Global Charcoal Market Size, Share, Trends & Growth Forecast Report - Segmented By Product Type (Charcoal briquettes, Lump charcoal, Extruded charcoal, Sugar Charcoal, and Others), Source, End-users, Distribution Channel, Quality, Sustainability, and Region (North America, Europe, Asia Pacific, Latin America, Middle east and Africa) – Industry Analysis (2026 to 2034)

Market Size, 2025

$6.73 BnMarket Estimate, 2026

$7.12 BnMarket Forecast, 2034

$11.18 BnCAGR, 2026–2034

5.80%Global Charcoal Market Report Summary

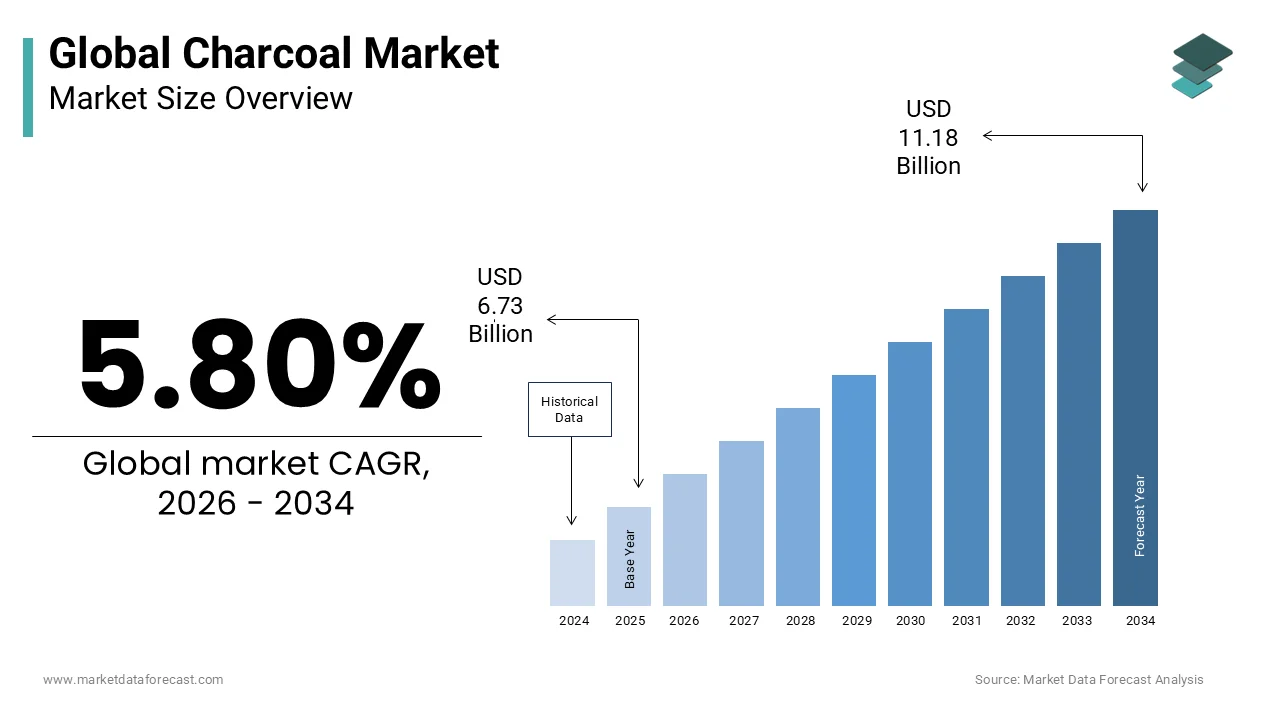

The global charcoal market was valued at USD 6.73 billion in 2025, is estimated to reach USD 7.12 billion in 2026, and is projected to reach USD 11.18 billion by 2034, growing at a CAGR of 5.80% during the forecast period. Market growth is driven by increasing demand for grilling and outdoor cooking, rising use in industrial applications, and growing adoption as an alternative fuel source. Charcoal is widely used due to its high energy efficiency, ease of storage, and versatility across residential and commercial applications. The expansion of hospitality and food service sectors, along with increasing recreational activities, is further supporting steady market growth globally.

