Global Crab Market Size, Share, Trends, & Growth Forecast Report Segmented By Type (Red King Crab, Blue King Crab, and other), and Region (Latin America, North America, Asia Pacific, Europe, Middle East and Africa), Industry Analysis from 2025 to 2033

Global Crab Market Summary

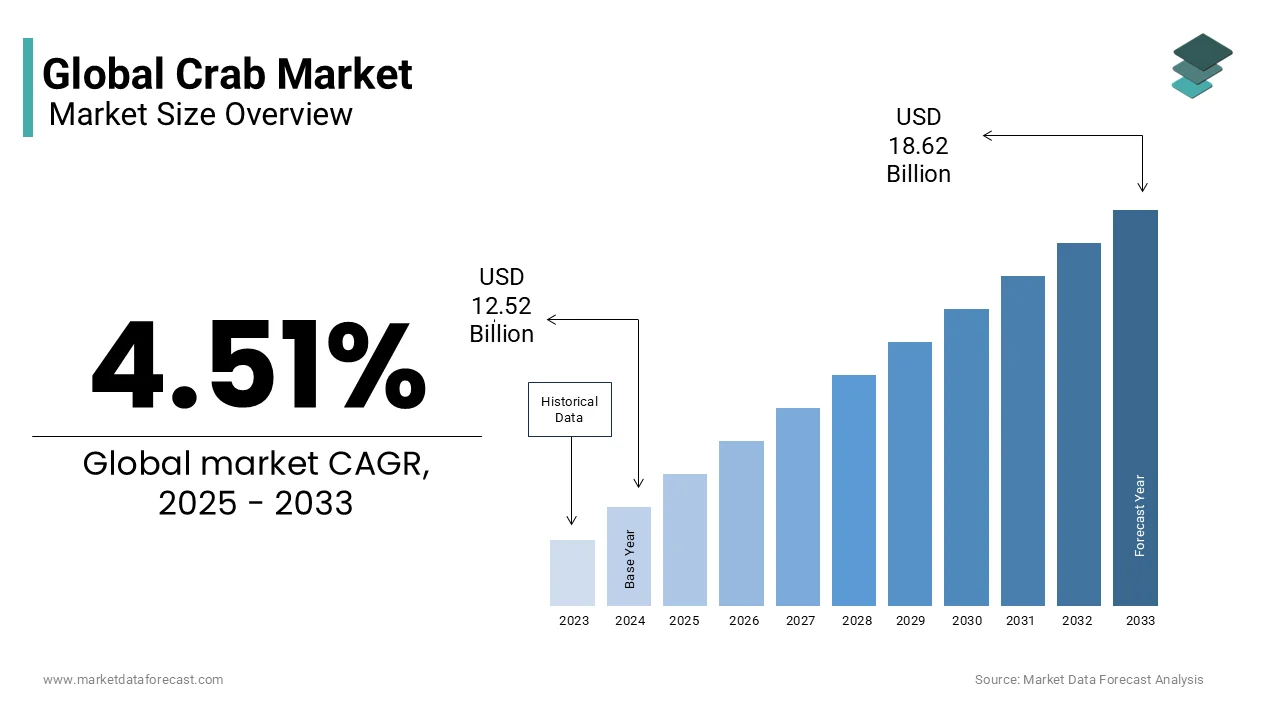

The global crab market size was valued at USD 12.52 billion in 2024 and is projected to reach USD 18.62 billion by 2033 from USD 13.08 billion in 2025, expanding at a CAGR of 4.51% during the forecast period.

Key Market Trends

- Rising global demand for premium seafood and exotic cuisines.

- Expansion of aquaculture and sustainable crab farming practices.

- Growth in frozen and ready-to-eat seafood product lines.

- Increasing consumption of high-protein, low-fat seafood in health-conscious diets.

Segmental Insights

- Based on Type, the red king crab segment dominated the global crab market, capturing 42.6% share in 2024.

Regional Insights

- Asia Pacific led the global crab market with a 36.2% share in 2024.

- North America is expected to grow steadily, driven by strong seafood imports.

- Europe shows increasing demand for sustainable and traceable seafood.

- Latin America and the Middle East & Africa are witnessing rising seafood exports and gradual demand growth.

Competitive Landscape

Major players operating in the global crab market include Supreme Crab & Seafood Inc., Maine Lobster Now, Pacific Sea Food, Handy Sea Food Incorporated, and Phil-Union Frozen Foods Inc. These companies are focusing on sustainable sourcing, premium product offerings, and expanding distribution networks to strengthen their market presence.

Global Crab Market Size

The global Crab market size was valued at USD 12.52 billion in 2024 and is expected to reach USD 18.62 billion by 2033 from USD 13.08 billion in 2025. The market is projected to grow at a CAGR of 4.51%.

Crab are predominantly sourced from wild fisheries and increasingly from controlled farming systems, crabs such as the blue crab (Callinectes sapidus), Dungeness crab (Metacarcinus magister), and mud crab (Scylla serrata) are prized for their delicate flavor and high protein content. Coastal communities in countries like Indonesia, the Philippines, and Vietnam rely heavily on crab fisheries for livelihoods and food security. The species also plays a role in marine ecosystem balance, serving as both scavenger and prey. Rising consumer demand for premium seafood, particularly in urban centers across North America, Europe, and East Asia, has intensified commercial interest, while sustainability concerns are reshaping supply chain practices.

MARKET DRIVERS

Rising Demand for Premium Seafood in Urban and High-Income Markets

The increasing preference for high-value seafood in affluent urban centers has significantly elevated crab consumption, which is driving the growth of crab market. The per capita seafood consumption in the United States reached 20.5 pounds in 2021, with crab ranking among the top five most consumed shellfish. In Japan, crab is a staple during festive seasons, with the annual consumption of imported snow crab in metric tons, as per the research. Similarly, in China, crab sales spike during the Mid-Autumn Festival, with premium hairy crab fetching pCrabs up per pair in high-end markets. The proliferation of fine-dining restaurants and sushi chains has further institutionalized crab as a luxury protein, driving consistent demand despite its premium pricing. This cultural and gastronomic elevation sustains robust market momentum.

Expansion of Aquaculture and Controlled Crab Farming Techniques

Advancements in crab aquaculture have enabled more reliable supply and reduced dependency on wild catch, particularly in Southeast Asia, is driving the growth of crab market. The Philippines and Vietnam collectively produced notable metric tons of farmed mud crabs, representing a year-on-year increase. Innovations in hatchery technology, such as the successful mass production of Scylla larvae, have improved survival rates, according to research. These developments allow for year-round supply, better size grading, and disease control which makes farmed crab increasingly competitive with wild-caught varieties. The scalability of aquaculture is transforming crab from a seasonal delicacy into a commercially viable, consistent commodity.

MARKET RESTRAINTS

Overfishing and Depletion of Wild Crab Stocks

The unsustainable fishing practices and habitat degradation is causing depletion of wild crab stocks, which is restricting the growth of crab market. According to the IUCN, the European edible crab (Cancer pagurus) is classified as Least Concern. Although it is a valuable commercial fishery species and localized stocks can be impacted by fishing pressure. In Southeast Asia, illegal, unreported, and unregulated (IUU) fishing has led to a reduction in mud crab stocks over the past decade, according to the research. The use of destructive gear, such as fine-mesh nets and crab pots that capture juveniles, disrupts breeding cycles and threatens long-term species viability. These ecological constraints limit supply and increase regulatory scrutiny, constraining market growth.

Stringent Import Regulations and Food Safety Standards

Global crab trade is increasingly hindered by rigorous food safety and phytosanitary regulations, particularly in major importing nations, is restricting the growth of crab market. The FDA inspects only a small fraction of imported seafood, estimated to be around 1% to 2% in 2023. This means that a large majority of imported seafood is not tested. China, a key export destination for Vietnamese and Indonesian crab, implemented stricter import controls, rejecting shipments for non-compliance with heavy metal and microbial standards, according to the study. The European Union’s Regulation (EC) No 853/2004 mandates traceability and cold-chain integrity, which many small-scale exporters struggle to meet. These barriers increase compliance costs, delay shipments, and exclude smaller producers from high-value markets which is fragmenting supply chains and limiting export-driven growth in producing countries.

