Asia Pacific Welding Consumables Market Size, Share, Trends & Growth Forecast Report By Type (Electrodes, Flux, Shielding Gas, Filler Metals, Others), Welding Technique, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore And Rest Of Asia-Pacific), Industry Analysis From 2025 To 2033

Asia Pacific Welding Consumables Market Size

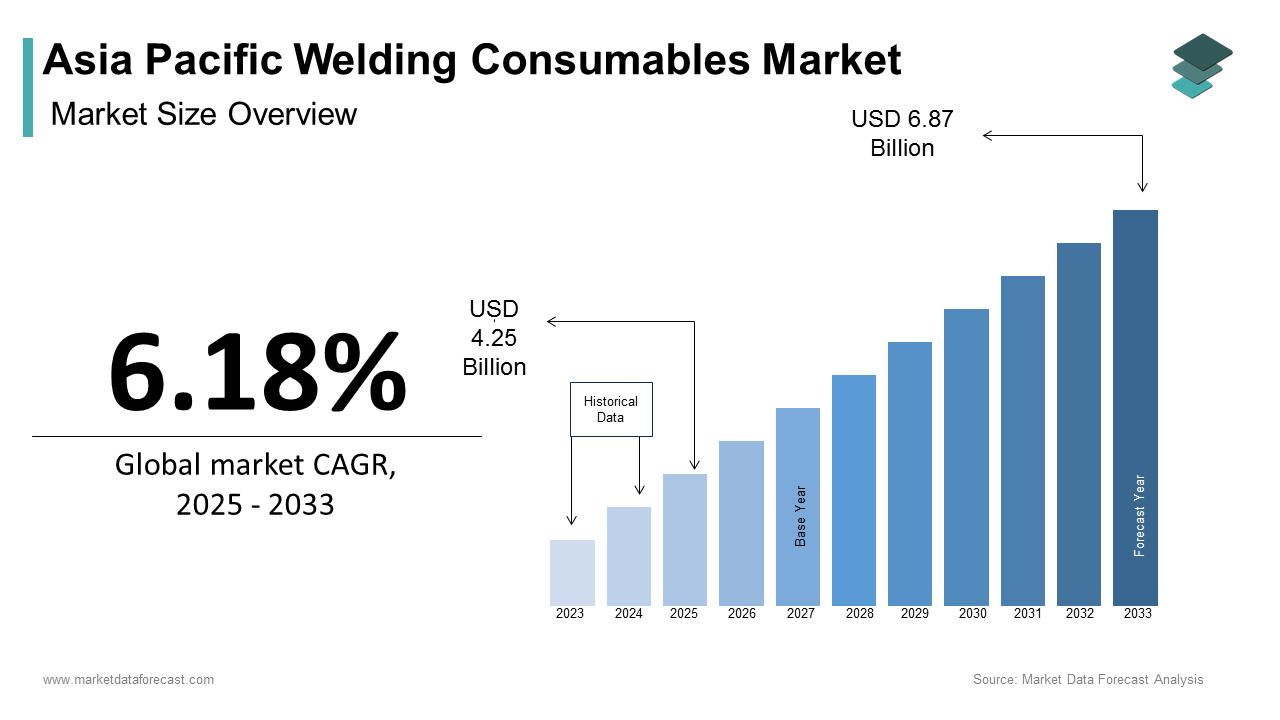

The Asia Pacific welding consumables market size was calculated to be USD 4.01 billion in 2024 and is anticipated to be worth USD 6.87 billion by 2033, from USD 4.25 billion in 2025, growing at a CAGR of 6.18% during the forecast period.

The welding consumables are critical in ensuring structural integrity across sectors such as construction, automotive, energy, and shipbuilding. The region has emerged as a global manufacturing hub, significantly driving demand for welding consumables. Countries like China, India, Japan, and South Korea are at the forefront of this growth due to rapid urbanization and infrastructural development. For instance, India's National Infrastructure Pipeline aims to invest nearly USD 1.4 trillion between 2020 and 2025, directly influencing the need for durable welding solutions. Moreover, regulatory emphasis on quality control and safety standards in manufacturing processes shapes product specifications and application methods. As per the International Institute of Welding, the adoption of advanced welding techniques in the region is growing at an annual rate of approximately 4%, driven by automation trends and skilled workforce development initiatives.