Key Market Trends

- Rising demand for outdoor cooking and grilling is driving market growth.

- Increasing use of charcoal as an alternative fuel source is boosting demand.

- Growing applications in industrial and metallurgical processes are supporting market expansion.

- Expansion of hospitality and food service sectors is enhancing consumption.

- Rising preference for sustainable and eco friendly charcoal products is influencing market development.

Segmental Insights

- Based on product type, the charcoal briquettes segment was the largest and held 55.4% of the global charcoal market share in 2025. This dominance is attributed to uniform size, longer burn time, and ease of use.

- Based on source, the hardwood segment held a significant share of the global charcoal market in 2025. The segment’s growth is driven by its higher calorific value and preference for premium applications.

- Based on end user, the residential segment dominated the global charcoal market in 2025, supported by widespread use in household cooking and grilling activities.

Regional Insights

- The global charcoal market is experiencing steady growth across regions, supported by rising consumption and diverse applications.

- North America was the largest contributor, accounting for 30.3% of the global charcoal market share in 2025, driven by strong demand for outdoor grilling, well established retail channels, and high consumer spending on recreational activities.

Competitive Landscape

The global charcoal market is moderately competitive, with key players focusing on product quality, sustainable sourcing, and expansion of distribution networks to strengthen their market position. Companies are investing in eco friendly production methods, branding, and product innovation. Prominent players in the global charcoal market include Royal Oak Enterprises LLC, Kingsford Products Company LLC, Duraflame Inc, Fire and Flavor Grilling Co, The Original Charcoal Company Ltd, PT Dharma Hutani Makmur, Bricapar S A, Gryfskand Sp z o o, The Saint Louis Charcoal Company, Parker Charcoal Company, Josper S A, and Mesjaya Abadi Sdn Bhd.

Global Charcoal Market Size

The global charcoal market size was valued at USD 6.73 billion in 2025, and the global market size is expected to reach USD 11.18 billion by 2034 from USD 7.12 billion in 2026. The market is growing at a CAGR of 5.80% during the forecast period.

The charcoal is the carbonaceous material derived from the pyrolysis of wood and other organic substances. This versatile product serves dual purposes, as a primary fuel source for residential cooking and industrial heating and as a critical reducing agent in metallurgical processes particularly in steel manufacturing. The market is characterized by a dichotomy between traditional lump charcoal used for culinary applications and charcoal briquettes which offer consistent burning properties. According to the World Steel Association, the global steel industry consumes millions of tonnes of charcoal annually as a substitute for coke in specific applications to reduce environmental impact. The shift toward sustainable sourcing has prompted stricter regulations on forest management and carbon emissions. As per the European Environment Agency, deforestation rates linked to charcoal production have decreased by 15% in regulated zones due to improved monitoring technologies. The integration of modern kiln technologies enhances yield efficiency and reduces particulate matter emissions. Consumer preferences are increasingly favoring certified sustainable charcoal products which support responsible forestry practices.

MARKET DRIVERS

Rising Global Demand for Barbecue and Outdoor Cooking Activities

The increasing popularity of barbecue and outdoor cooking activities is major factor boosting the growth of charcoal market. Consumers prefer charcoal over gas grills for the authentic smoky flavor it imparts to food, which enhances the culinary experience. As per the Hearth Patio and Barbecue Association, sales of charcoal grills in the United States increased by 12% in 2023 a sustained interest in home cooking and outdoor entertainment. The trend toward social gatherings and backyard events has further amplified this demand as charcoal provides a cost effective and versatile fuel source for large groups. The rise of competitive barbecue competitions and culinary shows also influences consumer behavior by showcasing the superior results achieved with lump charcoal. The availability of premium charcoal products, such as hardwood lump charcoal and flavored briquettes caters to diverse consumer preferences and willingness to pay for quality. Retailers are expanding their offerings to include eco-friendly and quick lighting options which appeal to convenience oriented customers. The seasonal nature of outdoor cooking creates peak demand periods during summer months driving strategic inventory management for distributors.

