Global Clutch Market Size Share, Trends, and Growth Analysis Report, Segmented By Transmission, Clutch Size, Vehicle, & Region (North America, Europe, Latin America, Asia Pacific, Middle East & Africa), Industry Forecast From 2025 to 2033

Global Clutch Market Summary

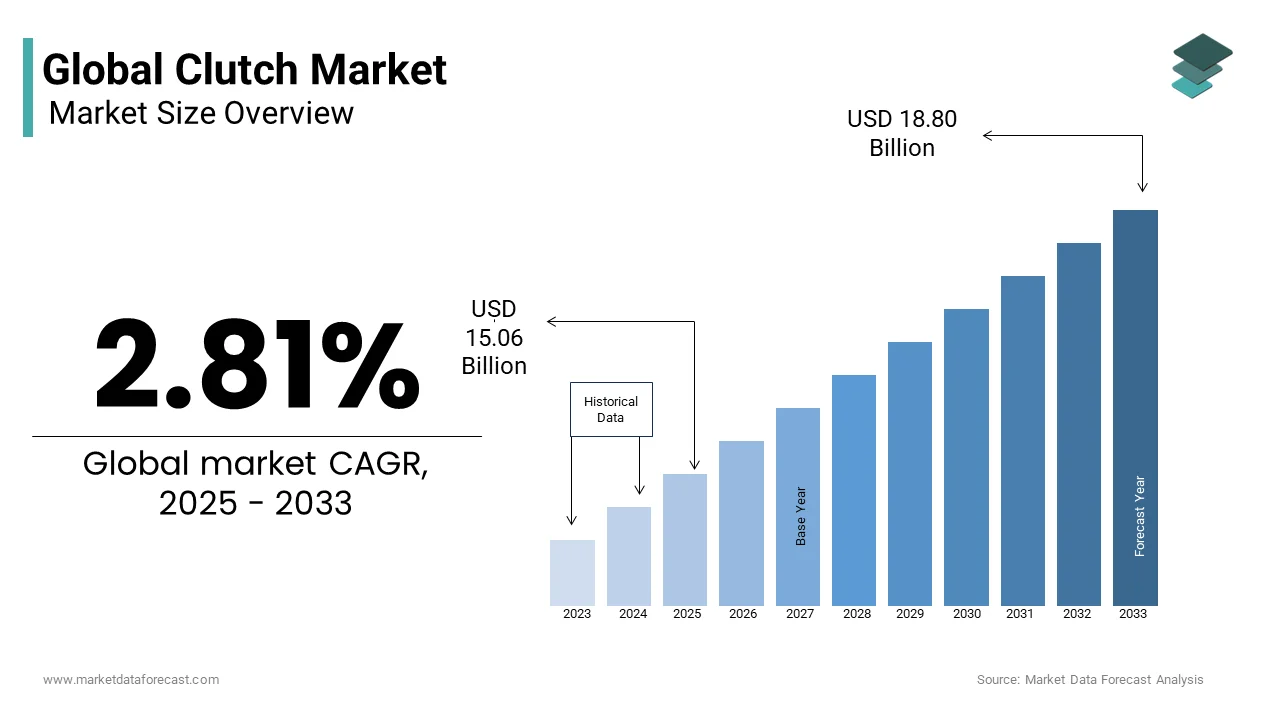

The global clutch market was valued at USD 14.65 billion in 2024, projected to reach USD 15.06 billion in 2025 and USD 18.80 billion by 2033, expanding at a CAGR of 2.81% during the forecast period. The demand for clutches continues to be driven by rising vehicle production, especially in emerging economies, and the steady adoption of manual and hybrid transmissions.

Key Market Trends

- Rising demand for passenger vehicles is driving clutch adoption.

- Increasing use of hybrid vehicles requires advanced clutch systems.

- Ongoing shift toward automated and dual-clutch transmission technology.

- Growth of Asia-Pacific as a leading hub for automotive manufacturing.

