Global Cycling Sunglasses Market Size, Share, Trends, & Growth Forecast Report By Lens (Polarized, Non-Polarized, Photochromic, Clear, Mirrored, Gradient, and Others), Frame Material (Polycarbonate, Grilamid, Nylon, Metal and Others), Price Range (Budget, Mid-Range, and Premium), Sales Channel (Offline Retail, Online Retail, Company-Owned Websites, and Others), Gender (Male, Female, and Unisex) and Region (North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America) – Industry Analysis from 2026 to 2034

Global Cycling Sunglasses Market Size

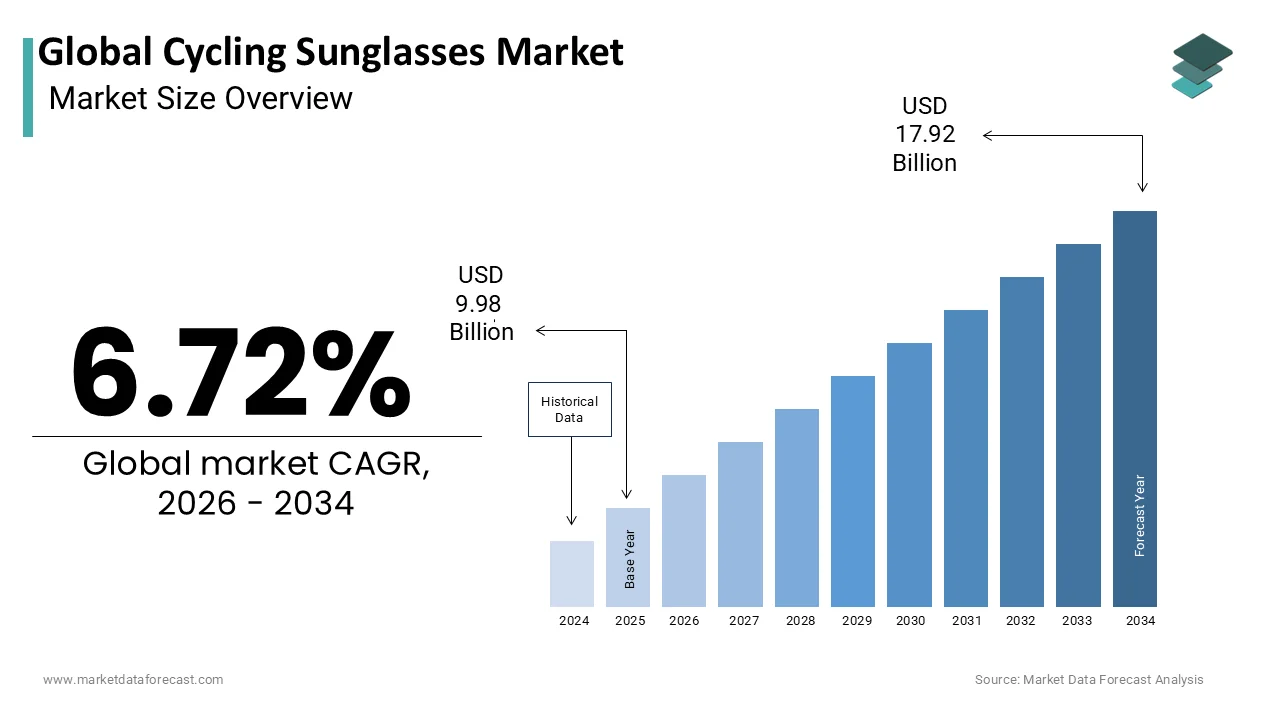

The global cycling sunglasses market size was valued at USD 9.98 billion in 2025 and is expected to reach USD 17.92 billion by 2034 from USD 10.65 billion in 2026. The market is projected to grow at a CAGR of 6.72%. from 2026 to 2034

Cycling sunglasses are specialized eyewear designed for cyclists to enhance their vision and protect their eyes from the sun, wind, dust, and other environmental factors. These sunglasses typically have features such as polarized lenses to reduce glare, lightweight and durable frames for comfort and safety, and adjustable nose and earpieces for a secure fit. These products come in various styles and lens colors to suit different lighting conditions and personal preferences. Cycling sunglasses not only provide functional benefits but also add to the cyclist's style and fashion sense. These products are an essential piece of gear for any cyclist, from recreational riders to professional athletes.

MARKET DRIVERS

The growing popularity of cycling as a sport and a recreational activity has resulted in an increasing demand for high-quality cycling eyewear propelling the demand for cycling sunglasses and driving the global market growth. The number of people participating in cycling has gradually grown over the last few years resulting in the increased demand for the products that are being used in the cycling sport. Cycling sunglasses are an essential piece of requirement for sportspeople to cycle. An increase in the number of people cycling worldwide is directly fueling the demand for these products and promoting market growth.

The integration of technological advancements to innovate and manufacture cycling sunglasses with advanced features is further supporting the global market growth. Technological advancements have led to the development of innovative features in cycling sunglasses, such as polarized lenses, anti-fog coatings, and photochromic lenses that can adjust to changing light conditions. The rapid adoption of advanced technologies is prompting the growth rate of the market.

The rising awareness about the harmful effects of UV rays on the eyes has led to a surge in demand for sunglasses that offer complete UV protection, which is leveling up the growth rate of the global cycling sunglasses market. The fashion aspect associated with cycling sunglasses is promoting the demand for these products, as consumers are increasingly seeking stylish and trendy eyewear to complement their cycling attire. The growing interest in cycling as a recreational and fitness activity is another key factor boosting the growth rate of the cycling sunglasses market. The rising trend of sports sponsorship and endorsement is supporting the global market growth, with cycling sunglasses being an essential accessory for cyclists. The emergence of new technologies and materials is expected to create new market opportunities for innovative and eco-friendly cycling sunglasses. The rising awareness of the harmful effects of UV rays on eye health presents a growth opportunity for cycling sunglasses with specialized UV protection features.

MARKET RESTRAINTS

The high costs associated with these products are one of the significant restraints to global market growth. The high cost of high-quality cycling sunglasses makes them unaffordable to low-budget consumers. The use of cycling sunglasses is limited to cycling activities, making them less versatile and reducing the market potential. The market is highly competitive, with established brands dominating the industry and making it difficult for new entrants to establish themselves. Technological advancements also pose a challenge, as failure to keep up with new materials and designs can make a brand obsolete in the market. Cycling sunglasses are weather-dependent and are only useful in sunny weather conditions, limiting their market potential in regions with different weather patterns. Overall, these restraints pose significant challenges to the cycling sunglasses market, requiring continuous innovation and adaptation to remain competitive.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Lens Type, Frame Material, Price Range, Sales Channel, Gender and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Oakley, Rudy Project, Tifosi Optics, Smith Optics, Bolle, Adidas Eyewear, Nike Vision, POC Sports, Julbo, Shimano Eyewear, BBB Cycling, Ryders Eyewear, Dragon Alliance, Uvex Sports and Sunwise |

SEGMENTAL ANALYSIS

By Lens Type

The polarized segment had the largest share of the global market in 2025 and is projected to grow at a healthy CAGR during the forecast period. Polarized lenses are estimated to have the highest demand in the cycling sunglasses market as they help to reduce glare and improve visibility in bright sunlight or reflective surfaces, making it easier for cyclists to navigate their way on the road or trails. Photochromic lenses are also popular as they can automatically adjust to different lighting conditions, making them versatile for cycling in different environments.

The non-polarized segment captured a notable share of the global market in 2024 and is anticipated to showcase a healthy CAGR in the coming years. The cost-effectiveness and increased adoption of non-polarized cycling sunglasses in casual cycling and urban commuting are driving the growth of the non-polarized segment in the worldwide market.

By Frame Material

The polycarbonate and nylon frame segments are estimated to account for the largest share of the global cycling sunglasses market during the forecast period due to their lightweight, durable, and flexible properties. These materials are also often more affordable than metal or grilamid frames, making them a popular choice for budget-conscious consumers. Overall, it will increase the market revenue in the coming years.

By Price Range

The budget and mid-range price segments are estimated to have a higher demand compared to the premium segment during the forecast period. Most consumers are price-sensitive and prefer affordable options that offer good value for money, which is majorly driving the growth of budget and mid-range priced cycling sunglasses in the global market.

By Sales Channel

The online retail segment is growing rapidly and is expected to register the highest CAGR among all the segments in the worldwide market. The sales of cycling sunglasses via e-commerce platforms globally have witnessed a significant spike in 2024. This shift towards online shopping has been driven by factors such as convenience, wider product selection, and competitive pricing.

By Gender

The male gender dominated the cycling sunglasses market in 2024 and is estimated to hold the major share of the worldwide cycling sunglasses market during the forecast period. The cycling sunglasses market has been male-dominated, and as such, male-oriented cycling sunglasses may have higher demand than female-oriented options.

REGIONAL ANALYSIS

North America had the largest share of the global market in 2025and is expected to occupy the highest share of the global cycling sunglasses market during the forecast period. Due to the growing popularity of cycling as a recreational activity and the increasing demand for high-quality sports eyewear in the region. The U.S. held the highest share of the North American market in 2024 and the presence of the U.S. domination can be seen in the forecast period as well due to the increasing participation in cycling activities.

Europe occupied the second-largest share of the global market in 2025and is predicted to grow at a noteworthy CAGR during the forecast period. The demand for cycling sunglasses in Europe is growing gradually, particularly in popular cycling destinations such as France, Italy, and Spain. The growing popularity of cycling as a form of exercise and leisure activity is the primary driver for the demand for the cycling sunglasses market in the European region.

The Asia-Pacific regional market is projected to grow at a promising CAGR during the forecast period. Owing to the rising awareness of eye protection during cycling activities and the increasing popularity of cycling as a fitness activity in Southeast Asian countries. China and India together accounted for the major share of the cycling sunglasses market in the Asia-Pacific region in 2024.

KEY MARKET PLAYERS

Companies playing a promising role in the global cycling sunglasses market include Oakley, Rudy Project, Tifosi Optics, Smith Optics, Bolle, Adidas Eyewear, Nike Vision, POC Sports, Julbo, Shimano Eyewear, BBB Cycling, Ryders Eyewear, Dragon Alliance, Uvex Sports and Sunwise.

RECENT HAPPENINGS IN THE MARKET

- In December 2024, SunGod, a renowned performance eyewear brand from Britain, teamed up with the crit cycling team Tekkerz based in London to introduce a limited-edition version of their popular Vulcans sunglasses known as TEKKERZ Vulcanz.

- In September 2021, in partnership with EssilorLuxottica, the eyeglasses company, Facebook finally made its anticipated foray into the smart glasses market by unveiling the Ray-Ban Stories smart spectacles.

MARKET SEGMENTATION

This research report on the global cycling sunglasses market has been segmented and sub-segmented based on lens type, frame material, price range, gender, sales channel, and region.

By Lens Type

- Polarized

- Non-Polarized

- Photochromic

- Clear

- Mirrored

- Gradient

- Others

By Frame Material

- Polycarbonate

- Grilamid

- Nylon

- Metal

- Others

By Price Range

- Budget

- Mid-Range

- Premium

By Sales Channel

- Offline Retail

- Online Retail

- Company-Owned Websites

- Others

By Gender

- Male

- Female

- Unisex

By Region

- North America

- Europe

- Asia-Pacific

- Middle East & Africa

- Latin America

Frequently Asked Questions

What is the cycling sunglasses market?

Cycling sunglasses are specialized eyewear designed for cyclists to enhance their vision and protect their eyes from the sun, wind, dust, and other environmental factors. The cycling sunglasses market is the market for these eyewear products.

What is the market size of cycling sunglasses?

The market size of cycling sunglasses was valued at around USD 8.2 billion in 2022 and is expected to grow at a CAGR of 6.72% from 2023 to 2028, reaching USD 13.2 billion by the end of the forecast period.

What are the opportunities in the cycling sunglasses market?

The growing interest in cycling, the increasing trend of sports sponsorship and endorsement, the emergence of new technologies and materials, and the rising awareness of the harmful effects of UV rays present growth opportunities for the cycling sunglasses market.

What are the restraints of the cycling sunglasses market?

The high cost of high-quality cycling sunglasses, limited use, market competition, technological advancements, and weather-dependent use are the restraints of the cycling sunglasses market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com