Industrial Application in Metallurgy and Steel Production

The industrial sector particularly metallurgy and steel production with its unique chemical properties as a reducing agent is additionally leveraging the growth of charcoal market. Charcoal is preferred in the production of high-grade steel and ferroalloys because it contains lower levels of impurities such as sulfur and phosphorus compared to coal or coke. As per the International Iron and Steel Institute, the use of charcoal in electric arc furnaces helps reduce the carbon footprint of steel manufacturing by replacing fossil fuel based reducers. Brazil is a leading example where the steel industry relies heavily on charcoal produced from sustainably managed eucalyptus plantations. The global push for green steel initiatives encourages the adoption of bio based carbon sources to meet emission reduction targets. Charcoal acts as a renewable alternative to coke thereby lowering greenhouse gas emissions associated with traditional steelmaking processes. The demand for specialty metals such as silicon metal and calcium carbide also contributes to industrial charcoal consumption. Industrial buyers prioritize consistent quality and supply reliability, which drives investments in large scale charcoal production facilities.

MARKET RESTRAINTS

Stringent Environmental Regulations and Deforestation Concerns

The strict environmental regulations aimed at combating deforestation and air pollution pose, particularly in regions with inadequate sustainable sourcing practices is degrading the growth of charcoal market. Traditional charcoal production methods often involve inefficient earth mound kilns, which release substantial amounts of methane and particulate matter into the atmosphere. Governments in Africa and South America are implementing stricter controls on illegal logging and unregulated charcoal production to protect forest reserves. According to the World Resources Institute, deforestation rates in the Amazon basin have been linked to unsustainable charcoal production leading to bans and restrictions on informal trade. These measures increase compliance costs for producers and limit supply availability in key markets. The European Union Deforestation Regulation requires companies to prove that their charcoal products are not linked to deforestation adding administrative burdens to importers. The transition to cleaner production technologies such as retort kilns requires significant capital investment which many small scale producers cannot afford. This financial barrier limits market participation and consolidates power among larger regulated entities. Consumer awareness of environmental impacts also shifts preference away from uncertified charcoal products.

Health Risks Associated with Indoor Charcoal Usage

The health risks associated with indoor charcoal usage, particularly in developing countries is restricting the growth of charcoal market. Burning charcoal in enclosed spaces without adequate ventilation leads to high levels of indoor air pollution, including carbon monoxide and fine particulate matter. As per the World Health Organization, household air pollution from solid fuels causes approximately 3.2 million premature deaths annually with charcoal being a significant contributor in urban areas of Africa and Asia. Exposure to these pollutants is linked to respiratory infections heart disease and lung cancer posing severe public health challenges. Governments and health organizations are actively promoting cleaner cooking solutions such as liquefied petroleum gas and electric stoves to mitigate these risks. This shift reduces the dependency on charcoal for daily cooking needs, particularly among urban populations with access to modern infrastructure. The stigma associated with charcoal as a dirty and harmful fuel source discourages its adoption in middle income households seeking healthier lifestyles. Regulatory bodies are imposing stricter standards on charcoal quality to reduce emissions but enforcement remains inconsistent. The availability of affordable and efficient clean cooking technologies accelerates the decline of traditional charcoal usage. Public health campaigns emphasize the dangers of indoor charcoal burning influencing consumer behavior and policy decisions.

