Global Commercial Aircraft Aerostructures Market Size, Share, Trends, & Growth Forecast Report, Segmented By Component, Material Type, Aircraft Type, End-user, And Region (North America, Europe, Asia Pacific, Latin America, Middle East And Africa), Industry Forecast From 2025 to 2034

Global Commercial Aircraft Aerostructures Market Size

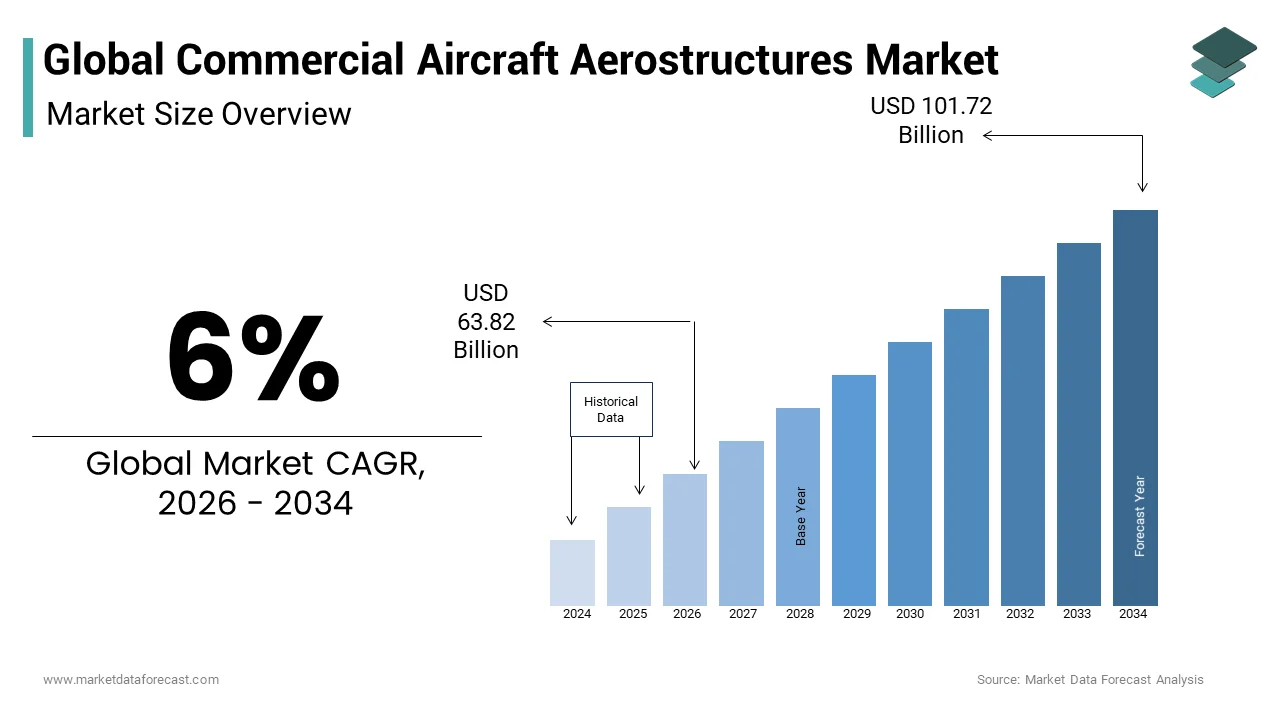

The global commercial aircraft aerostructures market size will reach USD 60.21 billion in 2025 and is anticipated to reach USD 63.82 billion in 2026 to reach USD 101.72 billion by 2034, growing at a CAGR of 6% during the forecast period from 2026 to 2034.

The aerostructure is an essential part of commercial aircraft. Demand and the growth of the aircraft market depend primarily on the delivery of commercial aircraft aerostructures. Advances in design, materials, and processes have helped the industry grow faster by meeting the needs of the airlines. The structure of the aircraft represents more than 30% of the total production value of the plane, followed by aviation engines, avionics, systems, and electronics, and interiors. The growing wealth of emerging economies, which causes access to air traffic, is an essential factor that leads to increased passenger traffic or travel per capita around the world. This creates demand for new aircraft, boosting the global commercial aircraft aerostructures market.

MARKET DRIVERS

The main driver that influences the growth of the Commercial Aircraft Aerostructures Market is the increase in OEMs in the outsourcing of aviation structures manufacturing as primary and secondary suppliers.

A trend that can affect the competitive dynamics of the market is expected to change in the manufacturing of the Commercial Aircraft Aerostructures of OEM-level players. In 2018, we saw a series of high-value-added M&A activities in the industry. The global commercial aircraft aerostructures market is driven primarily by the growing supply of commercial aircraft worldwide. As passenger mobility has increased in recent years, the commercial aircraft aerostructures industry is experiencing significant growth in the speed of deployment of commercial aviation, which actively drives and supports the growth of the global Commercial Aircraft Aerostructures Market.

In addition, it has been observed that the aircraft manufacturing industry is mainly adopting outsourcing methodologies for the manufacture of large-scale and high-speed aviation structures, thus accelerating the growth of the global Commercial Aircraft Aerostructures Market. In addition to these factors, the development and adoption of composite materials for aircraft manufacturing are accelerating the growth of the global Commercial Aircraft Aerostructures Market and are expected to lead the market during the forecast period.

MARKET RESTRAINTS

However, problems associated with compounds, such as recycling of materials, are expected to slow the growth of the Commercial Aircraft Aerostructures Market during the forecast period.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6% |

| Segments Covered | By Component, Material Type, Aircraft Type, End-user, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | GKN PLC, Spirit AeroSystems Inc., Korean Aerospace Industry, UTC Aerospace Systems, Triumph Group, Premium Aerotech GmbH, Mitsubishi Aircraft Corporation, Safran SA, |

SEGMENTAL ANALYSIS

By Aircraft Insights

The global commercial aircraft aerostructure market is divided into narrow-body airplanes, wide-body airplanes, extra-large airplanes, regional airplanes, general aviation, helicopters, military airplanes, and unmanned aerial vehicles. The narrow-body segment is likely to be the leader of the market during the forecast period. Wide-body airplanes are expected to remain the second-largest segment during the forecast period and grow at an impressive rate.

By Material Insights

The global commercial aircraft aerostructures business is divided into metallic aerostructures and composite aerostructures. The metal structures of the aircraft are assumed to remain as larger segments, while composite aircraft structures are foreseen to show higher growth over the next five years. Passenger planes are actively seeking lightweight composite parts that can contribute to the goal of achieving more excellent fuel economy and reducing emissions.

By Application Insights

The global market is divided into fuselage, wings, containers, gondolas, and pylons. The fuselage is projected to remain the most extensive application in the commercial aircraft aerostructures market during the prediction period. The fuselage is the main component of the aircraft and covers the body part of the plane.

REGIONAL ANALYSIS

Regionally, the Commercial Aircraft Aerostructures Market has been categorized into North America, Europe, Asia Pacific, and other regions (RoW). North America is expected to remain the largest market during the forecast period, led by the United States. The country is the center of commercial aircraft aerostructures with multi-level players and aircraft OEMs.

The Asia-Pacific region is likely to have the highest growth rate during the forecast period. The area will soon remain the most striking market in the future due to the upcoming commercial and regional aircraft, such as the C919 and MRJ, and the opening of assembly plants in China by Boeing and Airbus, and the larger size of the advertising fleet. Countries such as China, India, and Japan are increasingly investing in the development of general aviation aircraft.

Leading Company

Developing lightweight structures, accelerating production rates, acquisitions, and working with OEMs for the joint development of aviation structures are some of the strategies that Spirit AeroSystems Inc. has adopted to remain competitive in this industry.

KEY MARKET PLAYERS

Major Commercial Aircraft Aerostructures Market companies include

- GKN PLC

- Spirit AeroSystems Inc.

- Korean Aerospace Industry

- UTC Aerospace Systems

- Triumph Group

- Premium Aerotech GmbH

- Mitsubishi Aircraft Corporation

- Safran SA

- STELIA Aerospace SAS

- Leonardo SPA

- FACC AG

- Kawasaki Heavy Industries

- Subaru Corporation.

RECENT MARKET NEWS

- In June 2019, Virgin Atlantic announced that it had ordered up to 20 Airbus A330-900neos. The airline has firmly ordered 14 additional A330-900neos with six options. Airplane delivery is expected to begin in 2021.

- June 2019 Qantas Airways Ltd. Qantas has converted 26 orders for A321neo aircraft to A321 XLR. Qantas has also expanded to order an additional 10 XLR A321 for $ 1.4 billion.

- In September 2019, KLM Royal Dutch Airlines ordered $ 770 million for two B777-300ER aircraft.

- The Korean KAI aerospace industry (KAI) is a major supplier of Airbus and manufactures aeronautical structures, including the A350 XWB fuselage, wings, cargo doors, and landing gear, and Sharklet wing tip devices for A320 aircraft and A330neo.

MARKET SEGMENTATION

This research report on the global commercial aircraft aerostructures market is segmented and sub-segmented into the following categories.

By Component

- Fuselage

- Wings

- Empennage

- Nacelles & Pylons

- Flight Control Surfaces

- Doors & Skids

- Noses

By Material

- Composites

- Metal Alloys

- Alloys & Superalloys

- Hybrid Materials

By Aircraft Type

- Narrow-Body Aircraft

- Wide-Body Aircraft (Regional & Business Jets

- Very Large Aircraft

- Helicopters

- Military Aircraft

- Unmanned Aerial Vehicles

- Advanced Air Mobility (AAM) Vehicles

By End User

- Original Equipment Manufacturer (OEM)

- Aftermarket (Maintenance, Repair, and Overhaul - MRO)

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What is currently driving growth in the global commercial aircraft aerostructures market?

Increasing aircraft production and rising air passenger traffic are driving market growth.

Why are aerostructures important in commercial aircraft manufacturing?

They form the structural framework that supports the entire aircraft.

How would you explain aerostructures in simple terms?

They are the physical parts of an aircraft such as wings, fuselage, and tail sections.

Where are aerostructures most commonly used in aircraft?

They are widely used in fuselage, wings, empennage, and structural components.

What makes aerostructures essential for aircraft performance?

They provide strength, stability, and aerodynamic efficiency.

From an industry perspective, are aerostructures a critical investment?

Yes, they are fundamental to aircraft safety and operational efficiency.

What challenges are affecting the global commercial aircraft aerostructures market?

High manufacturing costs and supply chain disruptions are key challenges.

How is air travel demand influencing this market?

Growing passenger demand is increasing aircraft production and component requirements.

Which aircraft segments contribute the most to aerostructure demand?

Narrow-body and wide-body commercial aircraft are major contributors.

Is the global commercial aircraft aerostructures market growing steadily?

Yes, it is expanding with increasing fleet expansion and modernization.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com