Segmental Insights

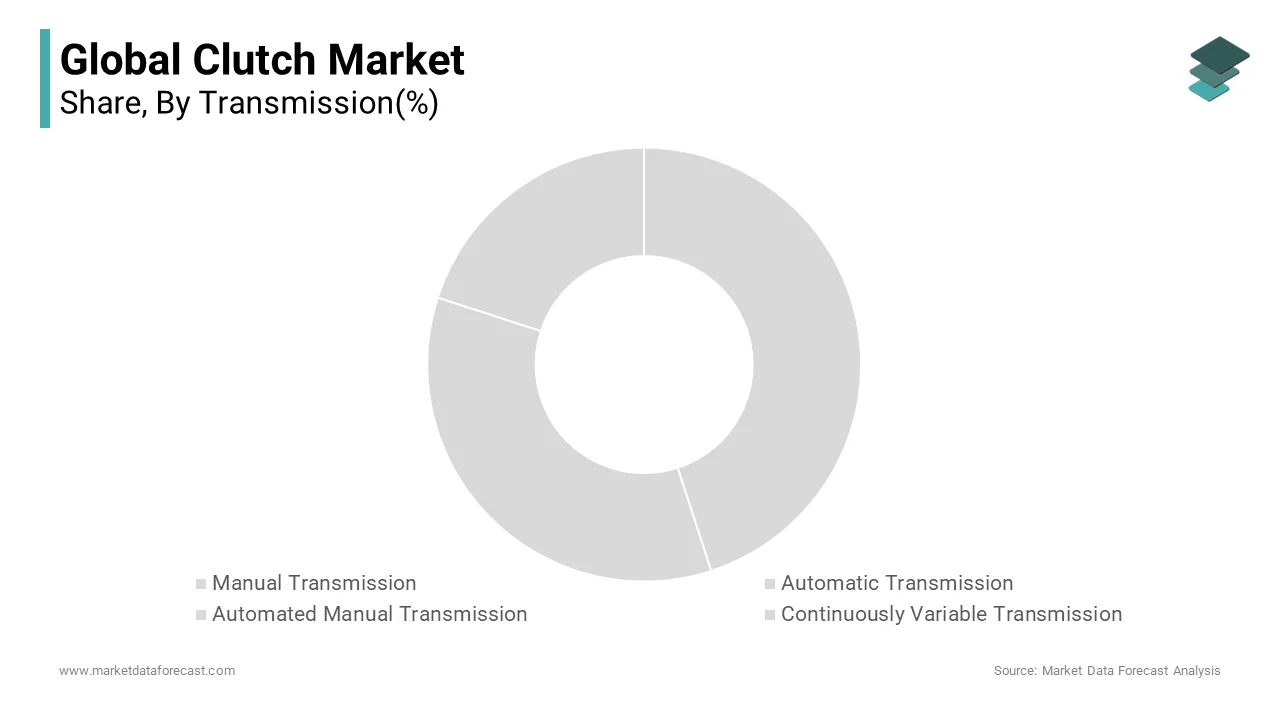

- Based on Transmission, the manual transmission segment dominated the clutch market with 54.2% share in 2024.

- Based on Clutch Size, the 9 to 10-inch disc segment led the market with 42.4% share in 2024.

- Based on Vehicle Type, the passenger vehicles segment held the largest market share at 54.3% in 2024.

Regional Insights

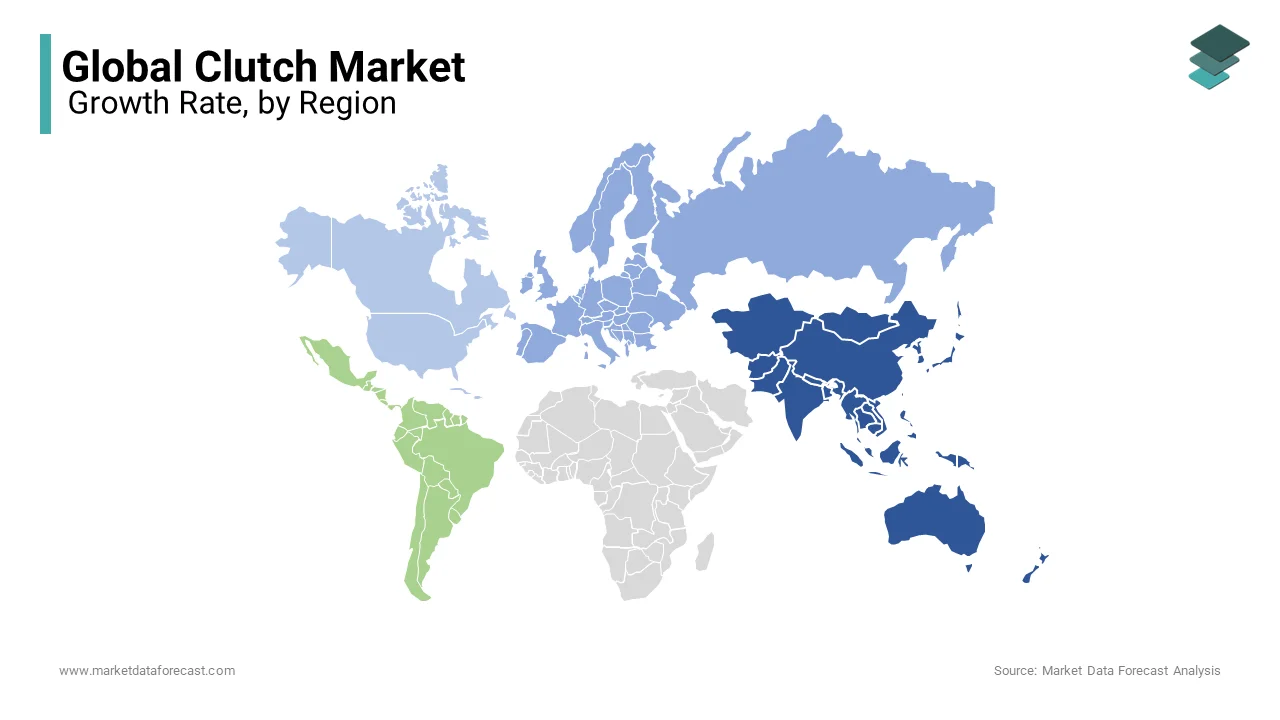

- Asia Pacific was the top performer in the clutch market, capturing 43.5% share in 2024, driven by high vehicle production and demand.

- Europe continues to grow with innovations in transmission systems and hybrid vehicles.

- North America remains steady, supported by passenger vehicle demand and aftermarket services.

- Latin America and the Middle East & Africa show moderate but consistent growth in vehicle sales.

Competitive Landscape

Key companies in the global clutch market include Aisin Seiki Co., Ltd., BorgWarner Inc., Clutch Auto Limited, Eaton Corporation PLC, Exedy Corporation, F.C.C. Co., Ltd., NSK Ltd., Schaeffler AG, Valeo S.A., and ZF Friedrichshafen AG. These companies focus on developing advanced clutch technologies, expanding their global presence, and catering to the growing demand from the passenger and hybrid vehicle segments.

Global Clutch Market Size

The global clutch market size was valued at USD 14.65 billion in 2024 and is anticipated to reach USD 15.06 billion in 2025 and USD 18.80 billion by 2033, growing at a CAGR of 2.81% during the forecast period from 2025 to 2033.

A clutch refers to the mechanical components designed to engage and disengage power transmission between rotating shafts, primarily in automotive, industrial, and agricultural machinery. These systems are integral to vehicle drivetrains, enabling smooth gear transitions and torque control. Modern clutches are evolving with advancements in material science and automation, supporting performance demands across manual, automatic, and dual-clutch transmissions. Apart from these, the International Organization of Motor Vehicle Manufacturers indicates that commercial vehicle production was over 26.4 million units in the same year, further amplifying demand for heavy-duty clutch assemblies.

MARKET DRIVERS

Persistent demand for commercial vehicles in emerging economies, where freight transportation infrastructure is expanding rapidly, is driving the growth of the lutch market. In India, commercial vehicle sales surged to 978,385 units in 2023, as reported by the Society of Indian Automobile Manufacturers, driven by e-commerce logistics and highway development projects. These vehicles require durable clutch mechanisms capable of withstanding frequent engagement cycles, with some long-haul trucks undergoing notable clutch actuations per day. Moreover, the expansion of cold chain logistics and intercity transport networks further intensifies demand for reliable torque transfer systems. This positions commercial vehicle growth as an important driver for clutch innovation and volume production.

The rising adoption of high-performance and specialty clutches in off-road and agricultural machinery, where operational conditions demand superior durability and thermal resistance, is driving the growth of the clutch market. Modern agricultural tractors, particularly those above 100 horsepower, utilize multi-disc wet clutches capable of handling peak torques exceeding 1,500 Nm.. Apart from these, according to a study, global production of construction equipment reached 5.8 million units in 2023. For instance, hydraulic excavators use a system of hydraulic pumps and directional control valves to manage the flow of pressurized fluid, which powers the cylinders and motors for implement operation and directional control.

MARKET RESTRAINTS

The accelerating shift toward electric vehicles (EVs) is restricting the growth of the clutch market. As per the International Energy Agency, over 14 million electric cars were sold globally in 2023, representing 18% of all new car sales, a figure projected to reach 35% by 2030. Unlike internal combustion engine vehicles, most battery-electric vehicles utilize single-speed transmissions without clutch pedals or manual engagement systems, which drastically reduces per-vehicle clutch content. Tesla’s Model 3, for example, operates without a conventional clutch mechanism, relying instead on direct-drive systems. According to a study, widespread EV adoption could eliminate demand for millions of conventional clutches annually by 2030.

Volatility in raw material supply for friction materials and ferrous alloys is also hampering the growth of the lutch market. The global steel production in 2023 relied on iron ore inputs exceeding notable metric tons, with prices fluctuating year-on-year due to geopolitical disruptions and export restrictions. China, the largest producer of graphite, is a key component in friction linings, and imposed export controls in 2023 on certain advanced carbon materials, which is affecting supply chains for high-performance clutch facings. Clutch manufacturers such as ZF Sachs and Valeo have cited material cost inflation exceeding 15% in 2022–2023, with price renegotiations and delaying product launches, thereby constraining profitability and scalability.

MARKET OPPORTUNITIES

The integration of smart clutch systems within automated manual transmissions (AMTs) in commercial fleets is attributed to leveraging the growth of the clutch market. As per the International Transport Forum, heavy-duty trucks equipped with AMTs demonstrate up to 5% improvement in fuel economy compared to conventional manual systems due to optimized shift timing and reduced clutch slippage. According to a study, a portion of its new Freightliner Cascadia units in North America were ordered with Allison fully automatic transmission configurations, which use a torque converter instead of an electronically actuated clutch and incorporate adaptive learning algorithms.

The development of hybrid-compatible clutch systems designed for high-torque and dual-power-source drivetrains is another factor fuelling the growth of the clutch market. As per the study, global production of hybrid electric vehicles reached millions of units, with many models utilizing specialized clutch mechanisms to manage transitions between internal combustion and electric propulsion. According to research, hybrid clutches must endure more thermal stress than conventional units due to frequent start-stop cycles and regenerative braking integration.

MARKET CHALLENGES

The escalating regulatory burden on emissions and lifecycle sustainability is compelling redesigns of traditional friction materials, which are challenging the growth of the clutch market. A portion of conventional brake and clutch friction formulations contains substances of very high concern (SVHCs), including copper and asbestos derivatives, which are being phased out under REACH regulations. This regulatory shift forces manufacturers to invest in alternative materials. These require advanced sealing and dust containment systems that add complexity to design and assembly.

The growing skills gap in precision manufacturing and clutch calibration in regions experiencing rapid industrialization additionally restrict the growth of the clutch market. As per a study, improper clutch alignment during assembly increases wear rates, reducing operational lifespan. In India, the National Skill Development Corporation identified a deficit of trained automotive technicians capable of servicing advanced transmission systems, including dual-clutch and automated manual units. This technical shortfall impedes aftermarket service quality and weakens consumer confidence in clutch longevity. Moreover, OEMs report that a portion of warranty claims for clutch assemblies are attributable to installation errors rather than component defects, emphasizing the urgent need for standardized training and certification in clutch system integration.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 2.81% |

| Segments Covered | By Transmission, Clutch Size, Vehicle, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Aisin Seiki Co., Ltd., Borgwarner Inc., Clutch Auto Limited, Eaton Corporation PLC, Exedy Corporation, F.C.C. Co., Ltd., NSK Ltd., Schaeffler AG., Valeo S.A., ZF Friedrichshafen AG., Eaton Corporation PLC, Exedy Corporation. |

SEGMENTAL ANALYSIS

By Transmission Insights

The manual transmission segment dominated the clutch market by capturing 54.2% of the global market share in 2024. Its widespread adoption across cost-sensitive markets and high-volume vehicle production in emerging economies is primarily driving the growth of the manual transmission segment. The continued prevalence of manual transmissions in compact and subcompact passenger vehicles, which accounted for a portion of new car sales in India, as per study research, is also driving the growth of the manual transmission segment. Apart from these, in Southeast Asia, motorcycles and three-wheelers, vehicles that almost exclusively use manual clutch systems, were fitted with wet multi-plate clutches, according to research. The affordability and mechanical simplicity of manual systems reduce manufacturing costs compared to automated alternatives, as per a study.

The Automated Manual Transmission (AMT) segment is predicted to witness the highest CAGR of 7.9% from 2025 to 2033 due to its adoption in commercial fleets seeking operational efficiency without the high cost of full automatics. In Europe, AMT penetration in heavy-duty trucks surged, as per a study, driven by fuel savings and reduced driver fatigue. Daimler Trucks North America reported that its Freightliner models equipped with AMT achieved an improvement in fuel economy due to optimized shift logic and minimized clutch slip. Urban logistics electrification, where AMTs are being adapted for hybrid delivery vans, is also driving the growth of the Automated Manual Transmission (AMT) segment. According to research, last-mile delivery vehicle production with AMT integration rose, particularly in models. These systems offer seamless torque management between electric motors and internal combustion engines, enabling smoother transitions and reduced wear.

By Clutch Size Insights

The 9 to 10-inch disc segment led the clutch market by capturing 42.4% of the global market in 2024. The growth of the 9 to 10-inch disc segment is driven by its optimal balance between torque capacity and spatial efficiency, which makes it ideal for mid-sized passenger vehicles and light commercial applications. The Honda Civic, Toyota Corolla, and Volkswagen Jetta are bestsellers in their category, with their mass-scale demand driven by efficient and reliable automatic transmissions. Their standardized dimensions also facilitate interchangeability across platforms, which reduces OEM tooling costs.

The 11-inch and above disc segment is estimated to register the fastest CAGR of 8.3% over the forecast period, owing to the rising production of heavy-duty vehicles and high-performance machinery requiring superior torque transmission. According to research, in 2021, major manufacturers like Caterpillar and Komatsu produced a wide variety of construction and mining equipment, including heavy machinery with engine power exceeding 2,000 horsepower. The use of a dual-disc setup is common and correct for heavy-duty applications, as it provides more friction area for increased torque capacity, as per a study. Apart from these, according to a study, average engine torque in long-haul freight trucks increased, necessitating larger clutch assemblies to manage higher power output and prevent clutch slippage. Moreover, the expansion of mega-mining operations in Australia and Chile has spurred demand for ultra-heavy clutches. These applications demand extreme durability, which directly accelerates demand for oversized clutch units.

By Vehicle Insights

The passenger vehicles segment led the clutch market by capturing 54.3% of the global market share in 2024. The growth of the passenger vehicles segment is driven by the sheer volume of internal combustion engine (ICE) passenger cars still in production and operation worldwide. According to research, despite the rise of electric vehicles, millions of ICE-powered passenger cars were manufactured. Furthermore, the average lifespan of a passenger car clutch is notable km, leading to substantial aftermarket replacement demand. According to a tudy, global clutch aftermarket sales for passenger vehicles were notable, with Asia Pacific contributing a portion due to high vehicle utilization rates. The continued affordability of manual systems, coupled with consumer familiarity, ensures their persistence even as transmission technologies evolve, particularly in regions where cost sensitivity outweighs automation preferences.

The Heavy Commercial Vehicles (HCVs) segment is predicted to witness the highest CAGR of 8.1% from 2025 to 2033. The growth of the Heavy Commercial Vehicles (HCVs) segment is driven by escalating freight transport volumes and infrastructure development in emerging economies. According to research, global freight ton-kilometers increased, with road transport accounting for a portion of inland movement. In India, HCV sales surged, driven by national highway expansion and logistics modernization. Apart from these, as per the European Environment Agency, a portion of EU freight is moved by road, with growing demand for automated clutch systems in long-haul fleets to improve driver efficiency and reduce emissions through optimized gear changes.

REGIONAL ANALYSIS

Asia Pacific was the top performer in the global clutch market in 2024 and accounted for 43.5% of the global market share in 2024. The domination of the Asia Pacific in the global market is primarily driven by the region’s status as the world’s largest automotive production center, with China and India alone manufacturing millions of vehicles annually, as per research. The dominance of manual transmissions in compact cars and two-wheelers, where a portion of motorcycles use manual clutches, fuels consistent demand. According to the study, Japan remains a key exporter of high-precision clutch components, supplying a portion of global dual-mass flywheel assemblies. Moreover, India's commercial vehicle market is seeing overall growth and long-term expansion, as per research. The presence of major OEMs like Tata Motors, Ashok Leyland, and Mahindra, coupled with a growing aftermarket network, ensures sustained investment in clutch technology and localized production. This strengthens the Asia Pacific’s central role in the global supply chain.

Europe is the second-largest in the clutch market due to its advanced engineering base and early adoption of automated transmission technologies. The region is a pioneer in developing high-efficiency clutch systems for passenger and commercial vehicles, with Germany alone hosting leading manufacturers such as ZF, Schaeffler, and BorgWarner’s European R&D centers. As per the study, a portion of new passenger cars in Western Europe are now equipped with automated manual or dual-clutch transmissions, driving demand for sophisticated electro-hydraulic clutch modules. Furthermore, as per the study, a portion of heavy-duty trucks produced in the EU are fitted with AMTs, strengthening the region’s place in next-generation clutch integration and setting global benchmarks for performance and sustainability.

North America grew steadily in the clutch market. The growth of North America in the global market share is driven by a mature automotive industry and high demand for durable, high-torque systems. The United States is the primary contributor, with millions of light and heavy vehicles produced, according to the study. While automatic transmission dominance limits manual clutch volume, the heavy-duty trucking sector sustains demand for industrial-grade clutches. According to a study, the U.S. freight industry logged 329.86 billion miles in 2023, placing immense stress on transmission systems and increasing replacement cycles. Eaton Corporation notes that Class 8 trucks in North America undergo clutch replacement every 500,000 miles on average, translating to a steady aftermarket stream. Apart from these, the resurgence of manual transmission in performance vehicles, such as the Chevrolet Corvette and Ford Mustang, has preserved niche demand.

Latin America is expected to be the most lucrative region in the clutch market, with Brazil emerging as the regional epicenter for clutch manufacturing and consumption. The country produced a large number of vehicles, as per a study, the majority of which were manual transmission models tailored to cost-conscious consumers. Brazil has historically been a strong market for manual transmission vehicles due to affordability, but automatic transmissions have recently surpassed manuals in new passenger car sales. Moreover, the agricultural sector drives industrial clutch usage. Brazil operatesseveralf tractors, many equipped with multi-disc wet clutches for continuous operation in sugarcane and soybean harvesting, according to the study. Argentina and Mexico also contribute through growing light commercial vehicle production.

The Middle East & Africa are likely to grow in the clutch market. The growth of the Middle East & Africa in the global market is driven by infrastructure expansion and fleet modernization. Saudi Arabia’s Vision 2030 initiative has spurred massive investments in construction and transportation. This has increased demand for heavy equipment and commercial vehicles, many of which rely on robust clutch systems. According to the research, equipment rentals in the GCC region grew, particularly for excavators and bulldozers using multi-plate clutches. However, logistical challenges and inconsistent power supply hinder large-scale industrialization, which limits immediate market expansion despite underlying structural demand.

KEY MARKET PLAYERS

Aisin Seiki Co., Ltd., Borgwarner Inc., Clutch Auto Limited, Eaton Corporation PLC, Exedy Corporation, F.C.C. Co., Ltd., NSK Ltd., Schaeffler AG., Valeo S.A., ZF Friedrichshafen AG., Eaton Corporation PLC, Exedy Corporation. Are the market players that are dominating the global clutch market?

Top Players In The Market

Schaeffler Group is a leading force in the global clutch market, with deep technological expertise in friction systems and transmission solutions. In the Asia Pacific region, the company has established advanced manufacturing facilities in India and China, enabling localized production for OEMs such as Tata Motors and SAIC. Schaeffler has intensified its focus on high-efficiency dual-mass flywheels and automated clutch actuators by aligning with regional demand for smoother gear shifts and reduced NVH.

BorgWarner Inc. holds a prominent position in the clutch market through its advanced drivetrain technologies and strategic regional investments. In the Asia Pacific region, the company operates multiple engineering and production centers, including in Bangalore and Wuhan, supporting key clients like Hyundai, Nissan, and Mahindra. BorgWarner has been instrumental in advancing automated manual transmission (AMT) clutch systems tailored for heavy-duty trucks and buses in India and Southeast Asia. The company also expanded its friction material testing laboratory in Pune to accelerate the development of low-emission, durable clutch facings compliant with evolving environmental regulations. These initiatives emphasize BorgWarner’s commitment to localized innovation and long-term engagement with Asia Pacific’s evolving transportation ecosystem.

ZF Friedrichshafen AG is a major contributor to the clutch market, particularly in commercial and industrial applications across the Asia Pacific. The company supplies integrated clutch and transmission systems to leading truck and bus manufacturers in China, Japan, and India, including Dongfeng and Ashok Leyland. ZF’s focus on automated manual transmissions like its Ecolife series has significantly influenced urban transit fleets in cities such as Jakarta and Mumbai, where fuel efficiency and driver ease are important. The company also partnered with several Chinese electric bus makers to adapt its clutch technologies for hybrid-electric drivelines, demonstrating agility in responding to regional electrification trends. These efforts strengthen ZF’s reputation as a technology-forward player deeply embedded in Asia Pacific’s commercial mobility transformation.

Top Strategies Used By The Key Market Participants

Key players in the clutch market are deploying strategic initiatives such as technological innovation, regional expansion, product portfolio diversification, partnerships with OEMs, and investment in sustainable materials. Companies are intensifying R&D to develop clutches compatible with hybrid and automated transmissions in high-growth markets. Localization of production is a dominant strategy, reducing lead times and tariffs while improving responsiveness to customer needs. Major firms are also acquiring niche technology providers to enhance capabilities in electronic clutch control and predictive maintenance systems. Apart from these, collaborations with research institutions are accelerating the development of asbestos-free friction materials and thermally resilient composites. Digital integration, including IoT-enabled clutch health monitoring, is being adopted to differentiate offerings in competitive commercial vehicle segments. These strategies collectively enhance agility, compliance, and value proposition in a rapidly evolving mobility landscape.

COMPETITION OVERVIEW

The competition in the clutch market is intensifying as established players and regional manufacturers vie for dominance across the automotive and industrial sectors. While global giants leverage technological superiority and extensive R&D networks, regional suppliers in the Asia Pacific and Latin America are gaining ground through cost-efficient production and localized service models. Differentiation is increasingly driven by innovation in materials, integration with automated transmissions, and compliance with environmental regulations. Strategic alliances with OEMs, especially in commercial and hybrid vehicle segments, are shaping competitive dynamics. Moreover, the shift toward electrification is forcing traditional clutch manufacturers to pivot toward hybrid-compatible systems or risk obsolescence.

MARKET SEGMENTATION

This research report on the global clutch market is segmented and sub-segmented into the following categories.

By Transmission Type

- Manual Transmission

- Automatic Transmission

- Automated Manual Transmission

- Continuously Variable Transmission

By Clutch Disc Size

- Below 9 Inches Disc

- 9 to 10 Inches Disc

- 10 to 11 Inches Disc

- 11 Inches & Above Disc

By Application Type

- Segment Type Size and Market Share Analysis

- Application Revenue and Trends by Type of Application

- Application Segment Analysis by Type

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What’s a clutch, and why is it in my car?

A clutch is what lets drivers change gears smoothly in vehicles with manual or semi-automatic transmissions. It’s the handshake between your engine and wheels—when you press the pedal, the clutch disconnects power so you can shift gears without grinding metal.

Why does everyone talk about “dual-clutch” these days?

Drivers (and automakers) love dual-clutch systems because they make shifting almost instant, more like a racing car than a commuter’s sedan. They’re super popular for performance cars and now spreading into everyday vehicles for smoother rides and better fuel efficiency.

Is the clutch market shrinking because of electric cars?

A little, yes. Electric vehicles don’t use traditional clutches, since their motors don’t need shifting. But hybrids, trucks, and many global cars still rely on clutch technology, and engineers are developing cool new electronic and adaptive clutch systems.

Who are the big players in this industry?

Names like Schaeffler, Valeo, BorgWarner, Exedy, and ZF Friedrichshafen AG might not mean much to everyday drivers, but they’re the companies building the clutches that keep cars on the road worldwide.

What’s happening in Asia-Pacific?

This region (think China, India, Japan) builds and buys more cars than anywhere else, so its clutch market is booming. Both OEMs (new cars) and the aftermarket (replacement parts) are huge business here.

What’s making clutches greener?

Manufacturers are experimenting with lighter, more durable materials and smarter electronic controls. The goal: better mileage, fewer emissions, and less wear-and-tear over time.

Will automatic and hybrid cars put manual clutches out of business?

Manuals are less common in Europe and North America, but demand remains strong in Asia, Africa, and South America. Many commercial vehicles and trucks still need robust clutch systems, and even automatics use specialized clutch packs.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com