MARKET DRIVERS

Growth in Shipbuilding and Maritime Industries

One of the key drivers propelling the Asia Pacific welding consumables market is the robust expansion of the shipbuilding and maritime industries. Countries such as South Korea, China, and Japan collectively dominate global shipbuilding output by accounting for more than 90% of total new orders as reported by Clarksons Research. Shipbuilding is inherently labor and material-intensive, with large vessels requiring several tons of welding consumables during construction. For example, the average container vessel requires approximately 300–500 tons of welding wire alone, depending on size and design complexity. Additionally, rising defense spending in countries like India and Australia has spurred naval modernization programs, which include the construction of submarines, frigates, and aircraft carriers.

Expansion of Renewable Energy Infrastructure

Another significant driver for the Asia Pacific welding consumables market is the accelerated deployment of renewable energy infrastructure in wind and solar power. Governments across the region have committed to ambitious clean energy targets to reduce carbon emissions and enhance energy security. According to the International Renewable Energy Agency (IRENA), the Asia Pacific accounted for nearly half of global renewable energy capacity additions in 2023, with China and India leading the charge.

Wind energy projects, especially offshore installations, require extensive use of welding consumables for tower segments, turbine foundations, and support structures. For instance, China's National Energy Administration reported that the country added over 7 GW of offshore wind capacity in 2023 alone, surpassing Europe to become the world leader in this domain. Each offshore wind turbine typically uses around 150–200 tons of structural steel, much of which undergoes welding during fabrication and installation.

India has ramped up its offshore wind ambitions by targeting 30 GW of installed capacity by 2030 under its National Offshore Wind Energy Policy. Such initiatives directly boost demand for high-strength, corrosion-resistant welding materials suited for harsh environmental conditions. Given the long-term outlook for green energy expansion, the welding consumables market is well-positioned to benefit from sustained investment in these sectors.

MARKET RESTRAINTS

Fluctuations in Raw Material Prices

A major restraint affecting the Asia Pacific welding consumables market is the volatility in raw material prices for steel, nickel, and copper. These metals constitute a substantial portion of welding electrode and wire production costs. Over the past few years, global commodity markets have experienced significant price swings due to geopolitical tensions, trade restrictions, and supply chain disruptions. Such fluctuations make cost forecasting difficult for manufacturers and often lead to inconsistent pricing for end-users. In China, one of the largest consumers of welding consumables, steel prices saw a year-on-year increase of 18% in mid-2023, as reported by the China Iron and Steel Association, directly impacting production margins for consumable suppliers. Additionally, import dependencies in countries like India and Indonesia expose local producers to exchange rate risks and freight cost variations.

Skilled Labor Shortage and Technical Expertise Gap

The growth of the Asia Pacific welding consumables market is driven by the persistent shortage of skilled labor and the lack of technical expertise in welding operations. Manual and semi-automated welding still account for a significant portion of industrial applications in SMEs and rural areas despite advancements in automation and robotic welding systems. According to the International Institute of Welding, Asia Pacific faces a deficit of over 1 million certified welders, with India and Southeast Asian nations experiencing acute shortages. In India, only about 30% of the welding workforce is formally trained, as reported by the Indian Institute of Welding. This skills gap leads to inconsistent weld quality, higher rework rates, and inefficient utilization of welding consumables, ultimately increasing operational costs for industries. The lack of skilled personnel not only hampers productivity but also limits the adoption of advanced welding technologies that require precision and adherence to international standards.

MARKET OPPORTUNITIES

Adoption of Digital Manufacturing and Smart Welding Technologies

One of the most promising opportunities in the Asia Pacific welding consumables market is the increasing adoption of digital manufacturing and smart welding technologies. There is a growing emphasis on integrating IoT-enabled equipment, real-time monitoring systems, and AI-based process optimization into welding operations. These advancements enhance efficiency, reduce material waste, and improve weld quality, thereby boosting demand for compatible consumables. In particular, China and South Korea are spearheading this transition through government-backed initiatives such as China's "Made in China 2025" and South Korea's "Smart Manufacturing Innovation Strategy." In Japan, companies like Panasonic and Fronius have introduced intelligent welding systems that optimize parameters based on real-time feedback, reducing spatter and improving deposition rates. These systems rely on specialized consumables that match their performance characteristics.

Rise of Electric Vehicle (EV) Manufacturing

The rapid expansion of electric vehicle (EV) manufacturing in the Asia Pacific region presents a significant opportunity for the welding consumables market. EV production involves extensive use of welding in battery pack assembly, chassis fabrication, and motor housing construction. Unlike traditional internal combustion engine vehicles, EVs require highly precise and lightweight welded components to enhance energy efficiency and structural integrity.

