Global Dermatology Diagnostic Devices Market Size, Share, Trends & Growth Forecast Report By Type, Application, Dermatoscopes and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis (2024 to 2032)

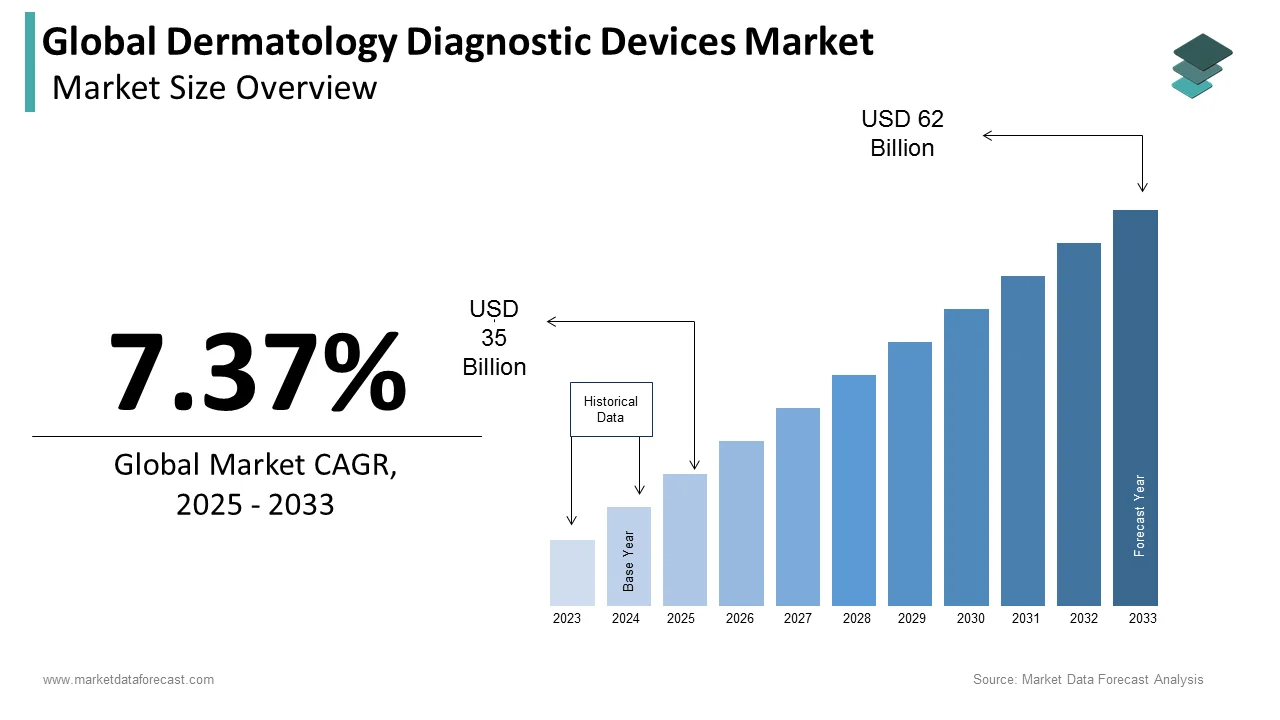

Market Size, 2025

$35Market Estimate, 2026

$37.58 BnMarket Forecast, 2034

$66.38 BnCAGR, 2026–2034

7.37%Global Dermatology Diagnostic Devices Market Report Summary

The global dermatology diagnostic devices market was valued at USD 35 billion in 2025, is estimated to reach USD 37.58 billion in 2026, and is projected to reach USD 66.38 billion by 2034, growing at a CAGR of 7.37% from 2026 to 2034. Market growth is driven by the increasing prevalence of skin disorders, including skin cancer and inflammatory conditions, along with rising awareness of early diagnosis. Technological advancements in imaging systems, dermatoscopes, and AI-powered diagnostic tools are enhancing diagnostic accuracy and efficiency. Additionally, growing demand for non-invasive diagnostic solutions and expanding dermatology clinics are supporting market expansion globally.

Key Market Trends

- Rising incidence of skin cancer and dermatological conditions.

- Increasing adoption of advanced imaging and AI-based diagnostic tools.

- Growing demand for non-invasive diagnostic technologies.

- Expansion of dermatology clinics and specialized care centers.

- Increasing focus on early detection and preventive dermatology care.

Segmental Insights

- Based on application, the skin cancer diagnosis segment dominated the global dermatology diagnostic devices market in 2025, driven by increasing awareness and screening initiatives.

- Based on type, the imaging devices segment led the market with 58.6% share in 2025, supported by advancements in high-resolution diagnostic imaging.

- Based on dermatoscopes, the cross polarized dermatoscopes segment held the largest share of 45.3% in 2025, due to superior visualization capabilities.

Regional Insights

The global dermatology diagnostic devices market is witnessing steady growth across key regions due to increasing disease burden and technological adoption.

- North America led the market in 2025 with 42.8% share, supported by advanced healthcare infrastructure and high adoption of diagnostic technologies.

- Europe followed with 28.3% share in 2025, driven by strong healthcare systems and rising awareness of skin health.

- Asia-Pacific is expected to register the fastest growth due to rising incidence of skin diseases, environmental factors, and improving healthcare access.

Competitive Landscape

The global dermatology diagnostic devices market is competitive, with key players focusing on technological innovation, product development, and expanding their global presence. Companies are investing in advanced imaging systems, AI integration, and portable diagnostic devices to enhance clinical outcomes.

Prominent companies operating in the global dermatology diagnostic devices market include Alma Lasers, Ltd., Canfield Scientific Inc., Cutera, Inc., Cynosure, Inc., 3Gen LLC, Lumenis, Ltd., Valeant Pharmaceuticals International, Inc., Bruker Corporation, Carl Zeiss, Genesis Biosystems, Inc., and Heine Optotechnik GmbH & Co. KG.

Global Dermatology Diagnostic Devices Market Size

The global dermatology diagnostic devices market was worth US$ 35 billion in 2025 and is anticipated to reach a valuation of US$ 66.38 billion by 2034 from US$ 37.58 billion in 2026, and it is predicted to register a CAGR of 7.37% during the forecast period 2026 to 2034.

The dermatology diagnostic devices are an array of instruments and systems designed to visualize, analyze, and quantify skin abnormalities for the early detection and management of cutaneous diseases. These technologies range from handheld dermoscopes and digital imaging systems to advanced confocal microscopes and optical coherence tomography scanners that provide non-invasive histological insights. The global burden of skin pathology necessitates such precision, as the World Health Organization estimates that between 2 and 3 million non-melanoma skin cancers and 132000 melanoma skin cancers occur globally each year, creating an urgent demand for accurate diagnostic tools. In Europe alone, health authorities report over 100000 new cases of melanoma annually, driving the integration of high-resolution imaging into standard clinical workflows to reduce unnecessary biopsies. The shift towards telemedicine has further amplified the relevance of these devices, with recent data indicating that over 60% of dermatology consultations in certain regions now involve some form of digital image transmission for remote assessment. Regulatory bodies like the European Medicines Agency increasingly emphasize the use of validated diagnostic aids to improve patient outcomes and streamline triage processes. As the prevalence of skin conditions rises due to environmental factors and aging populations, these devices serve as critical gatekeepers in the healthcare continuum, bridging the gap between initial visual inspection and definitive pathological diagnosis.

MARKET DRIVERS

Escalating Global Incidence of Skin Malignancies and Precancerous Lesions

The alarming rise in the global incidence of skin cancers and precancerous conditions, which necessitates early and accurate detection strategies, is propelling the growth of Europe dermatology diagnostic devices market. The International Agency for Research on Cancer projects that the number of new skin cancer cases will continue to surge, with melanoma rates increasing by approximately 3 to 7% annually in many fair-skinned populations. This epidemiological trend places immense pressure on healthcare systems to adopt advanced diagnostic tools that can distinguish between benign and malignant lesions with high specificity. Traditional visual inspection by the naked eye often lacks the sensitivity required for early-stage detection, leading to delayed diagnoses or unnecessary surgical interventions. Consequently, clinicians are increasingly relying on dermoscopy and digital mole mapping systems that offer magnification and polarized light capabilities to visualize subsurface structures invisible to the unaided eye. Furthermore, the growing awareness of ultraviolet radiation risks has led to higher screening rates, with millions of individuals undergoing annual skin checks in developed nations.

Technological Advancements in Artificial Intelligence and Digital Imaging

The rapid integration of artificial intelligence and machine learning algorithms into dermatological diagnostic devices, which enhances diagnostic precision and workflow efficiency, is additionally leveraging the growth of the dermatology diagnostics devices market. Modern digital dermoscopes and total body photography systems now incorporate AI-driven software capable of analyzing lesion patterns, asymmetry, and color variations with performance metrics that rival or exceed those of experienced dermatologists. According to recent clinical validations published in Nature Medicine, AI algorithms trained on vast datasets of over 100000 images have demonstrated sensitivity levels exceeding 95% in detecting melanomas, providing a powerful decision support tool for practitioners. This technological leap addresses the shortage of specialized dermatologists in many regions, allowing general practitioners to perform preliminary assessments with greater confidence. The ability of these systems to store longitudinal data and track minute changes in lesion morphology over time facilitates proactive monitoring of high-risk patients. Moreover, the seamless integration of these devices with electronic health records and telemedicine platforms enables remote diagnostics, expanding access to care in rural and underserved areas.

MARKET RESTRAINTS

High Capital Expenditure and Reimbursement Limitations

The widespread adoption of advanced devices is limited by the substantial capital investment required for acquisition and maintenance, which, coupled with inconsistent reimbursement policies across different healthcare systems, is limiting the growth of the dermatology diagnostic devices market. High-end systems such as reflectance confocal microscopes and total body photography units often carry price tags ranging from 50000 to 150000 US dollars, placing them out of reach for smaller private practices and clinics in developing regions. While these devices offer superior diagnostic capabilities, the lack of specific reimbursement codes for procedures utilizing these advanced technologies in many countries discourages their utilization. For instance, in several European healthcare markets, insurance providers do not fully cover the costs associated with digital dermoscopy or AI-assisted analysis, forcing patients to pay out of pocket or limiting the frequency of such examinations. This financial barrier creates a disparity in access to cutting-edge diagnostics, where only large hospital networks or affluent private clinics can afford to implement these tools. Additionally, the ongoing costs for software licenses, data storage, and regular calibration add to the total cost of ownership, further straining operational budgets.

Shortage of Trained Professionals and Standardization Gaps

The global shortage of dermatologists trained to operate sophisticated diagnostic devices and interpret complex imaging data effectively is restraining the growth of the dermatology diagnostic devices market. While the technology itself has advanced rapidly, the educational infrastructure required to train clinicians in the nuances of dermoscopy, confocal microscopy, and AI interpretation has lagged. Data from the American Academy of Dermatology suggests that there is a significant deficit of board-certified dermatologists, with ratios as low as one dermatologist per 30000 people in certain areas, exacerbating the bottleneck in adopting new technologies. Even when devices are available, the lack of standardized training protocols leads to variability in image acquisition and interpretation, which can compromise diagnostic accuracy and erode clinician confidence in the technology. Furthermore, the absence of universally accepted guidelines for the use of AI algorithms in clinical settings creates uncertainty among practitioners regarding liability and best practices. This skills gap is particularly pronounced in rural and low-resource settings where access to continuing medical education is limited.

MARKET OPPORTUNITIES

Expansion of Teledermatology and Remote Monitoring Solutions

The remote diagnosis and monitoring of skin conditions across vast geographical distances is creating new opportunities for the growth of the dermatology diagnostic devices market. The global telehealth market has witnessed exponential growth, with projections indicating that over 40% of all dermatology consultations will be conducted virtually by 2026, driven by patient demand for convenience and the need to alleviate clinic overcrowding. This shift creates a robust demand for portable, high-resolution diagnostic devices such as smartphone-attached dermoscopes and handheld digital imagers that allow patients or primary care providers to capture clinical-grade images at home or in remote locations. These devices facilitate the transmission of high-quality data to specialists for review, effectively extending the reach of expert care to underserved populations. Recent studies have shown that tele dermatology programs utilizing digital imaging can reduce wait times for specialist appointments by up to 50% while maintaining diagnostic accuracy comparable to in-person visits. As healthcare systems increasingly prioritize decentralized care models to reduce costs and improve accessibility, the integration of connected diagnostic devices into telemedicine platforms becomes essential.

Integration of Multimodal Imaging and Personalized Medicine

The emergence of multimodal imaging technologies with personalized medicine approaches offers a lucrative avenue for innovation, in addition to leveraging the growth of the dermatology diagnostic devices market. By combining different imaging modalities such as dermoscopy, optical coherence tomography, and fluorescence imaging into single unified platforms, manufacturers can provide comprehensive diagnostic insights that were previously unattainable with single-modality devices. This holistic approach allows for the detailed characterization of skin lesions at various depths, facilitating more precise treatment planning and monitoring of therapeutic responses. The rise of personalized medicine, which tailors treatments based on individual genetic and phenotypic profiles, relies heavily on accurate baseline data provided by these advanced imaging systems. Furthermore, the ability of these integrated systems to quantify treatment efficacy objectively supports the development of novel drug regimens and improves patient adherence. As pharmaceutical companies and clinical research organizations increasingly seek robust endpoints for trials, the demand for sophisticated imaging biomarkers grows, creating new revenue streams for device manufacturers who can offer versatile, high-performance multimodal solutions.

MARKET CHALLENGES

Regulatory Hurdles and Data Privacy Concerns

The complex landscape of regulatory approvals and addressing escalating data privacy concerns for manufacturers is a quiet challenge for the growth of the dermatology diagnostic devices market. The classification of these devices, particularly those incorporating artificial intelligence, varies significantly across jurisdictions, leading to prolonged and costly approval processes. For example, the European Union's Medical Device Regulation, implemented in recent years, has introduced stricter requirements for clinical evidence and post-market surveillance, causing delays in the launch of new products and increasing compliance burdens for companies. Simultaneously, the handling of sensitive patient images and health data by connected devices raises significant privacy issues under regulations such as the General Data Protection Regulation in Europe and the Health Insurance Portability and Accountability Act in the United States. Breaches of patient data can result in severe legal penalties and loss of trust, compelling manufacturers to invest heavily in cybersecurity measures and data encryption technologies.

Algorithmic Bias and Clinical Validation Requirements

The issue of algorithmic bias in AI-driven diagnostic tools and the rigorous requirement for extensive clinical validation across diverse populations iareadditionally limiting the growth of the dermatology diagnostic devices market. Many artificial intelligence models used in dermatology have been trained predominantly on datasets comprising light-skinned individuals, leading to reduced accuracy and higher error rates when diagnosing conditions in patients with darker skin tones. Research published in leading medical journals has highlighted that these biases can result in misdiagnosis and delayed treatment for minority populations, raising ethical concerns and limiting the universal applicability of these technologies. Furthermore, regulatory bodies increasingly demand robust clinical trials that demonstrate the efficacy and safety of these devices across all demographic groups before approving. The lack of standardized benchmarks for evaluating AI performance in real-world settings adds another layer of complexity, making it difficult for clinicians to compare different solutions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Application, Type, Dermatoscopes, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Alma Lasers, Ltd., Cutera, Inc., Cynosure, Inc., Lumenis, Ltd., Valeant Pharmaceuticals International, Inc., Gen, Inc., Bruker Corporation, Carl Zeiss, Genesis Biosystems, Inc., Heine Optotechnik GmbH & Co. KG., and Others. |

SEGMENTAL ANALYSIS

By Application Insights

The skin cancer diagnosis segment was the largest by holding a dominant share of the Dermatology Diagnostic Devices Market in 2025, owing to the alarming and continuous rise in the global incidence of both melanoma and non-melanoma skin cancers, which necessitates widespread screening and precise diagnostic capabilities. The World Health Organization estimates that between 2 and 3 million non-melanoma skin cancers and over 132000 melanoma cases occur globally each year, creating a massive patient pool requiring diagnostic evaluation. In regions with high ultraviolet exposure, such as Australia and North America, incidence rates have doubled over the past two decades, placing immense pressure on healthcare systems to adopt efficient diagnostic workflows. This epidemiological surge drives hospitals and clinics to invest heavily in dermoscopes and digital imaging systems that can differentiate malignant lesions from benign ones with high specificity. Consequently, government health initiatives and private healthcare providers are prioritizing the procurement of these devices to manage the growing caseload by ensuring that the skin cancer diagnosis segment remains the largest revenue generator in the market.

The other diagnostic applications segment is projected to register the fastest CAGR of 11.5% from 2026 to 2034, owing to the escalating global prevalence of chronic inflammatory skin diseases such as psoriasis, eczema, and rosacea, which require ongoing monitoring and precise assessment. The World Health Organization reports that psoriasis affects approximately 2 to 3% of the global population, translating to over 125 million individuals who require regular dermatological evaluation and treatment adjustment. Traditional methods of assessing disease severity are often subjective and prone to interobserver variability, leading to inconsistent treatment outcomes. Advanced diagnostic devices equipped with high-resolution imaging and quantitative analysis software offer objective metrics for evaluating lesion size, erythema, and scaling, enabling more personalized and effective treatment plans. As the burden of these chronic conditions increases due to lifestyle factors and environmental triggers, the demand for tools that facilitate accurate longitudinal monitoring grows exponentially. Furthermore, the development of novel biologic therapies for these conditions necessitates precise biomarkers to measure therapeutic response, further driving the adoption of sophisticated diagnostic imaging.

By Type Insights

The imaging devices segment was the largest by holding 58.6% of the dermatology diagnostic devices market share in 2025 due to their ability to provide superior diagnostic accuracy through high-resolution digital imaging and seamless integration with electronic health records and artificial intelligence algorithms. According to recent clinical studies, digital dermoscopy systems combined with AI analysis achieve sensitivity levels exceeding 95% in detecting melanoma, outperforming conventional methods. Furthermore, the capability to store and compare images over time allows for precise monitoring of lesion evolution, a feature for managing high-risk patients. The integration of these devices with cloud-based platforms facilitates tele dermatology, enabling remote consultations and second opinions, which have become increasingly vital in the post pandemic healthcare sector.

The microscopes segment is anticipated to witness the fastest CAGR of 12.8% from 2026 to 2034, owing to the growing clinical demand for non-invasive optical biopsy capabilities that can provide real-time, cellular-level diagnosis without the need for surgical tissue extraction. Reflectance confocal microscopy allows clinicians to visualize the epidermis and upper dermis with resolution comparable to histopathology, enabling immediate diagnosis of ambiguous lesions. As healthcare systems face pressure to minimize invasive procedures and optimize operating room utilization, the adoption of these "optical biopsy" tools is accelerating. The ability to make immediate treatment decisions during the patient visit enhances workflow efficiency and patient satisfaction. Furthermore, the technology is increasingly being used to define tumor margins before surgery, ensuring complete removal while sparing healthy tissue.

By Dermatoscopes Insights

The cross-polarized dermatoscopes segment was the largest by holding 45.3% of the dermatology diagnostic devices market share in 2025 due to their ability to provide high-quality images of subsurface skin structures by eliminating surface reflection without the need for direct contact or immersion liquids. Studies indicate that polarized light dermoscopy reveals specific structures, such as white shiny lines and crystalline structures,s that are not visible with non-polarized methods, thereby enhancing diagnostic accuracy for certain types of skin cancers. The ease of use allows for rapid scanning of multiple lesions, making it ideal for high-volume clinical settings and total body screenings. Furthermore, the ability to switch between polarized and non-polarized modes in many modern devices offers clinicians versatility in visualizing different skin features.

The hybrid dermatoscopes segment is likely to witness the fastest CAGR of 13.2% from 2026 to 2034. The growth of the segment is majorly driven by their unique ability to offer both polarized and non-polarized viewing modes in a single device, providing clinicians with a comprehensive toolkit for diagnosing a wide variety of skin conditions. Certain structures, such as milia-like cysts and comedo-like openings, are best viewed with non-polarized light, while vascular structures and shiny white streaks are better visualized with polarized light. Research demonstrates that the combination of both modes increases the overall diagnostic accuracy and confidence of dermatologists, particularly in complex cases. This versatility eliminates the need for purchasing and maintaining separate devices, offering a cost-effective solution for practices seeking to maximize their diagnostic capabilities. As the complexity of dermatological cases increases and the demand for precision grows, clinicians are increasingly preferring hybrid systems that do not compromise on any front.

REGIONAL ANALYSIS

North America Dermatology Diagnostic Devices Market Analysis

North America was the outperformer in the global Dermatology Diagnostic Devices Market by occupying 42.8% of the share in 2025, owing to the highest number of skin cancer cases globally, with over 5 million people treated for skin cancer annually, driving immense demand for diagnostic tools. Furthermore, the favorable reimbursement landscape provided by Medicare and private insurers for dermoscopy and digital imaging procedures encourages widespread adoption in clinical practices. The region also boasts a high density of board-certified dermatologists who are quick to integrate new technologies into their workflows to improve patient outcomes. Significant investment in research and development by academic institutions and government bodies like the National Institutes of Health further supports the validation and commercialization of novel diagnostic devices.

Europe Dermatology Diagnostic Devices Market Analysis

Europe dermatology diagnostic devices market ranked second by accounting for 28.3% of the market share in 2025, owing to the high incidence of skin cancer in countries with fair-skinned populations, such as Germany, the United Kingdom, and Scandinavia, where melanoma rates are among the highest in the world. Government initiatives in these nations focus on early detection programs, providing funding for screening campaigns that utilize advanced diagnostic devices. The implementation of the EU Medical Device Regulation has raised the bar for device quality and safety, fostering trust among clinicians and patients in certified technologies. Additionally, the growing integration of dermatology services into primary care and the expansion of tele dermatology networks across the continent are stimulating demand for portable and connected diagnostic tools.

Asia-Pacific Dermatology Diagnostic Devices Market Analysis

Asia-Pacific Dermatology Diagnostic Devices Market is anticipated to have the fastest CAGR throughout the forecasted years, owing to the rising incidence of skin cancers and inflammatory skin diseases due to changing lifestyles and environmental factors, coupled with a growing geriatric population that is more susceptible to skin conditions. Countries like Japan and Australia (often grouped in APAC for market analysis) have high skin cancer rates driving demand, while emerging economies like China and India are witnessing a surge in demand for aesthetic and diagnostic dermatology due to increased disposable income. Government initiatives to improve healthcare access in rural areas are leading to the deployment of portable and cost-effective diagnostic devices. The region is also becoming a manufacturing hub for medical devices, reducing costs and improving availability. The rapid adoption of smartphone-based diagnostic solutions and telemedicine platforms is bridging the gap caused by a shortage of dermatologists in many parts of the region.

Latin America Dermatology Diagnostic Devices Market Analysis

Latin America Dermatology Diagnostic Devices Market growth is likely to have prominent opportunities in the coming years, with the high prevalence of skin diseases due to tropical climates, a growing focus on skin cancer awareness, and an expanding private healthcare sector in countries like Brazil and Mexico. The high exposure to ultraviolet radiation in many countries leads to elevated rates of skin cancer and other sun-related skin conditions that necessitate regular screening, which is also driving the growth of the segment. Brazil has launched national campaigns to raise awareness about skin cancer, encouraging the population to seek regular dermatological check-ups. The growth of the private healthcare sector and medical tourism, especially for dermatological and aesthetic procedures, is boosting the demand for advanced diagnostic equipment in major urban centers. International collaborations and donations of medical equipment are also helping to improve diagnostic capabilities in public hospitals.

Middle East and Africa Dermatology Diagnostic Devices Market Analysis

The Middle East and Africa Dermatology Diagnostic Devices Market is driven by strategic government initiatives to develop world-class healthcare facilities, particularly in countries like Saudi Arabia, the United Arab Emirates, and South Africa. These nations are investing heavily in importing advanced medical technologies to reduce the need for patients to travel abroad for treatment. In Africa, the rising incidence of skin cancer among albino populations and the high burden of infectious skin diseases are creating an urgent need for affordable and robust diagnostic tools. The increasing awareness of skin health and the gradual expansion of insurance coverage in some countries are also contributing to market growth.

COMPETITIVE LANDSCAPE

The competition in the Dermatology Diagnostic Devices Market is characterized by intense rivalry among established optical manufacturers and emerging technology firms specializing in artificial intelligence and digital health. Major corporations leverage their extensive distribution networks and brand reputation to drive adoption of high-end imaging systems, while smaller innovators differentiate themselves through niche software solutions and portable hardware. The landscape is shifting as companies increasingly focus on integrating machine learning algorithms to automate lesion analysis and reduce diagnostic variability. Competitive dynamics are further influenced by the growing demand for tele dermatology tools, which require seamless connectivity and user-friendly interfaces. Players are also competing based on data security features and compliance with stringent global regulations such as the European Union Medical Device Regulation. The entry of consumer electronics giants into the wearable health monitoring space poses a potential disruptive threat, forcing traditional vendors to adapt rapidly.

KEY MARKET PARTICIPANTS

Major Competitors in the global dermatology diagnostic devices Market profiled in the report are

- Alma Lasers, Ltd.

- Canfield Scientific Inc

- Cutera, Inc.

- Cynosure, Inc.

- 3Gen LLC

- Lumenis, Ltd.

- Valeant Pharmaceuticals International, Inc.

- Bruker Corporation

- Carl Zeiss

- Genesis Biosystems, Inc.

- Heine Optotechnik GmbH & Co. KG

TOP PLAYERS IN THE MARKET

- Canfield Scientific Inc stands as a global leader in the Dermatology Diagnostic Devices Market by providing advanced imaging systems and software solutions for skin analysis. The company specializes in total body photography, dermoscopy, and wound assessment technologies that are widely used in clinical research and private practice. Canfield strengthens its market position through continuous innovation in artificial intelligence integration and cloud-based data management platforms. Recent actions include the launch of enhanced digital dermoscopy systems capable of real-time lesion tracking and automated risk assessment. The corporation actively collaborates with major pharmaceutical companies to support clinical trials requiring precise dermatological endpoints.

- 3Gen LLC maintains a significant presence in the Dermatology Diagnostic Devices Market through its extensive portfolio of handheld and digital dermatoscopes designed for diverse clinical settings. The company is renowned for delivering cost-effective yet high-quality diagnostic tools that cater to both dermatologists and primary care physicians. 3Gen recently focused on expanding its product line to include hybrid dermatoscopes that combine polarized and non-polarized light sources for superior image clarity. Their strategic initiatives involve developing smartphone-compatible accessories that facilitate tele dermatology and remote consultations. The firm actively engages in educational programs to train healthcare providers on effective dermoscopic techniques and early melanoma detection.

- Heine Optotechnik GmbH and Co KG exerts considerable influence in the Dermatology Diagnostic Devices Market by leveraging its century-long expertise in precision optical instruments. The German manufacturer offers a comprehensive range of dermatoscopes and illumination systems known for their exceptional optical quality and durability. Heine strengthens its market standing by integrating digital connectivity into its traditional optical devices, allowing seamless image capture and documentation. Recent developments include the introduction of battery-powered LED dermatoscopes with adjustable polarization modes to suit different diagnostic needs. The corporation focuses on expanding its global distribution network and establishing service centers to ensure reliable support for international clients.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Dermatology Diagnostic Devices Market predominantly employ product innovation and strategic partnerships to maintain a competitive advantage. Companies frequently launch advanced imaging systems integrated with artificial intelligence algorithms to enhance diagnostic accuracy and workflow efficiency. Another major strategy involves the expansion of tele dermatology capabilities by developing portable devices compatible with smartphones and cloud platforms. Market participants also focus on acquiring specialized technology startups to rapidly incorporate novel imaging modalities such as confocal microscopy into their portfolios. Furthermore, firms actively engage in clinical collaborations and research studies to validate the efficacy of their devices and secure regulatory approvals. These organizations prioritize comprehensive training programs and educational initiatives to foster user proficiency and build long-term loyalty among healthcare professionals globally.

MARKET SEGMENTATION

This research report on the global dermatology diagnostic devices market has been segmented and sub-segmented based on application, type, dermatoscopes, and region

By Application

- Skin Cancer Diagnosis

- Other Diagnostic Applications

By Type

- Imaging Devices

- Dermatoscopes

- Microscopes

By Dermatoscopes

- Contact Oil Immersion Dermatoscopes

- Cross-Polarized Dermatoscopes

- Hybrid Dermatoscopes

By Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the global dermatology diagnostic devices market?

The global dermatology diagnostic devices market includes devices for detecting and diagnosing skin conditions like cancer, acne, eczema, and other disorders globally

2. What drives growth in the global dermatology diagnostic devices market?

Growth is driven by increasing skin disease prevalence, advances in imaging technologies, rising demand for non-invasive diagnostics, and teledermatology expansion

3. Which devices dominate the global dermatology diagnostic devices market?

Imaging devices and dermatoscopes hold the largest shares due to their widespread use in early skin disease detection in the global dermatology diagnostic devices market

4. How does AI impact the global dermatology diagnostic devices market?

AI accelerates lesion analysis, enhances diagnostic accuracy, and supports telemedicine, boosting efficiency in the global dermatology diagnostic devices market

5. What regions lead the global dermatology diagnostic devices market?

North America leads in market share, followed by rapid growth in Asia-Pacific driven by increasing healthcare expenditure and medical tourism

6. How important are teledermatology tools in the global dermatology diagnostic devices market?

Teledermatology tools enable remote skin assessments and follow-ups, improving access and diagnosis rates within the global dermatology diagnostic devices market.

7. What role do skin cancer detection tools play in the global dermatology diagnostic devices market?

They are critical for early diagnosis, improving survival rates and driving demand in the global dermatology diagnostic devices market

8. What challenges affect the global dermatology diagnostic devices market?

Challenges include high device costs, regulatory approvals, need for skilled operators, and competition from alternative diagnostic methods

9. How do dermatology clinics contribute to the global dermatology diagnostic devices market?

Clinics form the largest end-user segment as they provide specialized diagnosis and treatment utilizing advanced dermatology devices

10. What recent trends are shaping the global dermatology diagnostic devices market?

Trends include increased AI adoption, integration with mobile devices, personalized dermatology, and minimally invasive diagnostics

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com