MARKET OPPORTUNITIES

Development of Sustainable and Certified Charcoal Products

The development of sustainable and certified charcoal products is certainly to create new opportunities for the growth of charcoal market. Certification schemes, such as the Forest Stewardship Council provide assurance that charcoal is sourced from responsibly managed forests ensuring biodiversity conservation and community benefits. As per the research, the area of certified forest land has expanded by 10% annually creating a larger base for sustainable charcoal production. Consumers in developed markets are increasingly willing to pay a premium for certified products that align with their environmental values. Retailers are responding by stocking exclusively certified brands to meet corporate sustainability goals and consumer demand. The introduction of innovative packaging solutions that highlight sustainability credentials further enhances brand appeal. Partnerships between charcoal producers and conservation organizations help promote best practices and improve supply chain transparency. The expansion of online retail platforms facilitates access to niche sustainable brands for global consumers. Education campaigns about the benefits of certified charcoal help shift consumer perceptions and drive adoption.

Expansion of Activated Charcoal Applications in Health and Filtration

The expansion of activated charcoal applications in health wellness and water filtration sectors is also creating new opportunities for the growth of charcoal market. Activated charcoal is widely used in medical treatments for poison removal and in cosmetic products for detoxification due to its high adsorption capacity. The water filtration industry also relies on activated charcoal to remove contaminants and improve taste making it essential for household and industrial purification systems. The versatility of activated charcoal allows for diversification into new product categories such as air purifiers and food processing aids. Manufacturers are investing in advanced activation techniques to enhance surface area and efficiency meeting stringent quality standards. The rising prevalence of waterborne diseases and pollution concerns boosts demand for effective filtration solutions. The pharmaceutical industry utilizes activated charcoal in drug formulation and emergency medicine expanding its clinical applications. Innovation in product forms, such as capsules powders and integrated filter cartridges enhances user convenience.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Availability

The supply chain volatility and fluctuating raw material availability is affecting production stability and pricing, which is to act as a barrier for the growth of charcoal market. Charcoal production depends heavily on the consistent supply of wood biomass, which is subject to seasonal variations weather conditions and regulatory restrictions. Climate change induced droughts and storms have disrupted wood supply chains in key producing regions leading to shortages. The competition for wood resources between the charcoal energy and paper industries further exacerbates scarcity and drives up input costs. Transportation logistics also pose challenges as charcoal is bulky and expensive to ship over long distances. According to the World Bank rising fuel costs have increased transportation expenses by 20% impacting the final retail price of charcoal. Geopolitical tensions and trade barriers can disrupt international supply routes limiting access to global markets. The informal nature of much of the charcoal trade complicates tracking and forecasting making it difficult for businesses to plan inventory. As per the International Energy Agency the lack of standardized data on charcoal production hinders effective policy making and market analysis. Producers face difficulties in securing long term contracts due to unpredictable supply volumes. The reliance on manual labor in many producing regions makes the sector vulnerable to labor shortages and wage fluctuations.

Inefficient Production Technologies and Low Yield Rates

The inefficient production technologies and low yield rates, particularly among small scale and informal producers is additionally to limit the growth of charcoal market. Traditional earth mound kilns typically achieve conversion efficiencies of only 10 to 20% meaning a large portion of the wood energy is lost as heat and smoke. However, the high cost of modern retort kilns and lack of technical expertise prevent widespread adoption among rural producers. This inefficiency leads to higher production costs and increased pressure on forest resources. According to the African Forestry Forum, poor quality charcoal generates more ash and burns unevenly reducing consumer satisfaction. The lack of standardized production protocols results in variable product characteristics which hinder brand building and export potential. Investment in technology upgrades requires access to finance which is often limited for smallholders. The slow transition to efficient technologies perpetuates environmental degradation and economic inefficiency. Regulatory incentives for technology adoption are often poorly implemented or inaccessible. Addressing this challenge requires coordinated efforts from governments NGOs and private sector stakeholders to provide training and financial support.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.80% |

| Segments Covered | By Product Type, Source, End-users, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa. |

