Asia Pacific Software Market Research Report – Segmented By Type (Application Software, System Infrastructure Software, Productivity Software ) Deployment, Vertical and Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis on Size, Share, Trends& Growth Forecast from 2025 to 2033

Asia Pacific Software Market Size

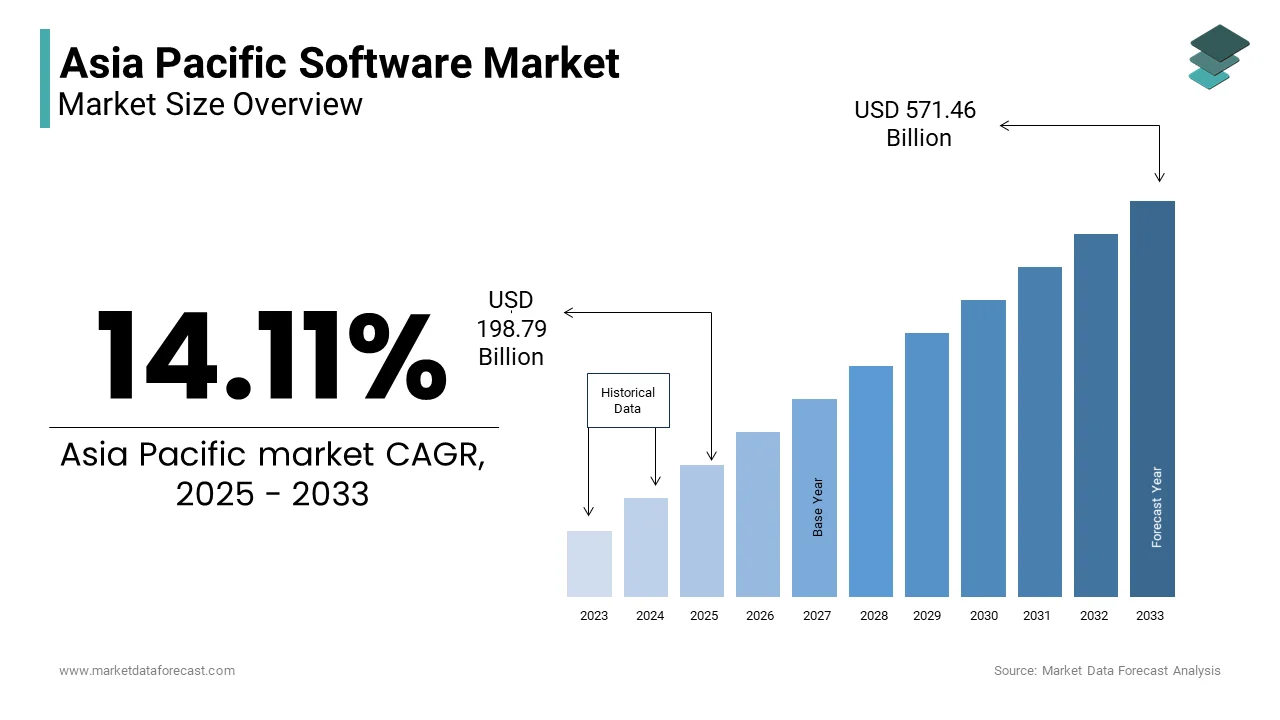

The Asia Pacific Software Market Size was valued at USD 174.21 billion in 2024. The Asia Pacific Software Market Size is expected to have 14.11 % CAGR from 2025 to 2033 and be worth USD 571.46 billion by 2033 from USD 198.79 billion in 2025.

The Asia Pacific software market growth is driven by rapid technological adoption and increasing investments in IT infrastructure. This expansion is fueled by the growing demand for enterprise software solutions, cloud computing, and artificial intelligence (AI) applications. Countries like China, India, Japan, and Australia are leading adopters, which is leveraging software innovations to enhance productivity and operational efficiency. Additionally, government initiatives promoting digitalization, such as India’s “Digital India” campaign, have accelerated software adoption.

MARKET DRIVERS

Rising Adoption of Cloud Computing and SaaS Solutions

The widespread adoption of cloud computing and Software-as-a-Service (SaaS) solutions is a primary driver of the Asia Pacific software market. For instance, in Japan, over 70% of enterprises have migrated their operations to cloud platforms by enabling scalability and reducing hardware costs. A key factor fueling this growth is the flexibility offered by cloud-based solutions, which allow businesses to access software remotely and scale resources as needed. According to the data from Accenture, companies using cloud-enabled software reported a 30% reduction in operational costs due to improved efficiency and accessibility. Additionally, the integration of AI and machine learning into cloud platforms has enhanced system capabilities, which is enabling predictive analytics and real-time decision-making. These innovations ensure that cloud computing remains a dominant force driving software adoption in the region.

