Asia Pacific Video Management Software Market Size, Share, Trends & Growth Forecast Report By Component (System Segment, Services Segment), Technology, Mode Of Deployment, End User, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore And Rest Of Asia-Pacific), Industry Analysis From 2025 To 2033

Asia Pacific Video Management Software Market Size

The Asia Pacific Video Management Software Market size was calculated to be USD 0.85 billion in 2024 and is anticipated to be worth USD 4.21 billion by 2033, from USD 1.02 billion in 2025, growing at a CAGR of 19.40% during the forecast period.

The Asia Pacific video management software (VMS) market refers to the ecosystem of digital platforms designed for centralized control, monitoring, storage, and analysis of video surveillance data across various sectors. These solutions are instrumental in enabling real-time security management, operational efficiency, and compliance with regulatory requirements. VMS is increasingly integrated with advanced technologies such as artificial intelligence (AI), machine learning, and cloud computing to enhance functionality beyond traditional surveillance.

MARKET DRIVERS

Urbanization and Smart City Initiatives Across Asia Pacific

One of the most significant drivers fueling the Asia Pacific video management software (VMS) market is the rapid pace of urbanization combined with large-scale smart city programs. Countries like India, China, Singapore, and Japan are investing heavily in transforming their urban landscapes into intelligent ecosystems that leverage digital infrastructure for enhanced security, mobility, and governance. According to the Asian Development Bank, a potential portion of the global urban population will reside in Asia by 2050, necessitating scalable surveillance and monitoring solutions. India's Smart Cities Mission, launched in 2015, aims to develop 100 cities through technology-driven infrastructure and public services. In this context, video surveillance networks equipped with VMS have become integral to traffic management, crime prevention, and emergency response systems. Moreover, government mandates and rising concerns around public security are pushing municipalities to install thousands of cameras linked to unified VMS platforms. The integration of cloud-based video management systems allows seamless scalability and remote access, aligning perfectly with the evolving needs of urban centers across the region.

Increasing Adoption of AI and Analytics-Driven Surveillance Systems

Another pivotal driver propelling the Asia Pacific video management software (VMS) market is the growing integration of artificial intelligence (AI) and advanced video analytics within surveillance frameworks. Organizations across industries—including banking, retail, manufacturing, and logistics—are increasingly deploying AI-enhanced VMS solutions to derive actionable insights from visual data beyond basic security functions. Similarly, major retailers are using VMS platforms embedded with behavior recognition algorithms to understand consumer patterns and optimize store layouts. As per the study, AI-integrated surveillance solutions have improved incident detection accuracy by up to 70% in high-footfall commercial zones. In addition, governments across Southeast Asia are leveraging facial recognition and license plate recognition technologies in conjunction with VMS to enhance law enforcement capabilities. Malaysia’s national CCTV network utilizes AI-driven analytics for real-time threat detection.

MARKET RESTRAINTS

High Initial Deployment Costs and Infrastructure Challenges

Despite the growing demand for video management software (VMS) across the Asia Pacific region, one of the primary restraints remains the high initial cost of deployment, particularly in developing economies. Implementing a comprehensive VMS solution requires substantial investment in hardware, software licensing, cloud infrastructure, and skilled personnel. According to Gartner, the average capital expenditure for setting up a mid-sized enterprise-level VMS system in emerging markets exceeds $150,000, which can be prohibitive for small and medium-sized businesses.

This financial burden is further exacerbated by inadequate IT infrastructure in certain regions. Countries like Vietnam, Indonesia, and the Philippines face challenges related to inconsistent internet connectivity and outdated networking systems, which hinder the smooth operation of cloud-based VMS platforms. As per the World Bank, only a certain percentage of the population in the ASEAN region had reliable broadband access, limiting the scalability of remotely managed video surveillance solutions.

Moreover, the integration of legacy surveillance systems with modern VMS platforms often demands additional retrofitting costs, discouraging widespread adoption. Public sector organizations, despite recognizing the necessity of upgraded surveillance mechanisms, frequently encounter budgetary constraints that delay procurement processes.

