Global Duplex Stainless Steel Market Size, Share, Trends & Growth Forecast Report - Segmentation By Grade (Super Duplex, Lean Duplex, Duplex), Product (Pumps & Valves, Fittings & Flanges, Tubes, Welding Wires), End-Use (Chemical, Oil & Gas, Desalination, Pulp & Paper), and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis From 2026 to 2034

Global Duplex Stainless Steel Market Report Summary

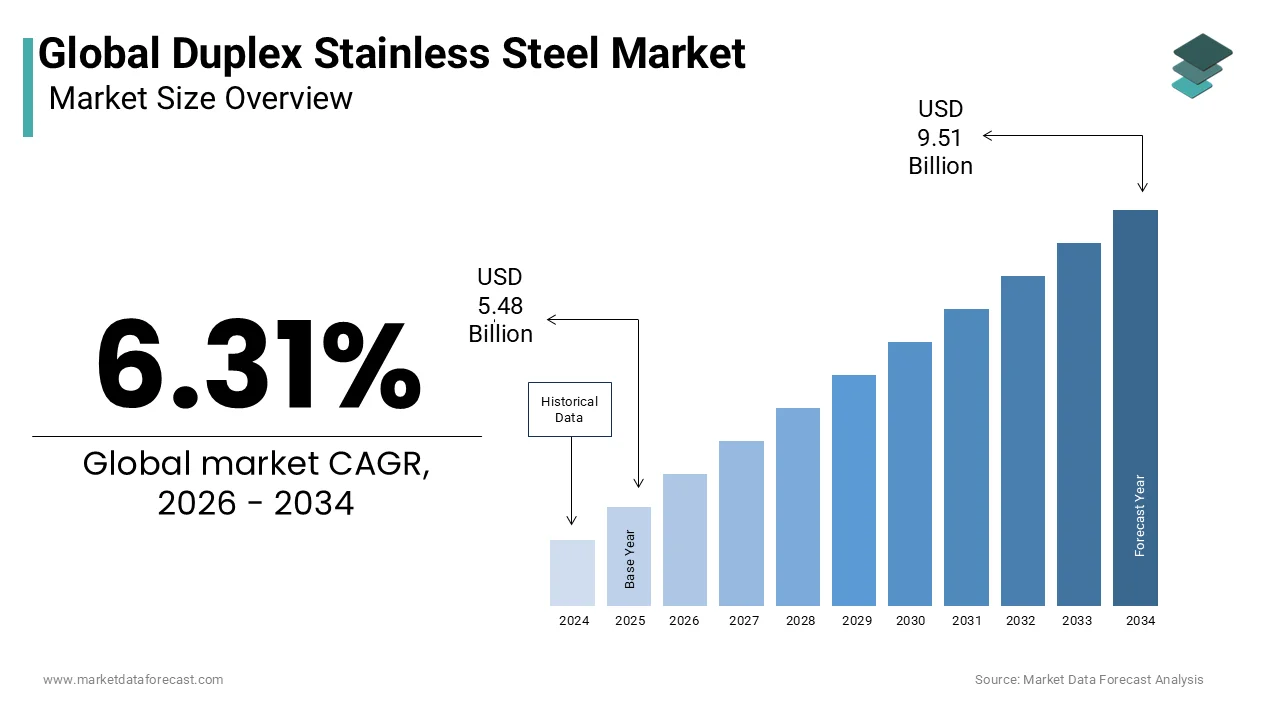

The global duplex stainless steel market was valued at USD 5.48 billion in 2025, is estimated to reach USD 5.83 billion in 2026, and is projected to reach USD 9.51 billion by 2034, growing at a CAGR of 6.31% during the forecast period. Market growth is driven by increasing demand for high strength and corrosion resistant materials across industrial applications. Duplex stainless steel is widely used due to its superior mechanical properties, durability, and resistance to harsh environments, making it ideal for oil and gas, chemical processing, and marine industries. The expansion of infrastructure, energy projects, and industrial manufacturing is further supporting steady global market growth.

Key Market Trends

- Rising demand for corrosion resistant and high strength materials is driving market growth.

- Increasing investments in oil and gas and energy infrastructure are boosting demand.

- Growing use in chemical processing and marine applications is supporting market expansion.

- Expansion of industrial manufacturing and construction sectors is enhancing market growth.

- Technological advancements in steel production are improving product performance and efficiency.

Segmental Insights

- Based on grade, the standard segment was the largest and held 55.4% of the global duplex stainless steel market share in 2025. This dominance is attributed to its balanced properties, cost effectiveness, and wide applicability across industries.

- Based on product, the tubes and pipes segment accounted for 40.3% of the global duplex stainless steel market share in 2025. The segment’s growth is driven by extensive use in fluid transportation systems, particularly in oil and gas and chemical industries.

- Based on end use, the oil and gas sector dominated with 45.6% of the global duplex stainless steel market share in 2025, supported by high demand for durable and corrosion resistant materials in offshore and onshore operations.

Regional Insights

- The global duplex stainless steel market is experiencing strong growth across regions, supported by industrial expansion and infrastructure development.

- Asia Pacific was the largest contributor, accounting for 40.6% of the global duplex stainless steel market share in 2025, driven by rapid industrialization, expanding energy sector, and strong manufacturing base in countries such as China and India.

Competitive Landscape

The global duplex stainless steel market is highly competitive, with key players focusing on product innovation, capacity expansion, and strategic partnerships to strengthen their market position. Companies are investing in advanced metallurgy, sustainable production, and global supply chain optimization. Prominent players in the global duplex stainless steel market include Tata Steel, Jindal Steel, Nippon Yakin Kogyo Co Ltd, Daido Steel Co Ltd, POSCO Group, ThyssenKrupp AG, ArcelorMittal S A, Acerinox S A, Sandvik Materials Technology AB, Allegheny Technologies Incorporated, and others.

Global Duplex Stainless Steel Market Size

The global duplex stainless steel market size was valued at USD 5.48 billion in 2025 and is projected to reach USD 9.51 billion by 2034 from USD 5.83 billion in 2026, growing at a CAGR of 6.31%.

The duplex stainless steel is class of stainless steels characterized by a mixed microstructure of austenite and ferrite phases, which provides superior strength and corrosion resistance compared to standard austenitic grades. These materials are in industries requiring high durability under harsh conditions, such as oil and gas extraction chemical processing and marine engineering. The unique combination of mechanical properties allows for thinner wall thicknesses in piping and vessels leading to weight reduction and cost savings in large scale projects. As per the International Energy Agency, sglobal investment in energy infrastructure reached 2.8 trillion US dollars in recent years driving demand for robust materials capable of withstanding extreme pressures and corrosive environments. The transition towards offshore wind energy further amplifies the need for duplex stainless steel due to its exceptional resistance to chloride induced stress corrosion cracking. According to the World Steel Association, stainless steel production accounts for approximately 5% of total global steel output with duplex grades representing a high value segment within this category. The material's ability to maintain integrity in sour service conditions where hydrogen sulfide is present makes it indispensable for modern hydrocarbon exploration. Furthermore, environmental regulations mandating longer asset lifecycles and reduced maintenance frequencies favor the adoption of duplex stainless steel over carbon steel alternatives. Manufacturers focus on optimizing alloy compositions to balance performance and cost while addressing sustainability goals through recyclability.

MARKET DRIVERS

Expansion Of Offshore Oil And Gas Exploration Activities Drives Demand

The expansion of offshore oil and gas exploration activities due to the material's unparalleled resistance to corrosive marine environments is accelerating the growth of duplex stainless steel market. As per the International Energy Agency, offshore production accounts for nearly 30% of global crude oil output necessitating robust infrastructure capable of enduring high pressure and saline conditions. Duplex stainless steel offers twice the yield strength of standard austenitic stainless steels allowing for the construction of lighter and more cost effective pipelines and risers. According to the United States Energy Information Administration, capital expenditure in offshore drilling projects has increased significantly as companies seek to tap into deepwater reserves. The presence of hydrogen sulfide and carbon dioxide in these reservoirs creates sour service conditions that can rapidly degrade conventional materials. Duplex grades such as 2205 and 2507 provide essential protection against stress corrosion cracking and pitting ensuring operational safety and longevity. The trend towards floating production storage and offloading units further boosts demand as these structures require extensive piping systems made from high performance alloys. Regulatory bodies mandate strict safety standards for offshore installations prompting operators to choose materials with proven reliability. The ability of duplex stainless steel to withstand dynamic loads and fatigue also contributes to its preference in subsea applications.

Growing Infrastructure Investments In Chemical And Petrochemical Processing

The growing infrastructure investments in the chemical and petrochemical processing sectors by increasing the requirement for corrosion resistant equipment is additionally fuelling the growth of duplex stainless steel market. As per the American Chemistry Council, the global chemical industry continues to expand with new facilities being constructed in Asia and the Middle East to meet rising demand for plastics and specialty chemicals. These plants operate under aggressive conditions involving acids alkalis and high temperatures, which necessitate the use of durable materials. Duplex stainless steel is widely used in heat exchangers pressure vessels and storage tanks due to its excellent resistance to localized corrosion. According to the Organization of the Petroleum Exporting Countries, downstream investment in refining capacity is projected to grow substantially requiring extensive piping networks made from high grade alloys. The shift towards processing heavier and more sour crude oils increases the corrosivity of process streams further driving the adoption of duplex grades. Additionally, the pharmaceutical and food processing industries are increasingly adopting duplex stainless steel for its hygienic properties and ease of cleaning. Regulatory standards for product purity and safety mandate the use of materials that do not contaminate processes. The longevity of duplex stainless steel reduces maintenance downtime and replacement costs offering a favorable total cost of ownership. The continuous modernization of industrial facilities ensures a steady and growing demand for these versatile alloys.

MARKET RESTRAINTS

Volatility In Raw Material Prices Impacts Production Costs

The volatility in raw material prices, particularly nickel chromium and molybdenum by creating uncertainty in production costs and pricing strategies is limiting the growth of duplexstainless steel market. As per the London Metal Exchange, prices for nickel and molybdenum have experienced significant fluctuations due to supply chain disruptions and geopolitical tensions. These elements are critical components of duplex stainless steel alloys and their cost variability directly affect manufacturing margins. According to the research, commodity markets remain susceptible to external shocks making it difficult for producers to maintain stable pricing for end users. Sudden spikes in raw material costs can lead to project delays or cancellations as buyers hesitate to commit to contracts with uncertain final prices. Manufacturers often struggle to pass these increased costs onto customers who may switch to cheaper alternatives, such as carbon steel with coatings. The dependence on imported raw materials exposes producers to currency exchange rate risks further complicating financial planning. Small and medium sized enterprises are particularly vulnerable to these price swings as they lack the hedging capabilities of larger corporations. The unpredictability of input costs hinders long term investment in capacity expansion and research and development. Furthermore, the scarcity of high grade ore deposits adds to the supply risk. This economic instability forces manufacturers to operate with caution limiting their ability to capitalize on market opportunities.

Complex Manufacturing Processes And Technical Barriers Limit Accessibility

The complex manufacturing processes and technical barriers by limiting the number of qualified suppliers and increasing entry costs, which is declining the growth of duplex stainless steel market. The precise control of cooling rates and heat treatment is essential to achieve the desired austenite ferrite balance and prevent the formation of harmful intermetallic phases. This requires sophisticated equipment and highly skilled personnel, which raises the barrier to entry for new players. According to the International Stainless Steel Forum, only a limited number of mills worldwide possess the capability to produce high quality duplex grades consistently. The welding of duplex stainless steel also demands strict adherence to procedures to avoid loss of corrosion resistance and mechanical properties. Incorrect handling can lead to premature failure in service resulting in costly repairs and liability issues. The need for specialized testing and certification further adds to the production timeline and expense. Customers often require extensive qualification processes before approving new suppliers which slows down market penetration. The technical complexity also limits the availability of standard stock items forcing buyers to place custom orders with longer lead times. This lack of flexibility can deter potential users who prefer readily available materials.

MARKET OPPORTUNITIES

Adoption In Renewable Energy Infrastructure Especially Offshore Wind

The growing demand with the adoption of renewable energy infrastructure, particularly offshore wind farms is to act as a major opportunity for the expansion of duplex stainless steel market. The offshore wind capacity is expected to increase significantly in the coming decade driven by government targets for carbon neutrality. These installations are exposed to harsh marine environments where salt spray and humidity cause rapid corrosion of standard materials. Duplex stainless steel offers superior resistance to chloride induced stress corrosion cracking making it ideal for turbine components substations and connection cables. According to the International Renewable Energy Agency, investment in offshore wind technology is accelerating with major projects planned in Europe Asia and North America. The use of duplex grades in critical structural parts enhances the reliability and lifespan of wind turbines reducing maintenance costs over their operational life. The trend towards larger and more powerful turbines requires materials that can withstand higher mechanical stresses without adding excessive weight. Duplex stainless steel's high strength to weight ratio meets this requirement effectively. Furthermore, the sustainability profile of stainless steel aligns with the environmental goals of the renewable energy sector. Its recyclability and durability contribute to a lower overall carbon footprint for wind energy projects. Manufacturers can capitalize on this trend by developing specialized grades optimized for wind energy applications.

Expansion In Desalination Plants To Address Water Scarcity

The expansion of desalination plants to address global water scarcity due to the material's exceptional resistance to seawater corrosion is also to leverage the growth of duplex stainless steel market. As per the United Nations Water Conference, the demand for fresh water is rising rapidly with desalination becoming a key solution for arid regions. Desalination processes involve handling highly saline water at elevated temperatures and pressures, which aggressively corrode conventional materials. Duplex stainless steel is widely used in heat exchangers pipes and pumps within desalination facilities due to its ability to withstand these harsh conditions. The shift towards reverse osmosis and thermal desalination technologies increases the need for durable materials that ensure continuous operation. Duplex grades reduce the risk of leakage and contamination ensuring the quality of produced water. The long service life of duplex stainless steel lowers the total cost of ownership for plant operators by minimizing replacement and repair frequency. Government initiatives to improve water security are driving investment in large scale desalination infrastructure. This creates a consistent demand for high performance alloys. Manufacturers can target this sector by offering tailored solutions that meet specific project requirements.

MARKET CHALLENGES

Competition From Alternative Materials And Coatings

The competition from alternative materials and advanced coatings by offering potentially lower cost solutions for corrosion protection is one of the major challenges for the growth of duplex stainless steel market. As per the National Association of Corrosion Engineers, the development of high performance polymer coatings and lined carbon steel pipes has improved their durability and cost effectiveness. These alternatives are often perceived as more economical for applications where the extreme strength of duplex stainless steel is not strictly necessary. According to the Society for Protective Coatings, advancements in coating technology have extended the service life of carbon steel structures reducing the incentive to switch to expensive alloys. In some cases, clad materials which combine a thin layer of stainless steel with a carbon steel base offer a compromise between performance and cost. This competition is particularly intense in the oil and gas sector where cost optimization is a priority. Project engineers may opt for coated carbon steel if initial capital expenditure is a deciding factor. The perception that coatings require less upfront investment can hinder the adoption of solid duplex stainless steel. Additionally the availability of super austenitic stainless steels provides another alternative with comparable corrosion resistance in certain environments. Manufacturers must continuously demonstrate the long term value and reliability of duplex grades to overcome these competitive pressures. Educating customers about the lifecycle costs and risks associated with coatings is essential.

Supply Chain Disruptions And Logistical Bottlenecks

The supply chain disruptions are affecting the timely delivery of raw materials and finished products, which is a also to decline the growth of duplex stainless steel market. As per the World Trade Organization, global supply chains have faced unprecedented challenges due to geopolitical conflicts pandemics and port congestions. These disruptions lead to delays in the procurement of critical alloying elements such as nickel and molybdenum, which are essential for duplex stainless steel production. According to the study, freight rates and shipping times have remained volatile impacting the cost and availability of imported materials. Manufacturers often face difficulties in meeting delivery deadlines for large scale projects resulting in penalties and strained customer relationships. The reliance on specific geographic regions for raw material sourcing increases vulnerability to local disruptions. For instance, export restrictions or trade tariffs can suddenly limit access to key inputs. The just in time inventory models adopted by many industries leave little buffer for such delays. This uncertainty forces companies to hold higher inventory levels tying up capital and increasing storage costs. Furthermore, the transportation of heavy steel products requires specialized logistics which can be constrained during peak demand periods. The lack of visibility in the supply chain complicates planning and risk management. Addressing these logistical challenges requires diversification of suppliers and investment in resilient distribution networks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.31% |

| Segments Covered | By Grade, Product, End-use, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa. |

| Market Leaders Profiled | Tata Steel (India), Jindal Steel (India), Nippon Yakin Kogyo Co Ltd. (Japan), Daido Steel Co., Ltd. (Japan), POSCO Group (South Korea), ThyssenKrupp AG (Germany), ArcelorMittal S.A. (Luxembourg), Acerinox S.A. (Spain), Sandvik Materials Technology AB (Sweden) and Allegheny Technologies Incorporated (U.S.), and Others. |

SEGMENTAL ANALYSIS

By Grade Insights

The standard segment was accounted in holding 55.4% of the duplex stainless steel market share in 2025 with its optimal balance between cost and performance making it the preferred choice for a wide range of industrial applications. As per the International Stainless Steel Forum, standard grades such as 2205 offer twice the yield strength of austenitic stainless steels while maintaining excellent corrosion resistance at a lower alloy content than super duplex grades. This cost efficiency is crucial for large scale projects in the oil and gas and chemical processing industries, where material costs significantly impact overall budget. According to the research, the widespread adoption of standard duplex in upstream and midstream infrastructure is due to its ability to withstand moderate corrosive environments without the premium price of higher alloyed variants. The availability of standard duplex from numerous manufacturers globally ensures a stable supply chain and competitive pricing. Engineers frequently specify this grade for pressure vessels heat exchangers and piping systems where the operating conditions do not require the extreme resistance of super duplex. The established design codes and extensive field experience with standard duplex further reinforce its market leadership. Manufacturers benefit from economies of scale in producing this grade which allows for consistent quality and reduced lead times.

The super segment is expected to register a fastest CAGR of 6.8% from 2026 to 20234 with the increasing demand for materials capable of withstanding extreme corrosion in deepwater oil and gas exploration. As per the International Energy Agency, offshore drilling activities are moving into deeper and more aggressive environments where hydrogen sulfide and high chloride levels pose severe threats to infrastructure integrity. Super duplex grades such as 2507 and Zeron 100 offer superior pitting and crevice corrosion resistance compared to standard duplex ensuring safety and reliability in these critical applications. The higher molybdenum and chromium content in super duplex provides enhanced protection against localized attack which is prevalent in sour service conditions. Regulatory standards for offshore safety mandate the use of high performance materials in critical components driving the specification of super duplex. The trend towards extended reach drilling and floating production systems further amplifies the need for lightweight yet strong materials.

By Product Insights

The tubes and pipes segment held 40.3% of the Duplex Stainless Steel Market share in 2025 with the role of duplex stainless steel tubes and pipes in transporting fluids in the oil and gas chemical and water treatment industries. As per the International Pipeline Conference, the global pipeline infrastructure is expanding to connect remote production sites with processing facilities and markets requiring durable and corrosion resistant materials. Duplex stainless steel pipes offer high strength allowing for thinner walls and reduced weight which lowers transportation and installation costs. According to the research, the use of duplex pipes in offshore platforms and subsea systems is preferred due to their resistance to seawater corrosion and stress cracking. The longevity of these pipes reduces the need for frequent replacements and maintenance ensuring continuous operation. The standardization of duplex pipe dimensions and specifications facilitates easy integration into existing systems. Major projects in the Middle East and Asia Pacific rely heavily on duplex pipes for their infrastructure development. The ability of duplex steel to handle high pressure and temperature conditions makes it indispensable for critical transport applications. Furthermore the welding and joining techniques for duplex pipes are well established ensuring reliable connections.

The fittings and flanges segment is swiftly growing at an anticipated CAGR of 7.2% from 2026 to 2034 owing to the increasing complexity of piping networks in industrial plants, which require numerous connections joints and transitions. As per the Engineering News Record, the construction of modern chemical and petrochemical facilities involves intricate piping layouts that necessitate a high ratio of fittings and flanges to straight pipes. Duplex stainless steel fittings and flanges ensure leak proof and corrosion resistant connections, which are for safety and operational efficiency. The standardized duplex fittings are essential for maintaining system integrity under high pressure and temperature conditions. The preference for duplex materials in retrofitting and upgrading existing plants also drives demand for compatible fittings. The ability to customize fittings for specific angles and configurations enhances their utility in complex designs. Furthermore, the growth of modular construction methods in industrial projects increases the use of pre-fabricated spools with integrated fittings. This trend accelerates the consumption of duplex fittings and flanges. The need for reliable connections in offshore and subsea applications further boosts this segment.

By End Use Insights

The oil and gas sector was the largest with 45.6% of the Duplex Stainless Steel Market share in 2025 owing to the extensive use of duplex stainless steel in upstream and midstream operations where corrosion resistance and high strength are important. As per the International Energy Agency, the global demand for energy continues to drive exploration and production activities in challenging environments such as offshore fields and sour gas reservoirs. Duplex stainless steel is essential for constructing pipelines risers and pressure vessels that can withstand high pressures and corrosive fluids. The material's durability reduces the risk of catastrophic failures ensuring operational safety and environmental protection. The expansion of liquefied natural gas facilities also contributes to demand as duplex steel is used in cryogenic applications. The long service life of duplex components lowers the total cost of ownership for oil and gas operators. Regulatory mandates for safety and environmental compliance further reinforce the use of high performance materials. The established supply chain and technical expertise in this sector support continued dominance.

The desalination sector is likely to register a fastest CAGR of 8.5% from 2026 to 2034 with the global water scarcity initiatives that are accelerating the construction of desalination plants worldwide. As per the United Nations Water Conference, the demand for fresh water is outpacing supply in many regions prompting governments to invest in large scale desalination infrastructure. Duplex stainless steel is critical for these plants due to its exceptional resistance to seawater corrosion and high strength. According to the survey, capacity of new desalination projects is increasing particularly in the Middle East North Africa and Australia. Reverse osmosis and thermal desalination technologies require materials that can handle high pressure and saline environments without degrading. Duplex stainless steel ensures the longevity and efficiency of pumps pipes and heat exchangers in these facilities. The shift towards sustainable water sources supports the expansion of desalination capacity. Regulatory frameworks promoting water security further drive investment in this sector. The reliability of duplex steel reduces maintenance costs and downtime enhancing the economic viability of desalination plants.

REGIONAL ANALYSIS

Asia Pacific Duplex Stainless Steel Market Analysis

Asia Pacific was the largest contributor in the duplex stainless steel market by holding 40.6% of the share in 2025 owing to the rapid industrialization and massive infrastructure development, particularly in China, India, and Southeast Asia. As per the study, the region is investing heavily in energy water and chemical infrastructure driving demand for high performance materials. China is the dominant producer and consumer of duplex stainless steel leveraging its vast manufacturing base and growing offshore oil and gas sector. According to the research, the chemical industry in Asia has expanded consistently supported by favorable government policies. The presence of major desalination projects in countries like Saudi Arabia's neighbors and Australia also contributes to demand. The growing middle class is driving consumption of packaged goods and automobiles, which rely on industrial infrastructure. Furthermore,, government initiatives to improve water security and energy independence are accelerating the adoption of duplex stainless steel. The availability of raw materials and skilled labor supports local production capabilities.

Middle East and Africa Duplex Stainless Steel Market Analysis

The Middle East And Africa was positioned second by holding 26.3% of the global Duplex Stainless Steel Market share in 2025 with the extensive oil and gas activities and significant investment in desalination infrastructure. As per the Organization of the Petroleum Exporting Countries, the region is a leading producer of crude oil and natural gas requiring robust materials for extraction and processing. Duplex stainless steel is widely used in offshore platforms pipelines and refineries due to its resistance to sour service conditions. Countries like Saudi Arabia and the United Arab Emirates are leaders in desalination technology relying on duplex stainless steel for high pressure systems. The region's harsh marine environment necessitates the use of corrosion resistant materials for coastal infrastructure. Government visions such as Saudi Vision 2030 are diversifying the economy including investments in industrial and tourism sectors that require durable materials.

North America Duplex Stainless Steel Market Analysis

North America Duplex Stainless Steel Market growth is esteemed to have a significant growth opportunities in coming years with the advanced technological capabilities and a mature oil and gas industry. The market status in North America is influenced by the shale gas revolution and offshore drilling activities in the Gulf of Mexico. As per the United States Energy Information Administration the production of oil and natural gas in the United States remains robust driving demand for duplex stainless steel in upstream and midstream infrastructure. The region is also a leader in chemical processing and pharmaceutical manufacturing which require high purity and corrosion resistant materials. According to the American Chemistry Council, the chemical industry in North America is expanding with new facilities being constructed along the Gulf Coast. The focus on infrastructure renewal and environmental compliance drives the replacement of aging pipes and vessels with duplex alternatives. The presence of major engineering firms and research institutions fosters innovation in material applications. Regulatory standards for safety and environmental protection are stringent encouraging the use of high-performance alloys. The established supply chain and technical expertise support market stability.

Europe Duplex Stainless Steel Market Analysis

Europe duplex stainless steel market growth is likely to grow with the stringent environmental regulations and a strong focus on sustainability and renewable energy. As per the European Commission, the European Green Deal is driving investment in offshore wind energy and green hydrogen production which utilize duplex stainless steel for critical components. Countries such as Norway the United Kingdom and Germany are leading in offshore wind farm development requiring corrosion resistant materials for subsea cables and turbines. The region has high levels of industrial activity in chemical and pharmaceutical sectors, which demand high quality stainless steel. The aging infrastructure in Europe requires regular maintenance and upgrades creating steady demand for replacement materials. The regulatory framework promotes the use of durable and recyclable materials aligning with the properties of duplex stainless steel. The presence of major stainless steel producers in Europe ensures a stable supply.

Latin America Duplex Stainless Steel Market Analysis

Latin America duplex stainless steel market growth is driven by the varying levels of industrial development and economic stability. In countries like Brazil and Mexico, the oil and gas sector is a major driver of demand for duplex stainless steel. As per the Economic Commission for Latin America and the Caribbean, offshore exploration activities in Brazil are expanding requiring robust materials for deepwater projects. The mining and chemical industries also contribute to demand although to a lesser extent. The infrastructure investment in the region is increasing focusing on water treatment and industrial facilities. The potential for growth in desalination projects in coastal areas exists but is currently limited by economic constraints. The reliance on imported materials affects market dynamics and pricing. Political and economic volatility can impact project timelines and investment decisions.

COMPETITIVE LANSCAPE

The competition in the Duplex Stainless Steel Market is characterized by the presence of established global manufacturers and specialized regional producers who compete on quality technology and service reliability. Leading corporations leverage their extensive distribution networks and economies of scale to dominate the market while niche players focus on custom alloys and specialized applications. The industry faces intense pressure to innovate due to stringent environmental regulations and the need for higher performance materials in harsh environments. This drives significant investment in research and development for new grades and processing techniques. Price competition is moderate as customers prioritize long term durability and safety over initial cost. Strategic alliances with engineering firms and project developers are common as companies seek to secure contracts for large scale infrastructure projects. The barrier to entry is high due to the capital intensive nature of steel production and the need for specialized metallurgical expertise.

Key Market Players

The major key players in the global duplex stainless steel market are

- Tata Steel

- Jindal Steel

- Nippon Yakin Kogyo Co Ltd.

- Daido Steel Co., Ltd.

- POSCO Group

- ThyssenKrupp AG

- ArcelorMittal S.A.

- Acerinox S.A.

- Sandvik Materials Technology AB

- Allegheny Technologies Incorporated

- Others

Top Players in the Market

- Outokumpu Oyj is a global leader in stainless steel production and plays a pivotal role in the Duplex Stainless Steel Market through its extensive portfolio of high performance alloys. The company provides a wide range of duplex grades including standard and super duplex for demanding applications in oil and gas chemical processing and marine engineering. Outokumpu focuses on sustainability by utilizing recycled materials and renewable energy in its production processes. Recent actions include expanding its service center network in North America and Asia to enhance customer proximity and supply chain efficiency. The corporation actively collaborates with end users to develop customized solutions that meet specific corrosion resistance requirements. Their commitment to circular economy principles enhances their corporate image and aligns with global environmental standards. This strategic approach ensures Outokumpu remains a preferred supplier for critical infrastructure projects worldwide.

- Acerinox S.A. is a major international stainless steel producer with a significant presence in the Duplex Stainless Steel Market through its diverse product offerings. The company manufactures high quality duplex stainless steel products catering to various industrial sectors including energy water treatment and construction. Acerinox emphasizes operational excellence and innovation to maintain its competitive edge. Recent initiatives include modernizing its production facilities in Europe and the United States to improve efficiency and product quality. The company has also strengthened its distribution channels to ensure timely delivery to global customers. Acerinox invests in sustainable practices such as reducing carbon emissions and optimizing resource usage. Their focus on customer centric solutions and technical support builds strong relationships with key industry players.

- Jindal Stainless Limited is a leading integrated stainless steel producer with a growing influence in the Duplex Stainless Steel Market particularly in the Asia Pacific region. The company offers a broad spectrum of duplex grades designed for harsh environments and high stress applications. Jindal Stainless focuses on capacity expansion and technological upgrades to meet rising domestic and international demand. Recent actions include commissioning new manufacturing lines and enhancing research capabilities to develop advanced alloy compositions. The company actively participates in large scale infrastructure projects providing specialized materials for oil and gas and desalination plants. Jindal Stainless prioritizes sustainability by implementing eco friendly production methods and waste reduction programs.

Top Strategies Used by the Key Market Participants

Key players in the Duplex Stainless Steel Market primarily focus on product innovation and geographic expansion to maintain competitive advantage. Companies invest heavily in research and development to create specialized alloys with enhanced corrosion resistance and mechanical properties for niche applications. Strategic partnerships with end users in oil and gas and chemical sectors help tailor solutions to specific operational needs. Expansion of production capacities in emerging markets allows manufacturers to capitalize on growing infrastructure demands. Sustainability initiatives such as recycling and energy efficient production are increasingly used to differentiate brands and comply with regulations. Vertical integration strategies ensure stable raw material supply and cost control.

MARKET SEGMENTATION

This research report on the global duplex stainless steel market has been segmented and sub-segmented based on grade, product, end-use, and region.

By Grade

- Super Duplex

- Lean Duplex

- Duplex

By Product

- Pumps & Valves

- Fittings & Flanges

- Tubes

- Welding Wires

By End-use

- Chemicals

- Oil & Gas

- Desalination

- Pulp and Paper

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1.What is the duplex stainless steel market?

The duplex stainless steel market covers the production and use of stainless steels with a mixed austenitic and ferritic microstructure offering high strength and corrosion resistance.

2.What are the key drivers of the duplex stainless steel market growth?

Market growth is driven by rising demand from oil and gas, chemical processing, desalination, and construction industries due to superior mechanical and corrosion properties.

3.What are the main grades of duplex stainless steel?

Common grades include standard duplex, lean duplex, and super duplex stainless steels used for different performance requirements.

4.How does duplex stainless steel differ from austenitic stainless steel?

Duplex stainless steel offers higher strength, better stress corrosion cracking resistance, and improved cost efficiency compared to austenitic stainless steel.

5.What are the major applications of duplex stainless steel?

Key applications include pipelines, pressure vessels, heat exchangers, storage tanks, bridges, and offshore structures.

6.What role does duplex stainless steel play in the oil and gas industry?

It is widely used for offshore platforms and pipelines due to its high resistance to corrosion and mechanical stress in harsh environments.

7.What industries are the largest consumers of duplex stainless steel?

Major end users include oil and gas, chemical processing, desalination, marine, construction, and power generation industries.

8.What regions dominate the global duplex stainless steel market?

Asia Pacific, Europe, and North America dominate the market due to industrial expansion and infrastructure development.

9.Who are the key players in the duplex stainless steel market?

Leading players include Outokumpu, Acerinox, Sandvik, ArcelorMittal, and Nippon Steel.

10.What challenges does the duplex stainless steel market face?

Challenges include high initial material costs, complex fabrication requirements, and limited awareness in some end use sectors.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com