Global Decaffeinated Products Market Size, Share, Trends, & Growth Forecast Report Segmented By Product Type, Others, Process, Distribution Channel, And Region (North America, Europe, APAC, Latin America, Middle East And Africa) – Industry Analysis From 2026 to 2034

Market Size, 2025

$3.21 BnMarket Estimate, 2026

$3.43 BnMarket Forecast, 2034

$5.89 BnCAGR, 2026–2034

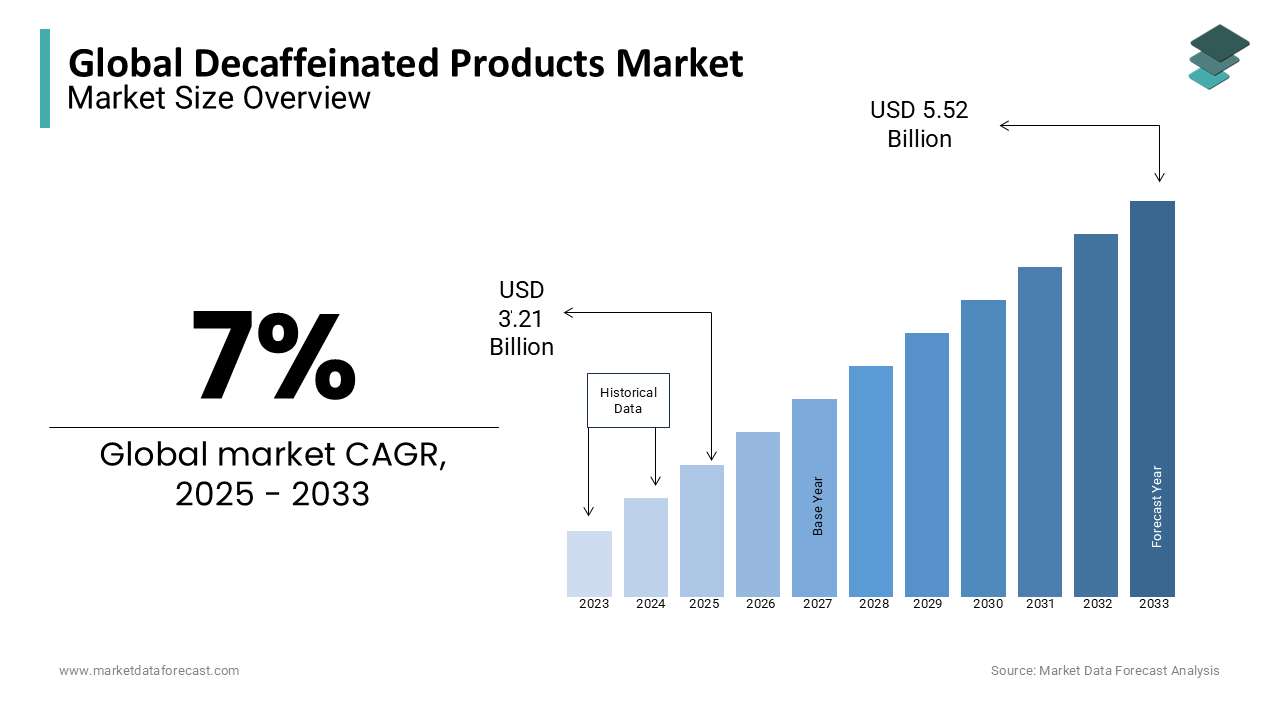

7%Global Decaffeinated Products Market Size

The global decaffeinated products market size was calculated to be USD 3.21 billion in 2025 and is anticipated to be worth USD 5.89 billion by 2034, from USD 3.43 billion in 2026, growing at a CAGR of 7% during the forecast period.

The decaffeinated products market is a diverse range of beverages and food items from which caffeine has been substantially removed, primarily targeting consumers seeking to reduce stimulant intake without sacrificing flavor or ritual. This sector includes decaffeinated coffee, tea, cocoa, and increasingly, soft drinks and energy alternatives. The process involves extracting caffeine while preserving the sensory profile of the original product, utilizing methods such as the Swiss Water Process, carbon dioxide extraction, or solvent-based techniques. Consumer awareness regarding the physiological effects of excessive caffeine consumption has catalyzed a shift towards healthier lifestyle choices, driving demand for these alternatives. According to the European Food Safety Authority, safe caffeine consumption is generally considered to be up to 400 mg per day for healthy adults, yet many individuals experience sensitivity at much lower levels, prompting them to seek decaffeinated options. As per the National Coffee Association, approximately 10% of American adults drink decaffeinated coffee each day, indicating a substantial and stable consumer base. Furthermore, the aging global population, which is more prone to sleep disorders and hypertension, contributes significantly to market growth. As per the World Health Organization, nearly 30% of adults worldwide suffer from chronic insomnia, a condition often exacerbated by caffeine intake later in the day. This demographic trend underscores the medical and lifestyle necessity for decaffeinated products, positioning them not merely as niche items but as essential components of modern dietary habits focused on wellness and balanced consumption.

