- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

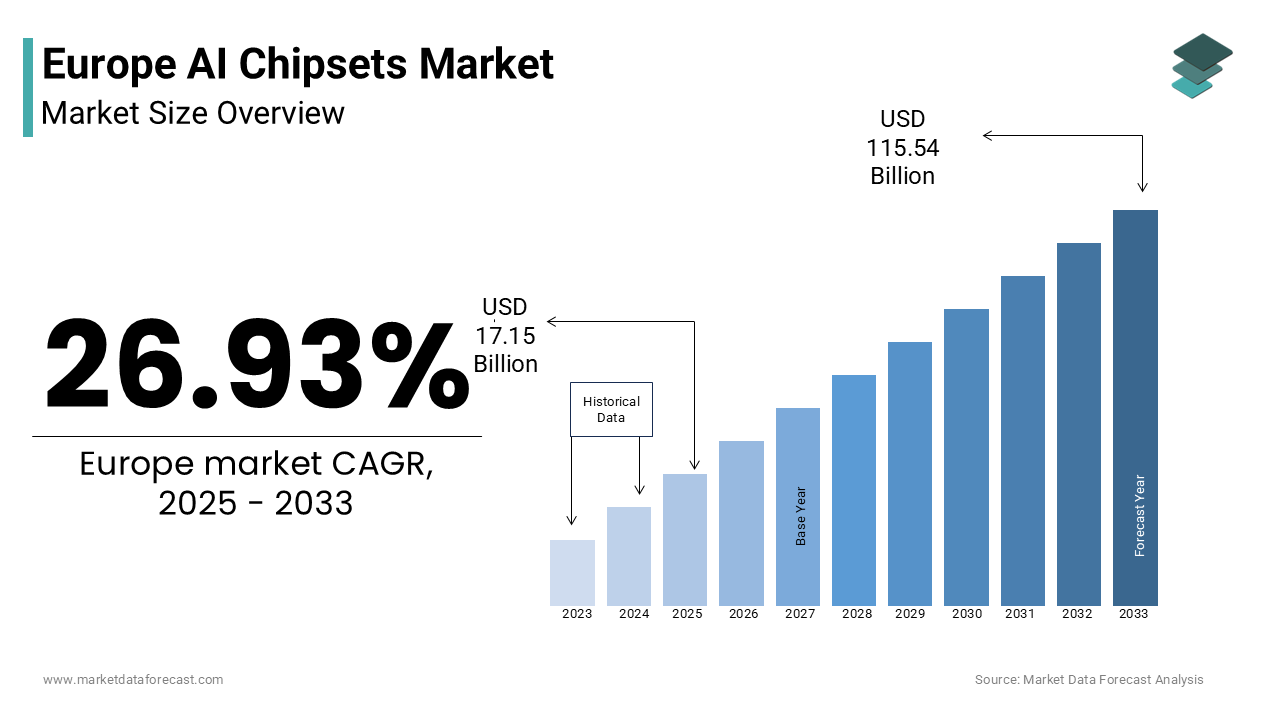

Market Size, 2025

$17.15 BnMarket Estimate, 2026

$21.77 BnMarket Forecast, 2034

$146.68 BnCAGR, 2026–2034

26.93%Europe AI Chipsets Market Report Summary

The Europe AI chipsets market was valued at USD 17.15 billion in 2025, is estimated to reach USD 21.77 billion in 2026, and is projected to reach USD 146.68 billion by 2034, growing at a CAGR of 26.93% during the forecast period from 2026 to 2034. The growth of the Europe AI chipsets market is driven by the accelerating adoption of artificial intelligence across data centers, industrial automation, healthcare, automotive systems, and public digital infrastructure. Strong regulatory momentum under the EU Artificial Intelligence Act is encouraging the deployment of transparent, energy-efficient, and secure AI hardware. Public investments under the EU Chips Act and Digital Europe Programme are strengthening semiconductor sovereignty and supporting domestic AI accelerator development. The rapid expansion of edge AI in smart factories, predictive maintenance, and real-time analytics is further boosting demand. Additionally, the establishment of national AI supercomputing hubs across Germany, France, Spain, and Finland is significantly increasing the adoption of high-performance AI training chipsets across Europe.

Key Market Trends

- Rising deployment of edge AI chipsets in industrial automation for real-time inspection, predictive maintenance, and robotics control.

- Growing investments in sovereign AI infrastructure under the EU Chips Act to reduce dependence on non-European semiconductor suppliers.

- Increasing demand for energy-efficient and explainable AI hardware is driven by regulatory requirements under the EU AI Act.

- Expansion of national AI supercomputing clusters for climate modeling, drug discovery, and scientific research across major European economies.

- Accelerating adoption of secure AI processors in public sector applications such as healthcare diagnostics, citizen services, and cybersecurity systems.

Segmental Insights

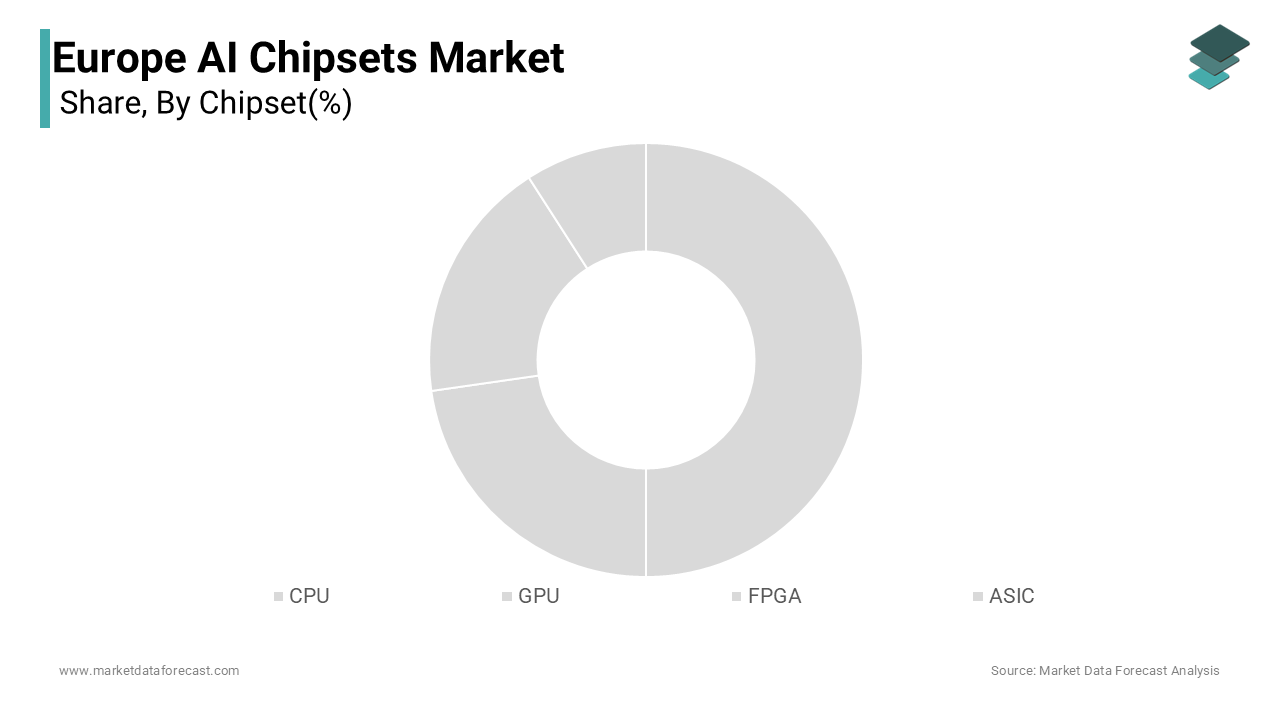

Based on the chipset, the GPU (Graphics Processing Unit) segment held the largest share of the Europe AI chipsets market in 2025, accounting for 42.3% of the total market, due to its widespread use in deep learning, neural network training, and high-performance computing applications across cloud data centers, research institutions, and enterprises.

Based on function, the inference segment was the largest and dominated the Europe AI chipsets market in 2025, driven by the extensive use of AI in real-time operational environments such as healthcare diagnostics, smart manufacturing, surveillance systems, and public sector services, where low latency and on-device processing are critica

Regional Insights

The Europe AI chipsets market is experiencing strong growth across major economies, supported by government-backed digital transformation strategies, advanced research ecosystems, and expanding industrial AI adoption.

- Germany was the largest contributor, accounting for 24.1% of the European AI chipsets market share in 2025, driven by its strong Industry 4.0 ecosystem, widespread deployment of AI in manufacturing, and large-scale investments in national AI infrastructure and semiconductor programs.

- France holds a significant position, supported by strategic investments in sovereign AI infrastructure, strong public sector AI adoption, and the presence of advanced semiconductor manufacturing capabilities through STMicroelectronics.

- The United Kingdom is witnessing the fastest growth, fueled by its strong AI startup ecosystem, leadership in AI chip design through companies like Graphcore, and increasing deployment of AI hardware across healthcare and financial services.

- The Netherlands and Sweden continue to emerge as important innovation hubs, supported by advanced semiconductor research, strong data center ecosystems, and a growing focus on ethical, secure, and energy-efficient AI systems.

Competitive Landscape

The Europe AI chipsets market is characterized by intense competition between global semiconductor leaders and emerging European AI hardware innovators. Major players are focusing on aligning their products with EU regulatory requirements related to transparency, energy efficiency, cybersecurity, and data sovereignty. Companies are increasingly investing in localized partnerships with governments, research institutions, and industrial players to strengthen their regional presence. Innovation in domain-specific accelerators for automotive, healthcare, and industrial applications is becoming a key competitive differentiator. Prominent players in the Europe AI chipsets market include NVIDIA Corporation, Intel Corporation, Advanced Micro Devices (AMD), IBM Corporation, Qualcomm Incorporated, Samsung Electronics Co., Ltd., Micron Technology Inc., Xilinx Inc., Graphcore, and Axelera AI.

Europe AI Chipsets Market Size

The Europe AI Chipsets Market was worth USD 17.15 billion in 2025. The Europe market is expected to reach USD 146.68 billion by 2034 from USD 21.77 billion in 2026, rising at a CAGR of 26.93% from 2026 to 2034.

Artificial intelligence chipsets are specialized semiconductor architectures, including graphics processing units tensor processing units and field programmable gate arrays engineered to accelerate machine learning inference and training workloads, across cloud edge and endpoint devices. Unlike general purpose processors these chipsets feature parallelized architectures high memory bandwidth and reduced precision computing capabilities tailored for neural network operations. Their deployment spans data centers autonomous vehicles medical diagnostics and smart manufacturing systems where low latency and energy efficiency are improtant. According to Eurostat the European Union installed over 14,000 new AI related patents in 2025 reflecting intensifying innovation in hardware enabled intelligence. The European High Performance Computing Joint Undertaking reported that seven EU member states now operate exascale ready supercomputers all integrating AI specific accelerators to support scientific modeling and public sector analytics. As per the European Commission’s 2023 AI strategy update all critical infrastructure projects funded under the Digital Europe Programme must incorporate AI ready computing hardware by 2026 reinforcing the strategic role of these chipsets in Europe’s technological sovereignty and digital transformation agenda.

MARKET DRIVERS

EU Regulatory Push for Trusted and Energy Efficient AI Spurs Hardware Innovation

The European Union’s Artificial Intelligence Act has demand for specialized AI chipsets that support transparent interpretable and energy efficient model execution, which is propelling the growth of Europe artificial intelligence chipset market. As the world’s first comprehensive AI regulatory framework, the law classifies high risk AI systems in healthcare transport and critical infrastructure requiring rigorous documentation of data lineage model behavior and power consumption. According to the European Commission, this regulatory scrutiny has driven manufacturers to adopt chipsets with built in explainability features and sub watt inference capabilities. In 2025, the Fraunhofer Institute demonstrated that AI accelerators with sparsity aware architectures reduced energy use by 62% in medical imaging applications compared to conventional GPUs meeting the EU’s Green AI benchmarks. Furthermore the European Environment Agency noted that data centers accounted for 2.7% of the EU’s total electricity demand in 2023 prompting national policies like France’s Low Carbon AI Initiative which offers tax credits for deploying chipsets under 15 watts per trillion operations. These regulatory and environmental imperatives are reshaping procurement criteria across public and private sectors favoring chipsets that balance performance with accountability and sustainability.

Expansion of Edge AI in Industrial Automation Drives Chipset Deployment

The integration of artificial intelligence at the industrial edge is specifically fuelling the growth of Europe artificial intelligence chipset market. As per the European Association of Automotive Suppliers, over 68% of new production lines installed in Germany Italy and Sweden since 2023 incorporate real time visual inspection systems powered by low power neural accelerators. These chipsets enable predictive maintenance defect detection and robot coordination without relying on cloud connectivity ensuring data sovereignty and millisecond level response times. The European Institute of Innovation and Technology reported that edge AI reduced unplanned downtime by 34% in pilot smart factories across the Rhine Alpine corridor. Additionally, the EU’s Chips Act allocated 3.3 billion euros in 2025 specifically for developing sovereign edge AI silicon with projects like the European Processor Initiative advancing RISC V based neural inference cores fabricated on 22 nanometer FD SOI processes at STMicroelectronics facilities in France. This emergence of industrial digitization policy support and localized semiconductor development is accelerating the adoption of purpose built AI chipsets beyond data centers and into the physical economy.

MARKET RESTRAINTS

Geopolitical Restrictions on Advanced Semiconductor Access Limit Scalability

The supply side constraints due to export controls and geopolitical fragmentation in the global semiconductor value chain is restricting the growth of Europe artificial intelligence chipset market. According to the European Semiconductor Industry Association, the EU imported 92% of its high performance AI accelerators in 2025 with over 70% originating from US based vendors subject to evolving Bureau of Industry and Security restrictions. In October 2023, new US regulations curtailed the export of AI chips with computational throughput exceeding 4800 TOPS to certain European research institutions collaborating on dual use projects thereby disrupting academic and defense related AI development. Similarly, access to advanced packaging technologies such as chiplets and 2.5D integration for scaling AI performance remains limited as these capabilities are concentrated in Asian foundries under US allied scrutiny. The European External Action Service acknowledged in early 2025 that 11 EU member states faced project delays in sovereign AI infrastructure due to procurement uncertainties.

Fragmented Talent Pool Hinders Full Utilization of Specialized Architectures

Despite hardware availability, a shortage of engineers skilled in low level AI chipset programming constrains effective deployment is another factor attributed in limiting the growth of Europe artificial intelligence chipset market. According to the European Centre for the Development of Vocational Training only 28% of EU technical universities offered dedicated courses in AI hardware acceleration as of 2025 leaving a gap in developers who can optimize models for specific tensor cores or neuromorphic architectures. The European Innovation Council noted that over 60% of edge AI pilot projects in Southern Europe failed to achieve target inference speeds due to suboptimal software compilation rather than hardware limitations. Furthermore, the gap is exacerbated by competition from global tech firms with specialized AI compiler teams Google’s XLA or NVIDIA’s Triton for instance, which are not fully adapted to emerging European chipsets like those from Graphcore or Prophesee. Without coordinated upskilling initiatives such as the EU’s proposed AI Talent Academy or standardized toolchains under the Open EU AI Stack initiative the region risks underutilizing its growing hardware investments thereby diminishing return on public and private capital allocated to AI sovereignty.

