Asia Pacific Variable Frequency Drive Market Size, Share, Trends & Growth Forecast Report By Product Type (AC Drives , Servo Drives), Application, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore And Rest of Asia-Pacific), Industry Analysis From 2025 To 2033

Asia Pacific Variable Frequency Drive Market Size

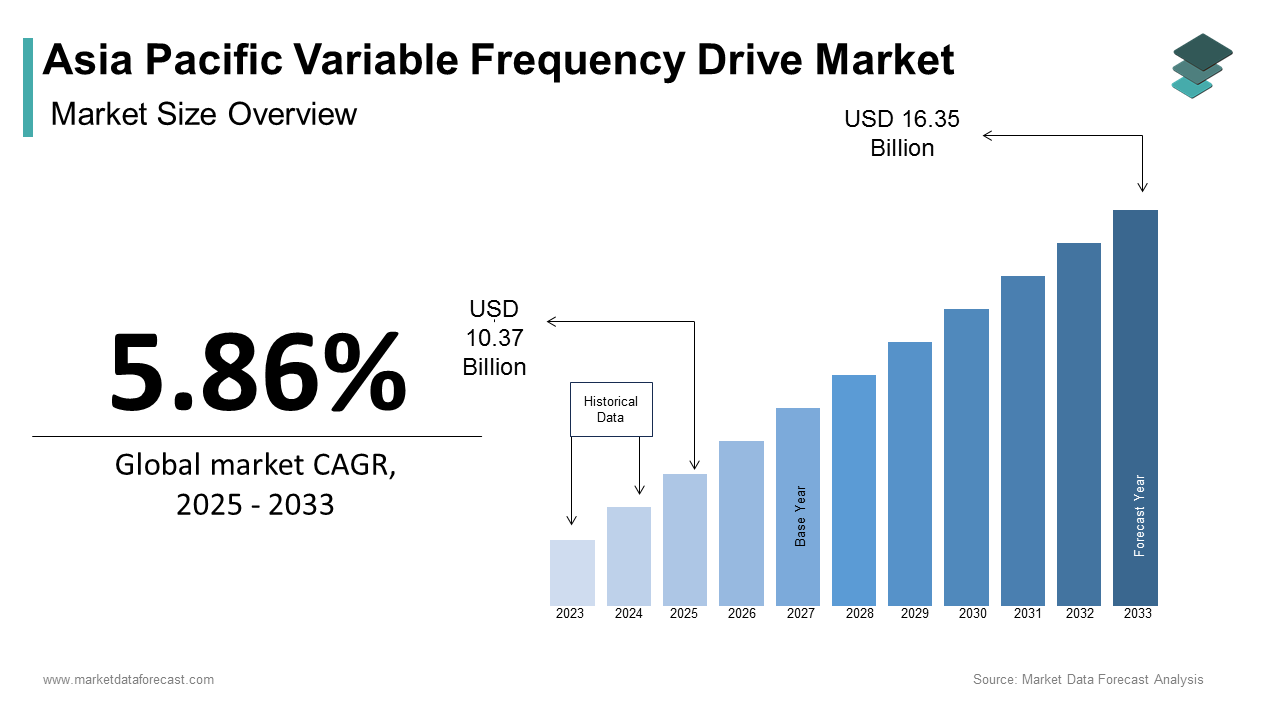

The Asia Pacific variable frequency drive market size was calculated to be USD 9.80 billion in 2024 and is anticipated to be worth USD 16.35 billion by 2033, from USD 10.37 billion in 2025, growing at a CAGR of 5.86% during the forecast period.

MARKET DRIVERS

Industrial Automation and Smart Manufacturing

Industrial automation and smart manufacturing serve are prompting the growth of the Asia Pacific VFD market with the region's push toward Industry 4.0. Government initiatives further amplify this trend. As per the Ministry of Industry and Information Technology in China, subsidies for industrial automation have increased by 25% since 2020, encouraging manufacturers to adopt VFDs. Additionally, the rise of IoT-enabled factories creates new opportunities, as VFDs integrate seamlessly with smart systems for real-time monitoring and predictive maintenance.

