, Australia, and Singapore are frontrunners—thanks to mature IT infrastructure, government smart-city initiatives (e.g., Singapore’s Smart Nation), and early 5G commercialization. China and India follow rapidly, fueled by hyperscaler data center expansion and private 5G pilots.

What industries are adopting SDN most aggressively?

Telecom operators (for network slicing and NFV), cloud & data center providers (for dynamic resource allocation), BFSI (for secure, low-latency trading networks), and manufacturing (Industry 4.0/IIoT integration) lead enterprise adoption.

How is 5G enabling SDN growth?

5G’s network slicing and ultra-low latency requirements rely on SDN/NFV architectures—making SDN foundational for CSPs deploying standalone (SA) 5G cores. Operators like SK Telecom, NTT Docomo, and Reliance Jio are integrating SDN at the RAN and core layers.

Are hybrid and multi-cloud strategies boosting demand?

Yes—enterprises managing workloads across AWS, Azure, Google Cloud, and local providers (e.g., Alibaba Cloud, Oracle Cloud in India) use SDN-based WAN (SD-WAN) and cloud interconnect solutions to ensure seamless, policy-driven traffic orchestration.

Who are the key players in the APAC SDN ecosystem?

Global vendors: Cisco, VMware (now Broadcom), Juniper Networks, NVIDIA (Cumulus, Mellanox); Regional leaders: Huawei, ZTE, NEC, Fujitsu, and cloud-native specialists like Cato Networks and Versa Networks—many offering localized support and compliance (e.g., China’s MLPS, India’s CERT-In).

How is security being integrated into SDN architectures?

Zero Trust frameworks and SASE (Secure Access Service Edge) are converging with SDN—enabling context-aware, micro-segmented security policies enforced across hybrid networks, with real-time threat response via API-driven orchestration.

What challenges hinder widespread SDN adoption?

Legacy infrastructure lock-in, skills gaps in network automation (e.g., Python, Ansible, Terraform), interoperability issues across multi-vendor environments, and regulatory concerns over centralized control in critical infrastructure remain key barriers.

How is open-source influencing the market?

Projects like ONOS, OpenDaylight, and SONiC (supported by Alibaba, Tencent, NTT) are gaining traction—especially among hyperscalers and telecoms seeking vendor-agnostic, customizable control planes and reduced licensing costs.

What’s the market outlook for 2025–2030?

The APAC SDN market is projected to grow at a strong CAGR—driven by AI/ML-driven network automation, edge computing expansion, and national digital backbone initiatives—making SDN the nervous system of next-generation intelligent infrastructure across the region.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com