Global Batteries for Electrical Vehicles Charging Stations Market Size, Share, Trends & Growth Forecast Report, Segmented Research Report, Segmented By Battery Type (Lead Acid Battery, Lithium-Ion Battery, Nickel Metal Hydride and others), Vehicle Type (BEV, PHEV, and HEV), And By Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa), Industrial Analysis From (2026 to 2034)

Market Size, 2025

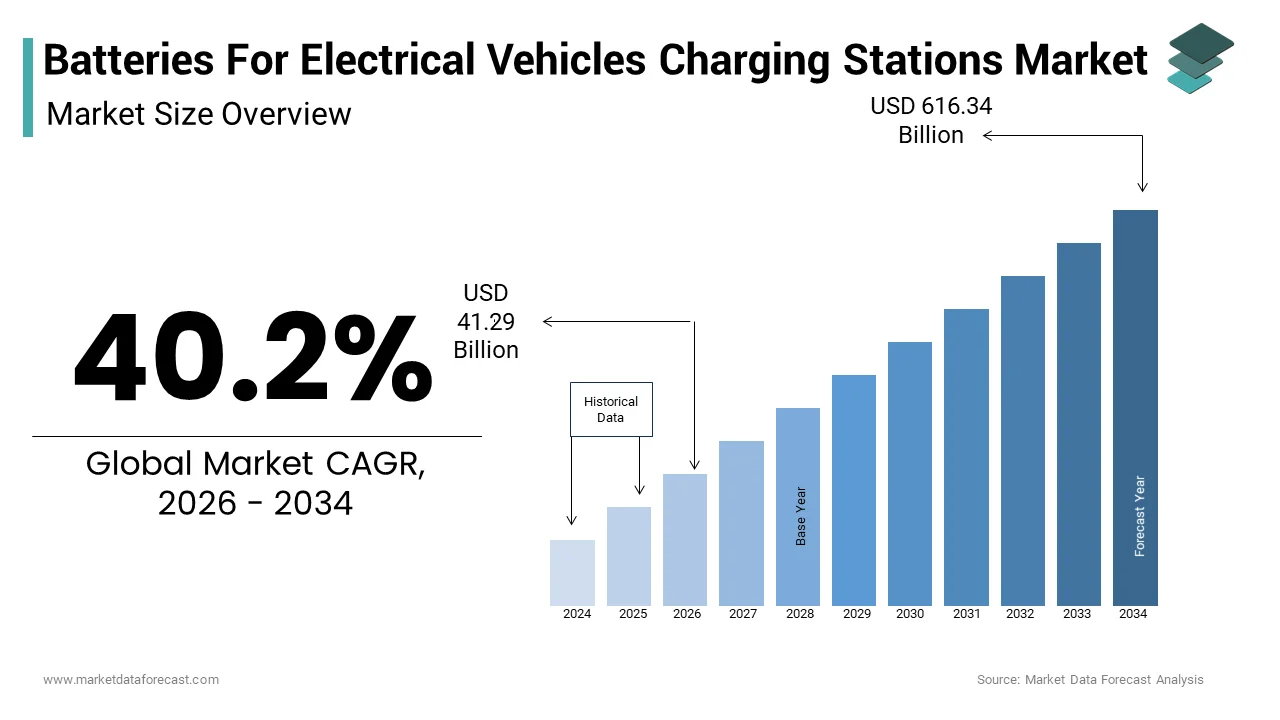

$29.45 BnMarket Estimate, 2026

$41.29 BnMarket Forecast, 2034

$616.34 BnCAGR, 2026–2034

40.2%Global Batteries for Electrical Vehicles Charging Stations Market Size

The global batteries for electrical vehicles charging station market size was valued at USD 29.45 billion in 2025 and is anticipated to reach USD 41.29 billion in 2026 to reach USD 616.34 billion by 2034, growing at a CAGR of 40.2% during the forecast period from 2026 to 2034.

Owing to the improved policy incentives, battery technology, and, therefore, the growing consumer interest in reducing vehicle carbon footprint, the share of electric vehicles (EVs) in the passenger car industry has improved over the past few years. The key determinant for increasing the driving range per recharge and decreasing the value of EVs is the development of electric vehicle batteries. To store more energy and to form them lighter and smaller, new cell chemistries are being developed for these batteries, which might enable EVs to compete with traditional vehicles.

MARKET TRENDS

Currently, lithium-nickel-manganese-cobalt-oxide (NMC) is the commonly used component in Electric vehicles. Additionally, lithium-nickel-cobalt-aluminum oxide (NCA) is employed in popular electric vehicles within the U.S. (Tesla Model 3, S, and X). However, the adoption of the latest battery chemistries for electric vehicles is increasing at a faster pace.

In the next three years, lithium-nickel-manganese-cobalt-aluminum oxide (NMCA) will have great opportunities as there is increasing adoption of these products for various purposes. They provide an extended life cycle and higher energy density as compared to the equivalent NCA and NMC materials. Hence, the development of advanced battery chemistry could be a positive trend influencing the electric vehicle battery market growth.

MARKET DRIVERS

Currently, the first source of power for EVs is lithium-ion batteries. As per a study published by the U.S. International Trade Commission in 2018, lithium-ion batteries account for over 75% of the rechargeable battery market. Additionally, the battery costs per kilowatt-hour (kWh) have fallen to less than 200 USD in 2019 from around 1000 USD in 2010. These factors are likely to propel the demand for batteries for the electric vehicle charging stations market. Moreover, due to the advancement of battery pack manufacturing techniques and cell chemistry, battery costs decreased below 100 USD/kWh by the top end of the forecast period. Affordable prices of the electric vehicle manufacturing cost are expected to propel the demand in the market. Electric vehicles hold a big emission advantage over traditional combustion engine vehicles, attributed to the reduction of transit-related emissions and also the potential to utilize and develop renewable energy resources. Growing demand to manufacture electric vehicles from government organizations and raising awareness over the benefits of these vehicles are likely to boost the demand for the fore market. Hence, vehicular emission concerns are expected to propel the adoption of EVs, which might increase the expansion of the batteries for eleelectrichicles charging stations market of the electric vehicle battery.

MARKET RESTRAINTS

Several minerals are necessary to store and utilize electricity as fuel, like cobalt, manganese, nickel, graphite, and rare-earth elements like neodymium. The supplies are geographically concentrated, and substitutes are non-existent or limited. The growing demand for EVs is probably going to lead to a short-term supply crunch for these essential battery components. Also, the shortage of charging infrastructure is an additional hurdle for the widespread adoption of electric vehicles, particularly in developing economies like India. Additionally, the price of installation is high, and the cost-efficiency for consumers to charge their vehicles is also not at the specified level. Hence, the supply chain risks and the lack of charging stations are likely to restrain the expansion of this market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 40.2% |

| Segments Covered | By Battery Type, Vehicle Type, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | A123 Systems LLC, ENVISION AESC SDI CO., LTD., LG Chem, SAMSUNG SDI CO., LTD., TOSHIBA CORPORATION, BYD Company Ltd. (Shenzhen, China), Panasonic Energy, Tesla (California, US) |

SEGMENT ANALYSIS

By Battery Insights

The batteries for the electric vehicle charging stations market are segmented into lithium-ion batteries (Li-Ion), lead-acid batteries, nickel-metal hydride (Ni-MH) batteries, and others. The lithium-ion segment held the biggest share of the market in 2019. Hence, the lithium-ion segment is predicted to dominate the global market of electric vehicle batteries over the forecast period.

By Vehicle Insights

Based on vehicle type, the batteries for electrical vehicles charging stations market for electric vehicle batteries are classified into the hybrid electric vehicle (HEV), plug-in hybrid electric vehicle (PHEV), and battery electric vehicle (BEV). The BEV segment is estimated to exhibit a better CAGR as compared to the HEV segment. The government agencies' stringent fuel economy regulations and implementation quota systems, particularly within developing economies, are likely to propel the adoption of BEV, which completely depends on rechargeable battery packs. The HEV segment held the biggest electric vehicle battery market share in 2019. HEVs use electric drive technology to deliver reduced fuel consumption and remove the dependence on charging stations. Hence, these factors, including their lower costs as compared to BEV, are anticipated to improve the dominance of this segment over others in the given forecast period.