Energy Efficiency Regulations

Energy efficiency regulations is also propelling the Asia Pacific VFD market amid growing concerns about climate change and resource conservation. According to the International Renewable Energy Agency, industrial motors account for approximately 40% of global electricity consumption, making them a prime target for energy-saving measures. For instance, Japan’s Top Runner Program mandates the use of energy-efficient equipment, including VFDs, in manufacturing facilities. Similarly, India’s Perform, Achieve, and Trade (PAT) scheme incentivizes industries to reduce energy consumption by adopting advanced technologies like VFDs. The surge in renewable energy projects further amplifies demand. BloombergNEF reports that Asia Pacific accounted for 57% of global renewable energy capacity additions in 2022, necessitating VFDs for wind turbine pitch control and solar tracking systems. Additionally, urbanization trends drive the adoption of VFDs in HVAC systems for commercial buildings. These regulatory and environmental factors collectively reinforce the pivotal role of energy efficiency mandates in shaping the VFD market’s growth trajectory.

MARKET RESTRAINTS

High Initial Costs

The high initial cost is hindering the growth of the Asia Pacific VFD market by deterring small and medium enterprises (SMEs) from adopting the technology despite its long-term benefits. According to Deloitte, the average cost of a VFD system ranges from 500to5,000, depending on specifications, making it inaccessible for budget-constrained businesses. Moreover, the complexity of installation and integration further compounds the issue. While larger corporations can absorb these costs, smaller players often prioritize short-term affordability over long-term efficiency gains.

Technical Complexity and Maintenance Challenges

The technical complexity and maintenance is another factor hampering the growth of the Asia Pacific VFD market in industries with limited technical expertise. According to the International Labour Organization, over 70% of industrial operators in emerging economies lack adequate training in advanced motor control technologies by resulting in operational inefficiencies. For instance, improper installation or calibration of VFDs can lead to motor overheating or resonance issues, increasing downtime and repair costs. Additionally, the need for regular maintenance amplifies operational expenses.

MARKET OPPORTUNITIES

Adoption of IoT-Enabled VFDs

The adoption of IoT-enabled VFDs is significant opportunity for the growth of the Asia Pacific VFD market by enabling manufacturers to enhance operational efficiency and cater to evolving customer demands. According to McKinsey & Company, IoT integration in industrial equipment is projected to boost productivity by up to 25%, offering a competitive edge. For instance, smart VFDs equipped with real-time monitoring and predictive maintenance capabilities are gaining traction in countries like South Korea and Japan, where precision and reliability are paramount. China, a leader in digital innovation, is spearheading the adoption of IoT-enabled VFDs in smart factories. As per Deloitte, China’s smart manufacturing market is expected to grow at a CAGR of 15% through 2025, driven by IoT deployments. Additionally, remote-controlled systems are becoming essential in hazardous environments, such as mining and chemical processing, enhancing worker safety.

Rising Investments in Renewable Energy Projects

The rising investments in renewable energy projects offer a significant growth for the Asia Pacific VFD market with the region’s commitment to sustainability. According to BloombergNEF, renewable energy capacity in Asia Pacific is expected to double by 2030, surpassing 2,000 gigawatts. This expansion necessitates advanced motor control solutions, particularly for wind turbine pitch control and solar tracking systems. For example, India’s target to achieve 500 GW of renewable energy capacity by 2030 will require extensive VFD deployment, creating a robust demand pipeline.

China’s dominance in the solar panel manufacturing sector drives the need for specialized VFDs in production facilities. As per a report by the International Energy Agency, China installed over 50 GW of solar capacity in 2022 alone with the scale of opportunities. Offshore wind projects, particularly in Vietnam and Taiwan, further amplify VFD demand due to their complex installation requirements.

MARKET CHALLENGES

Intense Market Competition

Intense market competition poses a challenge for the growth of Asia Pacific VFD market with the presence of numerous domestic and international players vying for market share. India and Southeast Asia witness similar dynamics, where local players struggle to compete with established brands. A study by the Confederation of Indian Industry reveals that price sensitivity among buyers exacerbates the issue, with 60% of customers prioritizing cost over quality. Additionally, the lack of product differentiation limits growth opportunities, forcing companies to focus on aggressive marketing strategies rather than innovation. Intellectual property disputes further complicate the scenario, as per the World Intellectual Property Organization, with allegations of design infringements being common.

