- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

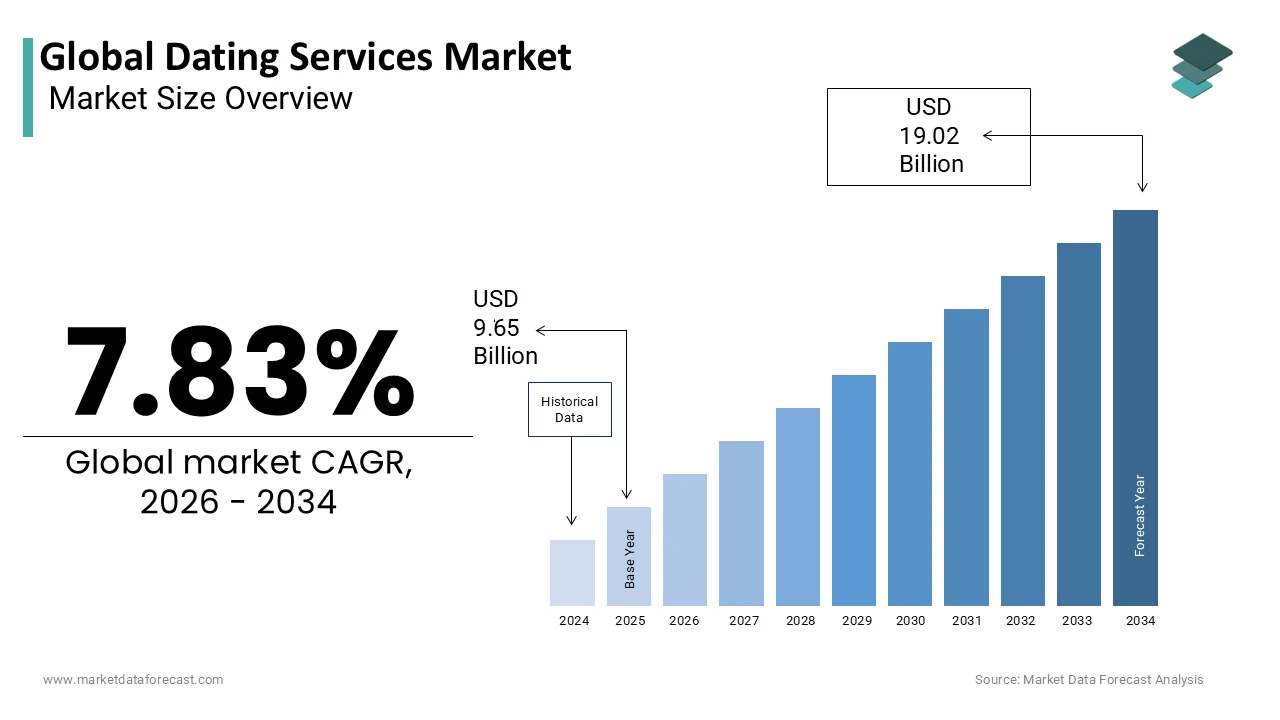

Market Size, 2025

$9.65 BnMarket Estimate, 2026

$10.41 BnMarket Forecast, 2034

$19.02 BnCAGR, 2026–2034

7.83%Global Dating Services Market Size

The global dating services market size was valued at USD 9.65 billion in 2025, and the global market size is expected to be worth USD 19.02 billion by 2034 from USD 10.41 billion in 2026, growing at a CAGR of 7.83% from 2026 to 2034.

The dating services market refers to a digital and physical ecosystem that facilitates romantic, social, or long-term relationship connections between individuals through various platforms. These include online dating websites, mobile applications, matchmaking agencies, speed dating events, and niche-based services tailored for specific demographics such as age groups, religious affiliations, sexual orientations, and professional backgrounds. The industry has evolved significantly from traditional matchmakers and classified ads to data-driven, AI-powered platforms that offer personalized matchmaking experiences.

This shift is largely attributed to changing social dynamics, increasing urbanization, and the desire for convenience in finding compatible partners.

In addition, the integration of artificial intelligence, behavioral analytics, and location-based technologies has transformed how users interact and form connections. With rising smartphone adoption and shifting cultural norms, the dating services market continues to expand, driven by both technological innovation and evolving consumer expectations regarding relationships and social interaction.

