Global Ethanol-Based Vehicle Market Size, Share, Trends, COVID-19 Impact and Growth Forecast Report, Segmented By Type (Trucks and cars), Fuel (Petrol and Diesel), By Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis From 2026 to 2034

Global Ethanol-Based Vehicle Market Size

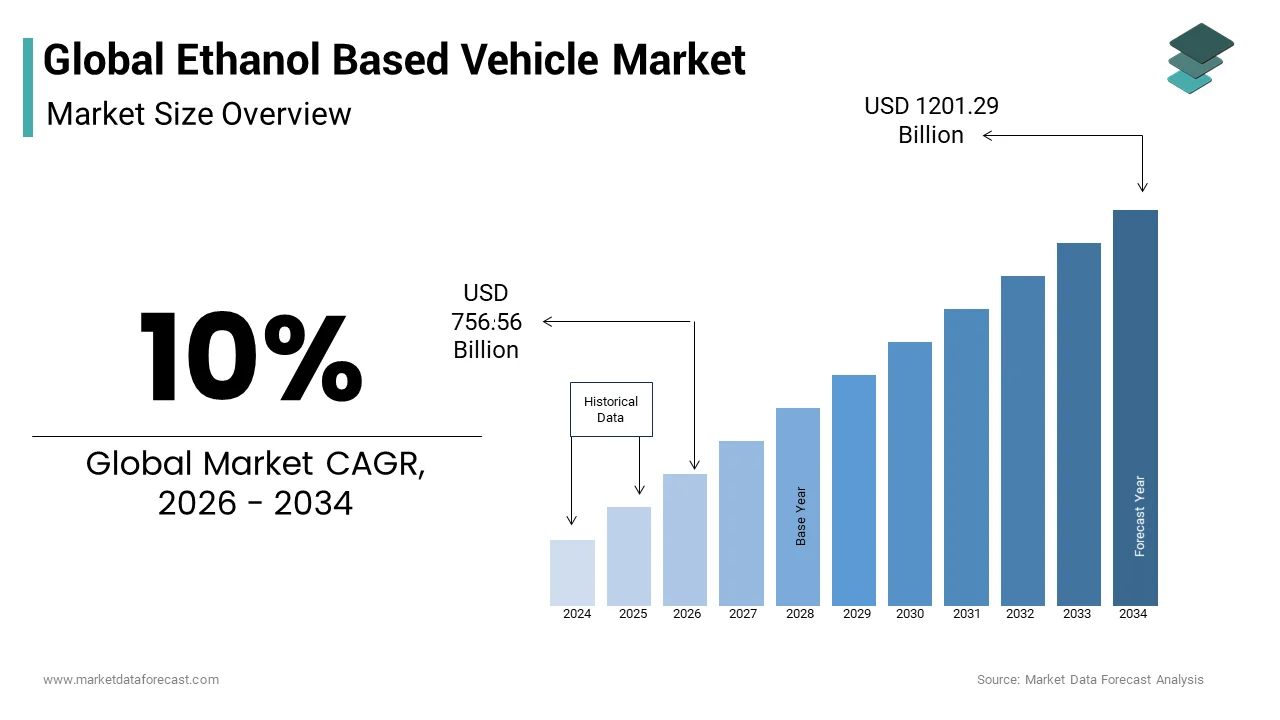

The global ethanol-based vehicle market size was valued at USD 714.07 billion in 2025 and is anticipated to reach USD 756.56 billion in 2026 to reach USD 1201.29 billion by 2034, growing at a CAGR of 10.0% during the forecast period from 2026 to 2034.

Ethanol-based vehicles are automobiles engineered to operate on ethanol fuel either in pure form or blended with gasoline. This sector represents a critical pivot in global transportation toward renewable energy sources aiming to mitigate greenhouse gas emissions and reduce dependency on fossil fuels. Ethanol serves as a high octane oxygenate that enhances combustion efficiency while lowering carbon monoxide and hydrocarbon outputs. The market dynamics are heavily influenced by agricultural policies fuel mandates and technological advancements in internal combustion engines capable of handling higher alcohol concentrations. As nations strive to meet stringent environmental targets the adoption of flex fuel vehicles has gained momentum particularly in regions with robust sugarcane or corn production capabilities. This synergy defines the current landscape where policy driven demand meets agricultural supply creating a distinct market ecosystem focused on sustainable mobility solutions without relying solely on electrification.

MARKET DRIVERS

Stringent Government Mandates and Carbon Reduction Targets Drive Adoption

Governments worldwide are implementing rigorous regulations to curb transportation-related emissions, which is one of the key factors driving the expansion of the ethanol-based vehicles market. The European Green Deal sets ambitious goals for climate neutrality by 2050, requiring member states to significantly reduce carbon footprints across all sectors including transport. As per the European Environment Agency, transport accounts for approximately 25% of total EU greenhouse gas emissions, necessitating immediate intervention through alternative fuels. Ethanol blends such as E10 and E85 offer a viable pathway to lower net carbon emissions because the carbon dioxide released during combustion is offset by the carbon absorbed during crop growth. Brazil serves as a pioneering example where the National Biofuels Policy mandates increasing ethanol content in gasoline to reduce reliance on imported oil and cut emissions. The Brazilian Ministry of Mines and Energy reported that ethanol usage prevented the emission of 650 million tons of carbon dioxide between 2003 and 2023. Similarly, the Renewable Fuel Standard in the United States requires billions of gallons of renewable fuel to be blended into transportation fuel annually. These regulatory frameworks create a guaranteed demand floor for ethanol producers and automakers alike. Manufacturers are compelled to produce flex fuel vehicles to comply with these standards, ensuring market availability. The legal imperative, combined with financial incentives such as tax credits for biofuel producers, creates a favorable economic environment. This regulatory pressure ensures that ethanol remains a cornerstone of national energy security strategies while addressing urgent climate concerns through measurable emission reductions.

Agricultural Surplus and Rural Economic Development Incentivize Production

The abundance of agricultural feedstocks such as corn, sugarcane, and wheat provides a robust foundation for ethanol production, linking rural economies with the automotive industry, which is further boosting the ethanol-based vehicles market growth. Farmers benefit from a stable demand source for their crops, which mitigates price volatility and ensures consistent income streams. In the United States, the corn belt states rely heavily on ethanol plants to absorb surplus grain production. According to the US Department of Agriculture, more than 5 billion bushels of corn were used for ethanol production in 2024, representing a significant portion of total harvest. This utilization stabilizes local markets and supports rural employment opportunities. In Brazil, the sugarcane industry employs over 1 million people directly and indirectly, as noted by the Brazilian Sugarcane Industry Association. The expansion of ethanol facilities stimulates infrastructure development in rural areas, including roads, storage, and logistics networks. Governments often provide subsidies to encourage farmers to grow energy crops, further strengthening this economic loop. The conversion of agricultural waste into second-generation ethanol also presents an opportunity to utilize residual biomass, enhancing overall resource efficiency. This symbiotic relationship between agriculture and energy sectors ensures a continuous supply chain for ethanol production. By transforming raw agricultural output into high-value fuel, nations can enhance their trade balance and reduce import dependence. The economic vitality provided to rural communities creates political support for ethanol mandates, ensuring long-term policy stability. This driver underscores the socioeconomic benefits of ethanol beyond environmental considerations, making it a politically resilient fuel option.

MARKET RESTRAINTS

Feedstock Price Volatility and Supply Chain Instability Restrain Growth

Fluctuations in the prices of key feedstocks such as corn and sugarcane introduce significant uncertainty into the ethanol production cost structure, which is significantly hampering the ethanol-based vehicles market expansion. Weather events, pest outbreaks, and geopolitical tensions can drastically alter crop yields, leading to unpredictable supply levels. For instance, severe droughts in major producing regions can reduce harvest volumes by 20% or more, as observed by the Food and Agriculture Organization during recent climate anomalies. When feedstock prices surge, ethanol producers face squeezed margins, which may lead to reduced output or higher consumer prices. This volatility discourages long-term investment in ethanol infrastructure as investors seek more predictable returns. Additionally, competition for land use between food and fuel crops raises ethical and economic concerns. High demand for ethanol can drive up global food prices, impacting food security in developing nations. The World Bank has highlighted instances where biofuel expansion contributed to food price spikes, causing social unrest in vulnerable regions. Such controversies can lead to policy reversals or reduced government support for ethanol programs. Furthermore, logistical challenges in transporting bulky agricultural materials to refineries add to operational costs. Infrastructure limitations in remote farming areas hinder efficient supply chain management. These factors collectively create a fragile economic model where external shocks can disrupt the entire value chain. Without effective hedging mechanisms or diversified feedstock sources, the market remains susceptible to abrupt changes. This inherent instability acts as a major restraint, preventing widespread and consistent adoption of ethanol-based vehicles globally.

Limited Energy Density and Infrastructure Compatibility Issues Hinder Expansion

Ethanol possesses a lower energy density compared to conventional gasoline, which results in reduced fuel economy and driving range for vehicles and further impeding the global market growth. Pure ethanol contains approximately 33% less energy per gallon than gasoline, as stated by the U.S. Department of Energy. This discrepancy means drivers must refuel more frequently, which can be inconvenient and costly despite potentially lower per-gallon prices. Flex-fuel vehicles adjust engine parameters to accommodate different blends but cannot fully compensate for the energy deficit. Consumers often perceive this reduced efficiency as a disadvantage, limiting mass-market appeal. Moreover, existing fueling infrastructure is not universally compatible with high ethanol blends. Many older pumps and storage tanks require upgrades to handle E85 due to ethanol's corrosive nature. The National Renewable Energy Laboratory indicates that only a fraction of retail stations in many countries offer E85, limiting accessibility for consumers. This lack of widespread availability creates range anxiety similar to early electric vehicle adoption hurdles. Retrofitting infrastructure requires substantial capital investment, which retailers are hesitant to undertake without guaranteed demand. Additionally, cold start issues in colder climates pose technical challenges for high ethanol blends, requiring additional engine heating systems. These technical and infrastructural barriers slow down consumer acceptance and market penetration. Until energy density improves or infrastructure becomes ubiquitous, ethanol vehicles will struggle to compete with the convenience and performance of traditional gasoline cars. This limitation restricts the market to specific regions with supportive policies and established infrastructure networks.

MARKET OPPORTUNITIES

Advancements in Second-Generation Ethanol Technology Create New Avenues

The development of second-generation ethanol produced from non-food biomass such as agricultural residues, wood chips, and municipal waste offers a sustainable growth path. This technology addresses food-versus-fuel concerns by utilizing waste materials that would otherwise be discarded or burned. According to the International Renewable Energy Agency, advanced biofuels could account for 20% of total biofuel production by 2030 if investment trends continue. Second-generation ethanol has a significantly lower carbon footprint than first-generation variants because it does not involve intensive farming practices. Several commercial plants have begun operations in Europe and North America, demonstrating technical feasibility. The European Commission supports research into cellulosic ethanol through funding programs aimed at achieving cost parity with fossil fuels. Innovations in enzymatic hydrolysis and fermentation processes are improving yield rates and reducing production costs. Companies are investing in integrated biorefineries that produce ethanol alongside other valuable chemicals, enhancing economic viability. This diversification reduces dependency on single feedstock sources and stabilizes supply chains. Policymakers are increasingly favoring advanced biofuels in renewable energy mandates, providing regulatory tailwinds. The potential to convert vast amounts of lignocellulosic biomass into fuel unlocks new resource pools globally. Forest residues alone could supply significant volumes of ethanol without impacting food security. As technology matures and scales up, production costs are expected to decline, making second-generation ethanol competitive. This evolution positions ethanol as a truly sustainable fuel option, aligning with circular economy principles and attracting environmentally conscious consumers and investors.

Integration with Hybrid Powertrains Enhances Efficiency and Appeal

Combining ethanol-fueled internal combustion engines with hybrid electric systems is another prominent opportunity for the global market. Hybrid vehicles optimize engine operation by using electric motors for low-speed driving and regenerative braking to recover energy. When paired with ethanol, the overall carbon intensity of the vehicle decreases significantly while maintaining long driving ranges. Toyota and other manufacturers are exploring flex-fuel hybrid models that leverage the high octane rating of ethanol to improve thermal efficiency. Studies by the Society of Automotive Engineers indicate that ethanol blends can improve engine efficiency by up to 10% when optimized for high compression ratios. This synergy allows hybrids to achieve superior fuel economy compared to gasoline-only counterparts. The dual powertrain approach mitigates the lower energy density of ethanol by ensuring the engine operates in its most efficient range. Consumers benefit from reduced fuel costs and lower emissions without sacrificing performance or convenience. Government incentives for low-emission vehicles often include hybrids, making them financially attractive. This combination extends the relevance of internal combustion technology in the transition to full electrification. It provides a bridge solution for markets where charging infrastructure is inadequate or electricity grids rely on fossil fuels. By enhancing the value proposition of ethanol through hybridization, automakers can attract a broader customer base. This strategic integration opens new market segments and prolongs the lifecycle of ethanol-based technologies in the evolving automotive landscape.

MARKET CHALLENGES

Inconsistent Global Policy Frameworks Impede Standardization and Trade

The lack of harmonized international regulations regarding ethanol blends and sustainability criteria creates fragmentation in the global market. Different countries adopt varying blend mandates ranging from E5 to E100, leading to compatibility issues for vehicle manufacturers. Automakers must design region-specific engines and fuel systems, increasing development costs and complexity. The absence of unified sustainability standards makes it difficult to verify the environmental benefits of ethanol across borders. Some nations prioritize corn-based ethanol while others favor sugarcane or cellulosic sources, leading to trade disputes and tariff barriers. The World Trade Organization has addressed several cases involving biofuel subsidies, highlighting the tension between domestic protectionism and free trade. Inconsistent carbon accounting methods further complicate cross-border transactions as buyers struggle to compare the true environmental impact of different ethanol sources. This regulatory uncertainty discourages multinational investment in production facilities and distribution networks. Investors prefer stable and predictable policy environments to commit capital for long-term projects. Without global alignment, the market remains fragmented, limiting economies of scale and technological diffusion. Developing nations may struggle to access advanced technologies due to proprietary restrictions and lack of standardized protocols. Harmonizing policies would facilitate smoother trade flows and accelerate technology transfer. However, political divergences and varying national interests make consensus challenging. This fragmentation acts as a significant challenge, preventing the ethanol market from realizing its full global potential and efficiency.

Public Perception and Misinformation about Food Security Risks

Negative public perception regarding the impact of ethanol production on food prices and land use is further challenging the global market expansion. Critics argue that diverting crops to fuel production exacerbates hunger and drives up food costs, especially in developing regions. Although studies show that multiple factors influence food prices, including energy costs and speculation, the narrative persists in media and public discourse. The Organisation for Economic Co-operation and Development notes that biofuels contributed modestly to food price increases, but the perception remains strong among consumers and policymakers. This skepticism influences voting behavior and policy decisions, leading to periodic reductions in support for ethanol programs. Environmental groups also raise concerns about indirect land use change where forests are cleared to replace cropland used for ethanol. Such allegations damage the green image of ethanol and undermine its credibility as a sustainable solution. Educating the public about advancements in second-generation ethanol and improved agricultural productivity is difficult amidst competing narratives. Social media amplifies misinformation, making it harder for industry stakeholders to convey accurate data. Trust deficits require transparent communication and third-party verification of sustainability claims. Without addressing these perceptual barriers, the market faces resistance from civil society and cautious regulators. Overcoming this challenge requires sustained engagement with stakeholders and demonstration of tangible benefits to both energy security and rural development. Until public confidence is restored, ethanol will face headwinds in expanding its market share globally.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 10.0% |

| Segments Covered | By Type, Fuel Type, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | AB Volvo, BMW AG, Daimler AG, Deere & Company, Ford Motor Company, General Motors Company, Honda Motor Co., Ltd., and Others. |

SEGMENTAL ANALYSIS

By Vehicle Insights

The cars segment led the market by capturing 71.7% of the global market share in 2025. The leading position of cars segment in the global market is attributed to the widespread availability of flex-fuel passenger vehicles, particularly in key markets like Brazil and the United States. Consumer preference for personal mobility solutions that offer flexibility in fuel choice drives this dominance. Automakers have prioritized car models equipped with engines capable of running on any blend of gasoline and ethanol up to E100. The extensive dealership network for passenger cars ensures easier access to maintenance and spare parts compared to commercial vehicles. Government incentives often target individual consumers through tax rebates for purchasing low-emission vehicles, which predominantly includes cars. The high volume of annual car sales globally amplifies the absolute number of ethanol-compatible units on the road. According to the International Organization of Motor Vehicle Manufacturers, global passenger car production exceeded 60 million units in 2023, with a significant portion supporting alternative fuels. The familiarity of drivers with car handling and the lower initial cost compared to trucks further bolster this segment. Urbanization trends also favor compact and mid-size cars that are increasingly available with ethanol capabilities. This broad consumer base ensures steady demand and continuous innovation in engine efficiency for passenger vehicles.

However, the trucks segment is a promising segment and is anticipated to register a CAGR of 9.2% during the forecast period in the global market owing to the stringent regulations targeting heavy-duty vehicle emissions and the need for decarbonizing logistics supply chains. Commercial fleet operators are increasingly adopting ethanol blends to meet corporate sustainability goals and reduce operational carbon footprints. The development of high-torque ethanol engines specifically designed for heavy loads has enhanced the viability of trucks in this sector. Governments in Europe and North America are implementing low-emission zones that penalize high-polluting diesel trucks, thereby encouraging a shift to cleaner alternatives. According to the European Automobile Manufacturers Association, heavy-duty vehicle emissions account for nearly 30% of road transport carbon dioxide output, necessitating urgent action. Ethanol offers a drop-in solution requiring minimal infrastructure changes for fleet refueling. The total cost of ownership for ethanol trucks is becoming competitive due to stable feedstock prices and improved fuel efficiency technologies. Logistics companies are piloting large-scale deployments of ethanol-powered trucks for last-mile delivery and long-haul transport. This strategic shift is supported by partnerships between truck manufacturers and biofuel producers, ensuring consistent supply. The momentum in green logistics initiatives globally propels this segment forward at a rapid pace.

By Fuel Insights

The petrol segment led the market by accounting for 54.5% of the global market share in 2025. The dominance of petrol segment in the global market can be credited to its inherent compatibility with existing internal combustion engine architectures. Most flex-fuel vehicles are originally designed as gasoline engines modified to accept ethanol blends, making petrol the primary base fuel. Consumers perceive petrol-ethanol blends as a seamless transition without compromising performance or requiring specialized maintenance. The vast existing infrastructure for gasoline distribution facilitates easy integration of ethanol blending at retail stations. Regulatory frameworks in major markets mandate ethanol blending into gasoline rather than diesel, which reinforces this dominance. According to the US Energy Information Administration, over 98% of gasoline sold in the United States contains ethanol, primarily in the form of E10. This widespread adoption creates a locked-in user base that continues to purchase petrol-based ethanol blends. The technical ease of blending ethanol with petrol compared to diesel reduces production costs for refiners. Petrol engines benefit from the high octane rating of ethanol, which allows for higher compression ratios and improved thermal efficiency. This performance advantage encourages automakers to optimize petrol engines for ethanol use. The established supply chain and consumer familiarity with petrol ensure its continued leadership in the market.

However, the diesel segment is emerging as the fastest growing category and is estimated to showcase a CAGR of 8.4% during the forecast period owing to the advancements in diesel-ethanol blend technology. Traditionally, ethanol and diesel do not mix well due to polarity differences, but new emulsification techniques and additive packages have enabled stable blends. Heavy-duty transport sectors, which rely heavily on diesel, are under intense pressure to reduce particulate matter and nitrogen oxide emissions. Ethanol-diesel blends offer a pathway to lower these pollutants while maintaining the high torque characteristics essential for commercial vehicles. The European Union has introduced stricter Euro 7 emission standards, prompting truck manufacturers to explore alternative fuel options including ethanol-diesel mixes. According to the International Council on Clean Transportation, advanced biofuels including ethanol-diesel blends can reduce lifecycle greenhouse gas emissions by up to 80% compared to fossil diesel. Fleet operators are conducting trials with B20 and higher ethanol blends to assess performance and durability. The availability of renewable diesel infrastructure in certain regions supports this transition. Technological breakthroughs in injection systems allow for precise control of ethanol-diesel combustion, improving efficiency. This niche but rapidly expanding segment addresses the specific needs of the commercial transport industry seeking sustainable solutions.

REGION ANALYSIS

North America Market Analysis

North America held a prominent position in the global ethanol-based vehicle market by accounting for 36.5% of the global market share in 2025. The region benefits from robust agricultural production, particularly corn in the United States, which serves as the primary feedstock for ethanol. The Renewable Fuel Standard mandates significant volumes of renewable fuel blending, creating a guaranteed demand for ethanol. Flex-fuel vehicles are widely available and accepted by consumers who appreciate the choice between gasoline and ethanol blends. According to the US Department of Energy, there are over 4,000 retail stations offering E85 across the country, facilitating consumer access. Canada is also expanding its ethanol usage through provincial mandates and federal clean fuel regulations. The established infrastructure and strong policy support make North America a mature market for ethanol vehicles. Technological innovations in engine efficiency continue to drive adoption in both passenger and commercial segments. The region leads in research and development for second-generation ethanol technologies, enhancing sustainability credentials. Trade agreements within the region facilitate the flow of ethanol and vehicles, strengthening market integration. Political support for domestic energy independence further reinforces the growth trajectory of ethanol-based vehicles in North America.

Europe Market Analysis

Europe accounted for a promising share of the global market in 2025. The leading position of Europe in the global market is primarily driven by aggressive climate policies and renewable energy targets. The European Union Green Deal aims for climate neutrality by 2050, requiring substantial reductions in transport emissions. Member states have implemented national biofuel mandates requiring increasing shares of renewable fuels in transportation. Ethanol is recognized as a key component in achieving these targets due to its proven technology and scalability. According to the European Commission, renewable energy in transport reached 10% in 2022, with ethanol contributing significantly to this figure. Countries like France, Germany, and Sweden are leaders in ethanol consumption and flex-fuel vehicle adoption. The ReFuelEU Aviation initiative also indirectly supports ground transport biofuel infrastructure development. European automakers are investing in flexible engine technologies that can handle various ethanol blends efficiently. Public awareness of environmental issues drives consumer preference for low-carbon fuel options. The region focuses heavily on sustainability criteria, ensuring that ethanol produced meets strict environmental standards. This regulatory rigor enhances the credibility of ethanol as a green fuel solution in Europe.

Asia Pacific Market Analysis

Asia Pacific is predicted to record the fastest CAGR in the global market during the forecast period owing to the diverse adoption levels across countries. India and Thailand are key drivers in this region with strong government support for ethanol blending programs. India aims to achieve 20% ethanol blending in gasoline by 2025 as part of its energy security strategy. The Indian Ministry of Petroleum and Natural Gas has accelerated the rollout of ethanol blending infrastructure across states. Thailand promotes gasohol blends extensively, with most petrol stations offering E10 and E20 options. According to the International Energy Agency, Asia Pacific biofuel demand is expected to grow significantly due to urbanization and rising vehicle ownership. China is also exploring ethanol expansion, though its focus remains heavily on electric vehicles. The region benefits from abundant sugarcane and cassava resources, which serve as feedstocks. Government subsidies and mandates are crucial in overcoming infrastructure challenges in rural areas. Consumer acceptance is growing as awareness of air pollution impacts increases. The diverse economic landscapes require tailored approaches for each country, but the overall trend points toward gradual expansion of ethanol vehicle usage.

Latin America Market Analysis

Latin America is estimated to account for a notable share of the global market during the forecast period, led primarily by Brazil, which is a global pioneer in ethanol technology. Brazil has a decades-long history of ethanol production and usage with a well-established infrastructure and consumer base. Nearly all new cars sold in Brazil are flex-fuel capable, allowing drivers to choose between gasoline and pure ethanol. According to the Brazilian Sugarcane Industry Association, ethanol accounted for over 45% of the light vehicle fuel matrix in recent years. The Proálcool program initiated in the 1970s laid the foundation for this success. Other countries in the region, such as Argentina and Colombia, are expanding their ethanol blending mandates. The abundance of sugarcane provides a cost-competitive feedstock advantage. Government policies prioritize energy independence and rural development through ethanol production. The region serves as a model for other nations seeking to implement successful ethanol programs. Technical expertise in ethanol engine optimization is highly developed in Latin America. This deep-rooted ecosystem ensures sustained leadership in the global ethanol vehicle landscape.

Middle East and Africa Market Analysis

The Middle East and Africa region holds a smaller share of the global ethanol-based vehicle market but shows emerging potential. South Africa is the primary driver in this region with ongoing discussions and pilot projects for ethanol blending. The African continent faces challenges related to infrastructure and feedstock availability but possesses significant agricultural resources. According to the African Development Bank, increasing local fuel production can enhance energy security and reduce import bills. Some countries are exploring sugarcane- and cassava-based ethanol production to leverage local agriculture. The Middle East is primarily focused on oil and gas, but diversification strategies include exploring biofuels for niche applications. Limited vehicle availability and lack of blending mandates restrict current market size. However, growing awareness of climate change and air quality issues is prompting policy reviews. International partnerships are helping to transfer technology and build capacity for ethanol production. The region represents a frontier market with long-term growth possibilities as infrastructure develops. Government interest in sustainable agriculture and energy diversification may accelerate adoption in the coming decade.

COMPETITIVE LANDSCAPE

The competition in the ethanol based vehicle market is characterized by intense rivalry among established automakers and emerging technology providers striving for dominance. Major manufacturers leverage their global scale and engineering prowess to offer diverse flex fuel options across vehicle segments. The market sees continuous innovation in engine efficiency and emission reduction technologies to comply with stringent environmental regulations. Strategic alliances between automakers and biofuel producers create integrated ecosystems that enhance supply chain stability. Regional players compete fiercely in local markets by tailoring products to specific regulatory and consumer preferences. Price competitiveness remains a key factor as consumers weigh the cost benefits of ethanol against traditional fuels. Intellectual property rights around advanced ethanol technologies drive patent filings and legal disputes. Market entry barriers are moderate due to the need for specialized engine calibration and infrastructure compatibility. Customer loyalty is influenced by brand reputation reliability and after sales service quality. The dynamic interplay of policy changes technological advancements and consumer behavior shapes the competitive landscape continuously.

KEY MARKET PLAYERS

Some of the market players dominate the global ethanol-based vehicle market.

- AB Volvo

- BMW AG

- Daimler AG

- Toyota Motor Corporation

- Volkswagen Group

- Deere & Company

- Ford Motor Company

- General Motors Company

- Honda Motor Co., Ltd

Top Players In The Market

- Toyota Motor Corporation stands as a pivotal player in the ethanol based vehicle market leveraging its extensive hybrid technology expertise. The company has developed advanced flex fuel hybrid systems that combine ethanol compatibility with electric propulsion for maximum efficiency. Toyota actively collaborates with governments and fuel providers to promote ethanol infrastructure development globally. Recent initiatives include launching new flex fuel models in key markets like Brazil and Southeast Asia. The company invests heavily in research to optimize engine performance for high ethanol blends. Toyota emphasizes the role of multi path solutions including ethanol in achieving carbon neutrality. Their commitment to sustainable mobility drives continuous innovation in fuel flexible powertrains. By integrating ethanol into their hybrid lineup Toyota addresses diverse regional fuel preferences. This strategic approach strengthens their global presence and appeals to environmentally conscious consumers. The company also participates in industry consortia to standardize ethanol technologies and best practices.

- Ford Motor Company maintains a strong foothold in the ethanol sector particularly in North America and South America. The brand has a long history of producing flex fuel vehicles and continues to expand its lineup with modern efficient engines. Ford works closely with agricultural stakeholders to support sustainable ethanol production practices. Recent actions include upgrading manufacturing facilities to produce more flex fuel capable trucks and SUVs. The company advocates for policies that support renewable fuel adoption and infrastructure investment. Ford integrates ethanol compatibility into its mainstream models ensuring broad consumer access. Their engineering teams focus on improving fuel economy and reducing emissions in ethanol powered vehicles. Ford also explores advanced biofuels including cellulosic ethanol for future applications. By championing flex fuel technology Ford reinforces its commitment to diverse energy solutions. This dedication helps maintain their competitive edge in markets with strong ethanol mandates.

- Volkswagen Group plays a significant role in the European ethanol market adapting its vehicle portfolio to meet regional regulatory requirements. The company produces flex fuel models tailored for markets like Brazil and Europe where ethanol blending is prevalent. Volkswagen invests in engine technologies that maximize efficiency with ethanol blends while minimizing emissions. Recent strategies include aligning product development with European renewable energy directives. The group collaborates with fuel suppliers to ensure quality and consistency of ethanol blends. Volkswagen promotes the environmental benefits of ethanol through marketing and consumer education campaigns. Their modular engine platforms allow for easy adaptation to different fuel types including ethanol. The company also supports research into second generation ethanol to enhance sustainability. By offering versatile vehicle options Volkswagen caters to varying consumer needs and regulatory landscapes. This flexibility strengthens their position in the evolving alternative fuel market.

Top Strategies Used By The Players In The Market

Key players in the ethanol based vehicle market employ strategies focused on technological innovation and strategic partnerships to strengthen their position. Companies invest heavily in research and development to create more efficient flex fuel engines that deliver better performance and lower emissions. Collaborations with agricultural firms ensure stable feedstock supplies and promote sustainable farming practices. Automakers also engage with governments to shape favorable policies and infrastructure development plans. Expanding production capacities for flex fuel vehicles allows companies to meet growing demand in key regions. Marketing efforts emphasize the environmental and economic benefits of ethanol to attract conscious consumers. Diversifying fuel options within vehicle portfolios provides flexibility and reduces dependency on single fuel sources. Investing in charging and refueling infrastructure partnerships enhances consumer convenience and adoption rates. Continuous improvement in supply chain logistics ensures cost effective delivery of ethanol compatible vehicles. These multifaceted strategies enable companies to navigate regulatory complexities and capture market share effectively.

MARKET SEGMENTATION

This research report on the global ethanol-based vehicle market is segmented and sub-segmented into the following categories.

By Type

- Trucks

- Cars

By Fuel Type

- Petrol

- Diesel

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

Why is the global ethanol-based vehicle market gaining attention as an alternative fuel solution?

The market is gaining attention due to increasing efforts to reduce carbon emissions, rising demand for renewable fuels, and government initiatives promoting sustainable transportation.

What are ethanol-based vehicles and how do they operate?

Ethanol-based vehicles are designed to run on ethanol-blended fuels or high-ethanol fuels, using modified engines and fuel systems that support cleaner combustion and reduced dependence on conventional gasoline.

How do ethanol-based vehicles contribute to environmental sustainability?

These vehicles help lower greenhouse gas emissions, reduce fossil fuel consumption, and support the use of renewable agricultural feedstocks in transportation.

Which vehicle segment is driving demand for ethanol-based vehicles globally?

Passenger vehicles account for the largest share due to their high production volumes and increasing adoption of alternative fuel technologies.

What factors are accelerating the adoption of ethanol-powered transportation?

Supportive government policies, abundant biofuel feedstock availability, rising fuel diversification strategies, and growing environmental awareness are accelerating adoption.

Which countries are leading the global ethanol-based vehicle market?

Brazil remains a leading market due to its extensive ethanol fuel infrastructure, while countries such as India, the United States, and several European nations are increasing ethanol fuel adoption.

How does ethanol fuel compare with conventional gasoline in transportation applications?

Ethanol fuel offers renewable sourcing, lower carbon emissions, and reduced reliance on imported petroleum, making it an attractive alternative fuel option.

What technological advancements are shaping the future of ethanol-based vehicles?

Flexible-fuel engine technologies, advanced fuel injection systems, hybrid biofuel powertrains, and improved combustion efficiency technologies are shaping the future of the market.

What challenges could impact the growth of the ethanol-based vehicle market?

Feedstock supply fluctuations, fuel infrastructure limitations, policy uncertainties, and competition from electric vehicles could impact market growth.

How are automakers responding to the growing demand for alternative fuel vehicles?

Manufacturers are developing flexible-fuel vehicles, enhancing engine compatibility, improving fuel efficiency, and expanding alternative fuel vehicle portfolios.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com