REGIONAL ANALYSIS

North America dominated the batteries for electrical vehicles charging stations market share in 2020, and it is expected to continue its dominance during the forecast period. This can be largely due to rising investments in the development of charging station infrastructure in the region. The Batteries for Electric Vehicle Charging Stations Market in the Asia Pacific is expected to hit the highest CAGR during the forecast period, owing to a rise in the demand for electric vehicles in China, India, and Japan. China is the leading market, with the greatest number of electric vehicles sold in the region in 2020, which was around 1.77 million units.

KEY MARKET PLAYERS

Some of the market players dominate the global batteries for electric vehicle charging stations market.

- A123 Systems LLC

- ENVISION AESC SDI CO., LTD. LG Chem

- SAMSUNG SDI CO., LTD

- TOSHIBA CORPORATION

- BYD Company Ltd. (Shenzhen, China)

- Panasonic Energy

- Tesla (California, US)

RECENT MARKET NEWS

- In March 2020, BYD officially launched the new Blade Battery for Electric vehicles that optimizes the battery pack structure by over 50%, as compared to the conventional lithium iron phosphate batteries. It also exponentially increases battery safety.

- In February 202, LG Chem partnered with the U.S.-based luxury EV company Lucid Motors to supply cylindrical batteries for its EVs from the second half of 2020 up to 2023.

MARKET SEGMENTATION

This research report on the global batteries for electric vehicles charging stations market has been segmented and sub-segmented based on battery type, vehicle type, and Region.

By Battery Type

- Lead Acid Battery

- Lithium-Ion Battery

- Nickel Metal Hydride

By Vehicle Type

- Battery Electric Vehicle (BEV)

- Hybrid Electric Vehicle (HEV)

- Plug-in Hybrid Vehicle (PHEV)

By Region

- North America

- Europe

- Asia-pacific

- Middle East and Africa

- Latin America

Frequently Asked Questions

Why is the batteries for electric vehicle charging stations market growing rapidly worldwide?

The market is expanding due to increasing electric vehicle adoption, rising investments in charging infrastructure, growing demand for energy storage solutions, and the integration of renewable energy with charging networks.

What are batteries for electric vehicle charging stations and how are they used?

These are stationary energy storage systems that store electricity and supply power to EV charging stations, helping manage energy demand, improve charging reliability, and support grid stability.

How do battery energy storage systems improve EV charging station performance?

They reduce peak electricity demand, enable faster charging, improve energy efficiency, support renewable energy integration, and ensure uninterrupted charging during grid fluctuations.

Which battery technology accounts for the largest share of the batteries for electric vehicle charging stations market?

Lithium-ion batteries account for the largest market share due to their high energy density, fast charging capability, long service life, and declining production costs.

What factors are driving the growth of the batteries for electric vehicle charging stations market globally?

Rapid EV adoption, expansion of public charging networks, government incentives, increasing renewable energy deployment, and advancements in battery storage technologies are driving market growth.

Which end users generate the highest demand for battery storage systems at EV charging stations?

Public charging network operators, commercial facilities, fleet operators, utilities, highway charging providers, shopping centers, and renewable energy developers are the primary end users.

What technologies are shaping the future of the batteries for electric vehicle charging stations market?

Lithium-ion energy storage, solid-state batteries, battery management systems (BMS), AI-powered energy management, smart grid integration, vehicle-to-grid (V2G), and cloud-based monitoring platforms are driving innovation.

How are renewable energy systems influencing the batteries for electric vehicle charging stations market?

Solar and wind energy integration is increasing demand for battery storage systems that balance energy supply, reduce grid dependence, and enable sustainable EV charging infrastructure.

What challenges could affect the growth of the batteries for electric vehicle charging stations market?

High installation costs, battery degradation, raw material supply constraints, recycling challenges, and grid infrastructure limitations could affect market growth.

Which regions are expected to lead the batteries for electric vehicle charging stations market?

Asia Pacific leads the market due to rapid EV adoption and charging infrastructure expansion, while Europe and North America continue to drive growth through clean energy initiatives and large-scale investments in energy storage.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com