China, the world’s largest EV market, produced over 7 million electric vehicles in 2023, as reported by the China Association of Automobile Manufacturers. This surge in production has created a parallel demand for aluminum and high-strength steel welding consumables, which are essential for joining lightweight materials without compromising strength.

As automakers shift toward modular and scalable platforms optimized for electric propulsion, the demand for advanced welding consumables tailored for dissimilar metal joining and high-speed production lines is expected to grow steadily, offering lucrative prospects for market players in the region.

MARKET CHALLENGES

Environmental Regulations and Carbon Emission Norms

One of the primary challenges confronting the Asia Pacific welding consumables market is the tightening of environmental regulations and the imposition of stricter carbon emission norms. Governments across the region are increasingly focusing on sustainable manufacturing practices to align with global climate commitments, such as the Paris Agreement. These policies are compelling industries to reassess their production methodologies, including the types of welding consumables used. For instance, China’s Ministry of Ecology and Environment has mandated reductions in industrial emissions under its 14th Five-Year Plan, which includes tighter controls on particulate matter and volatile organic compound (VOC) emissions from manufacturing processes. Traditional welding techniques, particularly those involving flux-cored and stick welding, tend to produce higher levels of fumes and slag, making them subject to scrutiny. As a result, manufacturers are being pushed toward cleaner alternatives such as metal-cored wires and low-fume fluxes, which often come at a higher cost.

Intensifying Competition from Local and Regional Players

Intensifying competition from local and regional manufacturers poses a significant challenge to established players in the Asia Pacific welding consumables market. The presence of numerous small-scale producers, particularly in China, India, and Southeast Asia, has led to price wars and margin compression. These local firms often leverage lower labor and production costs to offer competitively priced products, undercutting multinational corporations.

Companies such as Tianjin Bridge Welding Materials Group and Shanghai Changji Welding Materials Co., Ltd. have expanded their market share rapidly by aligning with national infrastructure and manufacturing programs. Their ability to deliver localized service and customization has further strengthened their foothold. In India, the rise of indigenous brands like Thermax and Finar Industries has disrupted traditional supplier relationships in sectors such as construction and small-scale engineering. As per the Indian Institute of Metals, local manufacturers captured nearly 65% of the domestic welding consumables market by volume in 2023, leveraging aggressive pricing strategies and shorter supply chains.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.18% |

| Segments Covered | By Type, Welding Technique, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of Asia-Pacific |

| Market Leaders Profiled | Colfax Corporation, The Lincoln Electric Company, Air Liquide S.A., Tianjin Golden Bridge Welding Materials Group Co., Ltd., Kobe Steel Ltd., Hyundai Welding Co., Ltd., Panasonic Corporation, Illinois Tool Works Inc., Ador Welding Ltd., Fronius International GmbH |

