Asia Pacific Solar Microinverter Market Research Report – Segmented By Type (Single Phase, Three Phase), Application, Power Rating, Distribution Channel, Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2026 to 2034

Market Size, 2025

$737.12 MnMarket Estimate, 2026

$881.74 MnMarket Forecast, 2034

$3696.33 MnCAGR, 2026–2034

19.62%Asia Pacific Solar Microinverter Market Size

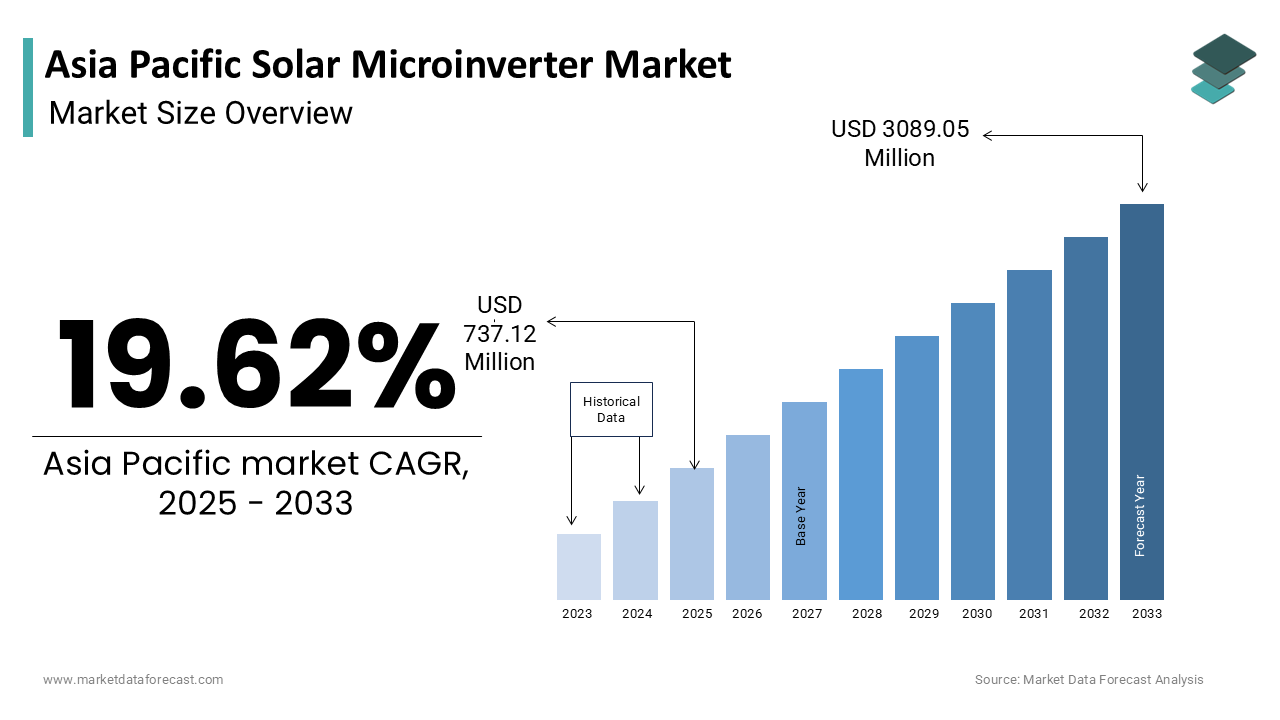

The Asia Pacific solar microinverter market was worth USD 737.12 million in 2025. The Asia Pacific market is expected to reach USD 3696.33 million by 2034 from USD 881.74 million in 2026, rising at a CAGR of 19.62% from 2026 to 2034.

The Asia Pacific solar microinverter market refers to the part of distributed energy technology that enables individual photovoltaic (PV) panels in a solar array to operate independently by converting DC power to AC at the panel level. Unlike traditional string inverters, which manage entire arrays collectively, microinverters optimize energy output from each solar module, enhancing system efficiency, reliability, and safety. Their growing adoption is particularly evident in rooftop residential and small commercial solar installations where shading, orientation differences, and module-level monitoring offer distinct advantages.

