Global Corrosion Inhibitors Market Size, Share, Trends, & Growth Forecast Report - Segmented By Product (Organic, Inorganic), End-User (Power Generation, Oil and Gas, Pulp and paper, Metal processing, Water Treatment, and Others), Type (Water-Based, Oil-Based), and Region (North America, Europe, Asia Pacific, Latin America, Middle east and Africa) – Industry Analysis From 2026 to 2034

Market Size, 2025

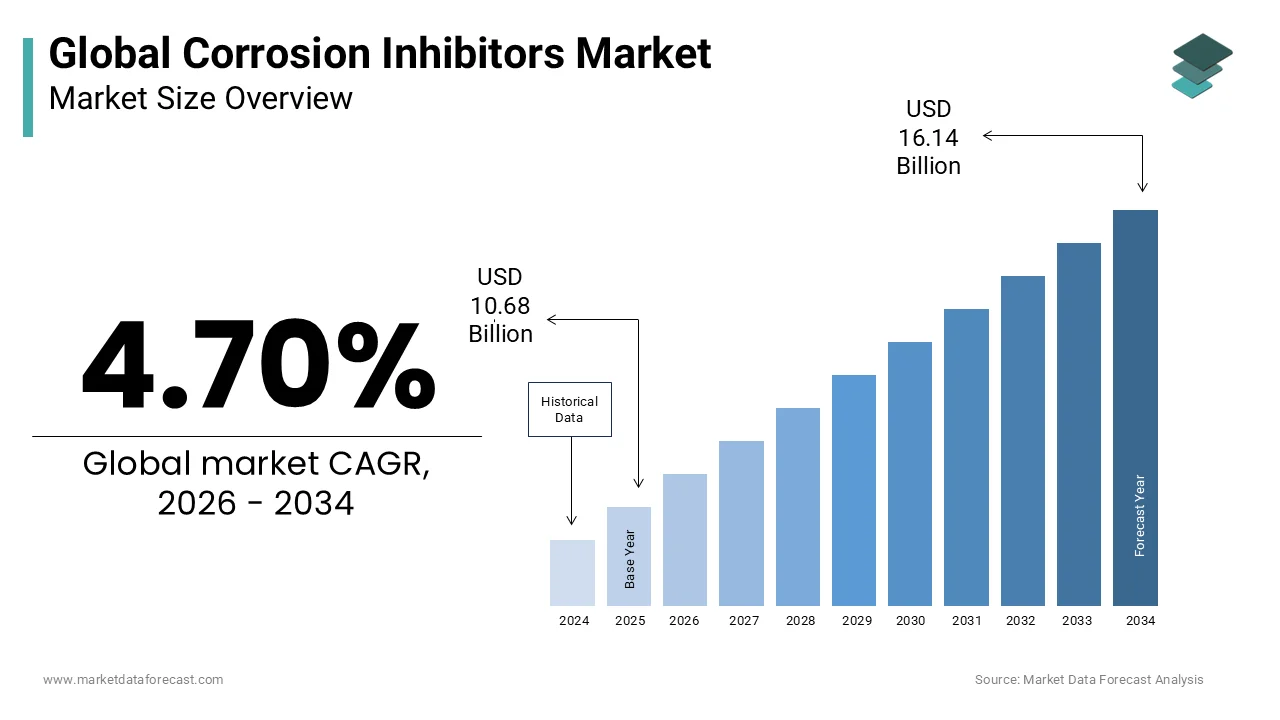

$10.68 BnMarket Estimate, 2026

$11.18 BnMarket Forecast, 2034

$16.14 BnCAGR, 2026–2034

4.70%Global Corrosion Inhibitors Market Size

The global corrosion inhibitors market size was valued at USD 10.68 billion in 2025, and is projected to reach USD 16.14 billion by 2034 from USD 11.18 billion in 2026, growing at a CAGR of 4.70%.

Corrosion inhibition is an effective way of protecting metals' internal corrosion, which, when an inhibitor is added in small concentrations, provides temporary protection. The polymers are used as corrosion inhibitors in a functional group substance that acts as additives that inhibit the fluids surrounding the metal or associated object and decrease the metal oxidation rate. Organic corrosion inhibitors are carbon compounds used for surface adsorption, which form a film, but sometimes act as cathodic and anodic inhibitors.

The growing construction, power generation, and metal processing industry in developing and developed economies is a major factor that is expected to drive the global corrosion inhibitors market's revenue growth during the forecast period. In addition, the increasing use of corrosion inhibitors to reduce equipment maintenance costs is expected to drive the revenue growth of the target market.