Increasing Demand for Enterprise Resource Planning (ERP) Systems

The rising demand for Enterprise Resource Planning (ERP) systems is another significant driver of the Asia Pacific software market. According to Deloitte, ERP adoption rates among large enterprises in the region increased by 40% annually between 2020 and 2022, with industries like manufacturing and finance leading the way. For example, in China, over 60% of manufacturing facilities utilize ERP systems to streamline supply chain management and improve operational efficiency. Another factor is the integration of IoT and AI technologies into ERP platforms by enhancing data analytics and process automation. Data from McKinsey reveals that companies using AI-driven ERP systems reported a 25% increase in productivity and a 20% reduction in resource wastage. Additionally, partnerships between ERP providers and local firms have streamlined implementation, attracting small and medium enterprises. These trends position ERP systems as a critical enabler of business growth and digital transformation in the region.

MARKET RESTRAINTS

Cybersecurity Threats and Vulnerabilities

Cybersecurity threats pose a significant restraint to the Asia Pacific software market as businesses increasingly rely on interconnected systems and cloud platforms. According to Symantec, cyberattacks targeting software systems increased by 35% in 2022, with ransomware and phishing scams being prevalent threats. For instance, a major breach in Australia exposed vulnerabilities in a financial institution’s ERP system by compromising sensitive customer data and disrupting operations. Additionally, the lack of standardized security protocols across industries exacerbates the issue, which is leaving many systems exposed to potential breaches.

High Implementation Costs for SMEs

High implementation costs remain a critical barrier for small and medium enterprises (SMEs) in emerging markets like Vietnam and Indonesia. As per a study by Ernst & Young, less than 30% of SMEs in these regions can afford full-scale software implementations, which is forcing them to rely on manual processes or outdated technologies. Furthermore, maintenance and upgrade expenses further exacerbate the issue, with annual costs accounting for 15-20% of the initial investment. These financial constraints not only restrict market penetration but also necessitate the development of cost-effective solutions tailored to the needs of price-sensitive consumers.

MARKET OPPORTUNITIES

Expansion into Emerging Markets

Emerging markets such as India, Indonesia, and Vietnam present significant opportunities for the Asia Pacific software market. The rise of affordable cloud-based platforms tailored to local needs has begun to bridge this gap by enabling wider adoption. For instance, in 2022, Microsoft launched a low-cost SaaS platform in India, specifically designed for small-scale agricultural operations, which is resulting in a 30% increase in productivity, as per the Indian Ministry of Agriculture. Additionally, government initiatives promoting rural digitalization have indirectly boosted demand for software solutions.

Integration of AI and Automation Technologies

The integration of artificial intelligence (AI) and automation technologies offers transformative opportunities for the Asia Pacific software market. For example, in South Korea, Samsung Electronics adopted AI-enabled software in its semiconductor manufacturing plants, reducing equipment downtime by 40%, as reported by McKinsey. Automation technologies, powered by machine learning algorithms, allow businesses to streamline repetitive tasks and improve efficiency. Data from Accenture reveals that companies using AI-integrated software reported a 25% reduction in operational expenses. Additionally, partnerships with tech firms like Huawei have streamlined the deployment of AI-driven solutions, which is attracting industries seeking advanced capabilities. These innovations position AI and automation as key drivers of future growth in the software market.

MARKET CHALLENGES

Fragmented Regulatory Frameworks

Fragmented regulatory frameworks pose a significant challenge to the Asia Pacific software market by creating operational inefficiencies for multinational companies. Each country imposes unique compliance requirements for software systems, which is complicating efforts to standardize solutions. For instance, while Japan mandates stringent cybersecurity certifications for cloud-based platforms, countries like Thailand have minimal regulations by leading to inconsistencies in system standards. These disparities increase administrative burdens and costs is hindering scalability. Such complexities necessitate significant investments in regulatory expertise by straining resources for smaller players and limiting market entry for new entrants.

Limited Skilled Workforce in Rural Areas

Limited availability of skilled professionals remains a critical challenge in rural and underdeveloped regions. According to the World Economic Forum, over 50% of Asia Pacific countries face a shortage of trained personnel capable of implementing and maintaining advanced software systems. Additionally, the lack of technical education programs exacerbates the issue, which is leaving many operators reliant on external consultants, which increases costs. Addressing these gaps requires substantial investments in training and capacity-building by posing a daunting task for both governments and private players.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 14.11% |

| Segments Covered | By Type , Deployment, Vertical and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | China, India, Japan, South Korea, Australia, New Zealand, Thailand, Indonesia, Philippines, Vietnam, Singapore, Rest of APAC. |

| Market Leader Profiled | International Business Machines Corp, McAfee, Microsoft Corp, SAP SE. |

SEGMENTAL ANALYSIS

By Type Insights

The application software segment was accounted in holding 50.4% of the Asia Pacific software market share in 2024 with the growing demand for industry-specific solutions, such as customer relationship management (CRM), enterprise resource planning (ERP), and supply chain management (SCM) systems. A key factor fueling this growth is the integration of AI and machine learning into application software, which is enabling predictive analytics and automation. Additionally, government initiatives promoting digitalization, such as India’s “Digital India” campaign, have accelerated adoption rates. For instance, in China, manufacturing facilities utilize ERP systems to optimize supply chains that is reducing costs. These innovations ensure that application software remains the largest and most critical segment in the market.

The cloud-based system infrastructure software segment is likely to register a CAGR of 18.5% from 2025 to 2033. This rapid expansion is fueled by the increasing adoption of cloud platforms for scalability and cost efficiency. A study by Gartner reveals that over 70% of enterprises in the region have migrated their IT infrastructure to the cloud, which is reducing hardware costs by up to 40%. Another driving factor is the rise of hybrid cloud solutions, which combine on-premises and cloud environments to meet diverse business needs. For example, in Japan, financial institutions utilize cloud-based infrastructure software to enhance data security and improve compliance with regulatory standards.

By Deployment Insights

The on-premises segment was the largest and held 60.1% of the Asia Pacific software market share in 2024. This dominance is driven by the widespread preference for localized control and data security among large enterprises. According to Symantec, over 70% of organizations in sectors like banking and defense rely on on-premises solutions to protect sensitive information from cyber threats. A key factor is the high customization capabilities offered by on-premises software by enabling businesses to tailor solutions to their specific needs. Additionally, regulatory requirements in countries like Japan mandate stringent data localization policies that further boosts the growth of the segment.

The cloud deployment segment is lucratively to grow with a CAGR of 20.3% from 2025 to 2033. This growth is fueled by the increasing demand for scalable and cost-effective solutions among small and medium enterprises (SMEs). SMEs in the region prefer cloud-based software due to its flexibility and reduced upfront costs. Another driving factor is the integration of advanced technologies like AI and IoT into cloud platforms, that is enhancing system capabilities. For instance, in Australia, healthcare providers utilize cloud-based software to manage patient data securely, which is improving accessibility and compliance with privacy laws.

By Vertical Insights

The IT & telecom sector dominated the Asia Pacific software market by accounting for 45.3% of the share in 2024 owing to the sector’s heavy reliance on software solutions to manage complex networks, enhance connectivity, and ensure cybersecurity. According to the International Telecommunication Union, over 70% of telecom operators in the region utilize advanced software tools for network optimization and customer experience management. A key factor is the integration of 5G technology, which requires robust software systems to manage data traffic and enable real-time communication. Additionally, government investments in digital infrastructure, such as India’s 5G rollout, have accelerated software adoption in the sector.

The healthcare segment is likely to is the fastest-growing vertical in the Asia Pacific software market, with a CAGR of 19.8% from 2025 to 2033. This growth is fueled by the increasing adoption of electronic health records (EHR) and telemedicine platforms during the post-pandemic era. A study by Deloitte reveals that over 60% of healthcare providers in the region have integrated software solutions to improve patient care and operational efficiency. Another driving factor is the integration of AI and machine learning into healthcare software, which is enabling predictive diagnostics and personalized treatment plans. For instance, in Japan, healthcare facilities utilize cloud-based platforms to manage patient data securely by ensuring compliance with privacy regulations.

COUNTRY LEVEL ANALYSIS

China was the top performer in the Asia Pacific software market with 35.4% of share in 2024 with its massive industrial base and ambitious digitalization initiatives, particularly in sectors like manufacturing and finance. According to the Chinese Ministry of Industry and Information Technology, software spending exceeded $100 billion in 2022, with cloud-based solutions gaining significant traction. A key factor is the government’s push for technological innovation, as seen in initiatives like “Made in China 2025.

Japan’s advanced technological infrastructure and focus on precision engineering are majorly prompting the growth of the market. According to the Japanese Ministry of Economy, Trade, and Industry, software adoption rates among enterprises exceed 70%, with industries like automotive and electronics leading the way. A key factor is the integration of AI and IoT technologies, which enhance system capabilities and improve efficiency. Additionally, the rise of smart city projects has amplified demand for software solutions in urban infrastructure management.

According to the Indian Ministry of Electronics and Information Technology, software exports exceeded $150 billion in 2022, with IT services being a key contributor. A major factor is the “Digital India” campaign, which has spurred investments in cloud computing and AI-driven solutions. Another factor is the rise of startups leveraging software innovations to address local challenges. Data from NASSCOM highlights that over 60% of Indian startups utilize cloud-based platforms to scale operations and attract global clients.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the Asia Pacific Software Market are International Business Machines Corp, McAfee, Microsoft Corp, SAP SE, Oracle Corp, NortonLifeLock, Adobe Inc, VMware, Block Inc Class A, Intuit Inc.