Governments across the region are advancing clean energy goals through supportive policies, subsidies, and net metering programs—factors that are accelerating solar PV deployment and, in turn, creating demand for advanced inverter technologies. In addition, rising consumer awareness about energy independence and smart home integration is influencing purchasing behavior toward high-performance components like microinverters.

MARKET DRIVERS

Rising Popularity of Rooftop Solar Installations in Residential and Commercial Sectors

One of the key drivers of the Asia Pacific solar microinverter market is the rapid expansion of rooftop solar installations in both residential and commercial sectors. Governments in countries such as India, Australia, Japan, and South Korea have introduced aggressive feed-in tariffs, tax incentives, and net metering policies to encourage decentralized solar adoption. Microinverters are particularly well-suited for these applications due to their ability to handle partial shading, improve system efficiency, and provide real-time performance monitoring at the module level. Also, the rise of prosumer culture, where households not only consume but also generate and sell back electricity is further boosting demand for intelligent energy solutions. Customers equipped with smart meters and home energy management systems benefit from the enhanced analytics and control features offered by microinverter-integrated setups.

Advancements in Smart Grid and Digital Energy Management Technologies

Technological advancements in smart grid infrastructure and energy management systems are significantly contributing to the growth of the Asia Pacific solar microinverter market. The integration of IoT-enabled devices, cloud-based monitoring platforms, and AI-driven diagnostics into solar PV systems has increased the demand for modular and intelligent power conversion equipment like microinverters. According to McKinsey & Company, utilities and policymakers across the Asia Pacific are investing heavily in smart grid modernization to enhance grid stability, reduce transmission losses, and accommodate higher shares of intermittent renewable energy. In Japan, initiatives such as the Smart Community Alliance promote the use of decentralized energy resources, including microinverters, to facilitate real-time load balancing and bidirectional energy flow.

Similarly, Australia’s Australian Renewable Energy Agency (ARENA) supports projects that deploy microinverter-based solar arrays in conjunction with battery storage and smart controllers to optimize local consumption and reduce grid dependency. In China, digital twin technology is being tested in pilot smart cities to simulate and manage distributed PV assets using microinverter data streams.

MARKET RESTRAINTS

High Initial Cost Compared to Traditional String Inverters

A primary constraint impeding the widespread adoption of solar microinverters in the Asia Pacific region is their relatively high upfront cost compared to conventional string inverters. While microinverters offer superior performance optimization and longer lifespans, their per-watt installation expense remains significantly higher, deterring cost-sensitive consumers and small-scale developers. According to Bloomberg NEF, the average price difference between microinverters and string inverters ranges between 15% to 25% per watt, depending on system size and brand preferences. This cost differential poses a challenge in emerging economies such as India, Indonesia, and the Philippines, where affordability and return-on-investment timelines play a decisive role in solar investment decisions. Moreover, in large-scale utility or industrial PV plants, the economic benefits of microinverters are often outweighed by the lower maintenance requirements of centralized string or central inverters. As a result, many project developers prioritize immediate cost savings over long-term efficiency gains, limiting the penetration of microinverter-based systems in certain segments.

Limited Awareness and Technical Expertise Among Installers and Consumers

Another significant barrier to the growth of the Asia Pacific solar microinverter market is the limited awareness and technical expertise among installers and end-users regarding the benefits and optimal deployment of microinverter systems. Many solar professionals in the region are still trained primarily in handling conventional string inverters, making the transition to microinverter-based solutions slower and more complex. This knowledge gap affects system design quality, commissioning procedures, and post-installation support, leading to suboptimal performance and consumer dissatisfaction in some cases. Consumer perception also plays a crucial role. Many homeowners and small business owners remain unfamiliar with the advantages of microinverters, such as individual panel monitoring, enhanced durability, and reduced performance degradation under partial shading conditions.

MARKET OPPORTUNITIES

Integration with Self-Consumption and Peer-to-Peer Energy Trading Models

One of the most promising opportunities for the Asia Pacific solar microinverter market lies in its integration with self-consumption and peer-to-peer (P2P) energy trading models. As governments and utilities seek to decentralize energy distribution and improve grid efficiency, microinverters are becoming instrumental in enabling localized energy sharing and consumption optimization. In Japan, the Ministry of Economy, Trade and Industry (METI) has been actively promoting community-based energy trading through blockchain-enabled platforms that allow households to trade excess solar electricity directly with neighbors. These systems rely heavily on microinverters' ability to monitor and control energy flows at the individual panel level, ensuring accurate billing and efficient resource allocation. Similarly, in Australia, the Australian Renewable Energy Agency (ARENA) has funded multiple P2P energy trials in cities like Perth and Melbourne, where microinverter-equipped homes supply surplus power to nearby buildings via smart contracts. These experiments demonstrate how microinverters can support dynamic, decentralized energy ecosystems beyond simple grid-tied operations. India is also exploring self-consumption models under its Green Open Access Policy, encouraging industries and residential complexes to adopt solar plus storage configurations. In such scenarios, microinverters enable granular control over energy usage, aligning with evolving regulatory frameworks and consumer demand for greater energy autonomy.

Expansion of Off-Grid and Rural Electrification Programs

The increasing emphasis on off-grid and rural electrification programs presents a major opportunity for the Asia Pacific solar microinverter market. Many remote and island communities in countries like Indonesia, the Philippines, Thailand, and Papua New Guinea still lack reliable access to centralized electricity grids, prompting governments and development agencies to invest in decentralized solar solutions. According to the International Energy Agency, over 40 million people in Southeast Asia lacked access to electricity as of 2023 , particularly in isolated archipelagos and mountainous regions. To address this challenge, national energy ministries are deploying modular solar PV systems integrated with microinverters to ensure stable and independent power supply. In Indonesia, the Directorate General of Electricity launched the "One Million Solar Roof Program", targeting off-grid villages and small islands with tailored solar kits. These systems benefit from microinverters’ ability to operate independently, reducing dependency on battery banks and minimizing system complexity. The Philippines Department of Energy has also introduced similar initiatives, supporting microgrid projects powered by microinverter-based solar arrays that provide uninterrupted electricity to healthcare facilities, schools, and local businesses in underserved areas.

MARKET CHALLENGES

Regulatory Uncertainties and Grid Interconnection Standards

A critical challenge facing the Asia Pacific solar microinverter market is the inconsistency in regulatory frameworks and grid interconnection standards across different countries in the region. Unlike Europe and North America, where harmonized technical norms govern solar PV integration, the Asia Pacific suffers from fragmented policies that vary significantly between nations and even within provinces or states. In India, for instance, state-level regulators differ in their net metering policies, affecting the financial viability of microinverter-based rooftop systems. Some jurisdictions impose restrictions on export limits or charge additional fees for grid synchronization, discouraging homeowner investment. Similarly, in China, while national-level directives promote distributed solar, local utility companies often apply stringent certification requirements for grid-connected inverters, causing delays in approvals and increased compliance costs for manufacturers.

Competition from Low-Cost Local Manufacturers

Intense competition from low-cost domestic manufacturers is another key challenge for established microinverter brands operating in the Asia Pacific. While global players such as Enphase Energy and Tigo Energy have made inroads into the region, they face stiff competition from emerging local firms offering budget-friendly alternatives that appeal to price-sensitive customers. China, in particular, has seen a proliferation of regional companies producing microinverters at significantly lower price points than their Western counterparts. These manufacturers often leverage existing semiconductor and electronics production capabilities to achieve economies of scale, undercutting premium providers in terms of affordability. Though sometimes lacking in software sophistication, these products gain traction due to their competitive pricing and ease of integration with locally assembled solar modules. This aggressive price competition forces global brands to either localize production, compromise on margins, or differentiate through enhanced software features and ecosystem compatibility—strategies that require substantial investment and time to implement effectively.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 19.62% |

| Segments Covered | By Type, Application, Power Rating, Distribution Channel and Country |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, the Philippines, Indonesia, Singapore, and the Rest of APAC. |

| Market Leaders Profiled | Enphase Energy Inc., APsystems (Altenergy Power System Inc.), Darfon Electronics Corp., Chilicon Power LLC, NEP (Northern Electric Power), SunPower Corporation, SMA Solar Technology AG, Renesola Ltd., Omnik New Energy Co. Ltd., and Altenergy Power System Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The single-phase segment accounted for a8.5% of the Asia Pacific solar microinverter market in 2024. This dominance is primarily driven by its extensive adoption across residential and small commercial settings, where electrical infrastructure supports lower power loads. One of the key factors fueling this growth is the rising demand for home-use weight management devices—ranging from smart scales to connected health monitors—that operate efficiently on single-phase systems. According to the International Energy Agency (IEA), a significant share of households in Southeast Asia now have access to electricity, enabling greater adoption of such appliances. Moreover, urbanization rates in countries like India and Indonesia are increasing rapidly; data from the World Bank shows that urban populations in these two nations grew by over 12% between 2015 and 2023, directly boosting demand for lightweight, easily installable equipment relying on single-phase connections. In addition, government initiatives promoting energy efficiency at the consumer level have further accelerated the integration of smart, single-phase-enabled products. For instance, China’s National Development and Reform Commission launched a Smart Home Appliance Efficiency Program in 2021, aiming to retrofit 40 million homes with IoT-connected, low-voltage devices—many of which operate on single-phase systems. This initiative has spurred domestic innovation and increased penetration of energy-efficient appliances. Furthermore, cost-effectiveness plays a crucial role. Installation and maintenance costs of single-phase systems are significantly lower compared to three-phase alternatives.

The three-phase segment is projected to grow at the fastest rate in the Asia Pacific solar microinverter market, exhibiting a CAGR of approximately 11.2% from 2025 to 2033. This rapid rise is largely attributable to the increasing deployment of high-capacity industrial sensors, AI-driven weight analytics systems, and automated logistics solutions that require robust power supply configurations. One major driver is the rise of smart manufacturing and Industry 4.0 across countries like South Korea, Japan, and China. These facilities increasingly use multi-axis digital load cells and intelligent conveyors that necessitate stable, high-power electrical inputs—best provided by three-phase infrastructure. Another contributing factor is the growing application of weight management technologies in large-scale healthcare and logistics sectors. In Australia, for example, hospitals are adopting heavy-duty patient handling systems that integrate three-phase powered bariatric scales and lifting devices.

Lastly, the surge in e-commerce and warehouse automation is driving demand for high-performance industrial weighbridges and conveyor-based sorting systems. Amazon’s expansion into Southeast Asia—including new fulfillment centers in Malaysia and Thailand since 2022—has led to higher installation of three-phase-powered digital weighing platforms.

By Application Insights

The residential application segment held a6.5% of the Asia Pacific solar microinverter market in 2024. This share reflects the growing consumer interest in personal health tracking and home-based wellness technologies, particularly in urbanized regions like Singapore, Japan, and South Korea. One of the primary drivers behind this segment’s dominance is the escalating prevalence of obesity and lifestyle diseases across the region. According to the World Health Organization (WHO), in excess of 180 million adults in the Asia-Pacific suffer from overweight or obesity, with countries like Indonesia and Thailand witnessing sharp increases in recent years. This has catalyzed the adoption of smart body composition analyzers, Bluetooth-enabled scales, and cloud-connected fitness apps, all falling under the umbrella of residential weight management solutions. Moreover, rising disposable incomes in emerging economies such as India and the Philippines have enabled broader access to premium health tech products. These trends empower consumers to purchase smart weighing devices through online platforms without hesitation.

Another critical enabler is the expansion of digital health ecosystems. Governments in Japan and South Korea have actively promoted telehealth and remote monitoring tools, especially post-pandemic. In Japan, the Ministry of Health, Labour and Welfare launched an initiative in 2022 to subsidize home health management kits, including smart scales, encouraging elderly citizens to monitor health metrics independently.

The Industrial / Utility application segment is anticipated to register a CAGR of around 12.6% during the forecast period (2025–2033). This quick expansion is being propelled by large-scale digitization efforts in logistics, waste management, and utilities infrastructure across the Asia Pacific. One of the most significant driving forces is the modernization of municipal waste and sanitation services, particularly in densely populated cities like Delhi, Jakarta, and Manila. Governments are increasingly deploying smart bin systems equipped with real-time weight sensors to optimize collection routes and reduce operational inefficiencies. Another key catalyst is the automation of freight and cargo handling operations. As global trade volumes rebound post-pandemic, ports and logistics hubs across the region—from Shanghai to Sydney—are investing heavily in automated weighbridge systems, conveyor belt scales, and drone-based payload monitoring. Moreover, the utility sector’s push towards smart grids and metering systems has created room for advanced load monitoring solutions. According to the Australian Energy Market Operator (AEMO), the number of smart grid installations increased in 2023, directly influencing the uptake of high-precision industrial weight sensors.

By Power Rating Insights

The “Below 250 W” power rating segment commanded the largest share, i.e,. 59% of the Asia Pacific solar microinverter market in 2024. This is attributed to the widespread usage of compact, low-energy-consuming devices in residential and portable applications. One of the main growth drivers is the surge in wearable and mobile health devices , such as smartwatches, fitness bands, and portable bioimpedance analyzers. These gadgets generally operate on minimal power consumption levels to ensure longer battery life and user convenience. Apart from these, advancements in semiconductor technology and miniaturization have enabled manufacturers to develop highly efficient, ultra-low-power microcontrollers and sensor chips. Companies like Texas Instruments and STMicroelectronics have introduced specialized ICs optimized for low-power operation, allowing developers to design sleeker and more energy-efficient weight-monitoring devices. This shift has been especially prominent in countries such as South Korea and Japan, where consumer electronics innovation is thriving. Another important factor is the growing preference for portable and multifunctional health devices, particularly in rural and semi-urban areas. In India, for instance, numerous startups have launched low-cost, solar-powered digital scales capable of functioning at less than 100 W, catering to off-grid communities. The Ministry of Health & Family Welfare reported in 2023 that over 10 million rural households participated in national health screening programs, any of which used low-power, portable weighing machines.

The Above 500 W power rating segment is expected to grow at the highest CAGR of about 13.5%. This swift acceleration is primarily due to the increasing integration of weight management systems in industrial and institutional environments that require high-performance, continuous-operation capabilities. A pivotal factor behind this growth is the adoption of AI-integrated weight monitoring systems in manufacturing and food processing industries. Large-scale food packaging plants in China and Thailand are increasingly deploying automated sorting and portioning machines that utilize high-wattage load cells and digital indicators. Also, the rise of autonomous robotics in warehousing and logistics is fueling demand for high-power sensors and scales. E-commerce giants such as Alibaba and Flipkart have deployed thousands of robotic palletizers and autonomous guided vehicles (AGVs) equipped with real-time weight analysis systems. These devices must operate on robust electrical setups to handle variable loads and maintain calibration accuracy. Lastly, the development of high-capacity healthcare equipment, such as motorized patient lifts and ICU bed scales, is contributing significantly to this segment's expansion. In Japan, where the aging population necessitates advanced care infrastructure, hospitals are installing smart beds with embedded load sensors rated above 500 W, capable of transmitting real-time weight and pressure data to centralized systems.

By Distribution Channel Insights

The online distribution channel accounted for the biggest market share of a2.6% in the Asia Pacific solar microinverter market in 2024. This segment's position is primarily driven by the rapid expansion of e-commerce platforms and the growing shift toward contactless shopping, especially after the pandemic-induced behavioral changes in consumer habits. One of the key enablers is the explosive growth of cross-border e-commerce, particularly in countries like India, Indonesia, and the Philippines. Platforms such as Amazon, Alibaba, and Shopee have significantly expanded their presence in these markets, offering a wide array of smart scales, fitness trackers, and health apps. Another influential factor is the increasing smartphone penetration and mobile internet accessibility, which has enabled seamless online shopping experiences. GSMA reported that by the end of 2023, 51% of the APAC population was using mobile internet, facilitating greater exposure to health tech products via app-based storefronts and social commerce. Moreover, digital marketing campaigns and influencer endorsements have played a crucial role in raising awareness and trust in online purchases. Finally, enhanced logistics and faster delivery networks offered by companies like Ninja Van and J&T Express have reduced delivery times and improved customer satisfaction, making online channels more attractive than traditional retail stores.