MARKET DRIVERS

Growing energy demand with rising population and increasing urbanization are driving the need for efficient power infrastructure in order to meet the demand for electricity. The oil & gas industry also accounts for a significant share in the global corrosion inhibitors market which also propels the market growth. Increasing exploration of reserves with growing production of shale gas from unconventional reserves is expected to drive corrosion inhibitors' demand over the forecast period—rising investments in the power sector. Changing preference toward environment-friendly corrosion inhibitors drives the market growth.

MARKET RESTRAINTS

Fluctuating commodity prices, coupled with environmental concerns, will hamper the growth of the corrosion inhibitor market. Low oil prices and slowing demand for fossil fuels due to the growing trend towards renewable energy sources are expected to restrict the demand for fossil fuels, which in turn is expected to affect the demand for corrosion inhibitors during the forecast period (2025 to 2033). The increasing usage of the product leads to the removal of harmful materials such as zinc, chromium, and phosphorus, which is expected to slow down the corrosion inhibitor market revenue growth during the forecast period.

MARKET OPPORTUNITIES

The growing need to effectively reduce the corrosion rate of a metal exposed to any environment will further stimulate several opportunities, which will lead to the growth of the Corrosion Inhibitors market during the forecast period.

MARKET CHALLENGES

Freedonia predicts that due to the increased challenges facing corrosion inhibitors, water treatment companies and other suppliers will continue to be successful with higher-value products that incorporate multifunctional additives and protect equipment in the industry. As a result, users are increasingly choosing more advanced multifunctional products that can minimize corrosion and extend equipment life in these harsh environments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.70% |

| Segments Covered | By Product, End-User, Type, And Region. |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

| Market Leaders Profiled | GE Water, BASF SE, Dai-Ichi Karkaria Ltd, AkzoNobel, Cortec Corporation, Champion Technologies Inc, Ashland Inc, Henkel, Dow Chemical Co, W.R Grace Co., Solutia Inc, Daubert Cromwell LLC, Ecolab |

SEGMENTAL ANALYSIS

By Product Insights

The organic segment had the largest market share of 82.8% in 2024. In recent years, there has been a significant development regarding corrosion inhibitors of biological origin. These are inexpensive, have low toxicity, and are readily available organic compounds, which are obtained from plant extracts such as aromatic herbs, spices, and medicinal plants. In general, corrosion inhibitors of biological origin have aromatic structures with long aliphatic chains and free electron pairs. For example, Delonix regia and rosemary leaves prevent the deterioration of metallic aluminum, while natural honey inhibits the corrosion of copper. The above-mentioned factors are expected to drive the growth of the segment during the forecast period.

Coating with an inorganic inhibitor is one of the traditional and simple ways to increase a metal's passivity. Some of the metals most commonly used as inorganic corrosion inhibitors include chromate, nitrate, molybdate, phosphate, and silicate salts of mercury, platinum, palladium, rhodium, rhenium, and iridium. Platinum group metals, including platinum, palladium, rhodium, and iridium, are thermodynamically stable on the pH scale because they are not attacked by non-oxidizing acidic solutions and do not corrode when they are exposed to moisture-laden air. These properties of inorganic corrosion inhibitors are expected to contribute significantly to the demand for the product in the near future.

By End-User Insights

The global market size of corrosion inhibitors for power generation was estimated to be around USD 4 billion in 2024. The product is widely used in equipment used in power generation, such as gas turbines, switches, pumps, and electronic components. Population growth around the world translates into increasing demand for energy. This trend will stimulate industry in general for the end-use of power generation.

The oil and gas segment size is expected to register gains of over 7.5% CAGR during the projected period. The product finds wide application in industry, as components used in oil and gas exploration are exposed to extreme weather conditions and require corrosion protection. In addition, shale gas exploration in the United States and Russia will complement business growth by 2033. The oil and gas segment held the largest market share of 34.1% in 2024. This is attributed to the growing number of internal corrosion problems in pipelines, refineries, and petrochemical plants. The corrosion inhibitor market is gaining popularity in the power generation industry in developing economies in the Asia-Pacific region. In power plants, erosion has been one of the major factors leading to critical downtime. The steam circuits of nuclear, thermal, and hydroelectric power plants are liable to deteriorate because the metallic components are always in contact with water. To ensure efficient power generation, most power plants monitor parameters such as pH value, conductivity, and the presence of corrosive anions and cations, which indicate the rate of corrosion. In addition, they ensure the adequate presence of corrosion inhibitors such as phosphonates, phosphate, zinc (for steel), and triazoles (for copper).