MARKET DRIVERS

Growing Health Consciousness and Sleep Quality Awareness

The growth of the decaffeinated products market is primarily driven by the escalating global emphasis on health consciousness and the critical importance of sleep quality. Modern consumers are increasingly educated about the adverse effects of caffeine, such as increased heart rate, anxiety, and disrupted sleep patterns, leading them to modify their dietary habits. According to the Centers for Disease Control and Prevention, 1 in 3 adults in the United States does not get enough sleep, a statistic that has spurred a cultural shift towards evening routines that promote relaxation rather than stimulation. This behavioral change has directly increased the consumption of decaffeinated beverages in the hours leading up to bedtime. As per the World Health Organization, chronic sleep deprivation is linked to various health issues, including obesity, diabetes, and cardiovascular diseases, prompting healthcare providers to recommend caffeine reduction as a preventive measure. The rise of digital health tracking devices has further amplified this trend, as individuals monitor their sleep scores and adjust their caffeine intake accordingly. Data from major fitness tracker manufacturers indicates that users who limit caffeine consumption after 2 PM report significantly improved sleep metrics. Consequently, retailers and manufacturers are responding by expanding their decaffeinated offerings, ensuring that consumers have accessible and appealing alternatives that support their health goals without compromising on taste or social enjoyment.

Expansion of Premium Coffee Culture and Specialty Beverages

The proliferation of premium coffee culture and the specialization of beverage experiences have significantly driven the demand for high-quality decaffeinated products, which is further fuelling the decaffeinated products market expansion. Historically, decaffeinated coffee was perceived as inferior in taste, but advancements in extraction technologies have enabled producers to retain the complex flavor profiles of specialty beans. According to the Specialty Coffee Association, the consumption of specialty coffee has grown by over 10% annually in recent years, with decaffeinated options becoming an integral part of this expansion. Consumers are no longer willing to accept bland or flat-tasting decaf; instead, they seek single-origin, artisanal decaffeinated coffees that offer the same nuanced notes as their caffeinated counterparts. As per the National Coffee Association, the percentage of consumers who prefer specialty-grade decaffeinated coffee has risen steadily, reflecting a sophistication in palates that demands quality across all categories. Coffee shops and cafes are responding by training baristas in specific brewing techniques for decaf beans, ensuring optimal extraction and flavor delivery. This elevation of decaffeinated products from a commodity to a premium experience has attracted a younger demographic that values both aesthetics and health. The integration of decaf options into third-wave coffee movements ensures that the product remains relevant and desirable, driving volume growth through enhanced perceived value and customer loyalty in competitive urban markets.

MARKET RESTRAINTS

Perception of Inferior Taste and Quality

The persistent consumer perception that decaffeination compromises taste and quality is a major impediment to the decaffeinated products market growth. Despite technological advancements, a segment of consumers remains skeptical about the flavor integrity of decaffeinated coffee and tea, believing that the removal process strips away essential oils and aromatic compounds. According to a survey conducted by the International Coffee Organization, approximately 40% of non-decaf drinkers cite taste as the primary reason for avoiding decaffeinated options. This perception is rooted in older processing methods that often resulted in bland or chemically altered flavors, creating a stigma that is difficult to overcome. As per consumer behavior studies published by the Journal of Sensory Studies, blind taste tests often reveal that modern decaffeinated products are comparable to regular ones, yet the psychological bias persists among mainstream consumers. This hesitation limits market penetration, particularly among casual drinkers who are less motivated by health concerns and more by immediate sensory satisfaction. Manufacturers face the challenge of educating consumers and demonstrating the quality improvements achieved through modern methods such as supercritical carbon dioxide extraction. Until this perceptual barrier is fully dismantled, the market will struggle to convert the large base of regular caffeine consumers, restricting growth to those already predisposed to health-driven purchasing decisions.

Higher Production Costs and Retail Pricing

The higher production costs associated with decaffeination processes are further hindering the global market expansion. The decaffeination process requires additional steps, specialized equipment, and rigorous quality control measures, all of which increase the overall cost of goods sold. According to the US Department of Agriculture, the cost of producing decaffeinated coffee beans can be 20% to 30% higher than that of regular beans due to the complexity of extraction and the loss of weight during processing. As per industry analysis from the Food Marketing Institute, these increased costs are passed on to consumers, making decaffeinated products significantly more expensive than their standard counterparts. In economic environments characterized by inflation and reduced disposable income, consumers may prioritize affordability over health benefits, opting for cheaper regular coffee or tea instead. This price sensitivity is particularly pronounced in emerging markets where discretionary spending on premium beverages is limited. Furthermore, the need for separate supply chains and storage facilities to prevent cross-contamination with caffeinated products adds to logistical expenses. These financial barriers restrict the accessibility of decaffeinated products to higher-income demographics, limiting mass-market adoption and slowing the overall growth trajectory of the sector despite rising health awareness.

MARKET OPPORTUNITIES

Innovation in Natural and Chemical-Free Extraction Methods

The development and marketing of natural and chemical-free extraction methods is a substantial opportunity for the decaffeinated products market to attract health-conscious and environmentally aware consumers. Techniques such as the Swiss Water Process and mountain water method use only water and temperature to remove caffeine, avoiding the use of organic solvents like methylene chloride or ethyl acetate. According to the Organic Trade Association, the demand for organic and naturally processed foods has grown by 12% annually, indicating a strong consumer preference for clean-label products. As per the Specialty Coffee Association, certifications such as Organic and Fair Trade are increasingly important to buyers, and decaffeinated products that align with these values command a premium price. Manufacturers who highlight their use of eco-friendly and non-toxic processes can differentiate their brands in a crowded marketplace. This transparency appeals to millennials and Gen Z consumers who prioritize sustainability and health in their purchasing decisions. Additionally, these methods often preserve the antioxidant properties of the beans, offering added health benefits that can be leveraged in marketing campaigns. By investing in and promoting these advanced extraction technologies, companies can capture a loyal customer base that is willing to pay more for products that align with their ethical and health standards, thereby driving revenue growth and brand equity.

Expansion into New Product Categories Beyond Coffee and Tea

Expanding decaffeinated offerings beyond traditional coffee and tea into new product categories such as soft drinks, energy beverages, and chocolate presents a lucrative opportunity for market growth. As consumers seek to reduce overall caffeine intake, they are looking for alternatives in all aspects of their diet, not just morning beverages. According to the Beverage Marketing Corporation, the sales of decaffeinated soft drinks and functional beverages have shown steady growth, driven by parents seeking safer options for children and adults managing anxiety. As per the Confectionery Association, the demand for decaffeinated chocolate and cocoa products is rising, particularly among individuals with heart conditions or sleep disorders. This diversification allows manufacturers to tap into new revenue streams and reduce dependency on the saturated coffee market. Innovations in decaffeinating cola nuts and guarana can create unique selling propositions in the energy drink sector, appealing to consumers who want the boost of other ingredients without the jitters of caffeine. Furthermore, the integration of decaffeinated ingredients into ready-to-drink meals and snacks can address the needs of sensitive consumers throughout the day. By broadening the scope of decaffeinated products, companies can reach a wider audience and establish themselves as comprehensive wellness brands, fostering long-term customer loyalty and market expansion.

MARKET CHALLENGES

Regulatory Variations and Labeling Standards

Navigating the complex landscape of regulatory variations and labeling standards across different regions poses a significant challenge for global players in the decaffeinated products market. Definitions of what constitutes decaffeinated vary widely, with some jurisdictions requiring 97% caffeine removal while others accept lower thresholds. According to the European Union regulations, decaffeinated coffee must have no more than 0.1% caffeine content by dry weight, whereas the United States Food and Drug Administration requires that 97% of the caffeine be removed. As per the Codex Alimentarius, international standards are not uniformly adopted, creating compliance hurdles for exporters and multinational corporations. These discrepancies necessitate separate production lines and labeling protocols for different markets, increasing operational complexity and costs. Furthermore, changes in regulatory frameworks regarding the use of certain solvents in decaffeination can disrupt supply chains and force costly reformulations. Companies must invest heavily in legal and compliance teams to ensure adherence to local laws, which can be particularly burdensome for smaller enterprises. The lack of harmonization also confuses consumers, who may not understand the differences in product quality or safety standards across borders. This regulatory fragmentation impedes the seamless global expansion of decaffeinated brands and creates barriers to entry in new markets, limiting the potential for economies of scale.

Supply Chain Vulnerabilities and Raw Material Availability

The decaffeinated products market faces challenges related to supply chain vulnerabilities and the availability of high-quality raw materials suitable for decaffeination. Not all coffee beans or tea leaves are ideal for the decaffeination process, as certain varieties lose their structural integrity or flavor profile more easily. According to the International Coffee Organization, climate change impacts such as droughts and pests are reducing the yield of premium Arabica beans, which are preferred for decaffeination due to their superior taste. As per the Food and Agriculture Organization, extreme weather events have led to volatile crop yields in key producing regions like Brazil and Vietnam, causing fluctuations in supply and price. This instability makes it difficult for manufacturers to secure consistent volumes of high-quality raw material at predictable costs. Additionally, the decaffeination process itself results in a loss of bean weight and volume, requiring larger initial inputs to produce the same amount of finished product. This inefficiency exacerbates supply pressures and increases the carbon footprint of the final product. Companies must develop resilient supply chains with diversified sourcing strategies to mitigate these risks, but this requires significant investment and long-term partnerships with farmers. The inherent unpredictability of agricultural outputs, combined with the specific requirements of decaffeination, creates a fragile supply environment that can disrupt production and affect market stability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7% |

| Segments Covered | By Product, Bean Species, Distribution Channel, And Region. |

| Various Analyses Covered | Global, Regional, Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Nestlé S.A., Swiss Water Decaffeinated Coffee Inc., The Kraft Heinz Company, Starbucks Corporation, The Coca-Cola Company (Costa Coffee), Peet's Coffee, Tata Consumer Products Limited, J.M. Smucker Company, Illycaffè S.p.A., and Lavazza Group |

SEGMENTAL ANALYSIS

By Product Insights

The roasted segment held the dominant position in the market and accounted for the highest share of the global market in 2025 due to its immediate readiness for consumption and widespread availability in both retail and food service sectors. According to the National Coffee Association, over 60% of decaffeinated coffee consumers purchase pre-roasted beans or ground coffee for home brewing, highlighting the preference for ready-to-use formats. This segment benefits from established supply chains and extensive distribution networks that ensure consistent product availability across supermarkets and specialty stores. As per the Specialty Coffee Association, the majority of coffee shops offer roasted decaffeinated options as a standard part of their menu, catering to customers who wish to enjoy coffee later in the day without sleep disruption. The roasting process also enhances the aroma and flavor profile, addressing historical concerns about the taste quality of decaffeinated products. Modern roasting techniques allow for precise control over flavor development, ensuring that decaffeinated varieties meet the high expectations of discerning consumers. Furthermore, the integration of roasted decaf into single-serve pod systems has expanded its reach, appealing to users seeking quick and hassle-free brewing methods. The combination of convenience, improved taste, and broad accessibility solidifies the leadership of the roasted segment in the global decaffeinated products market.

On the other hand, the raw decaffeinated green beans segment is estimated to be the fastest-growing segment and register a CAGR of 6.2% during the forecast period. This rapid expansion is driven by the rising popularity of home roasting and the demand for transparency in sourcing among specialty coffee enthusiasts. According to the Home Roasters Guild, the number of individuals engaging in home coffee roasting has increased by 15% annually, fueled by the desire for customization and freshness. Consumers in this segment prefer purchasing raw decaffeinated beans to control the roast level and preserve specific flavor notes that may be lost in commercial roasting. As per the Specialty Coffee Association, there is a growing trend towards direct trade and ethical sourcing, with buyers seeking verified information about the origin and decaffeination method of their green beans. This transparency appeals to health-conscious consumers who want to ensure that no harmful chemicals are used in the processing. Additionally, the availability of high-quality Arabica green beans processed using natural methods such as the Swiss Water Process has enhanced the appeal of this segment. Online platforms and specialty retailers are increasingly offering curated selections of raw decaf beans, making them more accessible to hobbyists and professional roasters alike. The ability to experiment with different roast profiles and blend combinations further drives engagement, positioning raw decaffeinated beans as a dynamic and expanding niche within the broader market.

