Global Data Center Transformers Market Size, Share, Trends, & Growth Forecast Report By Insulation (Dry and Liquid), Components (Solutions and Services), End-Users (Enterprises, Cloud Providers, Colocation Providers, Hyperscale Data Centres), Data Centre Sizes (Small and Medium, and Large), Verticals (BFSI, IT and Telecommunication, Media and Entertainment, Retail, Manufacturing, Healthcare, Government and Defense and Others) and Regional - (2025 to 2033)

Global Data Center Transformers Market Size

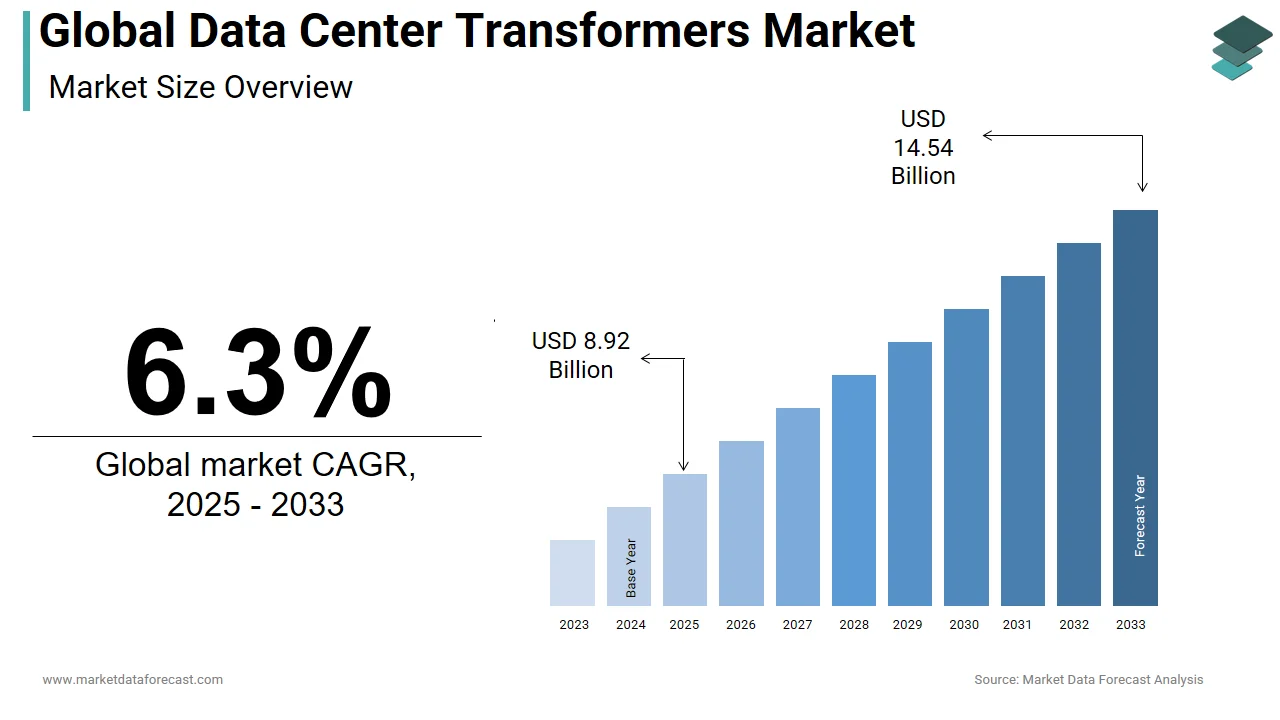

The global data center transformer market was worth USD 8.39 billion in 2024. The global market size is expected to grow from USD 8.92 billion in 2025 to USD 14.54 billion by 2033, growing at a CAGR of 6.3% from 2025 to 2033.

A transformer is a device that transforms and distributes electricity from one circuit to a different. The function of a transformer is to intensify or decrease the voltage levels before distributing it to subsequent circuits. Transformers utilized in data center facilities are typically three-phase medium voltage step-down transformers. The rising number of knowledge centers across various industries, like IT and telecom, BFSI, etc., is foreseen to accelerate the data center transformers market over the outlook period.

Data centers are employed by different enterprises where the networking and computing equipment are stored that collect, store, and process the information required. These data centers consume an outsized amount of energy with the increasing operations and always-ON feature. Data center transformers (DCT) are utilized in data centers to extend the operating efficiency and reduce the electrical losses and protect the information.

MARKET DRIVERS

Key factors that are driving the market growth include the rising number of knowledge centers and the imminent got to ensure effective power distribution within the info centers. The data centers registered significant growth in technologies and services in recent years. There has been a rise in IT spending of organizations to simplify operations and data storage capabilities. Rapidly growing data traffic is driving data storage demand, which has resulted in the continuous expansion of the worldwide data center transformers market. Data center structures are related to more power consumption and are increasing in proportion and size day by day. Also, the growing workload on the info centers has, in turn, increased the demand for better quality power supply. These factors further justify the presence of transformers in a data center and are contributing to the expansion of this market.

The data center industry measures a facility’s efficient use of electricity in terms of power usage effectiveness (PUE). The PUE value is impacted negatively if there are a high number of electrical losses within the distribution of power. Therefore, data center manufacturers across the U.S. are focused on providing energy-efficient equipment by constantly making improvements within the transformer designs to fulfill the wants of the U.S. Department of Energy (DOE) set within the year 2016. Changes in design concerning impedance, in-rush current, and short-circuit current are expected to enhance the efficiency of the transformers by reducing electrical losses. These design improvements are expected to propel the adoption of knowledge center transformers in the near future.

MARKET RESTRAINTS

Enterprises face a serious restraint within the data center power market thanks to the need for high initial investment. The implementation of recent power systems in data centers requires a shift from traditional to the newest and updated data center components. This transition process requires high initial investment. Most enterprises, including SMEs with less capital, often cannot update their data centers thanks to this requirement.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.3% |

| Segments Covered | By Insulation, Components, End User Types, Data Center Sizes, Verticals, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Eaton, ABB Ltd, General Electric, Hyosung Heavy Industries, LeGrand, Schneider Electric, Siemens AG, Tripp Lite, Vatransformer, Vertiv Co and Others. |