| Market Leaders Profiled | Royal Oak Enterprises, LLC, Kingsford Products Company LLC, Duraflame, Inc., Fire & Flavor Grilling Co., The Original Charcoal Company Ltd., PT Dharma Hutani Makmur, Bricapar S.A., Gryfskand Sp. z o.o., The Saint Louis Charcoal Company, Parker Charcoal Company, Josper S.A., and Others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The charcoal briquettes segment was the largest by holding 55.4% of the global charcoal market share in 2025 due to their uniform shape consistent burning properties and cost effectiveness. The preference among casual barbecue enthusiasts and commercial establishments for a predictable cooking experience that briquettes provide. As per the Hearth Patio and Barbecue Association, over 70% of charcoal users in North America prefer briquettes for their reliability and ease of use during long cooking sessions. This consistency is crucial for restaurants and catering services that require standardized heat levels for menu items. The affordability of briquettes compared to premium lump charcoal making them accessible to a broader consumer base is additionally levelling up the growth of charcoal market. Briquettes are often manufactured using sawdust and wood scraps which are byproducts of the lumber industry thereby reducing raw material costs. According to the US Department of Agriculture, the utilization of wood waste for briquette production supports circular economy principles while keeping prices competitive. The widespread availability of briquettes in supermarkets convenience stores and big box retailers further enhances their market dominance. Marketing efforts by major brands emphasize convenience and value, which resonates with mass market consumers.

The lump charcoal segment is esteemed to witness a fastest CAGR of 6.8% from 2026 to 2034 with the rising demand for premium grilling experiences and natural products. The growing consumer preference for all natural chemical free fuel sources that do not contain binders or additives commonly found in briquettes is also escalating the growth of the segment. As per study, sales of natural and organic food products have influenced adjacent categories, including grilling fuels with consumers seeking cleaner options for cooking. Lump charcoal is made from pure hardwood chunks, which impart a distinct smoky flavor to food appealing to culinary enthusiasts and professional chefs. The expansion of the gourmet barbecue culture, where high heat and authentic flavor are prioritized. According to the study, the number of competitive barbecue teams has increased by 15% in recent years driving demand for high performance fuels. Lump charcoal burns hotter and faster than briquettes making it ideal for searing meats and achieving specific culinary techniques. The proliferation of specialty grilling stores and online retailers has improved access to premium lump charcoal brands from various regions. Social media platforms and cooking shows frequently highlight the benefits of lump charcoal influencing consumer behavior.

By Source Insights

The hardwood segment was accounted in holding a significant share of the charcoal market in 2025. The growth of the segment is majorly driven by the high calorific value of hardwood charcoal, which provides longer burn times and higher temperatures essential for both industrial and culinary applications. Species, such as oak hickory and maple are preferred for their ability to produce dense long lasting embers. As per the Food and Agriculture Organization of the United Nations, hardwood forests in temperate regions provide a sustainable supply of biomass for charcoal production when managed correctly. The established infrastructure for harvesting and processing hardwood in North America and Europe ensures consistent quality and supply. The traditional preference for hardwood charcoal in barbecue culture, particularly in regions like the Southern United States, where specific wood flavors are prized. The versatility of hardwood charcoal allows it to be used in both lump and briquette forms catering to diverse market segments. Industrial users also favor hardwood charcoal for metallurgical processes due to its low ash content and high carbon purity.

The coconut shell segment is likely to grow at a fastest CAGR of 7.5% from 2026 to 2034 with its sustainability credentials and superior properties for activated charcoal production. The abundant availability of coconut shells as agricultural waste in tropical regions, such as Southeast Asia and Latin America is also boosting the growth of the segment. Utilizing this waste stream for charcoal production reduces environmental pollution and provides additional income for farmers. As per the International Coconut Community, millions of tonnes of coconut shells are generated annually offering a vast renewable resource for charcoal manufacturing. According to the Global Water Intelligence, the demand for activated carbon is rising due to stricter water quality regulations globally. Coconut shell charcoal produces less ash and burns hotter than many wood based alternatives making it attractive for specialized industrial applications. The eco-friendly image of upcycling agricultural waste appeals to environmentally conscious consumers and corporations. Certifications for sustainable sourcing further enhance market access in developed countries.