MARKET DRIVERS

Increasing Smartphone Penetration and Internet Accessibility

One of the primary drivers of the dating services market is the widespread proliferation of smartphones and increased internet accessibility across both developed and emerging economies. This expansion enables seamless access to dating apps and platforms, making them more convenient and accessible than ever before.

Moreover, the affordability of smartphones has played a crucial role in expanding the user base. Similarly, in Latin America and Southeast Asia, where internet infrastructure has improved dramatically over the past decade, dating service providers like Tinder, Bumble, and local players have seen exponential growth.

This technological democratization has not only broadened access but also diversified the demographic profile of users, extending beyond young urban professionals to include older adults and rural populations.

Changing Social Norms and Greater Acceptance of Online Dating

Another significant driver of the dating services market is the evolving perception and social acceptance of online dating as a legitimate and preferred method of forming relationships. As per the Pew Research Center, in 2023, nearly half of all U.S. adults believed that online dating was a good way to meet people, a marked increase from just 29% in 2013. Similar shifts have been observed in Europe and parts of Asia, where societal stigma around digital matchmaking is rapidly diminishing.

This change is particularly evident among younger generations, including millennials and Gen Z, who are more open to forming emotional and romantic connections online. Besides, the impact of the pandemic accelerated this trend, as lockdowns and social distancing measures forced many to rely on virtual interactions for companionship.

Media representation, celebrity endorsements, and successful real-life stories have further normalized online dating. Platforms like Match.com, Hinge, and OkCupid have capitalized on this shift by promoting inclusivity, safety, and authenticity, reinforcing trust and encouraging broader adoption.

MARKET RESTRAINTS

Privacy Concerns and Data Security Issues

A major restraint affecting the dating services market is the growing concern over privacy and data security breaches. As these platforms collect extensive personal information—including location, preferences, photos, and even financial details—users are becoming increasingly wary of potential misuse or unauthorized access. According to the Identity Theft Resource Center, data breaches in the technology and social media sectors increased in 2023 compared to the previous year, with dating apps being among the most vulnerable targets.

High-profile incidents involving well-known dating platforms have amplified public skepticism. For example, in 2022, a leading dating app faced scrutiny after reports surfaced about third-party tracking tools accessing sensitive user data without consent, as highlighted by the Electronic Frontier Foundation. Such incidents erode consumer trust and may deter new users from signing up or cause existing ones to delete their accounts.

Besides, regulatory scrutiny has intensified, particularly in Europe, where the General Data Protection Regulation (GDPR) mandates strict compliance regarding data handling. Non-compliance can result in hefty fines and reputational damage, forcing companies to invest heavily in cybersecurity measures.

Prevalence of Fraudulent Activities and Catfishing Incidents

Another key constraint in the dating services market is the prevalence of fraudulent activities, including catfishing, romance scams, and fake profiles. These deceptive practices not only compromise user safety but also damage the credibility of dating platforms.

According to the Federal Trade Commission, losses from romance scams in the U.S. exceeded USD 1.3 billion in 2023, with a significant portion originating from online dating platforms.

Such incidents often involve scammers creating fake identities to build emotional connections before soliciting money or personal information. Despite efforts by platforms to implement verification systems and AI-based detection tools, fraudulent actors continue to exploit vulnerabilities, particularly on free or less-regulated services.

These issues discourage potential users, especially those unfamiliar with digital interactions, from engaging with dating services. They also lead to increased pressure on platform operators to enhance security features, which can raise operational costs and slow down user acquisition.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Machine Learning for Enhanced Matching

An emerging opportunity within the dating services market is the integration of artificial intelligence (AI) and machine learning (ML) to improve user experience and enhance compatibility matching. Traditional dating platforms relied primarily on basic filters such as age, location, and interests; however, advancements in AI now allow for deeper behavioral analysis and predictive modeling.

Dating platforms are leveraging AI to analyze user interactions, communication patterns, and response behaviors to generate more accurate match suggestions. For instance, some apps use natural language processing to assess conversation flow and sentiment, identifying potential chemistry between users.

Moreover, AI-powered chatbots and voice assistants are being deployed to guide users through the dating process, offering real-time advice and improving overall satisfaction. Companies like Tinder and Hinge have already begun incorporating these technologies to refine their algorithms and offer a more intuitive experience.

Expansion into Niche and Specialized Dating Segments

Another significant opportunity in the dating services market lies in the expansion into niche and specialized segments catering to unique demographics, cultural preferences, and lifestyle choices. As mainstream platforms become increasingly saturated, users are seeking alternatives that align more closely with their specific values, beliefs, and life goals. According to McKinsey & Company, niche markets are experiencing higher growth rates due to their ability to offer differentiated and highly relevant experiences.

