Global Bipolar Disorder Market Size, Share, Trends & Growth Forecast Report By Type (Bipolar I Disorder, Bipolar II Disorder, Cyclothymic Disorder), Mechanism Of Action, Drug Class and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 To 2033.

Global Bipolar Disorder Market Size

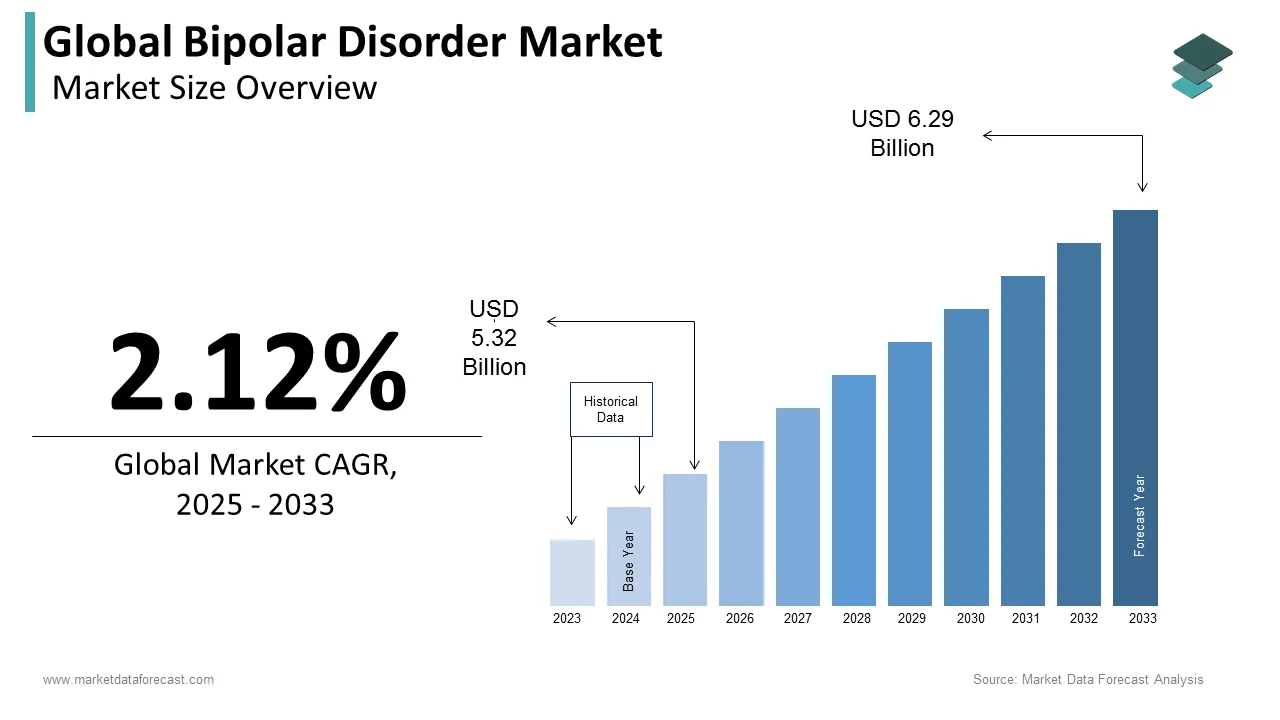

The size of the global bipolar disorder market was worth USD 5.21 billion in 2024. The global market is anticipated to grow at a CAGR of 2.12% from 2025 to 2033 and be worth USD 6.29 billion by 2033 from USD 5.32 billion in 2025.

Bipolar disorder is formerly known as manic depression. It is a mental illness specified by pathological mood swings from mania to depression. Bipolar depression is a mental disorder whose symptoms include periods with mood swings of severe depression or emotional highs. It was once called Manic Depression. In recent years, public awareness of the symptoms and treatment of bipolar disorder has increased. Typically, the treatment for bipolar disorder is for a lifetime. An abnormally elevated mood that lasts for days depends on the individual. The sudden changes in the mental state bring out high or low spirits in a person. During mania, an individual behaves or feels abnormally happy, energetic, and irritable. They often make impulsive decisions with little regard for the consequences; there is also a reduced need for sleep during manic phases. According to the Institute for Health Matric and Evaluation (IHME), it is estimated that the presence of bipolar disorder across the world is varied by country from 0.3 to 1.2%. With 52% to 48% being male and female globally, forty-six million people had bipolar in 2017.

MARKET DRIVERS

The rising prevalence of bipolar disorder, technological developments, and growing government support propels the bipolar disorder market growth.

Advancements in technology allowing more accurate detection of a patient's mood positively influence market growth. The government's bipolar disorder awareness campaigns also propel market growth. The rise in the prevalence of bipolar disorder and the various risks such as high stress, substance abuse, and others, advancements in a combination of drugs, and the need for antidepressant medications are primarily propelling the global bipolar disorder market growth. Other factors, such as increasing research and development activities and investments by the government to improve the healthcare industry, are expected to drive market growth.Moreover, creating awareness among people about bipolar disorder and the advanced technologies that facilitate precise detection of a patient's mood and mental state further accelerate the growth of the bipolar disorder market.

MARKET RESTRAINTS

Inadequate facilities for diagnosing bipolar disorder are major restraining the bipolar disorder market growth.

Strict government rules on misdiagnosing the disorder and defective equipment result in bipolar disorder being written off as another personality disorder or depression. Several drugs used to treat the disorder have been found to have addictive side effects, resulting in controlled manufacturing of the required pharmaceuticals. The use of tricyclic antidepressants has declined due to a higher incidence of side effects than other drugs used in bipolar disorder treatment.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Type, Mechanism of Action, Drug Class, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Gedeon Richter, Indivior, AstraZeneca, Janssen Pharmaceuticals, Lundbeck, Bristol-Myers Squibb, Otsuka Holdings Co. Ltd., Glaxo SmithKline (GSK), Allergan Plc, Pfizer, Inc and AbbVie, Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The bipolar I disorder segment dominated the market accounting for the most significant share of the bipolar disorder market in 2024. The growing incidence of this disease and the increasing number of people suffering severe stress levels are accelerating the growth of this segment.The Bipolar II disorder segment held a substantial market share in 2024 and is expected to grow at a considerable CAGR during the forecast period.

By Mechanism of Action Insights

The market is predicted to be dominated by the Serotonin-norepinephrine reuptake inhibitors segment during the forecast period owing to their safety in treating major depression. Serotonin-norepinephrine Reuptake Inhibitors are a class of effective medications in treating depression.

By Drug Class Insights

The antipsychotic drugs segment led the market in 2024. Owing to the rising occurrence of depression stemming from physical illness and psychosis resulted in the growth of the antipsychotic drugs segment. The increasing occurrence of depression stemming from physical illness and psychosis resulted in antipsychotic medications, the leading market segment. These Antidepressants are medications used to treat the major depressive disorder, some anxiety disorders, and some chronic pain conditions.

REGIONAL ANALYSIS

North America held a significant share of the global bipolar disorder market in 2024. The domination of the North American region can be attributed to increased stress levels and comprehensive substance abuse issues. Various government schemes and campaigns designed to create awareness fuel the market expansion in Europe and North America. In 2019, the North American region accounted for over 50% of the global bipolar disorder market and forecasted during the forecast period; this region shows its dominance. Y-O-Y growth in the prevalence of the bipolar disorder in this region is majorly increasing the market demand. A considerable amount of the North American region population suffers from high stress and sleep issues, increasing the incidence of bipolar disorder in this region and driving this regional market growth. Governments of North American countries have initiated various programs to increase awareness about bipolar disorder among the population in recent times, which is further estimated to favor market growth.

Among the other regions, the Asia Pacific market is forecasted to be brisk during the forecast period. The incidence of mental disorders is significantly growing in APAC countries such as India and China in the recent past. Hence, this factor is expected to accelerate the treatment market for bipolar disorder in this region during the forecast period.

KEY MARKET PLAYERS

Companies that are playing a promising role in the global bipolar disorder market profiled in this report are Gedeon Richter, Indivior, AstraZeneca, Janssen Pharmaceuticals, Lundbeck, Bristol-Myers Squibb, Ostuca Holdings Co. Ltd., Glaxo SmithKline (GSK), Allergan Plc, Pfizer, Inc. and AbbVie, Inc.

MARKET SEGMENTATION

This research report on the global bipolar disorder market has been segmented and sub-segmented into the following categories.

By Type

- Bipolar I Disorder

- Bipolar II Disorder

- Cyclothymic Disorder

By Mechanism of Action

- Monoamine Oxidase Inhibitors

- Tricyclic Antidepressants

- Benzodiazepines

- Serotonin-norepinephrine Reuptake Inhibitors

- Beta-Blockers

- Selective Serotonin Reuptake Inhibitors

- Others

By Drug Class

- Antianxiety Drugs

- Mood Stabilizers

- Antidepressant Drugs

- Antipsychotic Drugs

- Anticonvulsants

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

How much was the global bipolar disorder market worth in 2024?

The global bipolar disorder market size was valued at USD 5.21 billion in 2024.

Does this report include the impact of COVID-19 on the bipolar disorder market?

Yes, we have studied and included the COVID-19 impact on the global bipolar disorder market in this report.

Which are some of the notable companies in the bipolar disorder market?

Gedeon Richter, Indivior, AstraZeneca, Janssen Pharmaceuticals, Lundbeck, Bristol-Myers Squibb, Ostuca Holdings Co. Ltd., Glaxo SmithKline (GSK), Allergan Plc, Pfizer, Inc. and AbbVie, Inc. are some of the promising companies in the bipolar disorder market.

Which region is expected to lead the bipolar disorder market in the future?

Geographically, the North American region is anticipated to lead the market. However, the Asia-Pacific is growing the fastest among all the regions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com