MARKET OPPORTUNITIES

Growth of E-Commerce and Direct-to-Consumer Frozen Crab Sales

The digitalization of seafood retail has opened new distribution channels for premium crab products, particularly in urban markets, is providing opportunity for the carb market growth. According to study, online grocery sales in the U.S. grew, with frozen and vacuum-sealed crab claw and leg meat emerging as high-margin categories. Companies like Seattle Fish Company and Boston Lobster have expanded their e-commerce platforms to offer flash-frozen Dungeness and king crab with next-day delivery. The integration of blockchain for origin tracing and QR-code-based freshness verification has enhanced consumer trust. This shift enables producers to bypass traditional intermediaries, improve margins, and reach geographically dispersed high-income consumers which creates a scalable as well as low-waste commercial model.

Development of Value-Added Crab Products and Byproduct Utilization

Innovation in value-added crab products and efficient byproduct use is providing opportunities for the expansion of crab market. Chitosan, derived from crab shells, is used in water purification, wound healing, and biodegradable packaging. In South Korea, companies like CJ CheilJedang are developing crab-based flavour enhancers and ready-to-eat meals for convenience food markets. Apart from these, crab roe and hepatopancreas are being marketed as gourmet ingredients in sauces and spreads. These value-added applications improve profitability, reduce environmental impact, and diversify income for processors in an otherwise volatile commodity market.

MARKET CHALLENGES

Climate Change and Ocean Acidification Affecting Crab Larval Development

Climate change is disrupting crab life cycles, particularly during the vulnerable larval stage is challenging the growth of the crab market. According to a study, ocean acidification, driven by increased CO₂ absorption, reduces the survival rate of Dungeness crab larvae due to impaired shell formation and metabolic stress. The U.S. National Oceanic and Atmospheric Administration (NOAA) warns that acidified waters in the Pacific Northwest could collapse juvenile recruitment within a decade. In Alaska, warming sea temperatures have shifted snow crab habitats northward, leading to a population decline in the Bering Sea, prompting the state to cancel the commercial season. These ecological shifts destabilize fisheries, increase operational risks, and impede long-term planning which threatenes both livelihoods and supply continuity.

Labor-Intensive Processing and Post-Harvest Losses

The crab processing remains highly labor-dependent, which is challenging the growth of the crab market. Manual cracking, picking, and grading accounting for a portion of operational costs in countries like Indonesia and the Philippines, according to the study. Mechanization is limited due to the irregular shape and fragility of crab meat. In Vietnam, post-harvest losses in the crab supply chain, primarily due to inadequate refrigeration and delayed processing, as per the study. In India, a portion of landed crabs are transported in open baskets without temperature control, leading to spoilage and microbial contamination. These inefficiencies reduce yield, increase costs, and compromise food safety. Pilot projects for automated crab crackers are underway in Japan and Norway. However, widespread adoption remains constrained by high capital costs and technical complexity by leaving the sector vulnerable to labor shortages and quality inconsistencies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.51% |

| Segments Covered | By Type, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Supreme Crab & Seafood Inc., Maine Lobster Now, Pacific Sea Food, Handy Sea Food Incorporated, and Phil-Union Frozen Foods Inc., and others |

SEGMENTAL ANALYSIS

By Type Insights

The red king crab segment dominated the crab market by capturing 42.6% of the global market share in 2024. The growth of the red king crab segment is primarily driven by its premium positioning, large size, and rich, sweet meat favored in high-end culinary applications. Red King Crabs, primarily harvested in the Bering Sea and Russian Far East, can weigh up to 10 kilograms, with leg meat accounting for a portion of the edible yield, according to the study. The species is a staple in luxury seafood menus across the U.S., Japan, and China, where a single crab can retail. Russia, the world’s largest supplier, exported significant metric tons of king crab products, as per the study. Its association with exclusivity and festive dining sustains strong demand despite high pCrabs and regulatory constraints.

The Snow Crab (Chionoecetes opilio) is estimated to register the fastest CAGR of 7.8% from 2025 to 2033. The growth of the snow crab segment can be attributed to its widespread use in sushi, seafood salads, and processed food products, particularly in North America and Asia. Snow Crab accounts for a portion of Canada’s crab exports, with the country harvesting notable metric tons. Its long, slender legs yield delicate, flaky meat ideal for pre-cooked, frozen, and ready-to-eat formats. The consumer preference for mild-flavored, easy-to-eat seafood has elevated Snow Crab’s appeal in convenience-driven markets with the rapid commercial expansion.

REGIONAL ANALYSIS

Asia Pacific Crab Market Insights

The Asia Pacific was the top performer in the global crab market with 36.2% of the share in 2024. The domination of Asia Pacific in the global market is primarily driven by strong cultural preferences for crab as a celebratory and luxury food item, particularly in China, Japan, and South Korea. In China, annual crab consumption in metric tons, with the Mid-Autumn Festival alone driving demand for major metric tons of hairy crab, according to study. Japan imports tons of frozen snow and king crab annually, primarily from Russia and Canada. Aquaculture in Vietnam and the Philippines has scaled up mud crab farming, producing tons. The region’s dense coastal populations, rising disposable incomes, and gourmet food culture make it the epicenter of global crab demand and culinary innovation.

North America Crab Market Insights

North America crab market was positioned second with the United States serving as the primary consumer and regulatory benchmark. American consumers exhibit a strong preference for premium crab varieties, particularly Alaskan King and Dungeness crab. The U.S. imports its crab supply, due to domestic supply limitations. The closure of the Bering Sea snow crab fishery, driven by climate-induced stock collapse, has heightened reliance on international sources. However, the U.S. remains a top performer in sustainable fisheries management, with the Alaska Department of Fish and Game enforcing strict quotas and seasonal closures. The proliferation of seafood delivery platforms and frozen gourmet crab products has sustained demand despite supply volatility.

Europe Crab Market Insights

Europe crab market is attributed to hit the highest CAGR during the forecast period with strong demand concentrated in the UK, France, Spain, and Scandinavia. The brown crab (Cancer pagurus) is the most commercially significant species. European consumers increasingly favor traceable, MSC-certified crab products, pushing retailers toward sustainability. Processed crab meat is widely used in salads, sandwiches, and ready meals, particularly in the UK, where chilled crab sticks are a supermarket staple. Regulatory rigor and consumer awareness define the region’s high-value as well as compliance-driven market.

Latin America Crab Market Insights

Latin America crab market growth is likely to grow with the blue crab (Callinectes sapidus), which is both consumed domestically and exported to the U.S. and Europe. Ecuador, Colombia, and Brazil are emerging as key producers and regional hubs Ecuador exported tons of processed blue crab meat, as per the study. However, infrastructure gaps, limited cold-chain logistics, and fluctuating exchange rates constrain scalability. Furthermore, rising regional tourism and hotel demand for fresh seafood are stimulating local consumption, while export-oriented processing plants are adopting EU and FDA standards to access premium markets.

Middle East & Africa Crab Market Insights

Middle East & Africa is likely to grow in the global crab market, with the Gulf Cooperation Council (GCC) nations driving premium demand and North African countries contributing to artisanal fisheries. In Egypt, artisanal fishers harvest blue and swimming crabs from the Nile Delta and Mediterranean, supplying local markets. However, limited consumer familiarity with crab outside coastal communities and underdeveloped processing facilities restrict broader market penetration. Thus, the region offers untapped potential for premium seafood expansion due to rising affluence and international cuisine adoption.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Supreme Crab & Seafood Inc., Maine Lobster Now, Pacific Sea Food, Handy Sea Food Incorporated, and Phil-Union Frozen Foods Inc. are the key players in the global crab market.

Competition in the crab market is intensifying due to supply volatility, rising consumer expectations, and regulatory complexity. Large multinational processors compete with regional exporters and artisanal suppliers, each leveraging distinct advantages in cost, quality, or authenticity. The scarcity of wild stocks has shifted competitive dynamics toward aquaculture innovation and supply chain control. Differentiation is achieved through sustainability certifications, product form (whole, leg, or minced), and culinary readiness. In Asia, local brands dominate fresh crab sales, while global players lead in frozen and processed segments. PCrab sensitivity remains moderate due to the premium nature of crab, but food safety compliance and traceability have become important barriers to entry. The convergence of climate risks, trade regulations, and gourmet demand is reshaping the competitive landscape which favours agile, vertically integrated, and technologically advanced operators.