The Direct Sales distribution channel is projected to exhibit the highest CAGR of approximately 14.3%. This impressive growth trajectory is being driven by the increasing reliance on manufacturer-to-consumer engagement models, especially in the B2B and enterprise sectors, where customized weight management solutions are in high demand. One of the key drivers is the rise of tailored health tech solutions for corporate wellness programs, particularly in countries like Japan, South Korea, and Australia. Multinational corporations are increasingly collaborating directly with manufacturers to implement employee health monitoring systems, including personalized weight assessment tools. For example, Panasonic Life Solutions partnered directly with several Japanese firms in 2023 to provide custom-built smart body composition analyzers for workplace health assessments, bypassing intermediaries to ensure better pricing and service customization. Another notable factor is the expansion of direct-to-hospital procurement models in the healthcare industry, especially in emerging markets like India and Indonesia. Hospitals and clinics are opting for direct contracts with suppliers to procure high-end bariatric scales, patient lift systems, and medical-grade weighing platforms. Also, industrial buyers are preferring direct interactions with manufacturers for technical support and system integration. In China, for instance, automotive and logistics firms are engaging directly with scale manufacturers to integrate weight sensors into assembly lines and loading docks. The China Association of Automobile Manufacturers noted that over 50% of new factory automation projects in 2023 involved direct supplier collaboration, enhancing efficiency and minimizing lead times. Lastly, digital transformation in sales processes, including virtual consultations, live demos, and cloud-based quotations, has enabled manufacturers to build stronger relationships with end-users. Companies like Mettler Toledo and Avery Weigh-Tronix have invested heavily in CRM solutions and AI chatbots to streamline direct outreach.

REGIONAL ANALYSIS

China held the top position in the Asia Pacific solar microinverter market by commanding 32.5% of the regional market in 2024. As the world's largest producer and installer of solar PV systems, China has aggressively pursued distributed solar generation, where microinverters play a vital role in optimizing performance at the module level. The Chinese government’s Renewable Energy Law and the 14th Five-Year Plan (2021–2025) have laid a clear roadmap for solar expansion, including ambitious targets for rooftop and community solar installations. According to the National Energy Administration of China, newly added distributed photovoltaic (PV) capacity reached 54 GW in 2023, surpassing previous records and driving demand for microinverter technologies that enable panel-level monitoring and safety enhancements. Additionally, strong domestic manufacturing capabilities have bolstered the availability and affordability of microinverters. Leading Chinese firms such as Sungrow Power, Enphase Energy (with a significant R&D and production base in China), and GoodWe have scaled their output, benefiting from local supply chains and aggressive innovation in MPPT efficiency and wireless communication features. Furthermore, grid parity and feed-in-tariff reductions have incentivized homeowners and businesses to adopt solar systems with microinverters for better ROI.

India is a fast-emerging hub with strong policy backing in the Asia Pacific solar microinverter market. The country has witnessed exponential growth in solar adoption, driven by both central and state-level incentives aimed at decentralizing power generation and improving energy access. Under this initiative, subsidies of up to 40% are available for rooftop solar installations, encouraging homeowners to invest in microinverter-based systems that enhance performance and safety. Moreover, rising electricity tariffs and frequent power outages in rural and semi-urban areas have prompted consumers to seek reliable solar backup solutions. According to the Central Electricity Authority (CEA), electricity prices in industrial categories rose, pushing businesses to opt for modular and scalable solar systems with microinverters that allow easy expansion and maintenance. India’s domestic manufacturing push under the Production-Linked Incentive (PLI) scheme has also contributed to the microinverter boom. The Government of India allocated INR 24,000 crores (~USD 2.9 billion) under the PLI for high-efficiency solar PV modules, indirectly spurring demand for compatible balance-of-system components, including microinverters. In addition, international players such as Enphase and SolarEdge have intensified their presence in India, partnering with local distributors and installers to tailor products for Indian climatic and grid conditions.

Japan occupied the major spot in the Asia Pacific solar microinverter market. As one of the earliest adopters of solar PV globally, Japan has steadily transitioned from centralized inverters to distributed architectures featuring microinverters, especially in residential and small commercial applications. The post-Fukushima shift away from nuclear energy has accelerated Japan’s pursuit of decentralized renewables. Like, Japan added nearly 8.5 GW of new solar capacity in 2023, with over 60% of new residential installations incorporating microinverter technology. This preference stems from microinverters’ ability to maximize yield in space-constrained rooftops and shaded environments. Also, strict safety regulations and grid codes have made microinverters a preferred choice. Furthermore, aging infrastructure and the need for asset longevity have encouraged the adoption of resilient and modular systems. Major Japanese utilities and housing developers, including Mitsubishi and Panasonic, have begun standardizing microinverters in new-build solar homes to ensure long-term reliability and ease of maintenance.

Australia has a high penetration in the residential solar market. The country is among the global leaders in rooftop solar adoption, and this has created fertile ground for microinverter deployment, especially in the residential segment. According to the Clean Energy Council (CEC), over 3.7 million Australian households had installed solar PV systems by the end of 2023, representing nearly 32% of total households Moreover, stringent safety standards enforced by the Australian Standards Institute (AS/NZS 5033) mandate safer, lower-voltage systems, favoring microinverter adoption. Installers prefer them for their plug-and-play simplicity and reduced risk of DC arc faults, aligning with the regulatory environment. Additionally, the popularity of smart home technology in Australia has facilitated the integration of microinverters with home energy management systems. Major retailers like Enphase have capitalized on this trend, introducing bundled solutions with real-time monitoring dashboards accessible via smartphones.

South Korea has a rising interest in distributed solar solutions. Though traditionally reliant on centralized energy infrastructure, the country has recently embraced distributed generation models to meet climate goals and improve energy resilience. The Renewable Portfolio Standard (RPS) policy, administered by the Ministry of Trade, Industry and Energy (MOTIE), requires utilities to source a certain percentage of their electricity from renewables. According to Korea Energy Economics Institute (KEEI), South Korea added 5.1 GW of new solar PV capacity, with nearly 35% coming from small-scale residential and commercial projects —a segment where microinverters are gaining traction due to their superior shading response and lower installation complexity. Besides, government-backed green finance schemes such as the Green Investment Support Program have incentivized homeowners and SMEs to adopt microinverter-based systems by offering low-interest loans and insurance packages covering performance degradation and maintenance costs.

Top Players in the Asia Pacific Solar Microinverter Market

Enphase Energy

Enphase Energy is a global leader in solar microinverter technology and holds a strong presence in the Asia Pacific region. Known for pioneering microinverter systems, the company has played a crucial role in shifting the market away from traditional string inverters. In the Asia Pacific, Enphase has focused on expanding its product portfolio tailored to residential and small commercial applications. Its commitment to innovation, reliability, and system-level monitoring has made it a preferred choice among installers and end-users. Enphase's presence in countries like Australia, India, and Japan has been instrumental in shaping regional adoption trends.

SolarEdge Technologies

SolarEdge is another dominant player that has significantly influenced the growth of the solar microinverter segment in the Asia Pacific. While primarily known for its power optimizer technology, the company's integration of module-level electronics aligns closely with microinverter functionality, enabling high performance and energy optimization at the panel level. The company has expanded its distribution networks and partnered with local suppliers across Southeast Asia and Australia. SolarEdge’s emphasis on smart energy solutions and grid compatibility has strengthened its position in both residential and commercial markets.

GoodWe Technologies

GoodWe has emerged as a key domestic player in China and an influential exporter across the broader Asia Pacific region. Initially known for string inverters, GoodWe has aggressively expanded into the microinverter space to meet growing demand for distributed solar applications. With a focus on affordability, reliability, and localized customer support, the company has gained traction in emerging markets such as India, Vietnam, and the Philippines. GoodWe’s ability to blend advanced technological features with cost-effective deployment strategies has positioned it as a formidable contender in the regional microinverter landscape.

Top Strategies Used by Key Market Participants

One major strategy employed by key players in the Asia Pacific solar microinverter market is product innovation and technology differentiation. Companies are continuously enhancing their offerings with features such as improved energy harvesting, module-level monitoring, wireless connectivity, and integrated smart home compatibility. These advancements help differentiate brands in a competitive environment and cater to evolving consumer preferences for intelligent, high-performance solar systems.

Another critical approach is strategic partnerships and collaborations with local distributors, installers, and government bodies. By aligning with regional stakeholders, companies can better understand local market needs, streamline supply chains, and ensure regulatory compliance. These alliances also facilitate faster market penetration and improved after-sales service, which are vital for maintaining long-term customer relationships.

Lastly, localized marketing and customer education initiatives play a crucial role. Given the varying levels of awareness about microinverters across the region, companies invest in targeted campaigns, training programs for installers, and digital engagement to build trust and drive adoption.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Asia Pacific solar microinverter market include

- Enphase Energy Inc.

- APsystems (Altenergy Power System Inc.)

- Darfon Electronics Corp.

- Chilicon Power LLC

- NEP (Northern Electric Power)

- SunPower Corporation

- SMA Solar Technology AG

- Renesola Ltd.

- Omnik New Energy Co. Ltd.

- Altenergy Power System Inc.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific solar microinverter market is intensifying due to rising demand for decentralized solar power systems, increasing consumer awareness, and supportive government policies promoting renewable energy adoption. As more households and businesses shift toward sustainable energy solutions, the need for efficient, reliable, and scalable solar technologies has grown, propelling the importance of microinverters. International players with established global reputations are actively expanding their footprint in the region, while domestic manufacturers are leveraging cost advantages and local market knowledge to gain a competitive edge. The market landscape is characterized by continuous innovation, aggressive expansion strategies, and efforts to differentiate through performance, durability, and integration capabilities. Companies are investing heavily in research and development to enhance product efficiency and introduce smart functionalities that align with the region’s digital transformation trends. Additionally, strategic moves such as channel partnerships, localized customer support, and educational outreach have become essential for capturing market share.

RECENT MARKET DEVELOPMENTS

- In February 2024, Enphase Energy launched a new line of smart energy management solutions integrated with its microinverter systems, targeting residential users in Japan and Australia. This move aimed to enhance user experience by offering real-time monitoring and improved grid interaction, reinforcing Enphase’s leadership in the region.

- In May 2024, SolarEdge Technologies announced a strategic partnership with a leading Australian solar distributor to expand its reach in the residential and small commercial sectors. This collaboration was designed to streamline logistics, improve after-sales service, and ensure quicker access to products across remote and urban areas.

- In July 2024, GoodWe Technologies introduced a series of budget-friendly yet high-performance microinverter models tailored for the Indian and Southeast Asian markets. The launch was part of a broader initiative to capture market share in emerging economies where affordability plays a decisive role in purchasing decisions.

- In September 2024, Huawei Smart PV launched an enhanced cloud-based monitoring platform compatible with its microinverter-integrated systems, targeting commercial installations in China and South Korea. The platform enabled seamless data analytics and predictive maintenance, strengthening Huawei’s foothold in enterprise solar solutions.

- In November 2024, Chint Power Systems established a dedicated microinverter production line in Vietnam to serve the growing ASEAN market. This investment was intended to reduce lead times, cut costs, and ensure better alignment with regional regulatory standards, thereby improving the company’s competitiveness in the Asia Pacific.

MARKET SEGMENTATION

This research report on the Asia Pacific solar microinverter market is segmented and sub-segmented into the following categories.

By Type

- Single Phase

- Three Phase

By Application

- Residential

- Industrial / Utility

By Power Rating

- Below 250 W

- Above 500 W

By Distribution Channel

- Online

- Direct Sales

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is driving the demand for solar microinverters in Asia Pacific?

Rising environmental concerns, declining solar panel costs, advancements in solar technology, and government initiatives like solar subsidies and net metering programs are fueling market demand.

What is the future outlook for the Asia Pacific Solar Microinverter Market?

The market is expected to grow significantly through 2033, driven by smart grid integration, the rise of residential solar rooftops, and increased preference for module-level power electronics (MLPE).

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com