The Asia Pacific software market is highly competitive owing to the presence of global giants like Microsoft Corporation and SAP SE, alongside regional players catering to local needs. Global firms leverage their technological expertise and extensive portfolios to attract large-scale clients, while local operators capitalize on cultural insights and affordability. This rivalry has spurred significant innovations, such as AI-driven analytics and cloud-enabled platforms. However, challenges like cybersecurity threats and high implementation costs persist, creating barriers for new entrants. Despite these hurdles, the dynamic landscape fosters continuous improvement, with companies investing heavily in partnerships, marketing, and R&D to differentiate themselves. Only the most agile and innovative players thrive in this evolving market.

Top Players in the Market

Microsoft Corporation

Microsoft Corporation is a dominant player in the Asia Pacific software market by offering a wide range of solutions, including cloud computing, productivity tools, and enterprise applications. In 2023, the company expanded its Azure cloud platform in India, which is enabling local businesses to leverage AI-driven analytics for operational efficiency. Additionally, Microsoft partnered with regional governments to promote digital literacy, fostering wider adoption of its software tools. The company’s focus on cybersecurity and compliance has strengthened its reputation among enterprises.

SAP SE

SAP SE plays a pivotal role in the Asia Pacific software market through its advanced enterprise resource planning (ERP) solutions tailored to industries like manufacturing and finance. In 2023, SAP launched a low-cost SaaS platform in Southeast Asia, targeting small and medium enterprises (SMEs) seeking scalable solutions. Furthermore, SAP collaborated with local firms to integrate AI and IoT into its ERP systems by enhancing predictive analytics capabilities.

Oracle Corporation

Oracle Corporation specializes in database management and cloud infrastructure, making it a preferred choice for data-driven enterprises in the Asia Pacific region. In 2023, Oracle introduced an AI-powered analytics platform in Japan, enabling businesses to streamline decision-making processes. Additionally, the company partnered with telecom operators in Australia to enhance network management using its cloud-based solutions. Oracle’s emphasis on hybrid cloud environments has attracted industries seeking flexibility and security.

Top Strategies Used by Key Market Participants

Key players in the Asia Pacific software market employ diverse strategies to maintain their competitive edge. Localization is a major focus, with companies tailoring products to meet regional preferences and regulatory requirements. Partnerships with governments and industries streamline implementation, ensuring scalability and compliance. Additionally, investments in AI, IoT, and cloud technologies enhance system capabilities by enabling predictive analytics and real-time decision-making. Companies also prioritize cybersecurity, adopting advanced encryption protocols to address vulnerabilities.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, Microsoft Corporation expanded its Azure cloud platform in India by enabling businesses to leverage AI-driven analytics for operational efficiency and boosting regional adoption rates.

- In June 2023, SAP SE launched a low-cost SaaS platform in Southeast Asia, which is targeting SMEs and integrating AI and IoT capabilities to enhance predictive analytics for manufacturing facilities.

- In August 2023, Oracle Corporation introduced an AI-powered analytics platform in Japan by streamlining decision-making processes for enterprises and improving data-driven insights.

- In November 2023, Microsoft Corporation partnered with regional governments in Australia to promote digital literacy by fostering wider adoption of its productivity tools and cloud solutions.

- In January 2024, SAP SE collaborated with local firms in Vietnam to integrate IoT into its ERP systems by reducing operational costs for manufacturing plants by 30% and enhancing scalability.

MARKET SEGMENTATION

This research report on the asia pacific software market has been segmented and sub-segmented into the following.

By Type

- Application Software

- System Infrastructure Software

- Productivity Software

By Deployment

- On-Premises

- Cloud

By Vertical

- IT

- Telecom

By Country

- China

- India

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Indonesia

- Philippines

- Vietnam

- Singapore

- Rest of APAC

Frequently Asked Questions

Which countries are the major players in the Asia Pacific software market?

Key countries include China, India, Japan, South Korea, Australia, and Singapore—each with strong tech ecosystems and increasing investments in software development and innovation.

How is cloud adoption impacting the Asia Pacific software landscape?

Cloud adoption is accelerating software delivery and scalability, making SaaS models more popular, especially among SMEs. Major global cloud providers and local players are rapidly expanding in the region.

What role does AI play in the software market in Asia Pacific?

AI is being integrated into various software applications, from customer service (chatbots) to data analytics and predictive modeling, especially in sectors like finance, healthcare, and manufacturing.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com