Specialized dating services targeting communities such as LGBTQ+, religious groups, professionals, single parents, pet lovers, and fitness enthusiasts are gaining traction.

Furthermore, regional customization is playing a critical role in market expansion. In Asia, for instance, platforms like Tantan in China and TrulyMadly in India have integrated culturally relevant features to appeal to local users. Similarly, in the Middle East, dating services are adapting to conservative norms by emphasizing family-approved introductions and modest interaction formats.

MARKET CHALLENGES

Intense Competition and Market Saturation

One of the foremost challenges facing the dating services market is the intense competition and increasing saturation of platforms vying for user attention and subscription revenues. With hundreds of dating apps and websites operating globally, differentiation has become increasingly difficult, prompting companies to invest heavily in marketing, branding, and feature enhancements to stand out.

Major players such as Tinder, Bumble, and Match Group dominate the premium segment, while numerous free or freemium models attempt to capture market share through alternative monetization strategies. This fragmentation leads to user fatigue, with many consumers downloading multiple apps in search of better matches, only to abandon them shortly afterward due to poor experiences or lack of results.

Besides, the consolidation of larger firms through acquisitions further intensifies the battle for dominance. Unless new entrants can offer truly innovative value propositions or target highly specific niches, breaking into the market remains a formidable challenge despite the sector’s overall growth potential.

Declining User Engagement and High Churn Rates

Another pressing challenge in the dating services market is declining user engagement and high churn rates, which pose a threat to sustainable revenue growth. Despite high initial sign-up numbers, many users discontinue using dating apps after a short period due to unmet expectations, negative experiences, or perceived inefficacy.

Several factors contribute to this trend, including algorithm fatigue, repetitive user interfaces, and the inability to convert casual swiping into meaningful relationships. Moreover, frequent exposure to fake profiles, ghosting, and superficial interactions has diminished trust and interest in long-term engagement.

To combat this, companies are investing in gamification elements, video-based profiles, and community-building features aimed at fostering deeper connections. However, implementing these changes without compromising usability or overwhelming users remains a delicate balancing act.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Services, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Grindr LLC, Love Group Global Ltd., Badoo, Harmony, Inc., Spark Networks SE, Zoosk Inc., The Meet Group Inc., Spice of Life, Match Group, Inc., and Rsvp.com.au Pty Ltd., and others. |

SEGMENTAL ANALYSIS

By Type Insights

The online dating services segment dominated the global dating services market, accounting for 82.4% of total market revenue in 2025. This overwhelming share is attributed to the rapid digital transformation of social interactions and the increasing reliance on smartphones and internet-based platforms for relationship-building.

One major driver behind this dominance is the widespread adoption of mobile applications and web-based platforms, which offer convenience, accessibility, and personalized matchmaking capabilities. The ability to connect instantly across geographical boundaries has made online dating a preferred choice, particularly among millennials and Gen Z.

Another key factor is the integration of advanced technologies like AI, machine learning, and behavioural analytics, which enhance user experience by offering smarter match suggestions. With continuous innovation and expanding digital infrastructure, the online segment remains the cornerstone of the modern dating industry.

The traditional dating services—including matchmaking agencies, speed dating events, and personal introductions—are projected to grow at the fastest rate, registering a CAGR of 6.3%. This resurgence reflects a growing consumer interest in curated, face-to-face experiences amid concerns about digital fatigue and superficial connections.

A primary driver of this growth is the rising demand for premium matchmaking services among affluent individuals and older demographics, who seek more structured and meaningful ways to find partners.

Besides, hybrid models that combine digital tools with in-person meetings are gaining traction. For example, elite matchmaking agencies now use AI-driven compatibility assessments before organizing exclusive events or one-on-one introductions. As consumers seek alternatives to swiping culture and algorithm-based matching, traditional dating services are repositioning themselves as premium, relationship-focused solutions, fueling their accelerated growth trajectory.

By Service Insights

Social dating led the dating services market, contributing a 37.5% of total industry revenue in 2025. Unlike adult-oriented platforms focused primarily on romantic relationships, social dating services emphasize casual interactions, friendship-building, and group activities, appealing to a broader audience.