TOP PLAYERS IN THE MARKET

Thai Union Group

Thai Union Group, a global leader in seafood, plays a pivotal role in the Asia Pacific crab market through its integrated supply chain and premium branded products. The company sources crab from sustainable fisheries in Indonesia, Vietnam, and the Philippines, focusing on value-added processed crab meat for export and domestic retail. It has also invested in cold-chain logistics and blockchain traceability to ensure product integrity from vessel to shelf. The company collaborates with local fishers to promote responsible harvesting and supports hatchery development for mud crab aquaculture. Its innovation in packaging, including vacuum-sealed and retort formats that enhances shelf life and export viability, strengthening its presence across Asia and beyond.

Maruha Nichiro Corporation

Maruha Nichiro Corporation is a dominant force in Japan’s crab import and processing sector, sourcing primarily from Russia, Canada, and Alaska to meet domestic demand for premium frozen and ready-to-eat crab products. The company operates advanced processing facilities in Hokkaido and Shizuoka, specializing in whole-cooked, leg-meat, and minced crab for sushi, bento, and restaurant use. The company actively engages in sustainability certifications, including MSC-labeled products, to align with Japanese retailers’ ethical sourcing policies. Its R&D focus on flavour enhancement and texture preservation which strengthens its reputation for quality in one of the world’s most discerning seafood markets.

Vietnam Seafoods Corporation

As a leading entity within Vietnam’s seafood export ecosystem, the Vietnam Seafoods Corporation contributes significantly to the Asia Pacific crab market through farmed and wild-caught blue swimming and mud crab production. The corporation exports processed crab meat to the U.S., EU, and Japan, adhering to stringent food safety standards. It has also launched organic crab farming pilots using probiotics instead of antibiotics, responding to import regulations.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the crab market are deploying a combination of vertical integration, technological innovation, and sustainability certification to secure competitive advantage. Companies are investing in traceability systems using blockchain and QR codes to meet consumer demand for transparency and compliance with import regulations. Expansion into value-added products, such as pre-cooked, seasoned, and ready-to-eat crab formats, is enabling premium pricing and reduced reliance on volatile whole-crab sales. Strategic sourcing from diverse geographies mitigates risks from regional fishery collapses or climate disruptions. Aquaculture development, particularly in Southeast Asia, allows for controlled supply and year-round availability. Partnerships with local fishers promote sustainable harvesting practices, while automation in processing improves yield and reduces labor dependency. E-commerce integration and direct-to-consumer models are being scaled to capture urban premium demand, especially in Asia and North America.

MARKET SEGMENTATION

This research report on the global Crab market has been segmented and sub-segmented based on type, and region.

By Type

- Red King Crab

- Blue King Crab

- Opilio

- Tanner

- Other Types (Dungeness Crab, Gazami, etc.)

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the crab market?

The crab market refers to the global industry involved in harvesting, farming, processing, distributing, and selling various crab species for consumption and related products.

2. What are the main types of crabs traded in the market?

Popular types include blue crab, snow crab, king crab, Dungeness crab, mud crab, and soft-shell crab.

3. Which regions dominate the global crab market?

North America, Asia-Pacific (especially China, Japan, and Vietnam), and Europe are the leading markets for crab production and consumption.

4. What factors are driving the growth of the crab market?

Rising demand for premium seafood, increasing health awareness about protein-rich diets, and growth in foodservice outlets fuel market expansion.

5. What challenges does the crab market face?

Challenges include overfishing, illegal harvesting, seasonal availability, environmental changes, and fluctuations in export regulations.

6. What are the key segments in the crab market?

Segments include live crabs, frozen crabs, processed crab meat, ready-to-eat crab dishes, and crab-based sauces or spreads.

7. What are the current trends shaping the crab industry?

Trends include growing popularity of value-added crab products, online seafood retailing, premium crab dishes in fine dining, and innovations in crab farming.

8. Who are the leading players in the crab market?

Key companies include Phillips Foods, Clearwater Seafoods, Alaskan Leader Seafood, Bumble Bee Seafoods, and Thai Union Group.

9. What is the outlook for crab prices in the coming years?

Prices may remain volatile due to seasonal harvests, climate impacts, and global demand, but steady growth is expected as sustainable supply improves.

10. What is the future growth potential of the crab market?

The crab market is projected to grow steadily, supported by rising seafood consumption, sustainable aquaculture development, and expanding global trade networks.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com