By End User Insights

The residential segment was the largest by capturing a dominant share of the charcoal market in 2025 with the widespread practice of home barbecuing and outdoor cooking. The cultural significance of backyard grilling in many households, particularly in North America, Europe, and Australia, where outdoor living is a key lifestyle component. The social aspect of gathering family and friends around a grill reinforces regular charcoal usage. The affordability and accessibility of charcoal for home consumers, who seek a cost effective way to prepare meals. Charcoal grills are generally cheaper than gas or electric alternatives lowering the barrier to entry for new users. According to study, the number of home cooks experimenting with grilling techniques has increased during recent years boosting charcoal sales. Retail promotions and seasonal discounts further stimulate household purchases. The availability of small packaging sizes suits the consumption patterns of individual families.

The industrial segment is projected to grow at the fastest CAGR of 5.2% from 2026 to 2034 with the increasing demand for charcoal in metallurgy and chemical production. The use of charcoal as a reducing agent in the production of silicon metal ferroalloys and high grade steel. Charcoal offers lower impurity levels compared to coal resulting in higher quality metal outputs. The shift toward green steel initiatives, where bio based carbon sources like charcoal are used to reduce the carbon footprint of steelmaking. According to the research, several major steel producers are investing in charcoal based processes to meet sustainability targets. The industrial sector requires large volumes of consistent quality charcoal which drives investments in large scale production facilities. The expansion of the electric vehicle market boosts demand for silicon metal further supporting industrial charcoal consumption. Regulatory pressures to reduce fossil fuel usage in heavy industries accelerate the adoption of renewable carbon sources. The industrial biomass usage is expected to increase as part of decarbonization strategies. The stability of long-term contracts with industrial buyers provides revenue security for producers.

REGIONAL ANALYSIS

North America Charcoal Market Analysis

North America was the top performer of the global charcoal market by holding 30.3% of share in 2025 with the strong culture of outdoor cooking and well established retail infrastructure. The United States and Canada are the primary contributors with high household penetration of barbecue grills. As per the Hearth Patio and Barbecue Association, charcoal sales in the region remain robust despite competition from gas grills due to the preferred flavor profile. The prevalence of backyard barbecuing as a social activity supported by a wide variety of charcoal products ranging from premium lump to standard briquettes. The presence of major charcoal manufacturers and distributors, who ensure wide availability in supermarkets and hardware stores is driving the growth of the segment. The region also has stringent environmental regulations that promote sustainable sourcing and efficient production methods. The growing interest in artisanal and gourmet grilling further boosts demand for high quality lump charcoal.

Europe Charcoal Market Analysis

Europe charcoal market growth was positioned second by capturing 22.1% of share in 2025 with the strict environmental regulations and a growing preference for sustainable products. Countries, such as Germany, France, and the United Kingdom are key contributors with strong traditions of outdoor cooking. As per the European Commission, the EU Deforestation Regulation impacts charcoal imports by requiring proof of sustainable sourcing. The second driver is the popularity of outdoor dining and social gatherings in urban areas where portable charcoal grills are common. As per Eurostat the import of charcoal into the EU has shifted toward suppliers with verified sustainability credentials. The region’s focus on reducing air pollution has led to restrictions on low quality charcoal production encouraging imports of high efficiency products. The presence of specialized barbecue shops and online retailers facilitates access to premium brands. The cultural diversity in Europe supports varied grilling traditions from Mediterranean skewers to Northern European sausages. These dynamics shape a market that values quality and sustainability over price.