SEGMENTAL ANALYSIS

By Type Insights

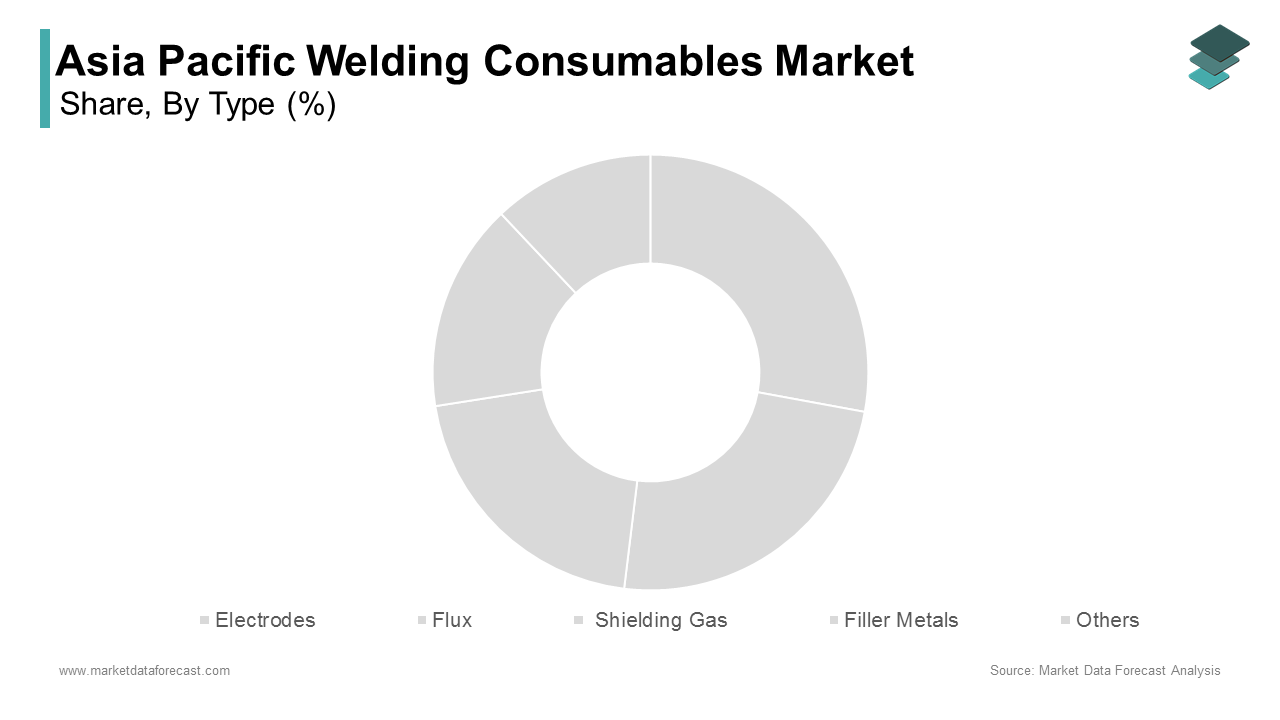

The filler metals segment was the largest and held 35.4% of the Asia Pacific welding consumables market share in 2024, with solid wires, flux-cored wires, and submerged arc wires, which are extensively used across industries such as construction, automotive, shipbuilding, and energy.

According to the China Welding Association, over 60% of industrial welding operations in China now utilize wire-based consumables due to their efficiency and consistency. In India, the government’s focus on infrastructure development under the National Infrastructure Pipeline has led to a surge in demand for steel structures, further boosting the consumption of filler wires. Additionally, the shipbuilding sector in South Korea and Japan heavily relies on flux-cored and solid wires for hull fabrication and engine room assembly. Clarksons Research reported that South Korea secured 38% of global shipbuilding orders in 2023, reinforcing the need for high-quality filler metals.

The shielding gases segment is swiftly emerging with a projected CAGR of 6.8% from 2025 to 2033, with the rising adoption of gas metal arc welding (GMAW) and gas tungsten arc welding (GTAW) in precision-dependent sectors such as electronics, aerospace, and electric vehicle manufacturing. In China, the expansion of the EV industry has significantly increased the demand for shielding gases like argon and carbon dioxide, which are essential for aluminum and thin-sheet welding applications. Japan’s push toward hydrogen economy initiatives has spurred the use of high-purity shielding gases in fuel cell stack assembly. As per the New Energy and Industrial Technology Development Organization (NEDO), Japan plans to deploy over 800,000 fuel cell vehicles by 2030, necessitating a steady supply of high-grade shielding gases.

By Welding Technique Insights

The arc welding segment held 42.3% of the Asia Pacific welding consumables market share in 2024 due to its extensive use in heavy industries such as shipbuilding, pipeline construction, and infrastructure development. According to the Japan Welding Society, more than 70% of welding operations in Japanese shipyards involve arc welding techniques due to their adaptability in both indoor and outdoor conditions. In India, where infrastructure projects are accelerating under the Smart Cities Mission and Bharatmala Pariyojana, SMAW continues to be the preferred choice among small and medium enterprises because of its minimal equipment requirements. Furthermore, the continued reliance on manual and semi-automated welding in Southeast Asian countries like Indonesia and Vietnam supports the sustained demand for arc welding consumables.

The laser-beam welding is swiftly growing with an estimated CAGR of 9.1% from 2025 to 2033. This growth is fueled by the increasing demand for high-precision, high-speed joining solutions in advanced manufacturing sectors such as semiconductors, medical devices, and battery assembly. A key driver behind the rise of laser-beam welding is its adoption in the electric vehicle (EV) industry in battery pack and motor housing fabrication. In China, companies like BYD and CATL have integrated laser welding into their production lines to achieve superior weld quality and thermal efficiency. According to the China Automotive Engineering Research Institute, over 90% of new EV models launched in 2023 featured laser-welded components, driving up demand for compatible consumables and protective materials. Laser welding enables micro-scale joins without warping delicate components, making it indispensable in this domain. With ongoing investments in clean technology and smart manufacturing, laser-beam welding is poised to outpace other techniques in terms of growth momentum across the Asia Pacific region.

REGIONAL ANALYSIS

China held the largest share of the Asia Pacific welding consumables market, accounting for 38.3% in 2024. The country’s industrial ecosystem demands vast quantities of welding materials for applications ranging from infrastructure to shipbuilding, as the world's top manufacturer and exporter of steel and machinery. According to the National Bureau of Statistics of China, the country completed over 1.2 billion square meters of residential floor space in 2023, all requiring structural steelwork and related welding operations. Moreover, the government’s “Dual Circulation” strategy emphasizes domestic manufacturing upgrades, leading to increased investment in automation and advanced welding technologies.

India was positioned second by leading with a 14.3% share of the Asia Pacific welding consumables market in 2024. The country’s rapid urbanization, coupled with strong government-backed infrastructure initiatives, has been instrumental in driving demand across various sectors, including roadways, railways, and power generation.

Additionally, the automotive sector, especially the growing electric vehicle (EV) industry, is contributing to market growth. Under the Faster Adoption and Manufacturing of Electric Vehicles (FAME II) scheme, over 2.5 million EVs had received subsidies by early 2024, as reported by the Department of Heavy Industry. This surge in EV production has led to increased usage of aluminum and dissimilar metal welding, requiring specialized consumables. With sustained policy support and industrial expansion, India is well-positioned to maintain its strong presence in the regional market.

Japan's welding consumables market is anticipated to grow with the highest CAGR in the coming years, with the industrial base and emphasis on precision manufacturing driving consistent demand for high-performance welding materials across sectors such as automotive, electronics, and aerospace.

Furthermore, Japan’s commitment to hydrogen energy and green technology is influencing the welding consumables market. Additionally, the shipbuilding industry, although smaller compared to China’s, remains technologically advanced, utilizing high-efficiency consumables for LNG carriers and offshore platforms.

South Korea's welding consumables market is likely to grow with a key player due to its strong presence in shipbuilding, automotive, and electronics manufacturing. The country's strategic focus on high-value industrial output ensures sustained demand for premium-grade welding materials. Shipbuilding remains a cornerstone of South Korea’s economic structure, with companies like Hyundai Heavy Industries, Samsung Heavy Industries, and Daewoo Shipbuilding & Marine Engineering leading global order books. Simultaneously, the automotive sector is transforming with increased investment in electric vehicles. The Korea Automobile Manufacturers Association reported that EV exports reached a record 520,000 units in 2023, necessitating advanced welding techniques for lightweight materials such as aluminum and high-strength steel. Moreover, South Korea’s semiconductor industry, which contributes significantly to the nation’s GDP, utilizes laser welding for micro-component assembly, further diversifying the demand spectrum for consumables.

Australia and New Zealand’s welding consumables market is expected to grow lucratively in the coming years. The region’s demand is primarily driven by mining, energy infrastructure, and defense-related manufacturing activities, particularly in Australia.

LEADING PLAYERS IN THE ASIA-PACIFIC WELDING CONSUMABLES MARKET

One of the leading players in the Asia Pacific welding consumables market is Lincoln Electric. Known for its extensive product portfolio and global reach, the company has a strong presence across key markets in the region, including China, India, and Japan. Lincoln Electric offers a wide range of electrodes, filler wires, fluxes, and shielding gases tailored to various industrial applications. The company’s focus on innovation, customer-centric solutions, and strategic partnerships enables it to maintain a competitive edge. Its investment in R&D and training programs further supports the adoption of advanced welding technologies in the region.

Another major player is ESAB Corporation, a global leader in welding and cutting solutions. ESAB has a significant footprint in the Asia Pacific region through its manufacturing facilities, distribution networks, and technical service centers. The company provides high-performance consumables suited for heavy industries such as shipbuilding, energy, and automotive. ESAB's commitment to sustainability, digital integration, and automation-ready products positions it strongly in evolving market conditions. Its ability to customize offerings based on regional needs enhances its relevance in diverse industrial ecosystems across the Asia Pacific.

Hobart Brothers, a subsidiary of Illinois Tool Works Inc., is another prominent participant in the welding consumables market. The company delivers a comprehensive range of products designed for both general fabrication and specialized applications. Hobart Brothers emphasizes quality assurance, process optimization, and workforce development through its educational initiatives. Its dedication to improving productivity and reducing operational costs makes it a preferred supplier among industry professionals.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

A major strategy adopted by key players in the Asia Pacific welding consumables market is product innovation and technological advancement. Companies are investing heavily in research and development to create high-performance, durable, and environmentally friendly welding consumables that meet evolving industry standards. These innovations cater to specialized sectors like electric vehicle manufacturing, renewable energy infrastructure, and precision electronics assembly.

Another crucial approach is strategic partnerships and collaborations with local distributors, equipment manufacturers, and training institutions. These alliances also support workforce development and skill enhancement, which are essential for maintaining consistent weld quality.

The expansion of production and distribution capabilities is a key tactic used by market leaders. Establishing new manufacturing units, warehouses, and service centers in high-growth areas allows companies to reduce lead times, lower logistics costs, and respond more swiftly to customer demands. This localized presence strengthens brand loyalty and ensures long-term competitiveness in the Asia Pacific region.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the Asia Pacific welding consumables market include Colfax Corporation, The Lincoln Electric Company, Air Liquide S.A., Tianjin Golden Bridge Welding Materials Group Co., Ltd., Kobe Steel Ltd., Hyundai Welding Co., Ltd., Panasonic Corporation, Illinois Tool Works Inc., Ador Welding Ltd., and Fronius International GmbH.

The competition in the Asia Pacific welding consumables market is characterized by a mix of global giants and rapidly growing regional manufacturers, creating a dynamic and highly contested landscape. International players leverage their technological expertise, established brand recognition, and extensive distribution networks to maintain a strong foothold. At the same time, local firms are gaining traction by offering cost-effective alternatives and adapting quickly to domestic demand patterns. This dual-market structure fosters continuous innovation and pricing pressure across segments. The presence of numerous small and medium-sized enterprises further intensifies rivalry, particularly in emerging economies where price sensitivity is high. Additionally, the increasing emphasis on automation, green manufacturing, and specialized welding applications is compelling companies to differentiate themselves through product quality, customization, and value-added services. As industries across the region evolve, market participants must continuously refine their strategies to sustain growth and capture larger shares in this competitive environment.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Lincoln Electric expanded its manufacturing facility in Shanghai, China, to increase production capacity for high-strength welding wires. This move was aimed at meeting rising demand from the construction and automotive sectors while reinforcing the company’s supply chain resilience in the region.

- In May 2024, ESAB launched a new line of low-fume flux-cored wires tailored for shipbuilding applications in South Korea. Designed to comply with stringent environmental regulations, these consumables were introduced in collaboration with major shipyards to enhance weld quality and worker safety.

- In July 2024, Hobart Brothers partnered with a leading vocational training institute in India to develop certified welding education programs. This initiative was intended to address the skills gap and promote the use of standardized welding practices and compatible consumables across the country.

- In September 2024, Kobe Steel, a key regional player, entered into a joint venture with an Australian engineering firm to distribute its welding consumables across Oceania. This alliance enabled faster market access and improved after-sales support for industrial clients in the mining and infrastructure sectors.

- In November 2024, Fronius International established a new technology center in Singapore focused on smart welding solutions. The center serves as a hub for demonstrating automated welding systems and promoting advanced consumable usage in precision manufacturing across Southeast Asia.

MARKET SEGMENTATION

This research report on the Asia Pacific welding consumables market has been segmented and sub-segmented based on type, welding technique, e, and region.

By Type

- Electrodes

- Flux

- Shielding Gas

- Filler Metals

- Others

By Welding Technique

- Arc Welding

- Resistance Welding

- Oxy-fuel Welding

- Laser-beam Welding

- Others

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What factors are driving the growth of the welding consumables market in Asia Pacific?

Key drivers include rapid industrialization, infrastructure development, increasing demand from the automotive and construction industries, and government initiatives for manufacturing growth.

2. Which countries are the major contributors to the Asia Pacific welding consumables market?

China, India, Japan, South Korea, and Australia are among the leading contributors due to their expanding industrial and manufacturing bases.

3. Who are the key players in the Asia Pacific welding consumables market?

Some major players include Colfax Corporation, The Lincoln Electric Company, Air Liquide S.A., Tianjin Golden Bridge Welding Materials Group, Kobe Steel Ltd., and Hyundai Welding Co., Ltd.

4. How are technological advancements influencing the welding consumables market in Asia Pacific?

Advancements such as automated welding systems, robotics, and the development of high-performance welding electrodes and wires are enhancing productivity, precision, and efficiency, thereby boosting market demand.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com