By Type Insights

The water-based segment had the largest market share of 57.2% in 2024. Water-based corrosion inhibitors are readily soluble in water and are generally sold in solid form. They form a protective layer on the metal surface by modifying the surface's physical characteristics to resist oxidation of the metal surface, thus providing protection against rust. In addition, they are cost-effective, form a clear coat after drying, and can be easily applied by spraying, dipping, or brushing before subsequent operations.

Oil-based corrosion inhibitors are primarily preferred for long-term protection and harsh environmental conditions due to their massive film and significant hydrophobic properties. They are mainly based on the structure of thick coatings, which make contact between water and metal surfaces difficult. These are generally the most cost-effective ways to control corrosion, as they allow the use of less expensive metals, salts, or organic compounds in a corrosive environment.

REGIONAL ANALYSIS

Asia-Pacific held the largest market share of 37.3% in 2024 and is expected to be one of the fastest-growing markets in the near future. The growth of the market can be attributed to the rapid industrialization of the region, which has led to the demand for power generation and also several other end-use industries. Growing chemicals and metallurgy sectors in developing economies in the region, notably India and China, are also expected to contribute significantly to the market in the near future.

Europe is one of the main consumers of corrosion inhibitors due to the massive consumption of water for industrial sectors such as sugar and ethanol and the manufacture of petrochemicals. Water treatment issues in Europe play a critical role in directly impacting corrosion control operations while maintaining the operational integrity of heat transfer equipment and reducing adverse effects on the environment.

North America has dominated the inorganic corrosion inhibitor market due to the rapid growth of the oil and gas industry and increased shale gas exploration activity using maximum inorganic inhibitors. Asia-Pacific and Latin America are the fastest-growing markets and are expected to experience lucrative growth during the forecast period. This mainly contributes to the high demand for inorganic inhibitors from the water treatment, automotive, oil, and gas industries. In Europe, inorganic inhibitors are limited due to zinc presence, which impacts the environment.

KEY MARKET PLAYERS

GE Water, BASF SE, Dai-Ichi Karkaria Ltd, AkzoNobel, Cortec Corporation, Champion Technologies Inc, Ashland Inc, Henkel, Dow Chemical Co, W.R Grace Co., Solutia Inc, Daubert Cromwell LLC, Ecolab are some of the notable companies in the global corrosion inhibitors market.

MARKET SEGMENTATION

This research report on the global corrosion inhibitors market has been segmented and sub-segmented based on product, end-user, type, and region.

By Product

- Organic

- Inorganic

By End-User

- Power generation

- Oil and gas

- Pulp and paper

- Metal processing

- Water treatment

- Others

By Type

- Water-Based

- Oil Based

By Region

- North America

- Latin America

- Europe

- Asia-Pacific

- Middle East & Africa

Frequently Asked Questions

1. What are corrosion inhibitors?

Corrosion inhibitors are chemical substances added to liquids, gases, or coatings to reduce or prevent the corrosion of metal surfaces.

2. What is driving the growth of the corrosion inhibitors market?

Market growth is driven by increasing industrialization, rising infrastructure investments, growing demand for asset protection, and the need to reduce maintenance costs.

3. Which industries commonly use corrosion inhibitors?

Corrosion inhibitors are widely used in oil and gas, power generation, water treatment, manufacturing, automotive, marine, and construction industries.

4. How do corrosion inhibitors work?

They work by forming a protective layer on metal surfaces or by altering the chemical environment to slow down corrosion reactions.

5. What are the major types of corrosion inhibitors?

The main types include organic inhibitors, inorganic inhibitors, volatile corrosion inhibitors, anodic inhibitors, and cathodic inhibitors.

6. Why are corrosion inhibitors important in the oil and gas industry?

They help protect pipelines, storage tanks, drilling equipment, and processing facilities from corrosion, extending equipment life and reducing operational risks.

7. How are corrosion inhibitors used in water treatment systems?

They are added to cooling towers, boilers, and water distribution systems to prevent corrosion and maintain system efficiency.

8. What role does infrastructure development play in the corrosion inhibitors market?

Growing investments in bridges, buildings, transportation networks, and industrial facilities increase the demand for corrosion protection solutions.

9. What challenges does the corrosion inhibitors market face?

Challenges include stringent environmental regulations, fluctuations in raw material prices, and the need for continuous product innovation.

10. What trends are shaping the corrosion inhibitors market?

Key trends include the development of green inhibitors, advancements in corrosion monitoring technologies, increased industrial automation, and demand for high performance protection solutions.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com