Asia Pacific Charcoal Market Analysis

Asia Pacific charcoal market growth is expected to have fastest CAGR during the forecast period with its role as a major producer and consumer of charcoal for both domestic and industrial use. Countries, such as China, Indonesia, and Thailand, are key players in production, while Japan and South Korea are significant consumers. As per the Food and Agriculture Organization of the United Nations, the region produces the world’s charcoal primarily from hardwood and coconut shells. The widespread use of charcoal for residential cooking in rural and semi urban areas where it remains a primary fuel source. Millions of households in Southeast Asia rely on charcoal for daily energy needs. The growing industrial demand for charcoal in metallurgy and activated carbon production, particularly in China. The export of charcoal to other regions also contributes to market volume.

Latin America Charcoal Market Analysis

Latin America charcoal market growth is likely to grow with its extensive use of charcoal in the steel industry. As per the study, the country is the only major steel producer that relies heavily on renewable charcoal rather than coal. The industrial demand from the steel sector, which supports large scale plantation forestry and charcoal production. According to the Ministry of Mines and Energy in Brazil, charcoal production is integrated with sustainable forest management practices. The second driver is the cultural tradition of churrasco or barbecue, which drives residential consumption, particularly in Brazil and Argentina. As per the research, the popularity of outdoor cooking supports a vibrant domestic market for lump charcoal. The availability of abundant biomass resources such as eucalyptus and native woods facilitates production.

Middle East and Africa Charcoal Market Analysis

The Middle East and Africa charcoal market growth is likely to grow with the significant residential usage and emerging industrial applications. Countries, such as Nigeria, Kenya, and South Africa are key markets, where charcoal is a primary cooking fuel for urban households. As per the International Energy Agency, charcoal consumption in Sub Saharan Africa is expected to rise due to urbanization and limited access to electricity. The first major driver is the reliance on charcoal as an affordable and accessible energy source for cooking in densely populated cities. The growing tourism and hospitality sector in countries like South Africa and Morocco, which uses charcoal for traditional cooking experiences. The informal nature of much of the charcoal trade poses challenges for regulation and sustainability. Efforts to promote improved cookstoves aim to reduce consumption and emissions.

COMPETITIVE LANDSCAPE

The charcoal market features a fragmented competitive landscape with a mix of large multinational corporations and numerous small regional producers. Major brands compete on the basis of product quality brand recognition and distribution reach while smaller players often focus on niche segments such as organic or artisanal charcoal. Price competition remains intense in the commodity briquette segment where cost efficiency is paramount. However, the premium lump charcoal sector sees competition driven by source origin sustainability credentials and burning performance. Regulatory pressures regarding deforestation and emissions are forcing companies to adopt cleaner production methods and transparent supply chains. This shift creates barriers to entry for informal producers who cannot meet compliance standards. Established players leverage economies of scale and long term supplier contracts to maintain stability. New entrants often differentiate through innovative branding and direct to consumer sales models. The rise of e-commerce allows niche brands to reach global audiences bypassing traditional retail gatekeepers. Consumer preference for natural and eco friendly products is reshaping competitive dynamics favoring sustainable practices.

Key Market Players

Some of the key players dominating the global charcoal market are

- Royal Oak Enterprises, LLC

- Kingsford Products Company, LLC

- Duraflame, Inc.

- Fire & Flavor Grilling Co.

- The Original Charcoal Company Ltd.

- PT Dharma Hutani Makmur

- Bricapar S.A.

- Gryfskand Sp. z o.o.

- The Saint Louis Charcoal Company

- Parker Charcoal Company

- Josper S.A.

- Mesjaya Abadi Sdn Bhd

Top Players in the Market

- Kingsford Products Company stands as a dominant force in the global charcoal market renowned for its iconic briquette products. The company leverages extensive distribution networks to ensure widespread availability in retail stores across North America and international markets. Recently Kingsford launched innovative quick light variants and eco friendly packaging to appeal to modern consumers seeking convenience and sustainability. These initiatives strengthen its brand loyalty among casual grillers who prioritize ease of use. The company also invests heavily in marketing campaigns tied to major sporting events and holidays to drive seasonal demand. Its strategic partnerships with grill manufacturers further integrate its products into the outdoor cooking ecosystem ensuring continued relevance and strong market presence globally.

- Royal Oak Industries is a leading supplier of premium lump charcoal known for its commitment to natural and additive free products. The company sources hardwood from sustainable forests to produce high quality charcoal that appeals to barbecue enthusiasts and professional chefs. Recently Royal Oak expanded its sourcing operations in South America to secure stable raw material supplies and reduce production costs. This move enhances its ability to meet growing global demand for premium grilling fuels. The company also introduced larger bag sizes for commercial clients strengthening its foothold in the hospitality sector. Royal Oak emphasizes transparency in its supply chain which resonates with environmentally conscious consumers.

- Jealous Devil LLC has emerged as a significant player in the premium charcoal segment by focusing on high quality all natural lump charcoal. The company targets serious grillers and pitmasters who demand consistent heat and clean burning fuel. Recently Jealous Devil expanded its retail presence by partnering with major home improvement chains and specialty food retailers. This expansion increases accessibility for consumers seeking premium alternatives to standard briquettes. The company also launched educational content on social media platforms to engage with the barbecue community and build brand advocacy. Its commitment to sustainable sourcing and minimal processing aligns with current consumer trends toward natural products.

Top Strategies Used by Key Market Participants

Key players in the Charcoal Market primarily focus on product differentiation through premiumization and sustainability certifications to attract discerning consumers. Companies are increasingly investing in sustainable sourcing practices such as Forest Stewardship Council certification to mitigate environmental concerns and enhance brand reputation. Strategic partnerships with retail giants and e commerce platforms expand distribution reach and improve product visibility. Innovation in packaging designs including resealable and eco friendly materials addresses consumer convenience and waste reduction needs. Marketing efforts emphasize the authentic flavor and natural qualities of lump charcoal to distinguish it from conventional briquettes. Expansion into emerging countries with growing middle classes offers new growth opportunities for established brands. Companies also diversify their portfolios by introducing related accessories such as grills and smokers to create bundled offerings.

MARKET SEGMENTATION

This research report on the global charcoal market has been segmented and sub-segmented based on product type, source, end-users, and region.

By Product Type

- Charcoal briquettes

- Lump charcoal

- Extruded charcoal

- Sugar Charcoal

- Others

By Source

- Bamboo

- Coconut shells

- Hardwood

- Softwood

- Others

By End User

- Residential

- Commercial

- Industrial

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the charcoal market?

The charcoal market refers to the global industry producing charcoal used for household cooking, grilling, industrial heating, and specialty culinary applications.

2. What factors are driving the growth of the charcoal market?

Key drivers include reliance on charcoal in energy-deficient regions, growth in urban migration, and rising popularity of grilling and culinary traditions globally.

3. Which regions rely most on charcoal for cooking?

Sub-Saharan Africa and parts of Southeast Asia have the highest reliance on charcoal due to limited electricity access and expensive alternative fuels.

4. What are the main types of charcoal available in the market?

The market includes lump charcoal, briquettes, white charcoal, and specialty or flavored charcoal for gourmet and grilling applications.

5. Which regions dominate the global charcoal market?

Africa leads in consumption for household cooking, while North America, Europe, and East Asia dominate premium and culinary-grade charcoal demand.

6. What are the key trends shaping the charcoal market?

Trends include premium and artisanal charcoal, biochar integration, carbon-negative production, and traceable sustainable sourcing.

7. What challenges does the charcoal market face?

Challenges include deforestation concerns, informal and opaque supply chains, inefficient production methods, and environmental pollution.

8. What are the opportunities in the charcoal market?

Opportunities exist in biochar and carbon-negative charcoal, gourmet and flavored charcoal, and integration of traceability and sustainable practices.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com