Skilled Labor Shortages

Skilled labor shortages represent another challenge for the growth of the Asia Pacific VFD market. According to the International Labour Organization, the industrial automation sector faces a deficit of skilled operators, particularly in emerging economies like India and Indonesia. For instance, a survey by the Associated Chambers of Commerce and Industry of India reveals that nearly 40% of manufacturing projects experience delays due to a lack of trained personnel. This shortage is exacerbated by the rapid pace of industrial modernization, which outstrips workforce availability. Furthermore, the complexity of modern VFDs, equipped with advanced technologies, requires specialized training, which is often inaccessible to workers in rural areas. This scarcity not only impacts project timelines but also increases operational risks, as untrained personnel are more prone to accidents.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.86% |

| Segments Covered | By Product Type, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of Asia-Pacific |

| Market Leaders Profiled | ABB Ltd., Siemens AG, Schneider Electric SE, Danfoss Group, Rockwell Automation Inc., Mitsubishi Electric Corporation, Fuji Electric Co. Ltd., Hitachi Ltd., Yaskawa Electric Corporation, Toshiba International Corporation, Delta Electronics Inc., WEG S.A. |

SEGMENTAL ANALYSIS

By Product Type Insights

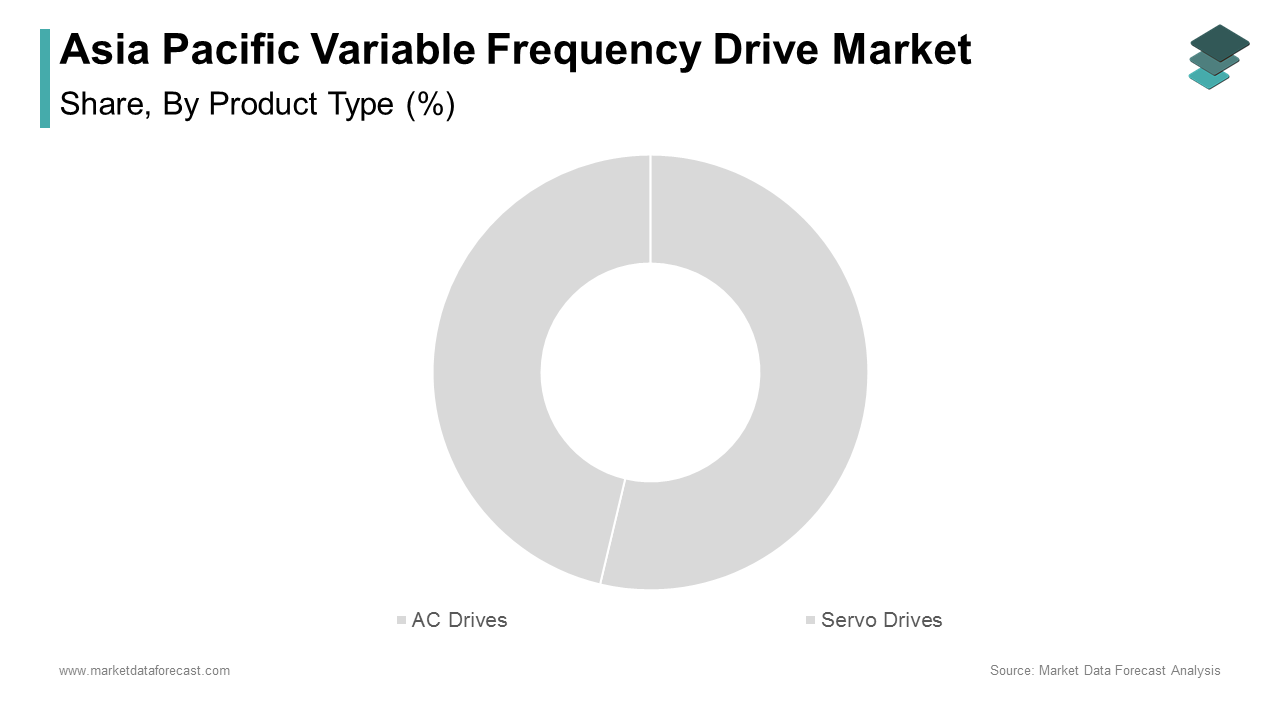

The AC drives segment held a dominant share of the Asia Pacific variable frequency drive market in 2024 owing to their versatility and energy efficiency by making them ideal for applications in pumps, HVAC systems, and conveyors. According to McKinsey & Company, AC drives are projected to reduce motor energy consumption by up to 30% by aligning with regional mandates for energy conservation. The widespread use of AC motors in industrial machinery.

The servo drives segment is anticipated to grow with a CAGR of 12.5% throughout the forecast period. This growth is fueled by their precision and adaptability in high-performance applications like robotics and CNC machines. For example, South Korea’s electronics sector, led by companies like Samsung and LG, relies heavily on servo drives for automated assembly lines, driving regional demand.

By Application Insights

The pumps segment held 30.2% of the Asia Pacific variable frequency drive market share in 2024 due to the growing emphasis on sustainability. For instance, India’s Jal Shakti Abhiyan initiative aims to optimize water usage through advanced pumping technologies, favoring VFD integration. Similarly, China’s agricultural sector, contributing approximately 10% to its GDP, utilizes VFD-equipped pumps for irrigation, reducing energy costs by up to 25%. Additionally, government policies promoting renewable energy projects amplify demand, as solar-powered pumps require precise motor control.

The HVAC systems segment is anticipated to grow with an expected CAGR of 11.8% in the coming years owing to the rapid urbanization and rising demand for energy-efficient building solutions. For example, India’s Smart Cities Mission aims to develop 100 smart cities, which is necessitating advanced HVAC systems with integrated VFDs to optimize energy consumption. Government initiatives further amplify this trend. As per the Ministry of Housing and Urban Affairs in India, subsidies for green buildings have increased by 20% since 2020, encouraging the adoption of VFD-enabled HVAC systems. Additionally, the proliferation of commercial spaces in urban centers like Singapore and Hong Kong drives demand for precise temperature control and energy savings.

REGIONAL ANALYSIS

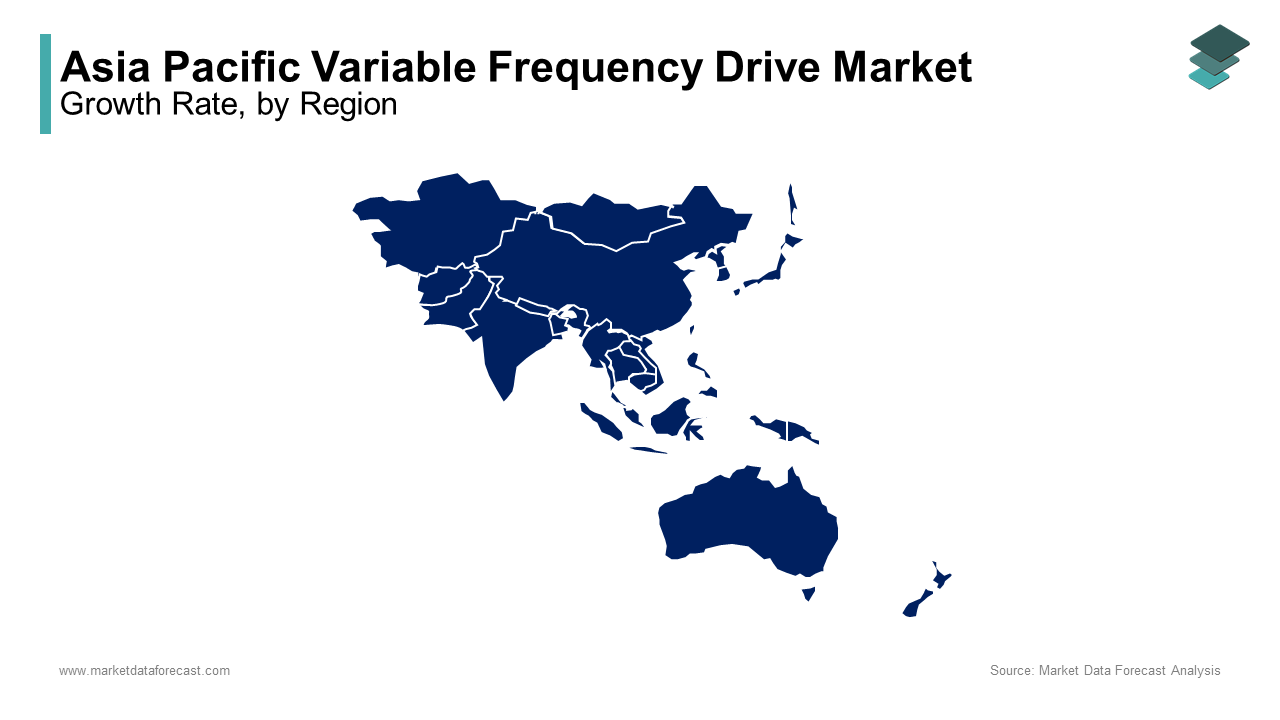

China

China was the top performer of the Asia Pacific variable frequency drive market with 40.3% of share in 2024 with its massive industrial base and stringent energy efficiency mandates. For instance, China’s "14th Five-Year Plan" allocates $150 billion to industrial modernization, emphasizing the adoption of VFDs in manufacturing facilities. Additionally, the country’s renewable energy projects, such as wind and solar installations, rely heavily on VFDs for motor control. According to the National Development and Reform Commission, subsidies for energy-saving technologies have increased by 30% since 2020, ensuring widespread adoption. Collaborations with global players like Siemens and ABB strengthen its technological edge.

India

India was ranked second with 20.3% of the Asia Pacific VFD market share in 2024 owing to the rapid urbanization and industrial expansion drive demand for VFDs. According to the Ministry of Power, energy efficiency initiatives like the Perform, Achieve, and Trade (PAT) scheme incentivize industries to adopt advanced technologies like VFDs. Infrastructure development also plays a pivotal role. For instance, India’s Smart Cities Mission aims to develop 100 smart cities, requiring extensive use of VFDs in HVAC and water management systems. Additionally, partnerships with domestic manufacturers, such as Delta Electronics, bolster supply chain resilience.

Japan

Japan VFD market growth is anticipated with the expertise in advanced automation technologies, particularly in automotive and electronics manufacturing. For instance, Toyota and Sony utilize VFDs extensively in production lines, enhancing precision and energy efficiency. Government initiatives play a pivotal role. According to the Ministry of Economy, Trade, and Industry, Japan plans to invest $5 billion in sustainable manufacturing by 2025, focusing on eco-friendly technologies. Collaborations with global players like Mitsubishi Electric ensure access to cutting-edge systems.

South Korea

South Korea VFD market growth is significantly growing with the electronics and semiconductor sectors. For example, Samsung and SK Hynix rely heavily on VFDs for automated assembly lines, driving regional demand. Government support further amplifies growth. According to the Ministry of Trade, Industry, and Energy, investments in smart manufacturing have increased by 25% since 2020, ensuring access to advanced technologies. Collaborations with domestic players like LS Electric bolster supply chain resilience.

Australia & New Zealand

Australia and New Zealand VFD market growth is likely to grow with its focus on sustainable practices and renewable energy projects. For instance, Australia’s solar farms, valued at over $20 billion annually, rely heavily on VFDs for motor control in tracking systems. Government initiatives further amplify growth. According to the Department of Industry, Science, and Resources, subsidies for green energy projects have increased by 20% since 2020, encouraging the adoption of energy-efficient technologies. Collaborations with global players like Schneider Electric ensure access to cutting-edge systems.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Major Players in the Asia Pacific VFD Market include ABB Ltd., Siemens AG, Schneider Electric SE, Danfoss Group, Rockwell Automation Inc., Mitsubishi Electric Corporation, Fuji Electric Co. Ltd., Hitachi Ltd., Yaskawa Electric Corporation, Toshiba International Corporation, Delta Electronics Inc., WEG S.A.

The Asia Pacific VFD market is characterized by intense competition, driven by the presence of global giants and regional players vying for dominance. Established companies like ABB, Siemens, and Schneider Electric leverage their technological expertise and extensive distribution networks to maintain its dominance. Meanwhile, local manufacturers compete aggressively on pricing, offering cost-effective solutions tailored to budget-conscious customers. The market’s competitive landscape is further shaped by rapid technological advancements and government initiatives aimed at boosting domestic manufacturing capabilities. To differentiate themselves, players focus on innovation, introducing cutting-edge products for energy efficiency and smart manufacturing. Sustainability initiatives, such as low-emission designs, are also gaining traction amid stricter environmental regulations. Collaborations with governments and participation in mega-projects further promote the strategic maneuvers undertaken by key participants.