Regulatory Complexities and Data Privacy Concerns

A significant barrier impeding the growth of the Asia Pacific video management software (VMS) market is the evolving landscape of data privacy regulations and surveillance-related legal restrictions. Governments across the region are increasingly scrutinizing the use of video surveillance due to concerns over civil liberties, data misuse, and unauthorized monitoring. For example, in Australia, the Office of the Australian Information Commissioner has mandated strict compliance with the Privacy Act 1988, requiring organizations to ensure transparency and accountability in how video data is collected and stored. Similarly, in India, the absence of a comprehensive federal data protection law has led to a fragmented regulatory environment, causing hesitation among enterprises to fully adopt VMS solutions without clear compliance guidelines. As per PwC, 58% of Indian companies surveyed in 2023 delayed or modified their surveillance strategies due to uncertainty around data governance norms. Consequently, AI-powered VMS installations that employ facial recognition must adhere to strict consent protocols, slowing down adoption in commercial applications.

MARKET OPPORTUNITIES

Expansion of Cloud-Based Video Management Platforms

A rapidly emerging opportunity in the Asia Pacific video management software (VMS) market is the shift toward cloud-based deployment models. Traditional on-premise VMS systems require significant capital investment in servers, storage units, and maintenance, whereas cloud-based alternatives offer scalable, subscription-driven solutions that reduce upfront costs and improve accessibility. China leads this transition, with major tech firms like Alibaba Cloud and Huawei promoting hybrid cloud-video surveillance architectures tailored for both government and enterprise clients. Alibaba Cloud reported a 60% year-on-year growth in cloud-based VMS subscriptions in 2023, largely attributed to the rise of smart retail and logistics automation. Similarly, in Australia, government agencies are migrating legacy surveillance systems to cloud environments to support real-time data access across multiple locations. Further, telecom operators in India and Thailand are partnering with VMS vendors to offer bundled cloud surveillance packages, lowering entry barriers for SMEs. The integration of 5G networks enhances this trend by enabling faster data transmission and reduced latency, ensuring seamless video streaming and analytics processing.

Integration of Edge Computing and Real-Time Analytics

Another transformative opportunity shaping the Asia Pacific video management software (VMS) market is the convergence of edge computing and real-time analytics within surveillance systems. Unlike conventional centralized architectures, edge-based VMS solutions process video data locally at the camera level reducing bandwidth consumption and enhancing responsiveness. South Korea is spearheading this shift, particularly in the industrial and transportation sectors. Similarly, Japanese manufacturers are embedding edge AI chips into surveillance cameras to monitor production lines in real-time, reducing defect rates and downtime. Beyond industrial applications, retail chains in Singapore and Malaysia are leveraging edge analytics to analyze foot traffic and customer behaviors instantaneously, allowing for dynamic store management.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Video Surveillance Networks

One of the foremost challenges confronting the Asia Pacific video management software (VMS) market is the escalating risk of cyberattacks targeting surveillance infrastructure. As VMS systems become increasingly interconnected through IP-based networks and cloud platforms, they expose critical vulnerabilities that malicious actors can exploit. According to Kaspersky Lab, there was a 40% year-over-year increase in cyber incidents involving video surveillance systems in the Asia Pacific region in 2023, with ransomware and unauthorized access being the most common threats. In India, a high-profile breach in 2022 compromised over 1,000 surveillance cameras used by state police departments, noting the fragility of digital security protocols in public-sector VMS deployments. Also, 62% of surveyed enterprises in APAC identified cybersecurity as a top concern when evaluating VMS vendors. The proliferation of low-cost, poorly secured Internet of Things (IoT) cameras in residential and SME deployments further exacerbates the issue. Many of these devices lack firmware updates and encryption standards, making them easy targets for botnet attacks.

Fragmented Standards and Interoperability Issues in Surveillance Technologies

A persistent challenge hindering the uniform growth of the Asia Pacific video management software (VMS) market is the lack of standardized protocols and interoperability between different surveillance technologies. The region's diverse vendor ecosystem, coupled with varying national regulations, results in fragmented deployment environments where VMS platforms struggle to seamlessly integrate with third-party hardware and software components. In China, despite a vast installed base of surveillance equipment, inconsistencies between proprietary VMS architectures from domestic vendors such as Hikvision and Dahua limit cross-platform operability. This forces municipal authorities to invest in redundant systems rather than achieving a truly converged command center. Similarly, in Japan, government agencies face difficulties integrating legacy analog systems with newer IP-based solutions due to mismatched encoding formats and communication protocols.

Southeast Asian countries like Thailand and Vietnam encounter additional complications stemming from the import of surveillance equipment from multiple global vendors, each adhering to different technical standards. As per the International Electrotechnical Commission, the absence of universally accepted open-source frameworks for VMS interoperability delays large-scale smart city integrations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 19.40% |

| Segments Covered | By Component, Technology, Mode of Deployment, End User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of Asia-Pacific |

| Market Leaders Profiled | Milestone Systems, Genetec Inc., Honeywell International Inc., Axis Communications, Bosch Security Systems, Panasonic Corporation, Huawei Technologies Co., Ltd., Hikvision Digital Technology Co., Ltd., Dahua Technology, Hanwha Vision, VIVOTEK Inc., March Networks, Verint Systems Inc., Qognify |

SEGMENTAL ANALYSIS

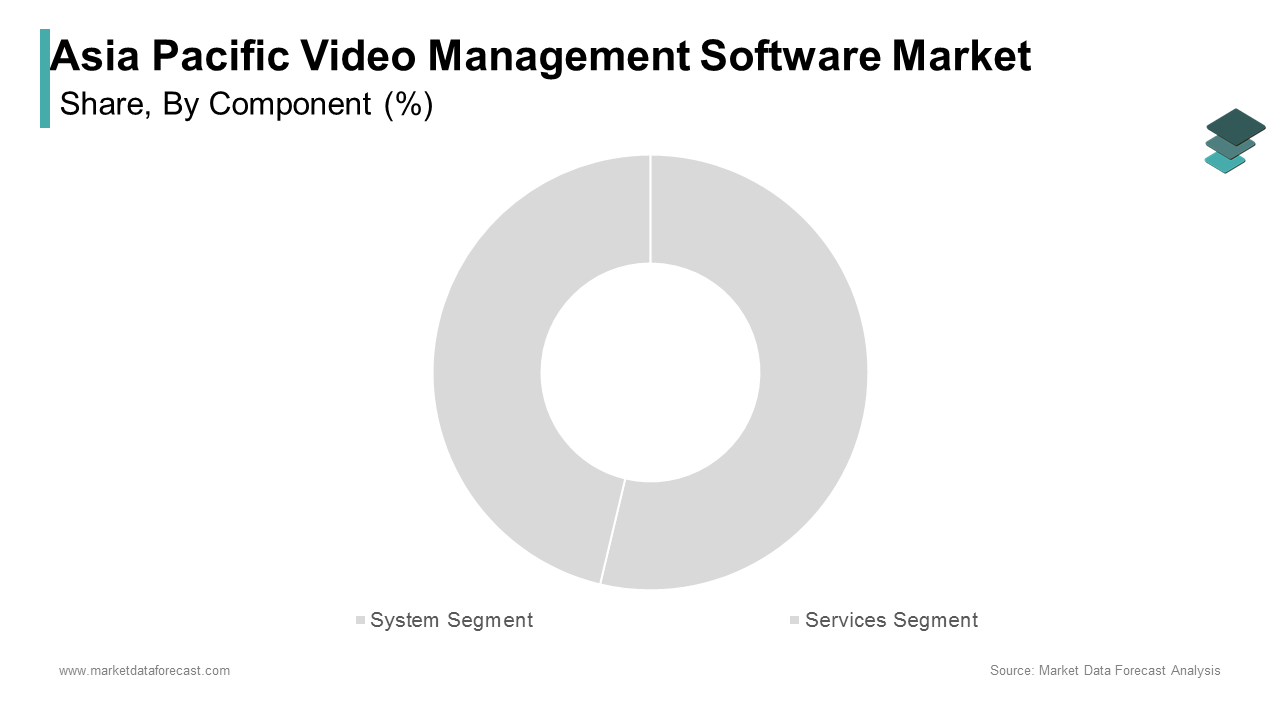

By Component Insights

The system segment spearheaded the Asia Pacific weight management market with 62.7% of total revenue in 2024. This segment includes hardware such as digital weighing scales, body composition analyzers, connected wearables, and integrated platforms used across healthcare facilities, fitness centers, and home settings. Also, one major driver behind this dominance is the rising prevalence of obesity and chronic diseases linked to weight gain, especially in emerging economies like India, China, and Indonesia. The World Health Organization (WHO) reported that over 150 million adults in the Western Pacific Region were obese in 2023, spurring demand for precision monitoring systems. In addition, government initiatives promoting preventive healthcare have led to the widespread integration of advanced weight-tracking systems in public clinics and hospitals. In Japan, for instance, the Ministry of Health, Labour and Welfare mandates regular health screenings, including BMI checks, which has significantly increased the deployment of clinical-grade weight management systems. Moreover, smart technology integration —such as IoT-enabled scales and AI-based analytics—is gaining traction among consumers and healthcare providers.

The services segment is the fastest-growing component within the Asia Pacific weight management market, projected to grow at a CAGR of 17.8% between 2025 and 2033. This involves consulting, remote monitoring services, training, and maintenance related to weight management technologies. A key aspect is the growing outsourcing of technical and operational support by healthcare providers and fitness centers, particularly in countries like Australia, South Korea, and Singapore. These nations are investing heavily in telehealth infrastructure, where service-based solutions play a critical role in managing patient weight metrics remotely.

Another propellant is the rise of personalized health coaching and digital wellness programs. Platforms like CureFit, Noom, and NutriSmart have gained popularity in urban APAC markets, often bundling their software tools with professional guidance services.

Furthermore, increased insurance coverage for wellness services in countries like Australia and New Zealand is encouraging more individuals to opt for structured weight management plans. Private insurers in these regions now cover services such as dietitian consultations and behavioral therapy which were previously considered out-of-pocket expenses.

By Technology Insights

The analog-based segment held the largest share of the Asia Pacific weight management market, estimated at 58.2% in 2024. Although analog systems lack the connectivity and real-time features of modern digital alternatives, they remain widely used in rural and semi-urban areas due to affordability and ease of use. Moreover, a primary reason for their continued dominance is strong uptake in low-income and middle-income countries across Southeast Asia and parts of South Asia. Organizations like the WHO highlight that nearly 60% of India's population resides in rural areas, where access to high-speed internet and digital literacy remains limited. As a result, analog systems remain the go-to solution in local clinics and government-run health centers. Another important aspect is the legacy infrastructure still in use, particularly in public healthcare systems across the region. For example, in the Philippines, the Department of Health reported in 2023 that more than 40% of its primary care facilities still rely on traditional weighing mechanisms due to budget constraints and a lack of trained personnel for handling complex digital systems.

In addition, cost-effectiveness plays a major role. Analog devices are typically priced lower than their IP-based counterparts, making them attractive for price-sensitive users.

The IP-based segment is the swiftest expanding, anticipated to move forward at a CAGR of 20.3% through 2033. It is driven by increasing digitization, smart city projects, and the expansion of connected health ecosystems across the region. One of the main catalysts is the booming adoption of IoT and cloud-connected devices in the healthcare sector. Countries like South Korea and Singapore are leading the charge, with national strategies promoting digital health records and remote patient monitoring. Further, the influential factor is the growth of wearable technology and mobile health apps, which increasingly incorporate IP-based sensors for real-time body metrics. Lastly, enterprise-level investments in employee wellness programs in large corporations across Japan, Australia, and India are accelerating the employment of IP-based systems.

By Mode Of Deployment Insights

The on-premise deployment model remained the prominent mode, capturing an estimated 55.5% of the Asia Pacific weight management market in 2024. This preference stems largely from concerns regarding data privacy and security, particularly in regulated sectors like healthcare and government facilities. Many APAC countries, including China and India, enforce stringent local data storage regulations, compelling organizations to host sensitive health information on internal servers rather than in the cloud. The Personal Data Protection Act (PDPA) in Singapore and the Cybersecurity Law of China both emphasize localized control, reinforcing the appeal of on-premise solutions.

Moreover, established healthcare institutions prefer on-site infrastructure due to existing IT investments and compatibility issues with legacy systems. In Japan, for example, the Ministry of Economy, Trade and Industry found that over 60% of public hospitals favored on-premise deployments for critical health applications, citing better control and compliance with national standards.

In rural or disconnected environments, a lack of consistent internet access also makes on-premise setups more practical.

Cloud-based deployment is growing at the highest rate, expected to achieve a CAGR of 22.5% between 2024 and 2030. This is primarily due to scalability, cost savings, and improved accessibility offered by cloud-native platforms. One pivotal growth driver is the expansion of telemedicine and virtual clinics, especially post-pandemic. By mid-2024, over 350 million digital health IDs had been issued, many tied to cloud-enabled wellness dashboards.

Simultaneously, increased smartphone penetration and rising mobile app usage are facilitating broader access to cloud-based health services. According to We Are Social’s 2024 Global Digital Report, APAC accounts for 60% of global mobile internet users, creating fertile ground for cloud-integrated weight management applications.

Also, SaaS-based wellness platforms are becoming popular among SMEs and fitness studios due to minimal upfront costs and flexible subscription models.

By End-User Industry Insights

The healthcare sector accounted for the biggest share, standing at 38.8% of the market in 2024. It is primary health centers heavily utilize weight management tools to monitor patient health, manage chronic conditions, and assist in preventive care. This dominance is underpinned by rising chronic disease burden, particularly diabetes and hypertension, which are closely linked to weight anomalies. In China, over 120 million people suffer from diabetes, necessitating routine weight and body composition assessments. Public health campaigns such as India’s National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases and Stroke (NPCDCS) have institutionalized weight screening in community health settings, further driving device adoption.

Moreover, electronic medical record (EMR) integration is pushing healthcare providers to procure standardized, interoperable weight management systems.

The retail sector is emerging as the rapidly growing end-user industry, projected to grow at a CAGR of 26% which is fueled by the rise of wellness-focused consumerism and personalized nutrition trends. Major retailers and pharmacy chains across APAC are incorporating in-store body composition kiosks and smart weighing stations, enabling shoppers to check their health metrics while purchasing supplements or fitness products. In Australia, Chemist Warehouse introduced interactive health zones featuring weight and BMI evaluation tools, attracting millions of users annually. E-commerce giants are also partnering with health-tech startups to offer AI-powered weight assessment tools on shopping apps, blending commerce with personalization. Lastly, corporate wellness programs rolled out by large retailers are contributing to this trend.

SEGMENTAL ANALYSIS

China held the largest share in the Asia Pacific video management software (VMS) market, estimated at 35.5% in 2024. As the most populous nation and a global manufacturing and surveillance technology hub, China has aggressively adopted smart city initiatives, public safety programs, and AI-powered surveillance systems. The government’s push toward national security and urban digitization has driven extensive deployment of VMS across cities like Shenzhen, Shanghai, and Beijing. Domestic giants like Hikvision and Dahua dominate both domestic and international markets, further fueling local VMS demand. Moreover, increasing cyber threats and the need for advanced threat detection have intensified adoption across sectors such as banking, transportation, and defense. This exponential growth in camera density directly correlates with the rising demand for video management solutions that can process, store, and analyze vast amounts of visual data.

REGIONAL ANALYSIS

Japan is a mature and technologically advanced market. The immature digital landscape, an aging population, and high-level technological adoption form the foundation of consistent VMS growth.

According to Japan's Ministry of Internal Affairs and Communications, over 95% of large commercial buildings in major cities like Tokyo and Osaka now use some form of centralized video surveillance system. In addition, Japan’s police force uses more than 80,000 surveillance cameras nationwide, many of which are linked via VMS for facial recognition and crowd monitoring, particularly in subway stations and airports. Innovation is another key driver.

India is growing rapidly due to massive urban infrastructure projects and increasing security concerns. The Indian government has launched multiple smart city missions, including the Smart Cities Mission, aimed at developing 100 technologically advanced urban centers. These efforts have led to the widespread installation of IP-based surveillance systems integrated with VMS platforms. According to the National Crime Records Bureau (NCRB), crime rates in urban areas rose by over 7% in 2023, prompting cities like Delhi, Mumbai, and Bengaluru to enhance their surveillance networks. Private sector participation is also accelerating. Real estate developers, shopping malls, and banks are increasingly adopting cloud-based VMS systems for real-time monitoring and remote access. In addition, the Digital India initiative has boosted broadband penetration and 4G/5G connectivity, enabling seamless transmission and storage of video data.

Australia and New Zealand are seeing a strong regulatory push and public safety focus which is reflecting their strong regulatory environment and proactive approach to public safety. Both nations have well-established privacy laws and data protection frameworks that encourage responsible use of surveillance technologies, while still promoting adoption across critical sectors. In Australia, the NSW Government’s Safe Cities Program invested AUD 120 million (approx. USD 80 million) in expanding city-wide surveillance networks between 2020 and 2023.

New Zealand, though smaller in scale, follows a similar trend. After the Christchurch mosque attacks in 2019, the government introduced stricter security protocols, resulting in increased deployment of VMS in religious institutions, schools, and public spaces. According to Stats NZ, the number of registered surveillance systems increased by over 20% between 2021 and 2023.

Cloud-based VMS adoption is also growing rapidly in ANZ, driven by enterprises seeking scalable, secure, and cost-effective solutions.

South Korea has smart infrastructure and tech innovation catalysts and is driven by its globally recognized leadership in digitization, smart infrastructure, and tech innovation. Seoul, Busan, and Incheon are among the most surveilled cities globally, supported by the Korean government’s U-City program, which integrates surveillance, IoT, and AI technologies into city planning.

South Korean companies like Hanwha Techwin and IDIS are major players in the global VMS ecosystem, offering cutting-edge solutions tailored for retail, healthcare, and logistics. Moreover, the rise of hybrid cloud architectures enables businesses to maintain data sovereignty while benefiting from cloud scalability.

Cybersecurity concerns and rising incidents of public disorder have also prompted new legislation mandating enhanced surveillance in schools, financial institutions, and transit hubs.

LEADING PLAYERS IN THE ASIA PACIFIC VIDEO MANAGEMENT SOFTWARE MARKET

Hikvision

Hikvision is a dominant force in the Asia Pacific video management software (VMS) market, offering a comprehensive portfolio of intelligent surveillance solutions tailored for diverse industries such as transportation, retail, and public safety. The company’s VMS platform integrates advanced technologies like AI-powered analytics, cloud-based storage, and edge computing capabilities, enabling real-time decision-making and enhanced security. In the global market, Hikvision has established itself as a benchmark for innovation and reliability, with its solutions deployed across multiple continents.

Dahua Technology

Dahua Technology plays a pivotal role in shaping the Asia Pacific VMS landscape through its cutting-edge software that supports high-definition video processing, smart analytics, and hybrid deployment models. Known for its open-platform approach, Dahua enables seamless integration with third-party hardware and software systems, enhancing interoperability across different infrastructure environments. Globally, the company has expanded its reach by forging alliances with regional distributors and system integrators, ensuring widespread adoption beyond Asia. Dahua's commitment to cybersecurity and data privacy has further strengthened its credibility, making it a trusted brand among both private and public sector organizations requiring secure, scalable video management solutions.

Hanwha Techwin

Hanwha Techwin stands out in the Asia Pacific VMS market due to its focus on delivering high-performance video analytics and AI-enhanced surveillance tools. The company’s Wisenet VMS platform supports large-scale deployments and offers features such as facial recognition, behavior analysis, and predictive threat detection. Hanwha has contributed significantly to global standards in smart city initiatives and industrial automation by integrating its VMS with IoT and cloud technologies. Its emphasis on user-centric design and ease of integration has made it a preferred choice for medium and large enterprises looking to upgrade their security frameworks.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading players in the Asia Pacific video management software market is product innovation and feature enhancement. Companies continuously invest in research and development to integrate emerging technologies such as artificial intelligence, machine learning, and computer vision into their platforms. These advancements enable more accurate analytics, real-time monitoring, and automated decision-making, which are highly valued by enterprise clients.

Another key strategy is strategic partnerships and ecosystem collaboration. VMS vendors are increasingly forming alliances with hardware manufacturers, telecom providers, and cloud service companies to offer bundled solutions that meet evolving customer needs. These collaborations help in expanding market reach and improving compatibility across different technology stacks.

Lastly, regional expansion and localized offerings play a crucial role in strengthening market presence. Companies are tailoring their products to comply with local regulations and address specific security concerns in different countries.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the Asia Pacific video management software (VMS) market include Milestone Systems, Genetec Inc., Honeywell International Inc., Axis Communications, Bosch Security Systems, Panasonic Corporation, Huawei Technologies Co., Ltd., Hikvision Digital Technology Co., Ltd., Dahua Technology, Hanwha Vision, VIVOTEK Inc., March Networks, Verint Systems Inc., Qognify.

The competitive landscape of the Asia Pacific video management software (VMS) market is marked by a mix of established global leaders and rapidly growing regional players. As demand for intelligent surveillance grows across sectors such as public safety, retail, banking, and transportation, companies are intensifying their efforts to differentiate themselves through technological innovation and strategic positioning. The market sees strong competition from vendors who are not only vying for dominance in core markets like China and Japan but are also aggressively expanding into emerging economies such as India, Indonesia, and Vietnam. While international giants leverage their vast R&D capabilities and global experience, domestic firms benefit from localized insights and regulatory familiarity. This dynamic creates a dual-layered competition where scale, adaptability, and product sophistication determine leadership positions. Also, rising cybersecurity threats and compliance requirements are pushing vendors to enhance the security features of their platforms, further intensifying the race for differentiation and market share.

RECENT HAPPENINGS IN THE MARKET

- In January 2024, Hikvision launched an updated version of its VMS platform integrated with generative AI capabilities for anomaly detection and predictive analytics. This move was aimed at enhancing situational awareness for large-scale security operations across urban centers in the Asia Pacific region.

- In March 2024, Dahua Technology announced a strategic partnership with a leading cloud infrastructure provider to expand its SaaS-based VMS offerings. The collaboration enabled Dahua to deliver scalable, subscription-driven video management solutions tailored for small and medium-sized businesses in Southeast Asia.

- In June 2024, Hanwha Techwin introduced a new AI-powered video analytics module designed specifically for smart retail applications. This enhancement allowed retailers to gain deeper insights into customer behavior while maintaining compliance with privacy regulations.

- In September 2024, NEC Corporation deployed its facial recognition-integrated VMS solution across several transportation hubs in Japan, reinforcing its position in the public safety segment and demonstrating its commitment to next-generation surveillance technologies.

- In November 2024, Bosch Security Systems expanded its regional headquarters in Singapore to accommodate increased demand for hybrid cloud VMS solutions. The facility supports localized R&D, customer support, and training programs, strengthening Bosch’s presence in the Asia Pacific market.

MARKET SEGMENTATION

This research report on the Asia Pacific Video Management Software Market has been segmented and sub-segmented based on component, technology, mode of deployment, end user, and region.

By Component

- System Segment

- Services Segment

By Technology

- Analog-Based Systems

- IP-Based Systems

By Mode of Deployment

- On-Premise Deployment

- Cloud Deployment

By End User

- Healthcare

- Retail

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What is driving the growth of the VMS market in Asia Pacific?

Key drivers include increasing security concerns, rapid urbanization, growth in smart city initiatives, and the rising adoption of IP-based video surveillance systems.

2. Which industries are the primary users of VMS in the Asia Pacific region?

Major industries include government, transportation, banking and finance, retail, healthcare, education, and manufacturing.

3. How is cloud technology influencing the VMS market?

Cloud-based VMS solutions are gaining popularity due to benefits like remote access, scalability, reduced infrastructure cost, and ease of maintenance.

4. Who are the major players in the Asia Pacific VMS market?

Leading players include Milestone Systems, Genetec Inc., Honeywell, Axis Communications, Hikvision, Dahua Technology, and Hanwha Vision.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com