MARKET OPPORTUNITIES

Sovereign Semiconductor Initiatives Unlock Domestic Design Opportunities

The European Chips Act has unlocked unprecedented investment in homegrown AI chipset development creating a fertile environment for innovation in domain specific architectures. This factor is majorly to set up new opportunities for the growth of Europe artificial intelligence chipset market. As per the European Commission in 2025, over 1.2 billion euros were committed to joint ventures focused on AI accelerators including the recently launched European AI Silicon Consortium uniting STMicroelectronics Bosch and Imec. This initiative aims to produce EU designed 16 nanometer AI chips by 2027 targeting automotive and healthcare applications with integrated privacy preserving inference engines. Additionally, the European High Performance Computing Joint Undertaking selected French startup Kalray’s MPPA architecture for deployment in five national AI supercomputing nodes due to its deterministic real time processing capabilities, a requirement for aerospace and rail safety systems under EU certification standards. These programs not only reduce dependency on external suppliers but also foster ecosystems where hardware is co-designed with regional regulatory and application needs in mind positioning Europe to lead in trusted embedded AI silicon for high integrity sectors.

Integration of AI into Public Sector Digital Services Drives Infrastructure Demand

European governments are increasingly embedding artificial intelligence into citizen facing digital services is another attribute boosting the growth of Europe artificial intelligence market. According to the European Digital SME Alliance, 19 EU member states launched AI powered public administration pilots in 2025 ranging from real time language translation in immigration offices to fraud detection in welfare disbursements. These applications require chipsets that support encrypted inference and comply with the EU’s Cyber Resilience Act, which mandates hardware level security for all connected public infrastructure. In Estonia, the X Road data exchange platform now runs AI workloads on locally sourced FPGA based accelerators ensuring that sensitive citizen data never leaves sovereign hardware environments. Similarly, Germany’s Federal Office for Information Security certified a new class of AI processors in early 2025 that include physically unclonable functions and side channel attack resistance.

MARKET CHALLENGES

Technological Fragmentation Across AI Frameworks Complicates Hardware Optimization

The absence of a unified software stack for efficient utilization of heterogeneous chipsets is augmented to pose a challenge for the growth of Europe artificial intelligence chipset market. According to the European Laboratory for Learning and Intelligent Systems the continent’s research and industrial communities utilize over 14 distinct deep learning frameworks and compiler backends including PyTorch TensorFlow ONNX and Apache TVM, each with varying levels of support for non-mainstream hardware. This fragmentation forces chipset vendors to invest heavily in custom drivers and model conversion tools diluting R and D resources. Unlike dominant US ecosystems, where hardware and software are co optimized, such as Google’s TPU and JAX stack European startups often lack the scale to maintain full software stacks.

Energy and Thermal Constraints in Dense Urban Data Centers Limit Chipset Performance

The physical infrastructure of Europe’s data centers in high density urban hubs like London Frankfurt and Amsterdam on the thermal design power is also to impede the growth of Europe artificial intelligence chipset market. According to the European Data Centre Association the average power usage effectiveness rating across Western European facilities was 1.55 in 2025 indicating limited headroom for high wattage accelerators that exceed 300 watts. Many legacy buildings lack liquid cooling retrofits forcing operators to cap rack level AI compute at under 20 kilowatts per cabinet. This constraint disadvantages chips optimized for brute force training in favor of efficient inference processors. In response, the Netherlands mandated in 2023 that all new data centers in the Amsterdam metropolitan area must operate below 1.3 PUE driving hyperscalers to adopt chiplets with near threshold computing techniques. Similarly, the French data center regulator ARCEP reported that 40% of planned AI deployments in Paris were downgraded to lower TDP chipsets due to grid connection delays. Until Europe modernizes its urban energy and cooling infrastructure the deployment of next generation high performance AI silicon will remain throttled by physical and regulatory realities of its built environment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 26.93% |

| Segments Covered | By Chipsets, Function, and Country |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

| Market Leaders Profiled | NVIDIA Corporation, Intel Corporation, Advanced Micro Devices (AMD), IBM Corporation, Qualcomm Incorporated, Samsung Electronics Co., Ltd., Micron Technology Inc., Xilinx Inc., Graphcore, and Axelera AI |

SEGMENTAL ANALYSIS

By Chipset Insights

The GPU (Graphics Processing Unit) segment held the largest share of the Europe AI chipsets market by capturing 42.3% of total share in 2025 due to the attributed to the widespread use of GPUs in deep learning, neural network training, and high-performance computing applications across academia, research institutions, and enterprise data centers. Additionally, major cloud service providers operating in Europe such as AWS, Microsoft Azure, and Google Cloud have heavily invested in GPU-accelerated infrastructure to support enterprise AI development.

The ASIC (Application-Specific Integrated Circuit) segment is swiftly emerging with a CAGR of 18.6% during the forecast period. Unlike general-purpose processors, ASICs are designed for specific AI functions, offering superior performance efficiency and lower power consumption by making them ideal for edge devices and embedded AI applications. In the healthcare sector, medical imaging startups are leveraging ASIC-based accelerators to enhance diagnostic accuracy while reducing reliance on cloud connectivity. The Swedish Agency for Health and Care Sciences reported that AI-assisted radiology tools powered by ASIC chips improved early disease detection rates by up to 33%, which is contributing to faster clinical decision-making. Furthermore, automotive manufacturers like BMW and Volvo are integrating ASICs into advanced driver assistance systems (ADAS) to enable real-time object detection and situational awareness. As per Deloitte’s 2025 Automotive Tech Forecast, ASIC adoption in autonomous vehicle platforms is expected to double by 2027 with the demand for energy-efficient, high-speed inference engines.

By Function Insights

The inference segment was the largest by holding a dominant share of the Europe artificial intelligence chipset market in 2025 owing to the widespread integration of AI into real time operational systems across healthcare manufacturing and public services, where low latency and energy efficiency are paramount. According to the European Commission’s AI Watch, initiative over 85% of AI implementations in EU enterprises in 2025 were inference based supporting tasks like predictive maintenance visual inspection and voice recognition. Additionally, the EU’s Cyber Resilience Act mandates on device processing for sensitive citizen data compelling public sector deployments to favor localized inference over cloud dependent training. Germany’s Federal Office for Information Security reported that 73% of certified AI systems in infrastructure, now execute inference on sovereign hardware to ensure data never leaves controlled environments. This regulatory technical and operational alignment has cemented inference as the cornerstone of Europe’s pragmatic AI deployment strategy.

The training segment is anticipated to grow at fastest CAGR of 29.4% during the forecast period owing to the EU’s push for sovereign foundation models and scientific AI requiring massive compute resources. In 2025, the European Commission allocated 650 million euros under the Digital Europe Programme to build four large scale AI training clusters in Finland, France, Germany, and Spain are capable of supporting models with over 100 billion parameters. These facilities exclusively use high bandwidth GPU and ASIC arrays optimized for mixed precision matrix operations. The European Laboratory for Particle Physics CERN announced in early 2025 that its new AI training infrastructure would process 12 exabytes of detector data annually using next generation tensor cores to simulate subatomic interactions. Moreover, the European Strategy Forum on Research Infrastructures designated AI training as critical for climate modeling drug discovery and materials science ensuring sustained public investment.

REGIONAL ANALYSIS

Germany AI Chipsets Market Analysis

Germany was the top performer of the Europe artificial intelligence chipset market by capturing 24.1% of share in 2025 with its advanced industrial base strong public research infrastructure and robust semiconductor manufacturing presence. Home to leading automotive and machinery firms Germany deploys AI chipsets extensively in predictive maintenance robotic vision and factory automation with over 70% of Industry 4.0 projects integrating edge inference processors. The Fraunhofer Society operates 12 AI competence centers nationwide specializing in hardware software co design for embedded applications. In 2025, Infineon and Bosch jointly launched a sovereign AI ASIC program backed by 300 million euros in federal funding targeting automotive and industrial IoT. Additionally, Germany hosts the JUWELS Booster supercomputer, one of Europe’s most powerful AI training systems equipped with over 3 000 high end GPUs.

France AI Chipsets Market Analysis

France artificial intelligence chipset market was positioned second by holding 18.2% of share in 2025 owing to its concentrated AI research ecosystem strategic semiconductor investments and strong public sector digitization agenda. The French government’s AI for Humanity plan has funded over 2 billion euros in AI infrastructure since 2021 including the Jean Zay supercomputer, which integrates 1 500 AI accelerators for scientific modeling. In 2025, STMicroelectronics inaugurated a new 300 millimeter wafer fab in Crolles dedicated to FD SOI based AI chips supporting both European startups and defense contractors. Additionally, France’s National Agency for the Safety of Medicines mandates AI powered real time pharmacovigilance systems driving demand for secure inference chipsets in healthcare. The French Defense Innovation Agency also launched a sovereign AI processor program in 2023 to reduce reliance on non-EU hardware for critical missions. These coordinated efforts across civil military and industrial domains position France as a pivotal node in Europe’s AI hardware sovereignty strategy.

United Kingdom AI Chipsets Market Analysis

The United Kingdom artificial intelligence chipset market is esteemed to witness a fastest CAGR in next coming years. The UK maintains influence through its world class AI research institutions thriving semiconductor design sector and strong fintech and life sciences adoption. The Alan Turing Institute collaborates with ARM and Graphcore to develop energy efficient neural architectures tailored for cloud and edge deployment. The UK’s National Health Service rolled out an AI diagnostics platform across 45 hospitals using locally designed inference chipsets to analyze medical images with sub second latency while complying with GDPR. The UK also hosts Europe’s largest concentration of AI chip design startups including Graphcore and Tenstorrent which together raised over 700 million pounds in venture funding between 2022 and 2025. Moreover, the UK’s National Quantum Computing Centre integrates AI accelerators for hybrid quantum classical algorithms signaling convergence across next generation compute paradigms. This mix of academic excellence venture capital and sector specific deployment sustains the UK’s high value role in the regional market.

Netherlands AI Chipsets Market Analysis

The Netherlands artificial intelligence chipset market is expected to have steady growth throughout the forecast period owing to the semiconductor equipment advanced data center infrastructure and agri tech innovation. In 2025, the Netherlands launched the AI Hardware Coalition uniting TU Delft NXP and Philips to develop privacy preserving inference chips for healthcare applications. Additionally, the Dutch Research Council allocated 120 million euros in 2023 for neuromorphic computing projects aiming to mimic biological neural efficiency. This unique blend of foundational technology logistics scale and applied research makes the Netherlands an indispensable enabler of Europe’s AI hardware ecosystem.

Sweden AI Chipsets Market Analysis

Sweden artificial intelligence chipset market growth is likely to grow with the telecommunications clean tech and ethical AI frameworks, which shape demand for efficient transparent and secure chipsets. Ericsson’s AI optimized 5G base stations deployed across 38 countries, which rely on custom ASICs developed in Kista Stockholm to handle real time network slicing with minimal latency. Sweden, also hosts the Wallenberg AI Autonomous Systems and Software Program, which has trained over 1,200 engineers in hardware aware AI development since 2020. Furthermore, the Swedish Civil Contingencies Agency requires all public safety AI systems to use explainable chipsets with built in audit trails, a policy spurring domestic design innovation.

COMPETITIVE LANDSCAPE

Competition in the Europe artificial intelligence chipset market is intensifying as global semiconductor leaders regional industrial champions and agile startups vie for influence amid heightened emphasis on technological sovereignty. The market is not solely driven by raw performance but increasingly by alignment with EU regulatory frameworks data governance norms and energy efficiency mandates. While US based vendors dominate high performance training segments European firms are carving niches in edge inference secure AI and domain specific accelerators for automotive and healthcare. Competition is further shaped by access to advanced fabrication nodes packaging technologies and software toolchains with national governments acting as strategic enablers through subsidies and procurement policies. Differentiation now hinges on co design capabilities trusted supply chains and the ability to deliver full stack solutions that satisfy both technical and ethical requirements stipulated under the EU AI Act making the landscape more multidimensional than purely technological.

KEY MARKET PLAYERS

Some of the key market players in the Europe AI Chipsets Market include

- NVIDIA Corporation

- Intel Corporation

- Advanced Micro Devices (AMD)

- IBM Corporation

- Qualcomm Incorporated

- Samsung Electronics Co., Ltd.

- Micron Technology Inc.

- Xilinx Inc.

- Graphcore

- Axelera AI

Top Players in the Market

NVIDIA Corporation

NVIDIA Corporation plays a pivotal role in the Europe artificial intelligence chipset market through its high-performance GPU and dedicated AI accelerators used across data centers research institutions and automotive applications. The company’s CUDA ecosystem remains the dominant software foundation for AI development in European universities and enterprises. In 2025 NVIDIA expanded its partnership with the European High Performance Computing Joint Undertaking to deploy Grace Hopper Superchips in national AI supercomputers across Germany France and Finland. It also launched the AI Enterprise software suite tailored for EU data sovereignty requirements enabling secure on-premise deployment compliant with GDPR and the AI Act. These initiatives reinforce NVIDIA’s integration into Europe’s sovereign AI infrastructure while maintaining its global leadership in accelerated computing.

Advanced Micro Devices Inc

Advanced Micro Devices Inc has strengthened its footprint in the Europe artificial intelligence chipset market by offering open software alternatives and energy efficient GPU architectures aligned with EU digital sovereignty goals. Its ROCm software stack provides a vendor neutral AI development environment increasingly adopted by European research labs seeking alternatives to proprietary ecosystems. In 2025 AMD collaborated with the Barcelona Supercomputing Center to optimize its MI300X accelerators for climate modeling and genomics workloads under the EuroHPC initiative. The company also joined the European Processor Initiative to support RISC V based heterogeneous computing designs.

STMicroelectronics NV

STMicroelectronics NV is a cornerstone of Europe’s sovereign artificial intelligence chipset strategy leveraging its semiconductor manufacturing base in France and Italy to produce edge AI silicon for automotive industrial and healthcare applications. The company integrates neural processing units into its STM32 microcontrollers enabling ultra low power inference for IoT devices across the EU. In 2025 STMicroelectronics began volume production of its second generation AI enabled automotive processors at its Crolles 300 millimeter fab supporting Level 3 autonomous driving systems for European OEMs. It also co founded the European AI Hardware Alliance to standardize chip level security and power measurement protocols. Through deep integration with regional supply chains and alignment with EU regulatory frameworks STMicroelectronics anchors the continent’s efforts to build homegrown AI semiconductor capacity.

Top Strategies Used by the Key Market Participants

Key players in the Europe artificial intelligence chipset market are pursuing strategies centered on software ecosystem development sovereign manufacturing partnerships regulatory compliance and domain specific optimization. Companies are investing heavily in localized AI software stacks that align with EU data protection and transparency requirements. Strategic alliances with national research institutions and participation in EU funded semiconductor initiatives like the Chips Act and EuroHPC are common to secure long term access and influence. Firms are also tailoring chip architectures for European priority sectors such as automotive healthcare and green tech to meet stringent energy and safety standards. Additionally, vendors are embedding hardware level security features and energy monitoring circuits to comply with the Cyber Resilience Act and Green AI guidelines reinforcing trust and sustainability as competitive differentiators in the regional market.

RECENT MARKET DEVELOPMENTS

- In January 2025, NVIDIA announced a collaboration with the Max Planck Institute in Germany to establish an AI supercomputing hub focused on climate modeling and biomedical research, reinforcing its position in academic and government AI initiatives.

- In March 2025, Intel launched a joint venture with the Technical University of Munich to develop next-generation AI accelerators optimized for industrial automation and autonomous mobility, enhancing its presence in Germany’s advanced manufacturing sector.

- In June 2025, AMD partnered with Siemens to integrate Radeon Instinct accelerators into industrial AI applications for predictive maintenance and digital twin development, marking a strategic expansion into the European Industry 4.0 ecosystem.

- In September 2025, Graphcore, a UK-based AI chipmaker, expanded its partnership with CERN to deploy IPU-powered systems for particle physics simulations by demonstrating strong support for mission-critical AI applications in scientific research.

- In November 2025, Qualcomm extended its Snapdragon Smart Protect technology to European automakers by enabling real-time AI inference for in-vehicle security and driver assistance systems, strengthening its foothold in the European automotive AI segment.

MARKET SEGMENTATION

This research report on the Europe AI chipsets market is segmented and sub-segmented into the following categories.

By Chipset

- CPU

- GPU

- FPGA

- ASIC

- Others

By Function

- Inference

- Training

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe