Europe Soybean Oil Market Size, Share, Trends, & Growth Forecast Report By End-Use (Food, Feed, Industrial) and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

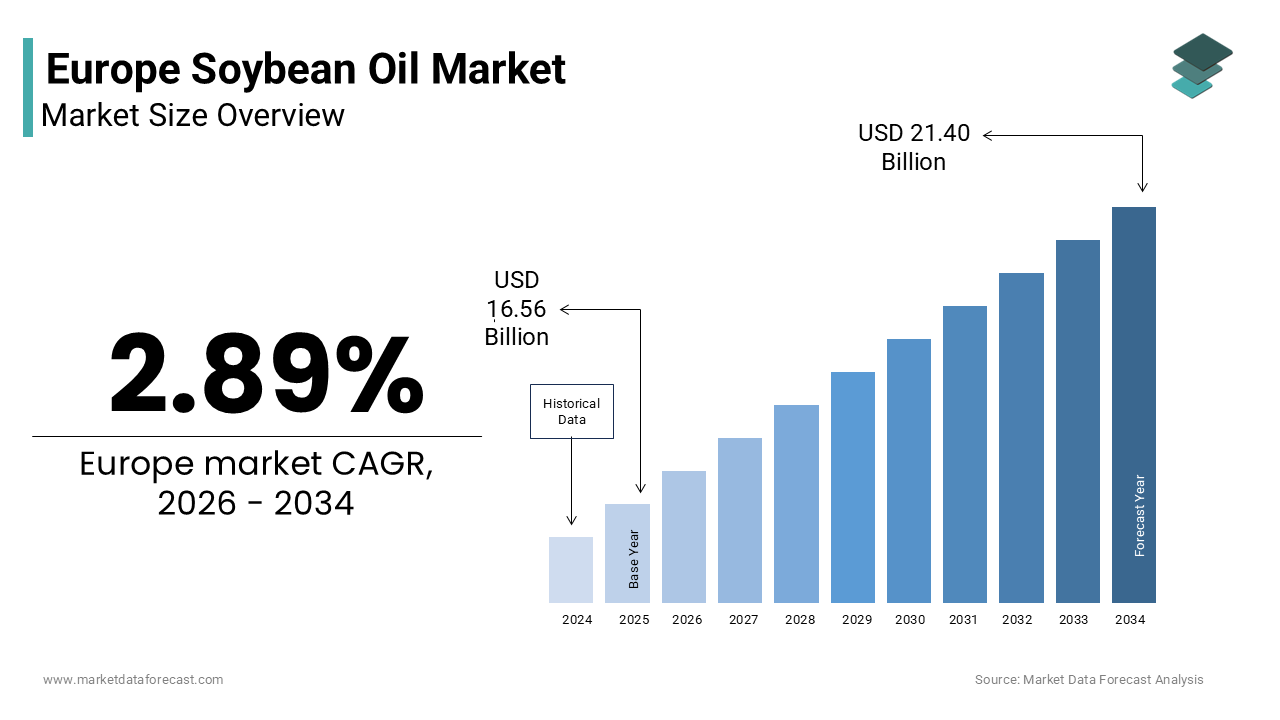

Market Size, 2025

$16.56 BnMarket Estimate, 2026

$17.04 BnMarket Forecast, 2034

$21.40 BnCAGR, 2026–2034

2.89%Europe Soybean Oil Market Report Summary

The Europe soybean oil market was valued at USD 16.56 billion in 2025, is estimated to reach USD 17.04 billion in 2026, and is projected to reach USD 21.40 billion by 2034, growing at a CAGR of 2.89% during the forecast period from 2026 to 2034. The growth of the Europe soybean oil market is driven by the expansion of the biodiesel industry, increasing demand from the food processing sector, and rising consumption in animal feed applications. The growing emphasis on renewable energy mandates, along with the shift towards sustainable and traceable supply chains, is further fueling market growth. Moreover, the rising demand for processed and convenience foods and the increasing adoption of bio-based industrial applications are expanding the utilization of soybean oil across Europe.

Key Market Trends

- Increasing use of soybean oil in biodiesel production is driven by renewable energy policies.

- Rising demand from the processed food and convenience food industry.

- Growing preference for non-GMO and high oleic soybean oil variants.

- Expansion of bio-based industrial applications such as lubricants and chemicals.

- Strong focus on sustainability, traceability, and deforestation-free supply chains.

Segmental Insights

- Based on end use, the feed segment was the largest and held a significant share of the Europe soybean oil market in 2025. The segment’s dominance is attributed to the high energy content of soybean oil, making it an essential ingredient in animal nutrition for improving growth rates and feed efficiency in livestock and aquaculture.

- Based on end use, the industrial segment is projected to witness the fastest growth during the forecast period. This growth is driven by the increasing adoption of soybean oil in bio-based lubricants, hydraulic fluids, and other environmentally friendly industrial applications aligned with sustainability goals.

Regional Insights

The Europe soybean oil market is witnessing steady growth across major countries, supported by strong demand from feed, food processing, and biodiesel industries.

- Germany was the largest contributor, accounting for 24.3% of the Europe soybean oil market share in 2025, driven by its strong livestock sector, leading biodiesel production, and advanced oilseed processing infrastructure.

- Spain continues to perform strongly, fueled by its large-scale animal farming industry, significant pork production, and growing biodiesel sector.

- The Netherlands remains a key hub due to its strategic port infrastructure, large-scale oilseed crushing facilities, and role as a major distribution center across Europe.

- France is witnessing steady growth supported by its diversified agricultural sector, increasing demand for non-GMO soybean oil, and expanding biodiesel production.

- Italy is also emerging as an important market driven by its strong food processing industry, animal husbandry sector, and growing demand for frying oils in industrial applications.

Competitive Landscape

The Europe soybean oil market is highly competitive, characterized by the presence of major global agribusiness companies with integrated supply chains and strong distribution networks. Leading players are focusing on sustainability compliance, traceability, and expansion of non-GMO product offerings to meet evolving consumer and regulatory demands. Investments in refining technologies, logistics optimization, and biofuel applications are further shaping the competitive landscape. Prominent players in the Europe soybean oil market include Cargill, Incorporated, Archer Daniels Midland Company, Bunge Limited, Louis Dreyfus Company, Wilmar International Ltd., Richardson International Limited, Viterra, and Arpadis Group.

Europe Soybean Oil Market Size

The Europe soybean oil market size was valued at USD 16.56 billion in 2025 and is anticipated to reach USD 17.04 billion in 2026 from USD 21.40 billion by 2034, growing at a CAGR of 2.89% during the forecast period from 2026 to 2034.

The soybean oil is refining, trade, and consumption of oil derived from Glycine max seeds, across the European continent, serving as a pivotal component in the food processing, animal feed, and emerging biofuel sectors. The oil is valued for its neutral flavor, high smoke point, and balanced fatty acid profile, which includes significant amounts of polyunsaturated fats. According to the European Commission, the European Union imported approximately 14.5 million metric tons of soybeans in the 2023-2024 marketing year, with the vast majority crushed domestically to produce oil and meal. As per data from Eurostat, the vegetable oil sector in Europe faces increasing scrutiny regarding deforestation, leading to stringent regulatory frameworks that dictate sourcing protocols. The region consumes over 3.8 million metric tons of soybean oil annually, with Germany, Spain, and the Netherlands acting as major crushing and distribution hubs. Consumer trends are shifting towards non-genetically modified organisms (non-GMO) and organic variants, forcing suppliers to adapt their supply chains. The market operates within a complex web of regulations including the Renewable Energy Directive, which influences the volume of oil diverted towards biodiesel production. This interplay between food security, environmental mandates, and industrial demand defines the current operational landscape of the European soybean oil industry.

MARKET DRIVERS

Expansion of the Biodiesel Industry Driven by Renewable Energy Mandates

The burgeoning biodiesel sector fueled by aggressive government targets to reduce carbon emissions in the transportation sector is majorly boosting the growth of Europe soybean oil market. The European Union's Renewable Energy Directive II mandates that member states achieve a 14% share of renewable energy in transport by 2030, creating a substantial pull for vegetable oil feedstocks. According to the European Biodiesel Board, biodiesel production in the EU reached 16.5 billion liters in 2024, with soybean oil accounting for an estimated 18% of the total feedstock mix due to its availability and favorable cold flow properties. This regulatory push has transformed soybean oil from a purely food commodity into a critical energy resource, with industrial consumption volumes rising year-on-year. Countries like Germany and France have implemented national subsidies that further incentivize the blending of soy-based biodiesel with fossil diesel, ensuring a steady offtake for crushers. The shift away from palm oil due to sustainability concerns has also redirected demand towards soybean oil, as it is perceived to have a lower deforestation risk when sourced from certified origins. As per the International Energy Agency, the transport sector in Europe is expected to increase its biofuel consumption by 25% over the next five years, securing a long-term growth trajectory for soybean oil. This structural demand from the energy sector provides a robust floor for prices and volumes, insulating the market from fluctuations in the food industry.

Surging Demand for Processed Foods and Convenience Meals

The relentless growth of the processed food industry and the consumer shift towards convenience meals serve for consumption is additionally leveraging the growth of Europe soybean oil market. Soybean oil is the preferred frying medium for many food manufacturers due to its high smoke point of 230 degrees Celsius, neutral taste, and cost-effectiveness compared to olive or sunflower oil. Data from FoodDrinkEurope indicates that the turnover of the European food and beverage industry exceeded 1.2 trillion euros in 2024, with the ready-to-eat meal segment growing at a rate of 6% annually. This expansion directly correlates with increased usage of soybean oil in the production of frozen foods, snacks, and bakery items where texture and shelf stability are paramount. The rise in urbanization and busy lifestyles has led to an increase in the sales of pre-cooked meals across major markets like the United Kingdom and Italy, according to NielsenIQ. Furthermore, the fast-food sector, which relies heavily on deep-frying operations, continues to expand, with major chains reporting an increase in outlet numbers across Eastern Europe. The functional properties of soybean oil, such as its ability to remain stable under repeated heating cycles, make it indispensable for large-scale industrial frying operations. As consumers continue to prioritize convenience without compromising on taste, the reliance on soybean oil as a key ingredient in the formulation of these products remains steadfast, driving consistent volume growth in the food processing segment.

MARKET RESTRAINTS

Stringent Deforestation Regulations and Supply Chain Compliance Costs

The implementation of rigorous deforestation-free supply chain regulations by imposing heavy compliance burdens on importers and processors is restricting the growth of Europe soybean oil market. The European Union Deforestation Regulation (EUDR), which entered into full force in 2023, prohibits the placement of commodities linked to forest destruction on the EU market, requiring extensive geolocation data and due diligence from suppliers. According to the European Commission, complying with these new rules is estimated to increase operational costs for importers, as they must invest in advanced traceability systems and audit their entire supply chain from farm to port. This regulatory hurdle has caused delays in shipments and led some traders to hesitate in sourcing soybeans from high-risk regions in South America, which supply major Europe's needs. As per the Federation of Oil, Seed and Fats Associations, the complexity of verifying land use history for millions of smallholder farms creates a bottleneck that restricts supply fluidity. Smaller market players often lack the financial resources to implement such sophisticated tracking mechanisms, potentially leading to market consolidation and reduced competition. The fear of non-compliance penalties, forces companies to adopt a cautious approach, sometimes resulting in reduced import volumes.

Intense Competition from Locally Produced Rapeseed and Sunflower Oils

The dominance of locally produced oilseeds, specifically rapeseed and sunflower is another attribute hampering the growth of Europe soybean oil market. The European Union is a global powerhouse in the production of rapeseed and sunflower seeds by offering a domestically sourced alternative that appeals to consumers and policymakers prioritizing food security and reduced carbon footprints. According to the European Oilseed Alliance, the EU produced over 9.5 million metric tons of rapeseed and 8.2 million metric tons of sunflower seeds in the 2024 harvest season, ensuring an abundant and often cheaper supply of local vegetable oils. This local abundance creates a price advantage for rapeseed and sunflower oils, which do not incur the same logistics costs and import tariffs associated with soybean oil from the Americas. Furthermore, the "Buy Local" sentiment among European consumers has strengthened, with many shoppers preferring products made with indigenous ingredients as per a survey by the European Consumer Organisation. The agricultural policies of the EU, which subsidize local oilseed farmers, further tilt the economic balance in favor of domestic oils. This intense competition limits the market penetration of soybean oil, confining it largely to specific industrial applications and biodiesel blending where local oils may not meet specific technical requirements or volume demands.

MARKET OPPORTUNITIES

Development of High Oleic and Non-GMO Specialty Variants

The formulation and commercialization of high oleic and non-genetically modified organism (non-GMO) soybean oil variants to capture premium products is also expected to impact positively on the growth of Europe soybean oil market. Consumers are increasingly health-conscious and awareness of genetically modified ingredients by creating a strong demand for cleaner and nutritionally superior oil options. High oleic soybean oil, which contains over 75% monounsaturated fats, offers enhanced oxidative stability and a healthier fatty acid profile comparable to olive oil, making it ideal for high-end food applications. Producers who can secure reliable supplies of identity-preserved non-GMO soybeans from certified sources in Europe or specific regions in the Americas can command significant price premiums. Data from Mintel indicates that product launches featuring "non-GMO" and "high oleic" claims on packaging increased in 2024, across the European food and beverage sector. This trend is particularly strong in the baby food, salad dressing, and premium snack categories where parents and health enthusiasts scrutinize ingredient lists. This strategic pivot allows the industry to tap into the growing wellness economy, transforming soybean oil from a low-margin commodity into a value-added health ingredient.

Utilization in Bio-Based Lubricants and Industrial Applications

The bio-based lubricants and industrial fluids are the European Green Deal and the push for a circular economy, which is likely to create new opportunities for the growth of Europe soybean oil market. Soybean oil possesses excellent lubricity and biodegradability by making it an ideal renewable feedstock for producing hydraulic fluids, metalworking fluids, and chain saw oils that replace petroleum-based counterparts. As per the European Bioplastics Association, the demand for bio-based industrial products in Europe is expected to rise annually as industries seek to reduce their environmental impact and comply with stricter emission standards. The chemical modification of soybean oil through epoxidation or transesterification allows it to meet the rigorous performance criteria required in heavy machinery and automotive applications. Government initiatives, such as the Horizon Europe program, are providing funding for research and development projects that explore new uses for vegetable oils in the industrial sector. As per study, just 5% of mineral lubricants with bio-based alternatives in the EU could consume an additional 500000 metric tons of vegetable oil. This shift is accelerated by corporate sustainability goals, where multinational manufacturers are committing to using renewable raw materials in their operations.

MARKET CHALLENGES

Volatility in Global Trade Policies and Geopolitical Instability

The volatility of global trade policies and geopolitical tensions that disrupt supply chains and inflate costs is one of the challenges for the growth of Europe soybean oil market. Since Europe imports the vast majority of its soybeans from Brazil, Argentina, and the United States, any diplomatic friction, trade war, or logistical blockade in these regions immediately impacts availability and pricing. According to the World Trade Organization, fluctuating tariff rates and export restrictions imposed by producing nations in response to global food security concerns have caused price swings, within single quarters in recent years. The ongoing geopolitical instability in Eastern Europe has also complicated logistics routes and increased shipping insurance costs, adding pressure to the landed price of soybean products. Furthermore, the reliance on a few key exporting countries creates a concentration risk, where a poor harvest or policy shift in one nation can send shockwaves through the entire European market. The uncertainty surrounding future trade agreements post-Brexit and evolving EU-Mercosur relations adds another layer of complexity by making long-term planning difficult for crushers and refiners. This inherent instability forces market participants to maintain costly hedging strategies and diverse supplier portfolios, yet the threat of sudden supply disruptions remains a constant challenge that undermines market predictability and investment confidence.

Negative Consumer Perception Regarding Genetic Modification and Health

Overcoming the entrenched negative consumer perception regarding genetic modification and the health implications of high omega-6 fatty acid contentis also acting as a barrier for the growth of Europe soybean oil market. Despite scientific consensus on the safety of approved GMO crops, a significant portion of the European public remains wary, associating soybean oil with unnatural processing and potential health risks. This sentiment is amplified by health advocacy groups that highlight the imbalance between omega-6 and omega-3 fatty acids in modern diets, incorrectly attributing various inflammatory conditions solely to soybean oil consumption. The European Food Safety Authority has struggled to effectively communicate the nuances of dietary fats to the public, leaving a vacuum filled by misinformation. As per data from the European Heart Network, misconceptions about vegetable oils have led to a 10% decline in household purchases of generic soybean oil in favor of perceived healthier alternatives like avocado or extra virgin olive oil. This reputational damage limits the market's ability to expand in the retail sector and forces manufacturers to invest heavily in labeling and marketing to reassure customers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.89% |

| Segments Covered | By End Use and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Cargill, Incorporated, Archer Daniels Midland Company, Bunge Limited, Louis Dreyfus Company, Wilmar International Ltd., Richardson International Limited, Viterra, and Arpadis Group |

SEGMENTAL ANALYSIS

By End Use Insights

The fed industry segment was accounted in holding 52.3% of the Europe soybean oil market share in 2025. The growth of the segment is driven by the indispensable requirement for high energy density in modern animal nutrition to ensure optimal growth rates and feed conversion ratios. Soybean oil provides approximately 9 kilocalories per gram, which is more than double the energy content of carbohydrates or proteins by making it the most efficient ingredient for boosting the caloric value of feed without increasing bulk. In these sectors, the inclusion of vegetable oils like soybean oil is standard practice to meet the specific metabolic needs of fast growing breeds. The economic pressure to reduce the time to market for livestock forces producers to maximize energy intake, and soybean oil offers a cost-effective solution compared to animal fats or other premium vegetable oils. This functional necessity ensures that the feed sector remains the largest consumer, driven by the fundamental biological requirements of intensive farming systems across the continent. The expanding aquaculture industry and the development of specialty feed formulations further escalate the dominance of the feed segment in the soybean oil market.

The Industrial applications segment is projected to witness a fastest CAGR of 6.8% from 2026 to 2034. The rapid adoption of bio-based lubricants and hydraulic fluids is driving the growth of the segment. Soybean oil possesses excellent lubricity, high flash points, and biodegradability, making it an ideal feedstock for producing environmentally friendly industrial fluids that minimize soil and water contamination. Industries such as construction, forestry, and marine operations are increasingly mandated to use biodegradable lubricants to prevent ecological damage in sensitive areas, leading to an increase in the procurement of soybean oil derivatives in 2024, as per data from the German Lubricants Association. The technical advancement in modifying soybean oil through epoxidation and transesterification has enhanced its stability and performance, allowing it to compete directly with synthetic mineral oils in heavy duty applications. Government incentives under the Horizon Europe program are funding research into new formulations, further accelerating commercialization.

REGIONAL ANALYSIS

Germany Soybean Oil Market Analysis

Germany was the top performer of the Europe soybean oil market by holding 24.3% of the Europe soybean oil market share in 2025. The growth of the segment is likely to grow with the fundamentally anchored in its powerful livestock industry and its leading role in biodiesel production. This immense volume requires vast quantities of energy rich ingredients, making soybean oil a critical component in ration formulations for the country's extensive pig and poultry sectors. Additionally, Germany is a pioneer in renewable energy, with the biodiesel sector consuming over 600000 metric tons of vegetable oils annually, as per data from the Union for the Promotion of Oil and Protein Plants. The country's strict adherence to the Renewable Energy Directive drives the blending of soybean oil into fuel, creating a dual demand stream from both agriculture and energy. Furthermore, the German food processing industry, which includes global giants in confectionery and ready meals, utilizes soybean oil for its functional properties in frying and baking. The presence of major crushing facilities in ports like Hamburg and Bremen ensures a steady supply of imported soybeans, which are processed domestically to capture value. The combination of industrial scale farming, aggressive green energy policies, and a robust food manufacturing base ensures Germany remains the undisputed leader in regional soybean oil consumption.

Spain Soybean Oil Market Analysis

Spain soybean oil market growth is likely to be driven by its status as a powerhouse in animal protein production and a key hub for vegetable oil refining. The growth is also being propelled by its position as the leading pork producer in the European Union and a major player in poultry farming. According to the Spanish Ministry of Agriculture, Fisheries and Food, Spain produced over 5.2 million metric tons of pork in 2024, requiring immense volumes of high energy feed to sustain such output. Soybean oil is extensively used in these feed formulations to optimize growth rates and meat quality, making the livestock sector the primary engine of demand. The country also hosts a significant biodiesel industry, with several large-scale plants dedicated to converting vegetable oils into renewable fuel, supported by national mandates that mirror EU directives. Furthermore, the Spanish food industry, famous for its fried snacks and canned fish products, utilizes soybean oil for its stability at high temperatures. The strategic location of Spanish ports facilitates efficient imports of soybeans from South America, reducing logistics costs for domestic crushers.

Netherlands Soybean Oil Market Analysis

The Netherlands soybean oil market growth is likely to have lucrative growth opportunities in coming years. This strategic advantage allows the Netherlands to host some of the world's largest oilseed crushing facilities, which process imported beans into oil and meal for both local use and distribution across the Rhine river basin. The Dutch livestock sector, particularly the intensive poultry and dairy industries, also contributes to domestic demand, consuming significant amounts of full fat soy products. The country's advanced chemical industry further utilizes soybean oil as a feedstock for bio-based products, aligning with the national circular economy goals. The presence of major multinational agribusinesses with European headquarters in the Netherlands fosters innovation in supply chain efficiency and sustainability certification. The combination of unparalleled logistics infrastructure, massive processing capacity, and a strong domestic agricultural base positions the Netherlands as an indispensable node in the European soybean oil value chain.

France Soybean Oil Market Analysis

France soybean oil market growth is to have steady opportunities in next coming years with a balanced demand from its diverse agricultural sector and a growing emphasis on non-GMO and sustainable sourcing. The country's substantial livestock industry, particularly in poultry and cattle farming, which relies on high quality feed to maintain production standards. France is also a significant producer of biodiesel, with government policies encouraging the use of vegetable oils to reduce carbon emissions in the transport sector. However, the French market is unique in its strong consumer resistance to genetically modified organisms, leading to a higher demand for identity-preserved non-GMO soybean oil compared to other European nations. This preference influences import patterns and pricing, with French crushers often sourcing from specific certified supply chains.

Italy Soybean Oil Market Analysis

Italy soybean oil market growth is likely to be driven by its robust animal husbandry sector, particularly in pig farming for cured meats, and a dynamic food processing industry. Italy is the renowned pig farming sector, which supplies the raw materials for iconic products like Parma ham and Prosciutto di San Daniele. These high-value supply chains require precise nutritional formulations to ensure meat quality, with soybean oil being a key energy source in feed rations. The Italian food industry, a global leader in pasta sauces, preserved vegetables, and fried snacks, also utilizes soybean oil for its neutral flavor and frying stability. While Italy produces significant amounts of olive oil, the volume is insufficient and too expensive for industrial frying and feed applications, creating a structural dependency on imported oils like soybean. The country's biodiesel sector is also expanding, supported by EU mandates, adding another layer of demand.

COMPETITIVE LANDSCAPE

The competition in the Europe soybean oil market is intense and characterized by the presence of large multinational agribusiness corporations that leverage their global scale and integrated supply chains to dominate the landscape. These giants compete fiercely on price efficiency and the ability to guarantee sustainable sourcing which has become a critical differentiator due to stringent European regulations. The market sees constant rivalry among top players to secure long-term contracts with major food processors and biodiesel producers who demand reliable volumes and specific quality standards. Smaller regional crushers struggle to compete unless they niche down into specialized segments like organic or non-GMO oils where they can command premium pricing. Innovation in logistics and traceability technology has become a battleground as companies strive to prove the origin and environmental impact of their products to regulators and consumers. The threat of substitution from locally produced rapeseed and sunflower oils adds another layer of competitive pressure forcing soybean oil suppliers to constantly justify their value proposition. Mergers and acquisitions are common as firms seek to consolidate assets and expand their geographic reach to better serve the diverse needs of the European countries.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Soybean Oil Market include

- Cargill, Incorporated

- Archer Daniels Midland Company

- Bunge Limited

- Louis Dreyfus Company

- Wilmar International Ltd.

- Richardson International Limited

- Viterra

- Arpadis Group

Top Players in the Europe Soybean Oil Market

Cargill

Cargill operates as a dominant force in the Europe soybean oil market through its extensive network of crushing facilities and refineries located in key ports like Rotterdam and Hamburg. The company contributes significantly to the global market by managing complex supply chains that connect South American farmers with European consumers while ensuring strict adherence to sustainability standards. Recently Cargill has strengthened its position by investing heavily in traceability technologies to comply with new European deforestation regulations. They have also expanded their production capacity for non-GMO soybean oil to meet the rising demand from health-conscious food manufacturers. Their commitment to regenerative agriculture programs helps secure long-term supply stability and enhances their reputation among environmentally aware stakeholders.

Bunge Limited

Bunge Limited is a major agribusiness player in the Europe soybean oil market known for its efficient logistics and large-scale processing capabilities across the continent. The company plays a crucial role in the global market by facilitating the trade of soybeans and derived oils while focusing on value-added products for the food and feed industries. To strengthen its market position Bunge has recently upgraded its refining plants in Spain and France to improve energy efficiency and reduce carbon emissions. They have also launched new initiatives to source certified sustainable soybeans exclusively from verified farms in Brazil and Argentina. These actions align with European Union mandates and appeal to customers seeking eco-friendly ingredients. Bunge continues to innovate in the biofuel sector by optimizing their production processes to create high-quality biodiesel feedstocks. Their strategic focus on operational excellence and sustainability ensures they remain a preferred partner for major European retailers and industrial users.

Louis Dreyfus Company

Louis Dreyfus Company stands as a key participant in the Europe soybean oil market leveraging its global trading expertise and robust infrastructure to deliver consistent supply to European clients. The company contributes to the global market by balancing supply and demand dynamics across continents and offering risk management solutions to farmers and buyers alike. Recent actions to strengthen their position include forming strategic partnerships with European feed manufacturers to secure long-term off-take agreements for soybean meal and oil. They have also invested in new storage facilities in Northern Europe to enhance logistical flexibility and reduce delivery times. Louis Dreyfus Company is actively developing specialized oil blends tailored for the growing industrial lubricants sector in Europe. Their dedication to digital transformation allows for real-time monitoring of cargo and inventory which improves overall supply chain reliability.

Top Strategies Used by Key Market Participants

Key players in the Europe soybean oil market primarily employ vertical integration strategies to control the supply chain from origination to final delivery ensuring consistent quality and volume. Companies are increasingly investing in sustainability certification programs to comply with strict European Union deforestation regulations and appeal to eco-conscious consumers. Another major strategy involves the expansion of non-GMO and organic product lines to capture premium market segments willing to pay higher prices for clean label ingredients. Participants are also focusing on technological advancements in crushing and refining processes to improve energy efficiency and reduce operational costs. Strategic alliances with local farmers and cooperatives help secure raw material supplies while promoting regenerative agricultural practices. Furthermore, key players are diversifying their product portfolios to include bio-based industrial applications such as lubricants and inks reducing reliance on traditional food and feed sectors. These combined approaches enable market leaders to navigate regulatory complexities and maintain competitiveness in a dynamic environment.

MARKET SEGMENTATION

This research report on the Europe Soybean Oil Market has been segmented and sub-segmented based on the following categories.

By End Use

- Food

- Feed

- Industrial

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are the primary uses of soybean oil in Europe?

Soybean oil is widely used in cooking, food processing, margarine production

What is the Europe Soybean Oil Market?

The Europe soybean oil market refers to the production, processing, distribution, and consumption of soybean oil used in food, industrial, and biofuel applications across European countries

Which countries are major contributors to the Europe Soybean Oil Market?

Germany, France, the Netherlands, Italy, and Spain are key contributors due to strong food processing industries.

What are the key types of soybean oil available in Europe?

Refined soybean oil, crude soybean oil, and organic soybean oil are commonly available types.

What role does soybean oil play in biodiesel production?

Soybean oil is used as a feedstock for biodiesel, contributing to renewable energy initiatives in Europe.

What role does soybean oil play in biodiesel production?

Soybean oil is rich in unsaturated fats and omega-3 fatty acids, making it a healthier option compared to some other cooking oils.

What challenges are faced by the Europe Soybean Oil Market?

Challenges include price volatility of soybeans, competition from alternative oils, and strict regulatory standards.

How do regulations impact the soybean oil market in Europe?

Strict food safety, labeling, and sustainability regulations influence production and trade practices.

How do regulations impact the soybean oil market in Europe?

Strict food safety, labeling, and sustainability regulations influence production and trade practices.

What is the impact of consumer preferences on the market?

Consumers are increasingly preferring non-GMO and organic soybean oil, influencing market trends.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com