A key reason for its leadership position is the growing popularity of lifestyle-oriented platforms that blend dating with entertainment and social networking, especially among younger users. Apps like Bumble BFF, Meetup, and Skout have expanded the definition of dating beyond romance, attracting users looking to build friendships, professional networks, or hobby-based communities.

Additionally, the integration of live video features, voice chat rooms, and virtual events has enhanced the appeal of social dating, particularly post-pandemic. With evolving user preferences and an emphasis on mental well-being through social connectivity, the social dating segment continues to expand, serving as a vital component of the broader digital dating ecosystem.

Niche dating is projected to grow at the highest CAGR of 9.4%. This rapid expansion is fueled by increasing demand for highly specialized dating platforms tailored to specific interests, cultural backgrounds, lifestyles, and professional affiliations.

One of the main drivers is the desire for more meaningful and compatible matches, as general dating platforms often fail to meet the expectations of users with unique preferences.

Moreover, regional customization and hyper-targeted marketing strategies have allowed niche platforms to effectively reach underserved audiences. In Asia, for instance, dating services like Tantan and Dil Mil cater specifically to local cultural norms and language preferences, contributing to significant user base expansion. Similarly, in the Middle East, platforms such as Muzmatch and SalamSwipe have gained popularity by aligning with Islamic values and family-oriented relationship goals.

REGIONAL ANALYSIS

North America

North America Led the global dating services market, capturing 35.5% of total revenue in 2025. The United States, in particular, serves as the epicenter of digital dating innovation, hosting some of the world’s most influential dating platforms such as Tinder, Bumble, and Match Group subsidiaries.

This dominance is largely attributed to the early adoption of digital dating culture and high smartphone penetration. Apart from these, changing societal attitudes toward online relationships have contributed significantly to widespread acceptance, especially among millennials and Gen Z.

Furthermore, strong venture capital investment and a thriving tech startup ecosystem have supported the continuous evolution of dating services in North America. As consumer behavior shifts toward hybrid and AI-enhanced dating models, North America remains at the forefront of shaping the industry’s future.

Europe

Europe is seeing rapid adoption and regulatory evolution. The region has witnessed steady growth due to increasing digital literacy, rising urbanization, and evolving relationship dynamics, particularly among younger populations.

A key growth driver is the expansion of localized dating platforms catering to linguistic and cultural nuances , such as AdopteUnMec in France and Lovoo in Germany. These platforms have successfully captured regional audiences while competing against global giants through targeted branding and community-driven engagement.

Apart from these, stricter data protection regulations under GDPR have led to increased trust among European users , prompting dating companies to invest in secure and transparent data handling practices. With regulatory frameworks influencing global best practices, Europe continues to play a pivotal role in shaping the ethical and operational standards of the dating services industry.

Asia-Pacific

Asia-Pacific represents one of the fastest-growing regions in the dating services market. Countries like China, India, and South Korea are witnessing a surge in dating app adoption due to rising disposable incomes, expanding smartphone usage, and shifting social norms.

China leads the region in terms of user volume. Meanwhile, India has emerged as a key growth market. Moreover, increased investment from global players into localized versions of dating apps has further boosted market expansion. With ongoing digital transformation and rising internet access, Asia-Pacific is poised to become a dominant force in the global dating services market in the coming decade.

Latin America

Latin America contributes descent share of the global dating services market, with Brazil, Mexico, and Colombia emerging as key growth centers. One of the primary factors driving growth is the rising influence of Western dating culture and greater smartphone affordability, which has enabled broader access to digital platforms. Additionally, the proliferation of free-to-use dating apps and gamified user experiences has attracted a large user base. Localized platforms like Amor.com and international brands such as Tinder and Badoo have adapted their offerings to suit regional preferences, incorporating Spanish and Portuguese language support, cultural references, and event-based promotions. With a growing middle class and increasing openness toward online relationships, Latin America is becoming an increasingly important market for dating service providers aiming to expand beyond traditional geographies.

Middle East and Africa

The Middle East and Africa collectively represent a small but rapidly growing segment. While conservative cultural norms historically limited dating app adoption, recent years have seen a shift, particularly in urban centers and among younger, digitally savvy populations.

In the Gulf Cooperation Council (GCC) countries, platforms like Muzmatch and SalamSwipe have gained traction by aligning with Islamic principles and promoting halal dating practices. In Sub-Saharan Africa, mobile-first dating services are flourishing due to high smartphone usage and low-cost data plans. Platforms like Zoosk and local startups such as SweepSouth have capitalized on this trend, offering culturally relevant matchmaking options to a young and dynamic population. As digital infrastructure improves and social attitudes continue to evolve, the Middle East and Africa present untapped opportunities for dating service providers willing to adapt to regional sensitivities and preferences.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies that play a noteworthy role in the global dating services market are Grindr LLC, Love Group Global Ltd., Badoo, Harmony, Inc., Spark Networks SE, Zoosk Inc., The Meet Group Inc., Spice of Life, Match Group, Inc. and Rsvp.com.au Pty Ltd.

The competition in the dating services market is highly dynamic, characterized by rapid technological advancements, evolving consumer expectations, and a growing number of players entering both mainstream and niche segments. Established giants continue to dominate due to strong brand recognition, vast user networks, and significant investment in innovation. However, emerging startups and regional players are gaining traction by offering differentiated services tailored to specific cultural, demographic, or interest-based groups. The battle for market share is intensifying as companies focus on enhancing user experience through AI-driven personalization, improved safety protocols, and hybrid models that blend digital and physical interactions. Strategic acquisitions, partnerships, and localized marketing campaigns have become essential tools for maintaining relevance in an increasingly saturated environment. As barriers to entry lower and consumer behavior continues to shift, the industry remains in a state of constant evolution, with innovation being the key determinant of long-term success.

TOP PLAYERS IN THE DATING SERVICES MARKET

Match Group, Inc.

Match Group is a global leader in the dating services industry, operating some of the most recognized platforms such as Tinder, Match.com, OkCupid, and Hinge. The company has significantly shaped the digital dating landscape by pioneering mobile-first experiences, AI-driven matchmaking, and innovative monetization models. Its diverse portfolio caters to a wide range of demographics, from casual daters to those seeking serious relationships.

IAC/InterActiveCorp

IAC owns and operates several major dating brands including Bumble, Tinder (through a joint venture), and The League. Known for its strategic acquisitions and brand incubation model, IAC has been instrumental in expanding the reach and functionality of dating platforms globally. Its emphasis on user empowerment, particularly through female-centric design and safety features, has influenced industry-wide standards.

Badoo Limited

Badoo is one of the largest dating platforms worldwide, especially dominant in Europe and Latin America. It focuses on real-time interactions, video profiles, and identity verification to enhance trust and engagement. Badoo’s contribution lies in integrating social networking elements into dating, making it more interactive and community-oriented while setting trends in user authentication and profile transparency.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Expanding into Niche and Regional Markets

Leading players are increasingly focusing on niche segments—such as LGBTQ+, religious, professional, and age-specific audiences—as well as localizing their offerings to cater to cultural preferences across different regions. This allows them to tap into underserved communities and build stronger emotional connections with users.

Enhancing User Safety and Verification Processes

To combat fraud and improve trust, companies are investing heavily in advanced identity verification tools, AI-based moderation systems, and real-time monitoring of suspicious activity. These measures not only protect users but also enhance platform credibility and encourage long-term engagement.

Integrating AI and Personalization Technologies

Major players are leveraging artificial intelligence and machine learning to refine match suggestions, personalize user experiences, and introduce interactive features like chatbots and voice assistants. These innovations increase engagement, reduce churn, and create more meaningful connections within the platform ecosystem.

RECENT HAPPENINGS IN THE MARKET

- In February 2025, Match Group launched a new AI-powered compatibility engine across its platforms, aiming to improve personalized matchmaking accuracy and increase user retention by delivering more relevant match suggestions.

- In March 2025, Bumble introduced a premium subscription tier focused on enhanced privacy features and exclusive event access, positioning itself as a safer and more elite dating option for high-value users.

- In May 2025, IAC announced the rebranding and expansion of its internal incubator to develop next-generation dating products, emphasizing immersive technologies such as augmented reality and live-streamed social experiences.

- In June 2025, Tinder partnered with cybersecurity experts to roll out mandatory photo verification and real-time behavioral analysis, reinforcing trust and reducing fake account prevalence across its global user base.

- In July 2025, ParshipGroup acquired a niche dating app targeting expatriates, expanding its international presence and diversifying its service offerings to appeal to multicultural and multilingual audiences.

MARKET SEGMENTATION

This research report on the global dating services market has been segmented and sub-segmented based on type, s, and service region.

By Type

- Online

- Offline

By Service

- Matchmaking

- Social Dating

- Adult Dating

- Niche Dating

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa