Global Digital Audio Workstation Market Size, Share, Trends, & Growth Forecast Report By Type (Recording, Editing, Mixing), End-Use (Commercial and Non-Commercial), Component (Software and Services), Deployment Model (Cloud and Local), Operating Systems (Mac OS, Windows, Linux, Others), & Region, Industry Forecast From 2024 to 2033

Global Digital Audio Workstation Market Size

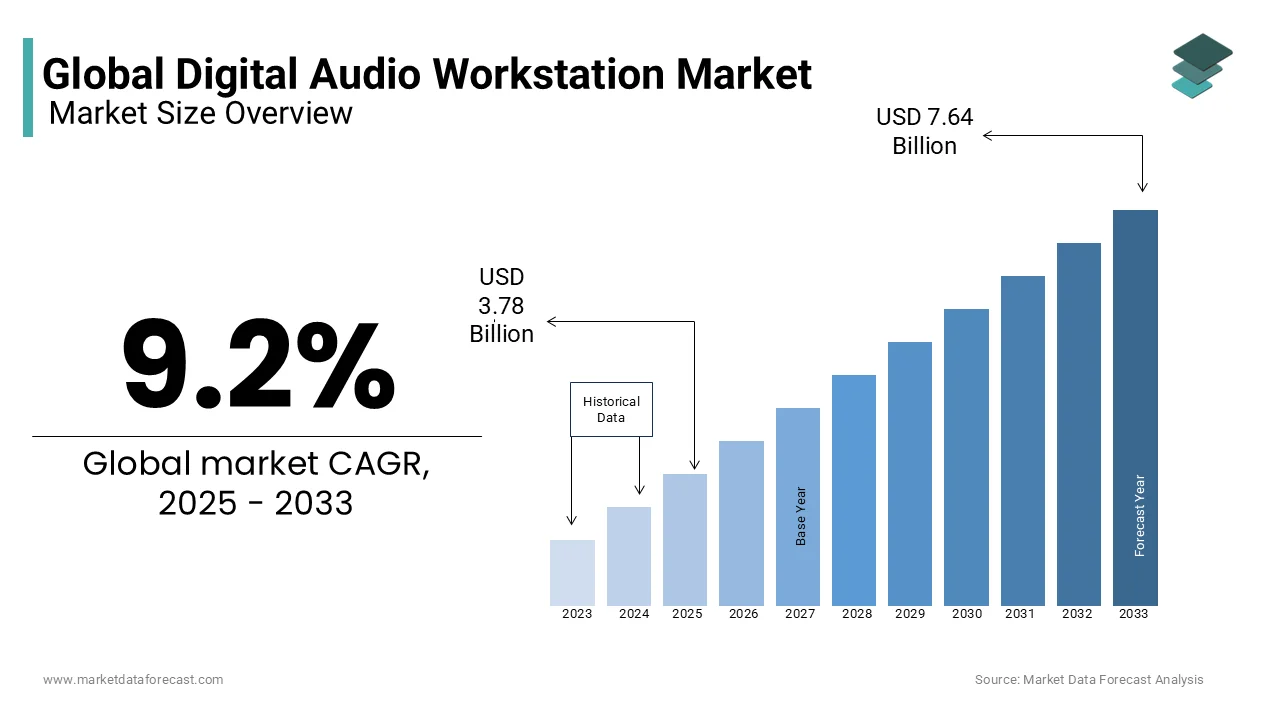

The global digital audio workstation (DAW) market was worth USD 3.46 billion in 2024. The global market is expected to reach USD 3.78 billion in 2025 and USD 7.64 billion by 2033, growing at a CAGR of 9.2% during the forecast period 2025 to 2033.

A digital audio workstation (DAW) is a sophisticated software environment sometimes integrated with hardware designed for recording, editing, mixing, and producing audio content across music, podcasts, film, and broadcasting. Nearly half of professional musicians now juggle multiple DAW platforms to leverage creative flexibility. This confluence of digital access, affordability, and cross-platform agility is redefining DAWs from niche tools to mainstream production workhorses.

MARKET DRIVERS

Boom in Independent Creation and Home Studios

The expansion of DAW usage is propelled by the proliferation of independent artists and home-based production setups. This user growth has been made possible by low-cost or freemium DAWs that lower the entry barrier for creators across genres. The affordability and flexibility of modern DAWs encourage users to produce high-quality audio from bedrooms or hobbyist spaces, challenging the traditional dominance of high-priced studio infrastructure. This shift has redefined audio production by empowering a broader, creatively diverse cohort of musicians, podcasters, and content makers to operate independently.

Internet Penetration Fueling Cloud and Collaboration

DAWs have benefited immensely from broad internet accessibility. This connectivity has enabled composers, producers, and sound engineers to collaborate remotely, with out-of-studio gigs no longer limiting creative synergy. Plus, streamlined online marketplaces for plugins and instrument libraries have enhanced DAW versatility. The fusion of network connectivity and cloud functionality is transforming DAWs into collaborative platforms rather than isolated desktop tools, amplifying their adoption and relevance in modern digital workflows.

MARKET RESTRAINTS

Steep Learning Curve & Complexity

The complexity of mastering these tools is one major barrier to DAW adoption. A significant share of potential users, particularly newcomers and non-technical hobbyists, are deterred by the intricate interfaces and steep learning curves of professional-grade DAWs. Navigating multi-track editing, automation lanes, plugins, and MIDI sequencing demands both time and expertise. For many aspiring creators, this complexity fosters frustration or premature abandonment, slowing broader DAW uptake, a constraint particularly acute in regions where formal audio training is scarce.

Software Piracy Erodes Developer Revenues

Software piracy remains a thorn in the DAW industry. Although anti-piracy mechanisms are increasingly deployed, the prevalence of cracked versions and pirated licenses persists, especially in markets with limited purchasing power or weak enforcement. This revenue leakage inhibits feature development, platform interoperability, and quality enhancements, ultimately dampening the sustainability of DAWs as evolving creative tools for global users.

MARKET OPPORTUNITIES

Cloud-Based DAWs & Remote Collaboration

The shift toward cloud-native DAWs is yielding compelling opportunities. This trend enables multiple creators to work simultaneously on a project from any location, fostering creative synergies among producers, musicians, and sound engineers across the globe. Cloud DAWs also lower hardware dependency, empowering small-scale creators and educational environments to access professional tools without expensive infrastructure.

AI-Enhanced Production Tools

Artificial intelligence integration in DAWs is unlocking unprecedented creative and production efficiencies. This has made high-quality audio production accessible not only to professionals but also to novice podcasters and music makers. As AI continues to evolve and embed into DAWs, it promises to democratize creativity further, enabling users to focus on artistic expression rather than technical minutiae.

MARKET CHALLENGES

Monetization in Freemium DAW Landscape

DAWs offering free or freemium tiers, like BandLab, present monetization complexities. Developers must strike a balance: provide sufficient capability to retain users while incentivizing upgrades without alienating the base. This precarious balance between wide access and revenue generation can limit investments in product enrichment if monetization strategies falter.

Standardization Across Diverse Platforms

The DAW ecosystem is fragmented, with dozens of platforms like Pro Tools, Logic, FL Studio, and others, each using different file formats, plugin standards, and workflows. Inconsistent compatibility across environments impedes collaborative workflows and adoption fluidity. Without unified standards or seamless cross-platform migration, creators face friction when transitioning, sharing, or integrating work across different DAW ecosystems, a barrier to streamlined production.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.2% |

| Segments Covered | By Type, End Use, Component, Deployment Mode, Operating System, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Apple (USA), Adobe (USA), Avid (USA), Steinberg (Germany), Ableton (Germany), MOTU (USA), Acoustica (USA), Native Instruments (Germany), MAGIX (Germany), Presonus (United States), Cakewalk (United States), Inage Line Software (Belgium), Bitwig (Germany), Renoise (Germany), Harrison Consoles (United States), and Others. |

SEGMENTAL ANALYSIS

By Component Insights

The software segment remained the prominent category in the market. DAWs’ core is software, multi-track editing, MIDI control, and a virtual instrument, all live inside software. Such capabilities are essential, and software remains the dominant driver behind market volume.

The services segment is the fastest-growing. People love updates, cloud access, and tutorials, so recurring revenue models and support ecosystems are quickly accelerating.

By Operating System Insights

In terms of compatibility with operating systems, the Mac OS segment represents a significant part of the market and is expected to maintain its leading position in the market during the forecast period. The growing adoption of Mac OS in recording and editing digital audio files is expected to drive demand during the forecast period. Mac offers a better overall solution for many users due to the excellent build quality and stability of Mac OS. Besides these, audio innovators are emphasizing adaptability and flexibility as virtualisation expedites. Industry experts have said the perception that broadcast audio is undergoing a significant shift, i.e., moving away from committed hardware to virtualised systems, which can assist an enormous variety of outputs and workflows, cannot be overlooked. So, the segment is expected to grow further in the coming years. Even though both PCs and Macs are utilised in post-production studios in Hollywood and there are convincing reasons for both sides, Apple excels with its native software, such as Motion and Final Cut Pro, whereas Macs and PCs perform effectively with other NLE software like Adobe Premiere Pro. On the other hand, PCs are usually available at a reduced cost and are affordable choices for hardware customization and upgrade options.

By Deployment Mode Insights

The on-premise (local) deployment segment led the market. The on-premises segment is dominant due to its widespread use in professional studios requiring stability and high performance. Professionals still rely on local DAWs for latency control, secure environments, and hardware integration.

The cloud-based segment is growing fastest, spurred by demand for flexible, accessible, collaborative DAWs across devices and locations. Especially in today’s remote, hybrid workflows, real-time sync and platform-agnostic access are game-changers.

By Type Insights

The editing segment was the biggest slice of the DAW pie. This prominence stems from musicians and producers gravitating toward platforms that emphasize ease of slicing, trimming, and arranging audio, key to efficient production. Also, editing capabilities serve as the backbone for adoption, offering users the power to sculpt audio quickly even when starting from scratch.

By End Use Insights

The commercial usage segment dominated the market. This makes sense; professional studios, broadcasters, and film/music enterprises demand premium audio tools. High-stakes production and live events push commercial DAWs to deliver precision, stability, and power, all of which justify the strong market share.

The individual (non-commercial) segment is fuelling the fastest upswings. The rise of home studios, YouTube creators, podcasters, and bedroom producers, empowered by accessible software and online tutorials, is powering this surge.

REGIONAL ANALYSIS

The global market for digital audio workstations by region encompasses North America, Asia-Pacific (APAC), Europe, the Middle East and Africa (EMEA), and Latin America. North America has the largest market share due to the early adoption of advanced technology solutions and vendor initiatives to reach the end user base. The United States and Canada are increasingly seeing the adoption of advanced technologies, including Android and Linux operating systems. Moreover, explosive growth has been experienced in the demand for music recording studios in the United States since the beginning of 2022; as a result, the region’s market size has expanded significantly. In addition, from powerful DAW applications such as FL Studio Mobile and GarageBand to simple mixers like MicPad, the transformation of mobile music apps has also contributed to the rise of the market expansion in the region. This has made music or audio composition on mobile devices as effective and serious as it is on workstations or personal computers.

- Furthermore, in October 2024, Ardour 8.10, an open-source digital audio workstation (DAW), was introduced and is available for customers in the USA and worldwide. This release comprises several bug fixes and enhancements over previous versions. Also, it solves considerable performance problems, improves MIDI operations.

Europe's digital audio workstation market is predicted to expand during the forecast period, owing to the fusion of modern technology and culture. The European Union is a key music market; however, it is not progressing as quickly as other global markets.

- According to a study by the International Federation of the Phonographic Industry, in 2023, the EU revenue generation from recorded music grew to an overall 5.2 billion euros by 8.2 per cent. However, compared to other markets and regions, its growth rate is substantially less, i.e., Mexico expanded by 8.2 per cent and China by 25.8 per cent, whereas Europe fell behind the world’s by 10.2 per cent.

KEY PLAYERS IN THE MARKET

The major companies operating in the global digital audio work station market include Apple (USA), Adobe (USA), Avid (USA), Steinberg (Germany), Ableton (Germany), MOTU (USA), Acoustica (USA), Native Instruments (Germany), MAGIX (Germany), Presonus (United States), Cakewalk (United States), Inage Line Software (Belgium), Bitwig (Germany), Renoise (Germany), Harrison Consoles (United States), and others.

TOP LEADING PLAYERS IN THE MARKET

Avid Technology

Avid, maker of the legendary Pro Tools, is a go-to in pro studios worldwide. In the Asia Pacific, they've deepened engagement through regional partnerships and training centers, nurturing adoption in film scoring and broadcast houses. Their push toward subscription-based licensing improves affordability for emerging APAC markets. Plus, cloud-enabled workflows like MediaCentral let studios in APAC countries collaborate across borders with international teams, aligning with the region’s growing content consumption and media output.

Apple (Logic Pro & GarageBand)

Apple’s Logic Pro (and free GarageBand) resonates strongly in APAC, notably Japan, India, South Korea, and Australia. Seamless integration with Apple hardware makes it ideal for creative professionals and educators there. Apple boosts its foothold by rolling out localized content packs and student licensing programs tailored to APAC, and by promoting iPad workflows that complement mobile-first production habits growing in the region.

Steinberg

Steinberg, the force behind Cubase and Nuendo, has steadily expanded in APAC. Innovations like Cubasis mobile DAW and robust VST ecosystem draw users across Southeast Asia and greater China. Through local reseller networks and integration with Yamaha gear, they’ve anchored their presence in APAC’s profusion of music schools and game/audio post-production studios. Their audio standards, like VST and ASI,O remain core to regional DAW-compatible hardware adoption.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

- Subscription & Ecosystem Lock-in: Companies are threading software, cloud services, and hardware into subscription bundles, think Avid’s Media Composer integration or Apple’s continuity between iPad and Mac DAWs. This builds loyalty and recurring revenue.

- AI & Collaboration Tools: Leaders are embedding AI-assisted features like Adobe’s real-time audio cleanup or Logic’s Smart Tempo plus collaborative editing in the cloud. These tools speed up workflows and appeal to modern creators.

- Hardware-Software Synergy: Ableton’s Push controller, PreSonus’ interface lineup bundled with Studio One, and Steinberg’s Cubasis mobile all reflect the blend of tactile input hardware with DAW software for cohesive creative tools.

- Community & Education Engagement: Whether it's Ableton’s Certified Trainer programs, Apple’s educational discounts, or Steinberg’s regional tutorials, investing in communities strengthens grassroots orientation and future adoption.

- Acquisitions & Platform Growth: Some players grow through strategic buys like BandLab’s acquisition of Cakewalk and ReverbNation expanding from DAW into full-funnel creator tools and distribution platforms.

COMPETITIVE LANDSCAPE

The DAW market brims with dynamic rivalry, shaped by both legacy powerhouses and agile innovators. Avid, Apple, and Steinberg lead with entrenched platforms like Pro Tools, Logic, and Cubase/Nuendo, rooted in professional workflows and deep technical features. Meanwhile, companies like Ableton and Image-Line stir disruption with performance-centric, intuitive tools. Underneath, robust ecosystems, VST standards, integration, AI, mobile portability, and cloud-linked projects define competition. Today's DAW battle is less about brute market share and more about flexible, creative, and collaborative experiences. As creators span sketch studios to pro labs, firms offering seamless cross-device performance, smarter tools, and supportive communities are winning ground. In this environment, innovation, accessibility, and ecosystem connectivity shape who stays on top.

RECENT MARKET DEVELOPMENTS

- In May 2024, Apple unveiled Logic Pro for iPad 2 plus Logic Pro for Mac 11, both enhanced with AI-powered studio assistant tools to elevate songwriting, beat-making, production, and mixing workflows in the DAW realm.

- In July 2017, Ableton acquired Cycling ‘74, the creators of Max/MSP, setting the stage for deep integration via Max for Live and unlocking customizable sound-design capabilities within Live’s DAW environment.

- In November 2021, PreSonus formalized its status under Fender by joining the iconic music brand, enabling tighter integration between Studio One DAW software and Fender’s hardware platforms.

- In November 2021, BandLab Technologies acquired ReverbNation, weaving artist services such as distribution and promotion into its BandLab cloud DAW ecosystem, expanding beyond mere production tools.

- In February 2023, BandLab added the beat marketplace Airbit to its portfolio, amplifying its platform’s appeal by integrating access to third-party beats directly within its cloud-based DAW experience.

MARKET SEGMENTATION

This research report on the global digital audio workstation market has been segmented and sub-segmented based on the type, end-use, component, deployment mode, operating system, and region.

By Component

- Software

- Services

By Operating System

- Mac OS

- Windows

- Linux

By Deployment Mode

- Cloud

- Local

By Type

- Recording

- Editing

- Mixing

By End Use

- Non-Commercial

- Commercial

By Region

- North America

- Europe

- The Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

How do cloud-based digital audio workstations differ from traditional DAW software?

Cloud-based digital audio workstations offer the advantage of accessibility from any device with an internet connection, collaborative features for remote work, and automatic updates without the need for manual installations. However, they may require a stable internet connection for optimal performance.

Are there any regulatory factors impacting the digital audio workstation market?

Regulatory factors such as copyright laws, data protection regulations, and licensing agreements for audio samples and plugins can influence the digital audio workstation market, particularly concerning the legal use of copyrighted material and compliance with industry standards.

How does the emergence of AI and machine learning technologies affect the digital audio workstation market?

AI and machine learning technologies are increasingly being integrated into digital audio workstations to automate tasks such as audio editing, mixing, and mastering. This can improve workflow efficiency and enhance the creative capabilities of users by providing intelligent suggestions and automating repetitive processes.

How do educational institutions contribute to the growth of the digital audio workstation market?

Educational institutions play a crucial role in the growth of the digital audio workstation market by incorporating DAW software into music production and audio engineering curricula, thereby familiarizing students with industry-standard tools and preparing them for careers in the music and entertainment industry. Additionally, student discounts and educational licenses offered by DAW developers encourage adoption among aspiring musicians and producers.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com