TOP PLAYERS IN THE MARKET

ABB Ltd.

ABB Ltd. is a key player in the Asia Pacific variable frequency drive market with its innovative and energy-efficient solutions. The company specializes in AC drives, catering to industries like water management, HVAC, and manufacturing. Recently, ABB launched its "ACS880" series of IoT-enabled VFDs, aligning with the region’s push toward smart manufacturing. To strengthen its presence, ABB expanded its R&D centers in India and China, fostering closer collaborations with local manufacturers. Additionally, partnerships with renewable energy firms ensure the adoption of its advanced drives in solar and wind projects.

Siemens AG

Siemens AG plays a pivotal role in the Asia Pacific VFD market by offering cutting-edge solutions for high-performance applications. Its SINAMICS series is widely used in automotive, textiles, and food processing industries due to superior precision and durability. Recently, Siemens established a new digitalization hub in Singapore to enhance product customization for regional markets. The company also partnered with Hyundai Heavy Industries to supply VFDs for automated production lines, driving demand in South Korea’s manufacturing sector.

Schneider Electric

Schneider Electric is a dominant force in the Asia Pacific VFD market, particularly in HVAC and industrial automation applications. Its Altivar series is widely adopted for energy-efficient motor control in commercial buildings and factories. Recently, Schneider introduced its "EcoStruxure" platform, enabling real-time monitoring and predictive maintenance for VFDs. The company also expanded its distribution network in Southeast Asia, enhancing accessibility for customers. Collaborations with logistics firms in Malaysia and Thailand further solidify its position.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the Asia Pacific VFD market employ diverse strategies to maintain their competitive edge. Innovation and R&D investments rank among the most prominent approaches, with companies developing IoT-enabled and energy-efficient drives. Strategic partnerships and collaborations are also widely adopted, enabling firms to tap into emerging markets and secure contracts for large-scale projects. Localization efforts, such as establishing regional manufacturing hubs, reduce costs and improve supply chain resilience. Sustainability-focused measures, such as developing eco-friendly drives, further strengthen market positioning. After-sales services, including predictive maintenance and operator training, play a pivotal role in fostering customer loyalty and driving repeat business.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, ABB Ltd. launched its "ACS880" series of IoT-enabled VFDs in India by enhancing energy efficiency for industrial applications.

- In May 2023, Siemens AG inaugurated a new digitalization hub in Singapore, which is focusing on customizing VFDs for regional smart manufacturing projects.

- In July 2023, Schneider Electric expanded its distribution network in Thailand by increasing accessibility for industrial and commercial customers.

- In September 2023, Delta Electronics partnered with Indian renewable energy firms to supply VFDs for solar-powered irrigation system, which is targeting agricultural modernization.

- In November 2023, Mitsubishi Electric introduced its "FR-A800" series of AI-driven VFDs in Japan, enabling real-time fault detection and predictive maintenance for industrial motors.

MARKET SEGMENTATION

This research report on the Asia Pacific variable frequency drive market has been segmented and sub-segmented based on product type, application, and region.

By Product Type

- AC Drives

- Servo Drives

By Application

- Pumps

- HVAC

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What is a variable frequency drive (VFD)?

A VFD is an electronic device that controls the speed and torque of electric motors by varying the frequency and voltage supplied.

2. Which industries use variable frequency drives in Asia-Pacific?

Key industries include manufacturing, oil & gas, water treatment, HVAC, and mining.

3. What factors are driving the Asia-Pacific VFD market?

Industrial automation, energy efficiency needs, and infrastructure development are major drivers.

4. Which countries lead the Asia-Pacific VFD market?

China, Japan, India, and South Korea are major markets.

5. What are the main types of VFDs?

AC drives, DC drives, and servo drives are the main categories.

6. Who are the major players in the Asia-Pacific VFD market?

Key companies include ABB, Siemens, Schneider Electric, Mitsubishi Electric, and Yaskawa.

7. Which power range segments are common in the VFD market?

Low-voltage, medium-voltage, and high-voltage VFDs serve different applications.

8. What challenges does the VFD market face in Asia-Pacific?

High initial costs, technical complexities, and fluctuating raw material prices.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com