REGIONAL ANALYSIS

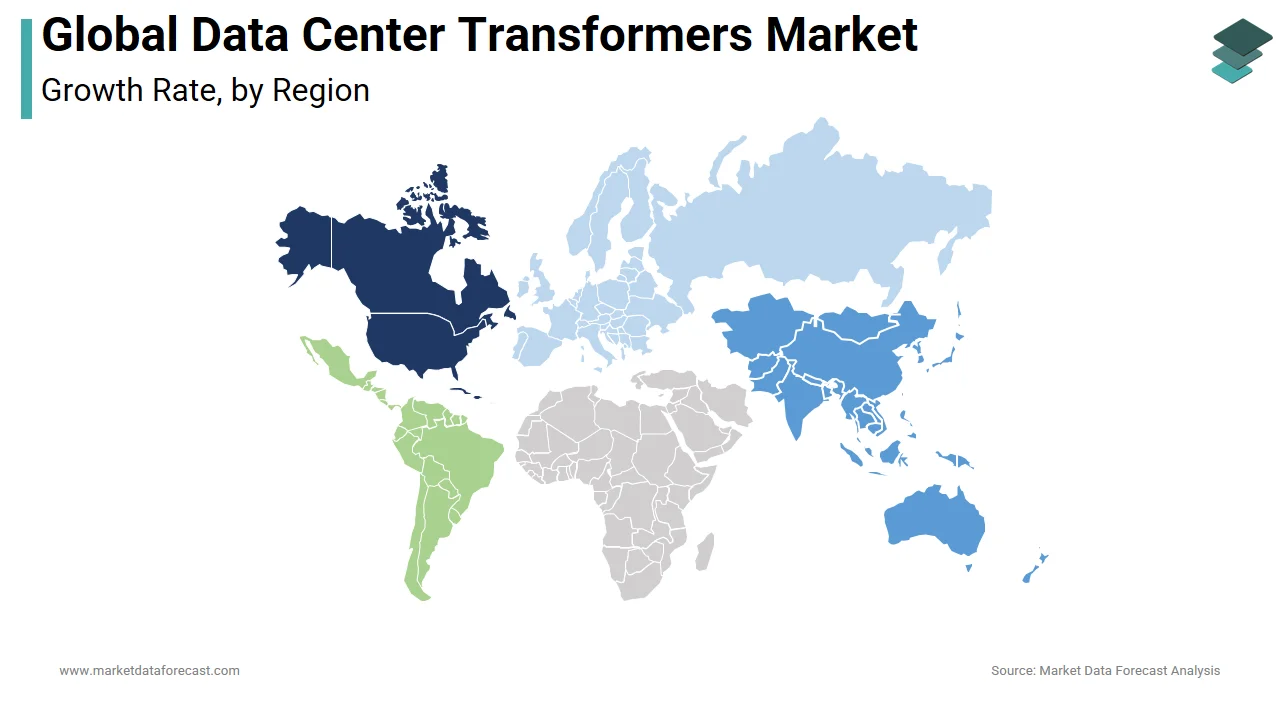

North America emerged as the largest shareholder in 2024 with more than 35% of the worldwide revenue. This is often attributed to the presence of major players like Eaton and General Electric. Advanced technological development and technical awareness amongst the users within the region also are expected to possess a positive impact on market growth. Moreover, the presence of several data centers within the region may be a crucial factor expected to drive the regional market.

Asia Pacific is that the fastest-growing regional marketplace for data center transformers with a CAGR of 8.9% over the forecast period. Increasing demand for data storage and cloud-based applications is contributing to the expansion of the regional market. Implementation of cloud-based services in sectors, like education and healthcare, including support from the governments, has increased the development of knowledge centers during this region. Furthermore, the high penetration of smartphones and internet availability, alongside increased demand for mobility, is projected to extend the number of knowledge centers in this area, which is predicted to directly contribute to the expansion of the market.

KEY MARKET PLAYERS

Eaton, ABB Ltd, General Electric, Hyosung Heavy Industries, LeGrand, Schneider Electric, Siemens AG, Tripp Lite, Vatransformer and Vertiv Co. are some of the major players in the global data center transformers market.

RECENT MARKET HAPPENINGS

-

In March 2020, Schneider Electric launched its first Smart-UPS Lithium-ion that is specially created for local edge environments and micro data centers. The second category is APC Easy UPS 1 Ph Online, which may be a versatile, high-quality, and cost-effective UPS developed to handle high voltage and inconsistent power conditions.

-

In February 2020, ABB Group released a replacement switchgear named NeoGear. ABB brought the laminated bus plate technology for low-voltage switch gears. With the digital capabilities and combined connectivity of the ABB Ability™ platform, NeoGear offers the utmost safety, the very best reliability, more flexibility, better efficiency, and measurable Return On Investment (ROI).

-

In May 2020, Huawei launched the SmartLi UPS solution and therefore the latest UPS module in Singapore. SmartLi UPS reinvents the facility supply system for next-generation data centers. Its built-in smart voltage balance technology supports the hybrid use of old and new battery strings also as ensures systems run properly albeit one battery module is faulty.

MARKET SEGMENTATION

This research report on the data center transformers market has been segmented and sub-segmented based on insulation, components, data center size, vertical end-user and region.

By Insulation

- Dry

- Liquid

By Components

- Solution

- Services

By End-User

- Enterprises

- Colocation Providers

- Cloud Providers

- Hyperscale Data Centers

By Data Center Size

- Small and Medium Data Center

- Large Data Center

By Vertical

- BFSI

- IT and Telecommunication

- Media and Entertainment

- Healthcare

- Government and Defense

- Retail

- Manufacturing

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is driving the growth of the global Data Centre Transformers market?

The primary drivers of the global Data Centre Transformers market include the exponential growth of data generated by industries, the rapid expansion of cloud services, and the rise of Internet of Things (IoT) devices. Additionally, increasing demand for green energy solutions and more efficient power systems in data centers have prompted innovations in transformer technology.

What are the key transformer technologies used in modern data centers?

The two main transformer types used in data centers are liquid-immersed transformers and dry-type transformers. Liquid-immersed transformers, known for their superior cooling properties and durability, are typically used in high-capacity data centers. Dry-type transformers, which are safer and require less maintenance, are often used in smaller data centers or in environments where fire safety is a priority.

How are innovations in cooling technologies affecting the Data Centre Transformers market?

Cooling technology innovations, such as liquid cooling and hybrid cooling systems, are significantly impacting the Data Centre Transformers market. These advancements enhance transformer efficiency by maintaining optimal operating temperatures, improving system reliability, and extending equipment lifespan. Such technologies are particularly relevant as data centers become more power-dense and need to handle higher workloads.

What impact is the shift toward cloud computing having on the Data Centre Transformers market?

The global shift toward cloud computing is a major factor boosting the demand for data center transformers. As businesses migrate to the cloud, the need for robust data center infrastructure grows, necessitating transformers that can support large-scale operations. This has also led to the rise of edge data centers, where transformers are required to provide localized, energy-efficient power solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com