Cloud Storage Market Size, Share, Trends & Growth Forecast Report By Type (Solutions and Services), Deployment Model (Public Cloud, Private Cloud and Hybrid Cloud), Organization Size (Large Enterprises, Small and Medium-Sized Enterprises), Vertical & Region, Industry Forecast From 2024 to 2033

Global Cloud Storage Market Size

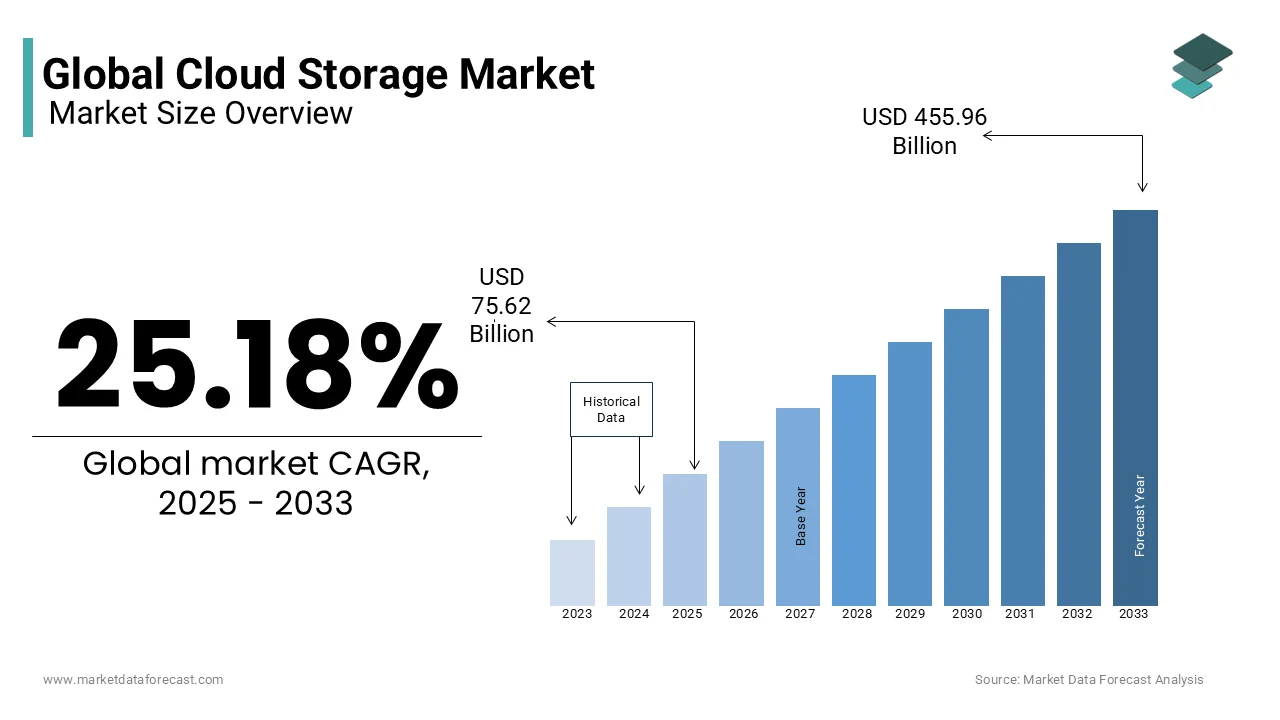

The global cloud storage market was worth USD 60.41 billion in 2024. The global market size is anticipated to grow from USD 75.62 billion in 2025 to USD 455.96 billion by 2033. The market is expected to move forward at a CAGR of 25.18% during the forecast period 2025 to 2033.

Cloud storage is a remote data storage service delivered over the internet by enabling individuals and organizations to store, manage, and retrieve digital information without relying on local physical infrastructure. Cloud storage has evolved beyond mere data backup to become a foundational component of digital transformation, which is supporting applications such as real-time collaboration, disaster recovery, artificial intelligence processing, and enterprise resource planning. As per the International Data Corporation, global data creation is projected to reach 181 zettabytes by 2025, driven by the proliferation of connected devices, high-resolution media, and transactional systems.

MARKET DRIVERS

Proliferation of Internet of Things (IoT) Devices Generating Massive Data Volumes

The exponential expansion of IoT ecosystems across industrial, consumer, and urban environments is driving the growth of the cloud storage Market. According to the International Telecommunication Union, over 18.8 billion IoT devices were in operation globally in 2023, a figure expected to surpass 29 billion by 2028. In the automotive sector, the Society of Automotive Engineers estimates that a single autonomous vehicle generates up to 4 terabytes of data per day, necessitating cloud infrastructure for real-time analysis and long-term archival. These data demands are further amplified in smart cities, where surveillance cameras, traffic sensors, and environmental monitors feed into centralized cloud repositories. As per the World Economic Forum, Singapore’s Smart Nation initiative processes over 2.3 billion data points daily from connected infrastructure, all stored and analyzed in cloud environments.

Accelerated Digital Transformation in Government and Public Sector Institutions

The governments worldwide are implementing digitalization initiatives that mandate the migration of legacy records, citizen services, and administrative workflows to cloud-based platforms, which is propelling the growth of the cloud storage Market. In India, the Ministry of Electronics and Information Technology reported that the Digital India program had digitized over 1.2 billion citizen records by 2023, including land titles, educational certificates, and Aadhaar-linked data, all stored in the National Cloud (MeghRaj). Similarly, the European Commission’s Interoperability Solutions for European Public Administrations (ISA²) program has enabled cross-border data exchange among 36 European countries, relying on cloud storage to manage shared legal, migration, and customs databases.

MARKET RESTRAINTS

Persistent Concerns Over Data Sovereignty and Jurisdictional Compliance

The data sovereignty to cloud storage adoption for multinational corporations and regulated industries is restricting the growth of the cloud storage Market. As per the United Nations Conference on Trade and Development, over 137 countries have enacted data localization laws requiring certain categories of data to remain within national borders. In the European Union, the General Data Protection Regulation (GDPR) imposes strict conditions on cross-border data transfers, with the European Data Protection Board reporting 1,456 formal complaints related to international data transfers in 2022 alone. These regulatory complexities increase operational costs and architectural fragmentation, as organizations must deploy region-specific cloud instances or adopt hybrid models. For example, Deutsche Bank operates separate cloud environments for its European, Asian, and American divisions to comply with local mandates.

High Latency and Bandwidth Limitations in Emerging Regions

The inadequate internet infrastructure, which is resulting in high latency and low bandwidth, is limiting the growth of the cloud storage Market. According to the International Telecommunication Union, the average fixed broadband speed in sub-Saharan Africa was 14.3 Mbps in 2023, less than half the global average of 34.7 Mbps, which makes large-scale data uploads and real-time synchronization impractical. Educational institutions are particularly affected. UNESCO found that 60% of universities in West Africa faced persistent disruptions in accessing cloud-hosted research databases due to unstable connections. These technical constraints force organizations to rely on local servers or offline storage, undermining the economic and operational benefits of cloud adoption.

MARKET OPPORTUNITIES

Integration of Cloud Storage with Artificial Intelligence and Machine Learning Workflows

The integration of cloud storage with AI and machine learning technologies with advanced models requires access to vast, which is to degrade the growth of the cloud storage Market. According to the Stanford Institute for Human-Centered Artificial Intelligence, the average AI training dataset size increased by 470% between 2018 and 2023, with large language models like GPT-3 requiring over 570 gigabytes of text data stored and processed in cloud environments. Cloud storage provides the elasticity needed to handle such massive datasets, allowing researchers and enterprises to scale resources dynamically.

Expansion of Edge Computing Ecosystems Complementing Cloud Storage Architectures

The rise of edge computing is processing data closer to its source rather than in centralized data centers, which is creating new opportunities for the growth of the cloud storage Market. As per the Institute of Electrical and Electronics Engineers, over 60% of enterprise data will be processed at the edge by 2025, up from 10% in 2020 with applications in smart factories, autonomous drones, and real-time surveillance. In the oil and gas industry, Shell deploys edge servers on offshore rigs to monitor equipment in real time, then transmits compressed operational data to AWS for long-term storage and predictive modeling. According to the Open Compute Project, hybrid edge-cloud deployments reduced data transmission costs by 35% in logistics firms using IoT trackers across global supply chains.

MARKET CHALLENGES

Escalating Cybersecurity Threats Targeting Cloud-Based Data Repositories

The cloud storage environments are increasingly targeted by sophisticated cyberattacks by including ransomware, data exfiltration, and supply chain intrusions. As per the Cybersecurity and Infrastructure Security Agency, cloud-based systems accounted for 45% of all reported data breaches in the United States in 2023, a 22% increase from 2020. In a high-profile incident, the 2022 breach of Microsoft Exchange Online exposed over 50,000 organizations’ email and file storage due to a zero-day vulnerability exploited by state-sponsored actors. Healthcare is particularly vulnerable, with the U.S. Department of Health and Human Services recording 725 healthcare data breaches in 2023, with 61% involving cloud-hosted systems.

Rising Environmental Impact of Large-Scale Data Center Operations

The environmental footprint of cloud storage infrastructure, particularly energy consumption and carbon emissions from data centers, is also restricting the growth of the cloud storage Market. Cooling systems alone consume 30–40% of a data center’s total power, as noted by the U.S. Department of Energy. Water usage is another concern; a 2023 investigation by the Pacific Institute revealed that Amazon’s data centers in Northern Virginia used 2.8 million gallons of water per day for cooling, straining local resources during droughts.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 25.18% |

| Segments Covered | By Type, Organization Size, Deployment, Model, Vertical, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | AWS (USA), IBM (USA), Microsoft (USA), Google (USA), Oracle (USA), HPE (US), Dell EMC (US), VMware (US), Rackspace (USA), Dropbox (US), and others. |

SEGMENT ANALYSIS

By Type Insights

The solutions segment dominated the global cloud storage market by capturing the largest share in 2024 with the growing deployment of integrated cloud storage platforms that offer core functionalities such as data encryption, automated backup, disaster recovery, and real-time synchronization. Enterprises increasingly prioritize ready-to-deploy software solutions that can be seamlessly embedded into existing IT ecosystems, reducing dependency on prolonged integration cycles. A key driver of this segment’s dominance is the rising demand for scalable, secure, and interoperable storage infrastructure across various sectors. As per the National Institute of Standards and Technology, large hospitals now store an average of 30 petabytes of imaging and patient data annually with high-performance cloud storage software with built-in compliance controls.

The services segment is swiftly emerging with an expected CAGR of 18.7% in the coming years owing to the increasing complexity of cloud environments, which necessitates specialized expertise in migration, integration, security, and optimization. As organizations adopt multi-cloud and hybrid architectures, the demand for professional and managed services has surged to ensure seamless interoperability and regulatory compliance. Managed service providers (MSPs) are playing a pivotal role in this transition; Rackspace Technology reported that its managed cloud services revenue grew by 15% year-on-year in 2023, driven by demand from healthcare and financial institutions. Additionally, regulatory mandates are increasing the need for compliance-focused services.

By Deployment Model Insights

The public segment held 58.3% of the cloud storage Market share in 2024, with the inherent advantages of cost efficiency, scalability, and rapid deployment offered by multi-tenant infrastructure operated by global hyperscalers such as Amazon Web Services, Microsoft Azure, and Google Cloud Platform. Enterprises across sectors are leveraging public cloud storage to avoid the capital expenditures associated with on-premises data centers while gaining access to cutting-edge technologies like AI-driven analytics and serverless computing.

The hybrid segment is likely to register a CAGR of 21.3% in the coming years with the balanced approach that combines the scalability of public cloud with the control and security of private infrastructure. Organizations in highly regulated sectors such as finance, defense, and healthcare are increasingly adopting hybrid models to meet data sovereignty requirements while leveraging public cloud resources for non-sensitive operations. Another driver is disaster resilience with the Business Continuity Institute reporting that 67% of enterprises using hybrid cloud storage achieved recovery time objectives (RTOs) under five minutes during outages. In manufacturing, Siemens integrates edge devices with hybrid cloud storage to process real-time factory data locally while archiving historical records in the public cloud for predictive maintenance.

By Organization Size Insights

The large enterprises segment accounted in holding a dominant share of the cloud storage market in 2024, with massive data volumes, complex IT ecosystems, and strategic investments in digital transformation initiatives that require enterprise-grade cloud storage infrastructure. These organizations operate across multiple geographies and regulatory jurisdictions, necessitating centralized, secure, and compliant data management systems. In the pharmaceutical industry, Pfizer stores over 50 petabytes of clinical trial data in Microsoft Azure, enabling real-time collaboration across 60 countries while adhering to FDA and EMA regulations.

The small and medium-sized enterprises (SMEs) segment is projected to grow with a CAGR of 19.8% during the forecast period, with the increased digital adoption, affordable subscription models, and government-backed digitalization programs that lower entry barriers to cloud storage. SMEs are increasingly recognizing cloud storage as a strategic enabler for competitiveness, agility, and business continuity. Additionally, integrated solutions such as cloud-based accounting, CRM, and email are bundling storage as a default feature.

By Vertical Insights

The banking, financial services, and insurance (BFSI) segment is the major revenue generator for the cloud storage market. This segment is driving forward because of the consistently increasing demand for safe storage facilities or systems, swift digitalization, and the rising application of e-wallets, online payments, and net banking. In addition, there is a rising preference for enterprise platforms that have intelligence, flexibility, agility, and expandability due to the mounting pressure on banking institutions to make informed decisions to be one step ahead of the competition. Also, big companies are building data centers nearby to accelerate the acceptance of different cloud storage models, enhance client service quality, and administer running costs for higher profits in the BFSI industry. Therefore, the segment's growth is driven by cost-effectiveness, flexibility, and better security.

REGIONAL ANALYSIS

North America Cloud Storage Market Insights

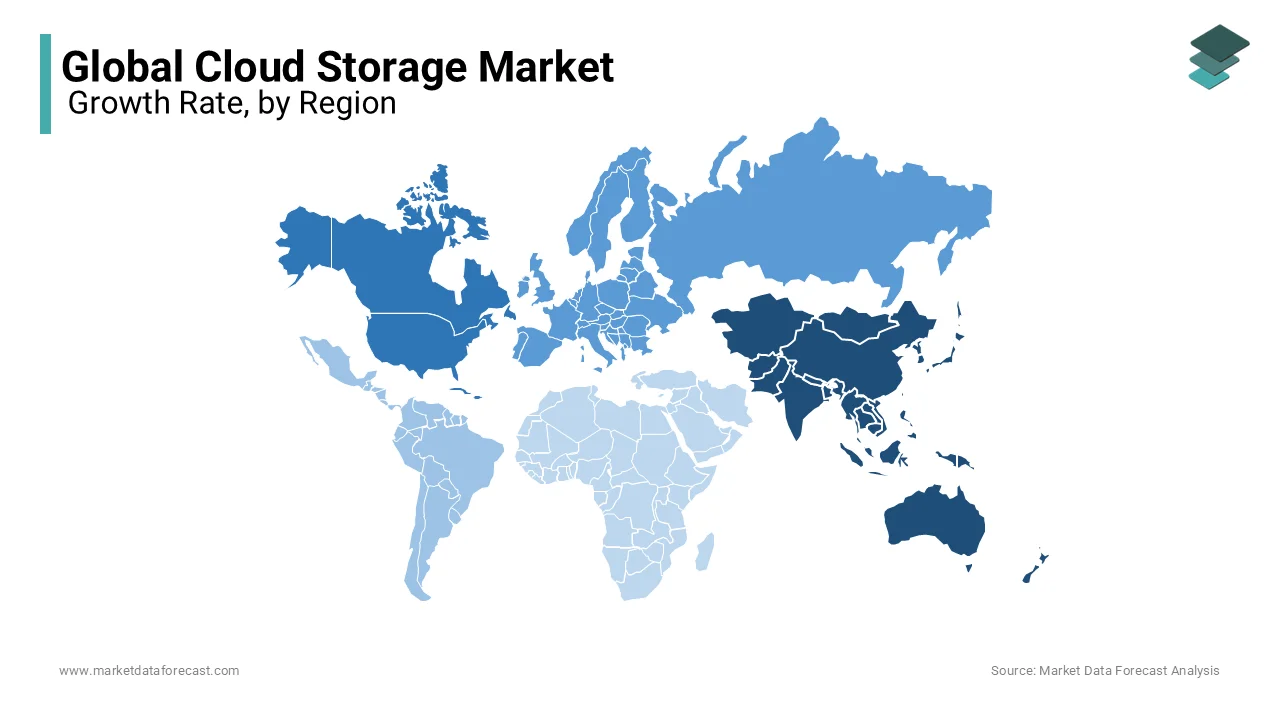

North America was the largest contributor with 41.6% of the cloud storage Market share in 2024. The United States serves as the epicenter of innovation and adoption, which is hosting the headquarters of AWS, Microsoft Azure, and Google Cloud. Federal and state-level digital transformation mandates have accelerated cloud integration; the U.S. General Services Administration reported that 85% of federal agencies had migrated applications to cloud storage by 2023 under the Cloud Smart policy. Additionally, the U.S. leads in edge-cloud integration, with companies like NVIDIA and Intel deploying hybrid architectures for AI training.

Europe Cloud Storage Market Insights

Europe was positioned second in the cloud storage Market by capturing 26.8% of share in 2024. The European Union’s Digital Decade policy aims for 90% of SMEs to use cloud computing by 2030 by accelerating investment in compliant storage solutions. France has launched the “Souveraineté Numérique” initiative, which is promoting French-owned cloud providers like OVHcloud to reduce dependency on U.S. hyperscalers. However, GDPR compliance remains a challenge. The European Data Protection Supervisor recorded 2,143 cloud-related complaints in 2022, prompting stricter audits.

Asia-Pacific Cloud Storage Market Insights

Asia-Pacific (APAC) cloud storage Market growth is likely to register a significant CAGR during the forecast period, with the rapid digitalization, urbanization, and government-led smart infrastructure projects. According to the Chinese Ministry of Industry and Information Technology, cloud adoption among state-owned enterprises increased by 38% from 2021 to 2023, driven by the “East Data West Computing” initiative to balance data center loads. Australia’s healthcare sector is adopting cloud storage at scale, with the Australian Digital Health Agency centralizing 24 million My Health Records on AWS.

Latin America Cloud Storage Market Insights

Latin America cloud storage Market growth is likely to be driven by Brazil and Mexico, leading adoption amid improving connectivity and digital government initiatives. Brazil’s “Gov.br” platform has migrated over 500 federal services to cloud storage, serving 150 million citizens, as reported by the Ministry of Management and Innovation in Public Services. Chile and Colombia are advancing data protection laws by encouraging compliant cloud adoption.

Middle East and Africa Cloud Storage Market Insights

Middle East and Africa (MEA) cloud storage market growth is likely to grow with the UAE, Saudi Arabia, and South Africa, with the adoption through national digital transformation strategies. Saudi Arabia’s Vision 2030 includes a $10 billion investment in cloud infrastructure, with NEOM’s smart city project relying on Huawei and AWS for data management.

KEY PLAYERS IN THE MARKET

Companies playing a significant role in the global cloud storage market include AWS (USA), IBM (USA), Microsoft (USA), Google (USA), Oracle (USA), HPE (US), Dell EMC (US), VMware (US), Rackspace (USA), and Dropbox (US).

TOP LEADING PLAYERS IN THE MARKET

Amazon Web Services (AWS)

Amazon Web Services (AWS) has maintained its position as a dominant force in the Asia Pacific cloud storage market through extensive infrastructure investment and localized service offerings. AWS operates multiple availability zones across key markets, including Singapore, Sydney, Tokyo, and Mumbai, ensuring low-latency access and compliance with regional data residency requirements. In 2023, AWS launched a new region in Indonesia to support the country’s digital economy by enabling local enterprises and government agencies to store data within national borders. The company has also partnered with telecom providers like NTT Communications and Reliance Jio to enhance hybrid cloud connectivity. AWS continues to innovate with services like S3 Intelligent-Tiering and Glacier Deep Archive, optimizing cost and performance for diverse workloads. Its collaboration with APAC-based fintechs and healthcare institutions to ensure GDPR and HIPAA-compliant storage further strengthens trust.

Microsoft Azure

Microsoft Azure has significantly expanded its footprint in the Asia Pacific cloud storage landscape by aligning with enterprise digital transformation goals and public sector modernization. The platform offers region-specific data centers in South Korea, Hong Kong, and New Zealand, supporting stringent regulatory demands in finance, healthcare, and government. In 2023, Microsoft launched Azure Local, a new edge-computing and storage solution in Japan, tailored for manufacturing and logistics firms requiring real-time data processing. The company deepened its integration with local ecosystems by collaborating with Singapore’s Smart Nation initiative to store and analyze urban data in Azure’s secure cloud environment. Additionally, Microsoft strengthened its partnerships with education providers, enabling universities across India and Australia to migrate research data to Azure for AI-driven analysis. Its hybrid offerings, such as Azure Stack, allow organizations to maintain on-premises control while leveraging cloud scalability.

Alibaba Cloud

Alibaba Cloud is a pivotal player in the Asia Pacific cloud storage market, leveraging its deep regional roots and strategic government collaborations to drive adoption. As the largest cloud provider in China, it has extended its influence to Southeast Asia by establishing data centers in Malaysia, Thailand, and the Philippines, catering to e-commerce, fintech, and smart city projects. In 2023, Alibaba Cloud launched a dedicated data sovereignty framework for ASEAN countries, ensuring compliance with local regulations while offering cross-border data synchronization for multinational clients. The company introduced PolarDB and Object Storage Service (OSS) upgrades optimized for high-concurrency applications, supporting platforms like Lazada during peak shopping seasons.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the cloud storage market employ a range of strategic initiatives to consolidate their competitive edge. Hyperscalers are expanding geographically by launching new regional data centers to comply with data sovereignty laws and reduce latency. Companies are investing in hybrid and multi-cloud architectures to meet enterprise demands for flexibility and risk mitigation. Product innovation focuses on AI-integrated storage, automated tiering, and enhanced security features such as zero-trust frameworks and end-to-end encryption. Strategic partnerships with telecom operators, system integrators, and government bodies are accelerating market penetration. Sustainability is emerging as a differentiator, with providers adopting renewable energy and energy-efficient cooling technologies. Customer lock-in is reinforced through ecosystem integration, bundling storage with compute, analytics, and productivity tools.

COMPETITION OVERVIEW

The competition in the cloud storage market is marked by intense rivalry among global hyperscalers and regional providers, each vying for dominance through innovation, compliance, and ecosystem integration. Amazon Web Services, Microsoft Azure, and Google Cloud leverage their vast infrastructure and technological breadth to maintain its dominance, while regional players like Alibaba Cloud, Tencent Cloud, and OVHcloud capitalize on local regulatory alignment and cost advantages. The battleground extends beyond price to include data sovereignty, security certifications, and sustainability credentials, which are increasingly influencing procurement decisions. Enterprises demand seamless interoperability across public, private, and hybrid environments, pushing vendors to refine multi-cloud management tools. Smaller providers differentiate through niche offerings such as edge-optimized storage or industry-specific compliance frameworks. Government digitalization programs are shaping procurement landscapes, with nations favoring providers that support national data policies.

RECENT MARKET DEVELOPMENTS

- In January 2023, Amazon Web Services launched a new cloud region in Jakarta, Indonesia by enabling local data residency and reducing latency for Southeast Asian enterprises and government agencies.

- In May 2023, Microsoft introduced Azure Local in Japan, a hybrid edge-cloud storage solution designed for manufacturing and logistics firms requiring real-time data processing and low-latency access.

- In September 2023, Alibaba Cloud partnered with the Thai Ministry of Digital Economy to digitize 10,000 small and medium enterprises using cloud storage and AI-driven analytics tools.

- In February 2024, Google Cloud enhanced its Chronicle security analytics platform with deeper integration into cloud storage by enabling real-time threat detection across petabyte-scale datasets.

- In July 2023, Tencent Cloud expanded its data center capacity in Hong Kong by 40% with its position in the financial services sector with low-latency, compliant storage solutions.

MARKET SEGMENTATION

This research report on the global cloud storage market has been segmented and sub-segmented based on the type, organization size, deployment model, vertical, and region.

By Type

- Solutions

- Services

By Organization Size

- Large enterprises

- Small and Medium-sized Enterprises (SMEs)

By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

By Vertical

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- Telecommunications and Information Technology-Enabled Services (ITES)

- Government and Public Sector

- Manufacturing

- Consumer Goods and Retail

- Media And Entertainment

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What are the primary factors driving the growth of the cloud storage market?

Key factors include the increasing adoption of cloud services across businesses, the need for data backup and disaster recovery, the rise of big data and IoT, and the growing trend towards remote work, which has heightened the demand for accessible and scalable storage solutions.

What are the key trends shaping the future of the cloud storage market?

Emerging trends include the growing adoption of hybrid and multi-cloud strategies, increased focus on security and data privacy, the integration of AI and machine learning for data management, and the rise of edge computing, which necessitates more localized cloud storage solutions.

What impact is the rise of 5G technology expected to have on the cloud storage market?

The rollout of 5G is expected to significantly boost the cloud storage market by enabling faster data transfer speeds, lower latency, and the ability to support a higher density of connected devices. This will accelerate the adoption of cloud-based applications and services, leading to increased demand for storage solutions.

What role do startups and smaller players play in the cloud storage market?

Startups and smaller players play a crucial role by driving innovation, particularly in niche markets such as cloud security, data management, and specialized storage solutions. They often collaborate with larger cloud providers or offer complementary services that cater to specific industry needs, thus enhancing the overall ecosystem.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com