By Bean Species Insights

The Arabica beans segment led the market with the major share of the global market in 2025. The growth of the Arabica beans segment in the global market is attributed to their superior flavor profile and lower caffeine content compared to other species. Approximately 70% of global coffee production consists of Arabica beans, and this proportion is even higher in the decaffeinated segment, where taste quality is paramount. According to the International Coffee Organization, Arabica beans are preferred for decaffeination because they retain their complex aromatic compounds better during the extraction process. The naturally lower caffeine content of Arabica beans, typically around 1.2% by weight, makes the decaffeination process more efficient and less likely to compromise the bean structure. As per the Specialty Coffee Association, premium decaffeinated coffees are almost exclusively made from Arabica varieties to meet the expectations of discerning consumers who prioritize acidity, sweetness, and fruitiness. The widespread cultivation of Arabica in high-altitude regions of Latin America and Africa ensures a steady supply of high-quality raw material for processors. Furthermore, the association of Arabica with specialty and artisanal coffee cultures reinforces its dominance, as brands leverage its reputation for excellence to justify premium pricing. The versatility of Arabica beans allows them to be used in various formats, from espresso blends to single-origin offerings, catering to diverse consumer preferences. This combination of sensory superiority, processing efficiency, and market perception ensures that Arabica remains the leading species in the decaffeinated coffee sector.

However, the robusta beans segment is emerging as the fastest-growing segment in the decaffeinated market and is expected to exhibit a CAGR of 5.3% during the forecast period, owing to their increasing use in instant coffee and espresso blends. Historically overlooked for decaffeination due to their stronger and more bitter taste, Robusta beans are gaining traction as manufacturers seek cost-effective alternatives and higher caffeine yields for extraction byproducts. According to the International Coffee Organization, Robusta accounts for approximately 30% of global coffee production, and its share in the decaffeinated sector is rising due to advancements in processing technologies that mitigate undesirable flavors. As per industry reports from major instant coffee producers, the demand for decaffeinated instant coffee has grown significantly, particularly in Asia and Europe, where Robusta is the primary ingredient. The higher caffeine content of Robusta beans, around 2.2% by weight, makes them an attractive source for pharmaceutical and cosmetic industries that utilize extracted caffeine, creating an additional revenue stream for processors. Furthermore, the resilience of Robusta plants to climate change and pests ensures a more stable supply chain compared to Arabica, appealing to manufacturers concerned about long-term sustainability. Improvements in washing and roasting techniques have also enhanced the cup quality of decaffeinated Robusta, making it more palatable for mainstream consumers. These factors collectively contribute to the accelerated growth of the Robusta segment in the decaffeinated products market.

By Distribution Channel Insights

The offline segment led the market and held the largest share of the decaffeinated products market in 2025. The growth of the offline segment globally is driven by the immediate availability and tactile shopping experience they offer. According to the Food Marketing Institute, over 80% of grocery purchases still occur in physical stores, where consumers can inspect packaging, read labels, and make impulse buys. The presence of decaffeinated products in prominent retail locations ensures high visibility and accessibility for a broad demographic, including older adults who may not be frequent online shoppers. As per the National Coffee Association, many consumers prefer to purchase coffee from local cafes where they can sample decaffeinated options before buying, fostering trust and loyalty. Specialty coffee shops play a crucial role in educating customers about the quality and variety of decaf offerings, driving trial and repeat purchases. The ability to interact with knowledgeable staff and receive personalized recommendations enhances the shopping experience, encouraging consumers to explore premium decaffeinated brands. Furthermore, offline channels benefit from established logistics and inventory management systems that ensure consistent stock levels and fresh products. The immediacy of purchase satisfies the needs of consumers who require coffee for daily consumption without waiting for delivery. This combination of convenience, sensory engagement, and trusted retail environments sustains the dominance of offline distribution in the decaffeinated products market.

On the other hand, the online segment is estimated to register a CAGR of 8.2% during the forecast period in the global market, owing to the convenience of home delivery and the expanding variety of niche products available digitally. According to the US Census Bureau, e-commerce sales in the retail sector have continued to rise, with food and beverage categories showing significant adoption rates among younger demographics. Online platforms allow consumers to access a wider range of decaffeinated products, including specialty single-origin beans and rare varieties that may not be available in local stores. As per McKinsey and Company, the personalization capabilities of online retailers, such as subscription services and tailored recommendations, enhance customer retention and frequency of purchase. The ability to compare prices, read reviews, and verify certifications such as Organic or Fair Trade empowers consumers to make informed decisions aligned with their values. Additionally, the rise of direct-to-consumer brands has disrupted traditional retail models, offering competitive pricing and exclusive products that appeal to health-conscious and tech-savvy buyers. The integration of seamless payment options and fast shipping services further reduces friction in the purchasing process. As digital literacy increases and logistics networks improve, online channels are becoming the preferred choice for many consumers, driving rapid expansion in this segment of the decaffeinated products market.

REGIONAL ANALYSIS

North America Decaffeinated Products Market Analysis

In North America, the United States is likely to witness progressive commercial investments and accelerated infrastructure scaling for alternative proteins over the next few years. The United States is the primary contributor, with a significant portion of the population actively managing caffeine intake due to health concerns such as hypertension and insomnia. According to the National Coffee Association, decaffeinated coffee consumption in the US has remained stable, with millions of households incorporating it into their daily routines. The prevalence of chronic sleep disorders, as noted by the Centers for Disease Control and Prevention, further fuels demand for evening-friendly beverages. Canada also contributes to regional growth, with increasing adoption of specialty decaf options in urban centers. The region benefits from advanced retail infrastructure and a strong presence of major coffee chains that prioritize quality and variety in their decaffeinated offerings. Furthermore, the trend towards wellness and preventive healthcare encourages consumers to choose natural and chemical-free decaffeination methods. The availability of diverse product formats, from pods to whole beans, ensures broad accessibility. Regulatory support for clear labeling and safety standards also enhances consumer confidence. These factors collectively maintain North America’s leadership position, characterized by high per capita consumption and a willingness to pay premium prices for high-quality decaffeinated products.

Europe Decaffeinated Products Market Analysis

In Europe, European countries are likely to enforce stricter novel food evaluations while simultaneously integrating alternative proteins into green transition milestones for the next few years. Germany, Italy, and France are key markets, where coffee is an integral part of daily life and decaffeinated options are widely accepted. According to the European Coffee Federation, decaffeinated coffee accounts for a notable percentage of total coffee sales in these countries, reflecting cultural acceptance and habitual consumption. The European Union’s strict regulations on food additives and processing methods ensure that only high-quality and safe decaffeination techniques are used, fostering consumer trust. As per Eurostat, the aging population in Europe contributes to higher demand for health-oriented products, including decaffeinated beverages that support sleep and cardiovascular health. The region is also a hub for innovation in sustainable and organic decaffeination processes, appealing to environmentally conscious consumers. Specialty coffee shops in major cities offer premium decaf selections, driving quality improvements and market expansion. Additionally, the growing interest in wellness lifestyles among younger demographics supports the adoption of decaffeinated teas and soft drinks. The combination of regulatory rigor, cultural affinity for coffee, and health consciousness ensures that Europe remains a vital and dynamic region in the global decaffeinated products market.

Asia-Pacific Decaffeinated Products Market Analysis

In the Asia-Pacific region, key consumer markets are likely to fast-track commercial authorizations and expand production capacity to address urban food security requirements for the next few years. Countries such as Japan, South Korea, and Australia are leading the adoption of decaffeinated coffee and tea, influenced by Western lifestyle trends and local health initiatives. According to the International Coffee Organization, coffee consumption in Asia has been rising steadily, with a corresponding increase in demand for specialized products, including decaf. In Japan, the prevalence of ready-to-drink beverages has facilitated the introduction of decaffeinated options in convenience stores and vending machines. As per the Australian Bureau of Statistics, health consciousness is a key driver of food choices, with consumers seeking products that support well-being and reduce stimulant intake. The region benefits from a growing middle class that is willing to invest in premium and healthy food items. Furthermore, the expansion of international coffee chains in urban centers has increased exposure to decaffeinated options, encouraging trial and adoption. Local manufacturers are also beginning to produce decaffeinated teas and herbal blends, catering to traditional preferences. While the market share is currently smaller than in North America or Europe, the rapid pace of urbanization and changing dietary habits suggests strong future growth potential for the decaffeinated products sector in Asia-Pacific.

Latin America Decaffeinated Products Market Analysis

In Latin America, regional agricultural leaders are likely to slowly incorporate cellular biotechnology alongside traditional livestock exporting channels to capture diverse international markets for the next few years. Brazil and Colombia are key players, supplying high-quality Arabica beans for global decaffeination processes. According to the International Coffee Organization, these countries export significant volumes of green coffee beans, including those destined for decaffeination facilities in North America and Europe. Domestic consumption of decaffeinated coffee is limited but increasing in urban areas where health awareness is rising. As per the Brazilian Ministry of Health, initiatives to promote healthy lifestyles are influencing consumer behavior, leading to greater interest in low-caffeine alternatives. The region faces challenges related to economic volatility and lower purchasing power, which restrict mass-market adoption. However, the presence of international coffee chains in major cities is introducing decaffeinated options to local consumers, fostering gradual acceptance. The growth of the tourism industry also contributes to demand, as visitors seek familiar beverage options. While production dominates the regional landscape, the potential for domestic market expansion exists as health trends gain traction and income levels improve. Strategic investments in local processing and marketing could unlock new opportunities for decaffeinated products in Latin America.

Middle East and Africa Decaffeinated Products Market Analysis

In the Middle East and Africa, localized innovative hubs are likely to spearhead deep tech funding and establish rigorous compliance criteria like halal certifications for the next few years. In countries such as the United Arab Emirates and Saudi Arabia, the influence of expatriate communities and international hospitality standards has introduced decaffeinated coffee to local consumers. According to the Gulf News, the hospitality sector in the GCC countries offers extensive decaffeinated menus to cater to diverse customer preferences, including those avoiding caffeine for religious or health reasons. In Africa, local consumption of decaffeinated coffee is minimal, with most production focused on exports. However, rising awareness of health issues such as hypertension and sleep disorders is beginning to influence urban consumers in South Africa and Kenya. As per the World Health Organization, non-communicable diseases are increasing in the region, prompting some individuals to modify their diets. The lack of local processing facilities means that most decaffeinated products are imported, resulting in higher prices and limited availability. Despite these challenges, the growing presence of global coffee brands and increasing health consciousness suggest potential for gradual market development.

COMPETITION OVERVIEW

The competition in the global decaffeinated products market is characterized by the presence of established multinational corporations and niche specialty brands vying for consumer attention. Large players leverage economies of scale and extensive distribution networks to maintain dominance in mass market segments. They compete on price accessibility and brand recognition while investing heavily in marketing to reinforce trust. Specialty brands differentiate themselves through superior quality, unique origins, and artisanal processing methods, appealing to discerning consumers willing to pay premiums. Innovation in decaffeination technology serves as a key competitive advantage, allowing companies to claim better taste and safety profiles. Sustainability initiatives such as fair trade sourcing and eco-friendly packaging are increasingly used to attract environmentally conscious buyers. The rise of private label products in retail chains adds pressure on branded manufacturers to justify higher prices with added value. Digital direct-to-consumer channels enable smaller brands to bypass traditional retail barriers and build loyal communities. Overall, the market requires continuous adaptation to health trends and technological advancements to sustain competitive relevance and drive growth in a maturing industry landscape.

KEY MARKET PLAYERS

A few major players of the global decaffeinated products market include

- Nestlé S.A.

- Swiss Water Decaffeinated Coffee Inc

- The Kraft Heinz Company

- Starbucks Corporation

- The Coca-Cola Company (Costa Coffee)

- Peet's Coffee

- Tata Consumer Products Limited

- J.M. Smucker Company

- Illycaffè S.p.A

- Lavazza Group

Top Strategies Used by Key Market Participants

Key players in the decaffeinated products market focus on product innovation to enhance flavor profiles and meet clean label demands. Companies invest in advanced decaffeination technologies such as supercritical carbon dioxide extraction to ensure chemical-free processing. Brand differentiation is achieved through sustainable sourcing certifications and transparent supply chain practices. Expansion into emerging markets via strategic partnerships and localized marketing campaigns drives volume growth. Digital engagement through e-commerce platforms and subscription models enhances customer retention and data collection. Diversification into related categories like decaffeinated tea and soft drinks broadens revenue streams. Educational campaigns highlighting health benefits help overcome consumer misconceptions about taste quality. Collaborations with healthcare professionals and wellness influencers build credibility and trust. These strategies collectively enable participants to capture value in a competitive landscape while addressing evolving consumer preferences for health and sustainability.

Leading Players in the Global Decaffeinated Products Market

- Nestlé S.A. is a global leader in the decaffeinated products market with an extensive portfolio spanning coffee, tea, and instant beverages. The company leverages its advanced research and development capabilities to innovate decaffeination processes that preserve flavor and aroma. Recent actions include the expansion of its Nescafé Dolce Gusto and Starbucks at Home ranges with new decaffeinated options tailored to health-conscious consumers. Nestlé actively promotes sustainability by sourcing beans through its Coffee Plan, which supports farmers and ensures high-quality raw materials. The organization invests heavily in marketing campaigns that highlight the health benefits of switching to decaf without compromising taste. By integrating digital platforms for direct consumer engagement, Nestlé strengthens brand loyalty and expands its reach in key markets. These strategic initiatives reinforce its position as a dominant player committed to meeting evolving dietary preferences and delivering premium decaffeinated experiences globally.

- JDE Peet’s N.V. holds a significant position in the decaffeinated sector through its diverse brands, including Jacobs Douwe Egberts and Peet’s Coffee. The company focuses on delivering high-quality decaffeinated coffee that meets the stringent standards of specialty coffee enthusiasts. Recent strategies involve launching single-origin decaf varieties and enhancing packaging sustainability to appeal to environmentally aware customers. JDE Peet’s has expanded its distribution networks in emerging markets to increase accessibility and brand visibility. The organization emphasizes transparency in sourcing and processing methods, ensuring that consumers trust the quality and safety of its decaffeinated products. By investing in state-of-the-art roasting facilities, JDE Peet’s maintains consistent flavor profiles across its product lines. Collaborations with retail partners and online platforms further drive sales growth. These efforts demonstrate the company’s commitment to innovation and customer satisfaction, solidifying its role as a key contributor to the global decaffeinated products landscape.

- The Kraft Heinz Company contributes to the decaffeinated products market primarily through its Maxwell House and Gevalia brands, which offer widely accessible decaffeinated coffee options. The company focuses on affordability and convenience, catering to mainstream consumers who seek reliable decaf choices for daily consumption. Recent actions include reformulating products to improve taste and introducing eco-friendly packaging solutions to align with sustainability goals. Kraft Heinz leverages its robust supply chain and retail relationships to ensure widespread availability in supermarkets and grocery stores. The organization utilizes data-driven insights to understand consumer preferences and tailor marketing messages effectively. By promoting the versatility of its decaffeinated offerings for various brewing methods, Kraft Heinz enhances user engagement. Strategic partnerships with food service providers also expand its presence in commercial settings. These initiatives help the company maintain competitiveness and respond to the growing demand for healthy and convenient beverage alternatives in the global market.

MARKET SEGMENTATION

This research report on the global decaffeinated products market has been segmented and sub-segmented based on product type, others, process, distribution channel, and region.

By Product Type

- Ground Coffee

- Ready-to-Drink (RTD) Coffee

- Black Tea

- Herbal Tea

- Carbonated Soft Drinks (CSDs)

- Functional Drinks

- Energy Drinks

- Sugar-Free Energy Drinks

By Process

- Chemical Solvent Extraction

- Water Processing

By Others

- Bottled Water

- Kombucha

By Distribution Channel

- B2C

- Online Retailers

By Region

- North America

- Europe

- The Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What are the major product categories in this market?

Key categories include decaffeinated coffee, decaffeinated tea, decaf soft drinks, and other caffeine-free beverages.

2. What is driving the growth of the decaffeinated products market?

Rising health awareness, increasing sensitivity to caffeine, growing sleep-related concerns, and demand for healthier beverage alternatives are key drivers.

3. How is decaffeinated coffee produced?

Decaffeinated coffee is produced using methods such as the Swiss Water Process, solvent-based methods, or carbon dioxide extraction to remove caffeine.

4. Who are the primary consumers of decaffeinated products?

Health-conscious consumers, pregnant women, elderly individuals, and people sensitive to caffeine form the major consumer base.

5. Which regions dominate the global decaffeinated products market?

North America and Europe lead the market due to higher health awareness and established coffee consumption habits.

6. How does health awareness impact market growth?

Growing concerns about anxiety, insomnia, and heart health are encouraging consumers to switch to decaffeinated options.

7. What role does the food service industry play in this market?

Cafés, restaurants, and hotels increasingly offer decaffeinated options to cater to diverse customer preferences.

8. What challenges does the decaffeinated products market face?

Higher production costs, flavor perception issues, and limited awareness in developing regions are key challenges.

9. How is innovation shaping the market?

Brands are introducing flavored decaf variants, ready-to-drink options, and plant-based decaf beverages to attract new consumers.

10. What is the future outlook of the global decaffeinated products market?

The market is expected to grow steadily, driven by health trends, product innovation, and expanding availability across retail and food service sectors.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com