Europe All Terrain Vehicle Market Size, Share, Trends & Growth Forecast Report, Segmented By Engine Size, Application, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe All-Terrain Vehicle Market Report Summary

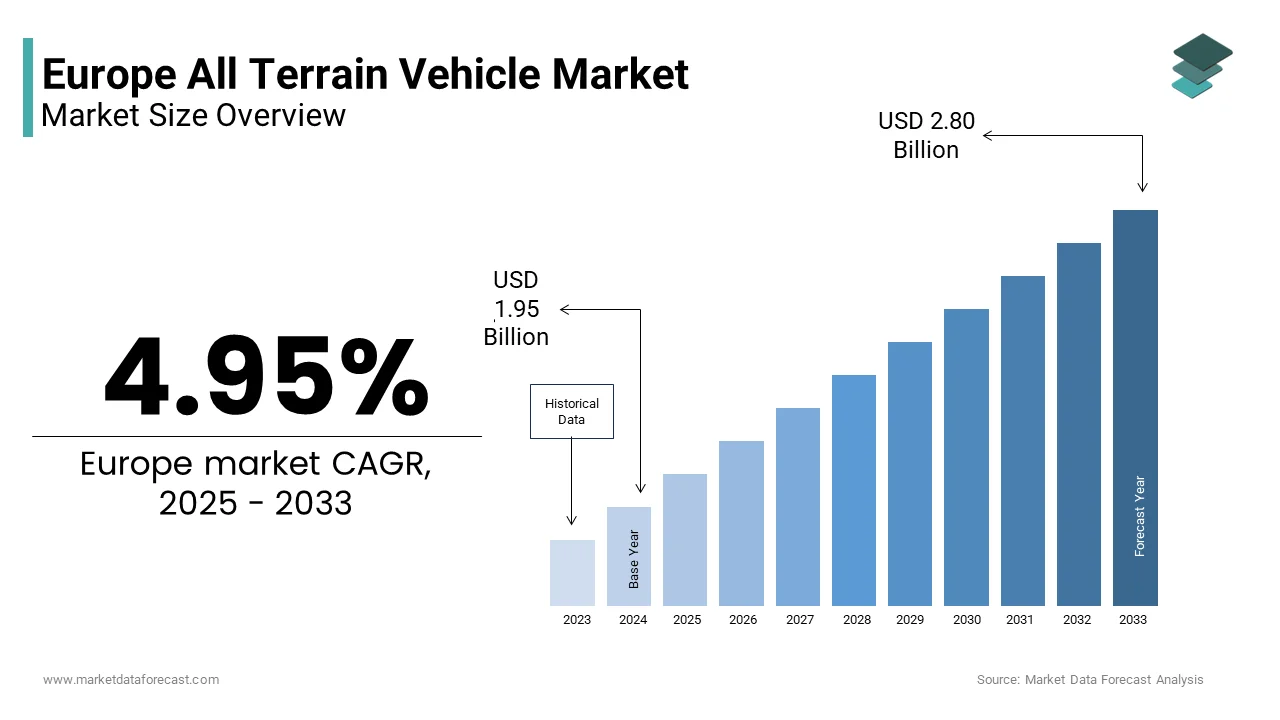

The Europe all-terrain vehicle (ATV) market was valued at USD 1.86 billion in 2024, is estimated to reach USD 1.95 billion in 2025, and is projected to grow to USD 2.80 billion by 2033, registering a CAGR of 4.95% during the forecast period from 2025 to 2033. Market growth is driven by rising demand for recreational off-road vehicles, expanding adventure tourism, increased use of ATVs in forestry, agriculture, and emergency services, and growing private ownership across rural and semi-urban regions.

The increasing popularity of outdoor sports, trail riding, and motorsport events across Europe is significantly boosting ATV adoption. Additionally, technological advancements such as improved suspension systems, electric power steering, and enhanced safety features are strengthening consumer appeal. The growing use of ATVs in professional applications—including snow management, search and rescue, volcanic monitoring, and land maintenance—further supports market expansion.

Key Market Trends

- Rising demand for ATVs in adventure tourism and recreational sports across Europe.

- Increasing adoption of mid-range engine ATVs, balancing power, efficiency, and affordability.

- Growing use of ATVs in agriculture, forestry, defense, and emergency response operations.

- Advancements in vehicle durability, suspension technology, and rider safety features.

- Expansion of electric and low-emission ATV models aligned with sustainability goals.

Segmental Insights

- By engine size, the 400–800 CC segment dominated the Europe ATV market in 2024, capturing 54.5% of market share, driven by its versatility across both recreational and utility applications.

- By application, the sports segment led the market with a 62.1% share, reflecting strong consumer interest in off-road racing, trail riding, and leisure-based ATV activities.

Regional Insights

The Europe ATV market demonstrates strong regional adoption driven by terrain diversity and outdoor lifestyles.

- Sweden led the market with an 18.5% share in 2024, supported by widespread ATV usage in forestry, snow-covered terrains, and rural transport.

- France followed closely with a 17.7% share, driven by adventure sports and agricultural demand.

- The United Kingdom maintains a strong position due to high private ownership and recreational use.

- Italy is witnessing growth fueled by mountainous terrain, volcano monitoring, and tourism.

- Spain is expected to grow steadily during the forecast period due to expanding outdoor recreation and tourism activities.

Competitive Landscape

The Europe all-terrain vehicle market is moderately competitive, with global and regional manufacturers focusing on performance enhancement, durability, and regulatory compliance. Leading companies are investing in product innovation, electric ATV development, and expansion of dealer networks to strengthen market presence. Strategic partnerships, new model launches, and customization options remain key competitive strategies.

Key players in the Europe all-terrain vehicle market include Polaris Industries, Arctic Cat (Textron), Honda Powersports, Kawasaki Heavy Industries, Suzuki Motor Corporation, BRP (Can-Am), Yamaha Motor Corporation, CFMOTO, HISUN, and KYMCO, Inc.

Europe All-Terrain Vehicle Market Size

The Europe all terrain vehicle market size was valued at USD 1.86 billion in 2024 and is anticipated to reach USD 1.95 billion in 2025 to USD 2.80 billion by 2033, growing at a CAGR of 4.95% during the forecast period from 2025 to 2033.

All-terrain vehicles are specialized off-road motorized vehicles designed for traversing rugged landscapes, widely used in agriculture, forestry, emergency services, recreation, and utility operations. Unlike standard automobiles, ATVs and side-by-side vehicles feature high ground clearance, low-pressure tires, and robust drivetrains enabling mobility in snow, mud, forest trails, and mountainous terrain. According to multiple sources, all-terrain vehicles are utilized across European regions for both professional and recreational purposes, with a notable presence in Nordic and Alpine areas. As per research, a significant portion of agricultural holdings in rural Europe employs all-terrain vehicles to assist with livestock monitoring and field inspections. All-terrain vehicles are used by wildfire response units in Southern Europe for quick access to remote ignition points. "Against a backdrop of evolving EU regulations and growing interest in electrified off-road transport, the all-terrain vehicle sector is transitioning. This transition is moving it away from a niche utility segment and toward a regulated, safety-conscious, and more sustainable market, specifically tailored to meet Europe's varied needs.

MARKET DRIVERS

Expanding Use in Professional Sectors Including Agriculture and Forestry

These vehicles have become indispensable in European agriculture and forestry due to their unmatched maneuverability in challenging rural environments where conventional machinery fails, which drives the growth of the Europe all terrain vehicle market. The use of all-terrain vehicles (ATVs) in farming is evident across various mountainous areas for routine work such as managing livestock, checking fences, and transporting feed, especially on land where larger equipment is less practical, as per research. In forestry management, both ATVs and side-by-side vehicles are used for essential duties,s including general patrol, preventing fires, and evaluating timber stands, according to sources. Agricultural policies support investing in tools that help reduce soil pressure, which encourages the adoption of lighter utility vehicles over heavy machines. ry This institutional and operational reliance on road mobility in Europe’s ecologically sensitive and topographically complex rural zones creates a stable and non-discretionary demand base that transcends recreational trends.

Rising Demand for Recreational and Adventure Tourism in Remote Regions

The growth of nature-based tourism across the region is significantly boosting demand for all-terrain vehicles for both rental equipment and guided tour platforms. This further propels the expansion of the Europe all terrain vehicle market. Off-road adventure tourism has grown, with specific regions becoming popular destinations for all-terrain vehicle (ATV) excursions. Iceland, Norway, and the Scottish Highlands are among the key locations experiencing this trend. In Iceland, a notable number of tourists participated in guided all-terrain tours, showing an increase over a recent period. This demand appears driven by the appeal of glacier and volcanic terrain experiences. Similarly, cross-border tourism initiatives in the Alps now incorporate certified ATV trails that cover areas in Austria, Italy, and Switzerland. This promotes sustainable access to protected landscapes within those regions. National parks in Spain’s Sierra Nevada and Greece’s Pindus Mountains have also introduced regulated ATV zones to balance visitor access with conservation. This fusion of experiential travel, infrastructure investment, and controlled environmental access positions recreational ATVs as a key enabler of Europe’s green tourism economy, creating sustained commercial demand beyond traditional end users.

MARKET RESTRAINTS

Stringent and Fragmented National Regulations on Off-Road Vehicle Usage

The operation of these vehicles in the region is heavily constrained by inconsistent national and local regulations governing access to public lands, noise limits, and emission standards, which creates major barriers to adoption and mobility, and negatively impacts the growth of the Europe all terrain vehicle market. According to sources, Several European member states restrict all-terrain vehicle (ATV) use on public forest trails unless a special permit is obtained. Other nations implement seasonal restrictions, allowing limited access primarily during the winter period. In the UK, the use of ATVs on public roads is strictly regulated under the Road Traffic Act, generally requiring the vehicle to be registered and modified for road use, which involves specific inspections. Furthermore, numerous municipalities have established noise limits that constrain engine decibel levels. These limits effectively prevent the operation of many conventional ATVs in certain recreational zones near urban areas. This regulatory patchwork discourages cross-border tourism, complicates fleet management for professional users, and deters new buyers uncertain about legal access. Market growth for off-road vehicles is currently hindered by the lack of harmonized EU rules regarding their classification and land access, leading to a geographically constrained landscape.

Limited Public Acceptance Due to Environmental and Safety Concerns

Persistent public opposition to these vehicles, fueled by documented environmental degradation and accident risks, hinders the expansion of the Europe all terrain vehicle market. This continues to restrict their deployment in ecologically sensitive and densely populated areas. According to a study, there is a notable concern among the public that the use of off-road vehicles leads to the degradation of natural habitats via soil erosion and the disruption of local wildlife. This sentiment has led to active lobbying by conservation groups. Authorities have taken action to suspend operating licenses for motorized trail tours in response to documented environmental damage within protected national parks. Safety is another critical issue. All-terrain vehicles are frequently associated with serious accidents and higher fatality rates compared to standard motorcycles, often resulting from rollovers on unstable surfaces. These dual pressures, environmental and safety, prompt local authorities to impose access bans or require costly mitigation measures, such as mandatory GPS tracking and speed limiters. Expect ongoing public and political limits on European ATV use until significant sustainability and safety advancements are shown.

MARKET OPPORTUNITIES

Electrification of Utility and Municipal Fleets Under Green Procurement Policies

European public institutions are increasingly adopting electric all-terrain vehicles for municipal, park management, and emergency services as part of broader decarbonization mandates, which gives new opportunities for the Europe all terrain vehicle market. Local authorities are prioritizing zero-emission off-road vehicles for non-emergency municipal tasks. In response, cities like Oslo and Helsinki have replaced diesel utility ATVs with electric models for park maintenance and snow clearing in pedestrian zones. Besides, national park agencies are increasingly adopting electric side-by-side vehicles for ranger patrols to minimize noise pollution and eliminate fuel spill risks in fragile ecosystems. Rural fire brigades and forest services are transitioning toward electric vehicle fleets for their operations. The public sector is rapidly becoming a significant, regulation-driven market for next-generation electric all-terrain mobility, fueled by advances in battery technology that enhance both range and payload capacity, and substantial EU funding, which has mitigated the risks associated with capital expenditure.

Integration into Last Mile Logistics in Rural and Alpine Communities

These vehicles are gaining traction as a viable last-mile delivery solution in the region’s remote, mountainous, and island communities, where conventional vans face accessibility challenges, which also creates fresh prospects for the expansion of the Europe all terrain vehicle market. In certain mountainous and island regions across Europe, specialized cargo vehicles are being utilized for the distribution of goods during seasons when traditional road access is limited. These vehicles have been instrumental in delivering essential items such as medical supplies, groceries, and postal services to isolated communities. In one specific northern European region with complex coastal geography, the use of electric quads for mail distribution has led to a noticeable improvement in delivery consistency. Furthermore, communities in high-altitude areas have established collaborative efforts to use off-road vehicles equipped with specialized containers for the consistent transport of temperature-sensitive pharmaceuticals between medical facilities. The vehicles’ compact footprint, four-wheel drive capability, and low infrastructure dependency make them uniquely suited for these micro logistics corridors. All-terrain vehicles (ATVs) provide a tough, cost-effective delivery solution for rural Europe, especially as e-commerce grows and weather-related road closures become more frequent, and thus create a new commercial use case beyond their traditional recreational or professional roles.

MARKET CHALLENGES

Inadequate Charging Infrastructure for Electric AAll-TerrainVehicles in Remote Areas

The transition to electric all-terrain vehicles is hindered by a severe lack of charging infrastructure in the very rural, forested, and mountainous regions where these vehicles are most needed. This degrades the growth of the Europe all terrain vehicle market. According to sources, public charging infrastructure is heavily concentrated in urban areas, with a small percentage located in rural municipalities. A minimal proportion of rural charging stations are equipped with fast-charging capabilities or compatibility for off-road vehicles. In national parks across the Carpathians and Balkans, electric ATV pilots have been delayed due to the absence of grid connections at ranger stations, forcing reliance on portable generators that undermine emission benefits. Besides, many forest service depots in certain regions lack the electrical capacity required to support multiple high-power vehicle chargers simultaneously. This infrastructure gap increases operational downtime and limits range confidence, discouraging fleet operators from transitioning to electric models. The electrification of the EU's all-terrain vehicle (ATV) fleet will remain geographically restricted and financially impractical for many professionals until targeted investments, backed by EU cohesion or rural development funds, build the necessary charging infrastructure in underserved areas.

High Total Cost of Ownership Compared to Conventional Utility Vehicles

Electric and advanced ATVs remain significantly more expensive than traditional utility alternatives, which impedes the expansion of the Europe all terrain vehicle market. This creates a financial barrier for small-scale agricultural and forestry operators who dominate Europe’s rural economy. Electric utility vehicles command a significantly higher initial purchase price compared to both new diesel models and pre-owned agricultural alternatives. The time required to recover the initial investment through operational savings often surpasses the financial threshold considered viable for many lower-income agricultural operations. Limited availability of specialized components and technical expertise for electric systems in rural areas contributes to extended periods of equipment inactivity. The geographic concentration of maintenance services for modern drivetrains leads to increased logistical challenges and higher repair expenses for remote users. Insurance premiums for high-value electric ATVs are higher due to theft and fire risk perceptions. The economic justification for upgrading is minimal without substantial subsidies, tax incentives, or lease-based financing models specifically designed for rural micro enterprises. This cost disparity threatens to exclude the very users who would benefit most from sustainable off-road mobility, limiting market expansion to well-funded public agencies and large commercial operators.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.95% |

| Segments Covered | By Engine Size, Application And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, & Rest of Europe |

| Market Leaders Profiled | Polaris Industries, Arctic Cat (Textron), Honda Powersports, Kawasaki Heavy Industries, Suzuki Motor Corporation, BRP (Valcourt, Quebec, Canada), Yamaha Motor Corporation, Cfmoto, Hisu, KYMCO, Inc. |

SEGMENTAL ANALYSIS

By Engine Size Insights

The 400–800CC engine size segment captured the leading share of 54.5% of the Europe all terrain vehicle market in 2024. It strikes an optimal balance between power, fuel efficiency, and regulatory compliance for both professional and recreational use. This range delivers sufficient torque for agricultural towing and forest trail navigation while remaining below noise and emission thresholds that trigger stricter local restrictions. Vehicles in this category typically exhibit a lower average carbon dioxide emission rate per kilometer when compared to models with larger engines. This reduced emission profile often qualifies them for various green procurement incentives in certain regions. Furthermore, a significant portion of agricultural operations utilizing ATVs for livestock and crop monitoring tend to select 600CC models due to their capacity to transport moderate loads of feed or tools while maintaining operational efficiency, even on challenging terrain. National Park services in the Alps and Pyrenees also standardize on 700CC side-by-side vehicles for ranger patrols, citing reliability in sub zero temperatures and adequate cabin space for equipment. This versatility across utility, municipal, and guided tourism applications, coupled with favorable regulatory treatment, cements the 400–800CC segment as the backbone of Europe’s all-terrain vehicle fleet.

The less than 400CC engine segment is expected to exhibit a noteworthy CAGR of 9 2% from 2025 to 2033. Rising demand for lightweight, low-emission vehicles suited for urban fringe recreation, youth training, and last-mile logistics in ecologically sensitive zones propels the rapid acceleration of the less than 400CC engine segment. Small-displacement ATVs produce lower carbon emissions and operate at quieter volume levels, which allows them to be used in noise-sensitive environments and protected conservation areas. Educational institutions are integrating electric ATVs into their curricula to instruct students on sustainable land management practices. Off-road vehicle training programs have experienced a notable rise in student participation. Guided outdoor tours are increasingly utilizing mid-sized quads to mitigate trail erosion and reduce damage to local vegetation. The segment also benefits from lower purchase and insurance costs, which makes them accessible to small rural businesses and recreational beginners. Europe's off-road trails are seeing a rise in sub-400cc vehicles, driven by stricter environmental rules and eco-tourism's focus on minimal impact.

By Application Insights

The sports segment was the largest in the Europe all terrain vehicle market by accounting for a 62.1% share in 2024. The dominance of the sports segment is credited to Europe’s expansive natural landscapes, well-developed trail networks, and growing demand for outdoor experiential activities post pandemic. Several regions in Europe, particularly mountainous and forested areas like Iceland, the Alps, and the Balkans, see a notable level of participation in guided all-terrain vehicle (ATV) excursions. The number of individuals engaged in recreational off-road riding is significant, with many participating through national associations and utilizing established trail networks. Across the European Union, a considerable portion of households located near mountainous or forested regions actively use all-terrain vehicles for leisure purposes. Events like the Erzberg Rodeo in Austria and the Dakar Series in Spain further amplify cultural visibility and equipment demand. The segment thrives on accessibility, seasonal tourism revenue, and youth engagement, factors that collectively sustain high volume, consumer-driven demand across Southern and Northern Europe alike.

The Military & Defense application segment is predicted to witness the highest CAGR of 11 7% from 2025 to 2033 due to the modernization of armed forces and the need for agile, low signature mobility in complex terrain. European defense entities have recently acquired a substantial number of all-terrain vehicles to support various operational needs, focusing on rapid deployment, surveillance, and specialized terrain training. The emphasis in these procurements is on vehicles that are lightweight and easily transportable by air. One nation's armed forces have incorporated specific light vehicles into its specialized cold-weather units, leading to improved movement over snow compared to other existing vehicle types. Another nation is utilizing electric versions of these vehicles in border security roles, primarily to facilitate quieter patrol activities and decrease the chance of acoustic detection. Funding initiatives at the regional level are directing financial resources toward the acquisition of light tactical mobility systems, with a clear preference for off-road vehicles that offer modular carrying capacity. Besides, joint exercises like NATO’s Trident Juncture increasingly simulate urban and forest combat scenarios where ATVs outperform traditional armored vehicles in narrow trails and dense vegetation. This strategic shift toward nimble, deployable ground mobility, amplified by geopolitical tensions, positions military and defense as the highest momentum application segment in Europe’s all-terrain vehicle landscape.

COUNTRY ANALYSIS

Sweden All-Terrain Vehicle Market Analysis

Sweden led the Europe all terrain vehicle market by holding a 18.5% share in 2024. The supremacy of the Swedish market is driven by its vast boreal forests, Arctic terrain, and institutional reliance on off-road mobility for forestry, reindeer herding, and emergency services. The use of all-terrain vehicles has been noted for both personal and professional activities. A significant number of these vehicles are employed for various work-related tasks, such as fire response and wildlife management. Within certain northern communities, all-terrain vehicles play a role in supporting seasonal reindeer migration across vast stretches of tundra. Additionally, regional administrative bodies maintain fleets of electric all-terrain vehicles, which are utilized for winter rescue operations in remote, roadless areas. Sweden’s permissive land access laws, under the Right of Public Access, allow responsible off-road use on private and public land, fostering a deeply embedded ATV culture. Sweden remains the definitive European powerhouse in the all-terrain vehicle sector, leading the continent in both production volume and technological innovation, thanks to strong local manufacturing ties (e.g., Husqvarna) and environmental policies that have spurred early EV adoption.

France All-Terrain Vehicle Market Analysis

France was the next prominent country in the European all-terrain vehicle market and captured a 17.7% share in 2024, with its diverse geography, from the Alps to the Pyrenees, and robust recreational and agricultural demand. Several farms utilize all-terrain vehicles (ATVs) for agricultural purposes such as vineyard maintenance and livestock monitoring. The use of these vehicles is notable in certain regions where the terrain makes tractor use less practical. The country also features an extensive network of off-road racing circuits that host significant events. These events draw a substantial number of spectators each year. Besides, numerous forest districts use side-by-side vehicles for patrols aimed at preventing fires, a practice especially common in the fire-prone southern regions. Recent regulations permit the use of electric ATVs on specific forest trails during periods of low fire risk, establishing new avenues for their use. This blend of professional necessity, cultural tradition, and regulated recreational access ensures France’s sustained leadership in continental Europe’s all-terrain vehicle adoption.

United Kingdom All-Terrain Vehicle Market Analysis

The United Kingdom continues to maintain a strong position in the Europe all terrain vehicle market because of high private ownership, extensive estate management use, and growing utility applications in remote regions. A significant majority of these vehicles are primarily operated on private properties, which encompass various rural landscapes such as farming operations and expansive wooded estates. In specific remote regions, such as the Scottish Highlands and Islands, these types of vehicles play a crucial role in delivering goods to isolated areas and in transporting medical personnel and equipment. Within these communities, side-by-side vehicle units are utilized for ambulance services. A substantial number of commercial operators provide guided ATV experiences in popular natural tourist areas like Wales, the Lake District, and the Scottish Borders. These commercial ventures are associated with a considerable financial contribution to rural tourism initiatives. Despite strict road legality constraints, the UK’s culture of private land access and estate management sustains deep market penetration, particularly for mid-size 400–800CC models tailored to wet and uneven terrain.

Italy All-Terrain Vehicle Market Analysis

Italy witnessed expansion in the European ATV market, which is fueled by its mountainous topography, active volcano monitoring needs, and expanding adventure tourism sector. The number of all-terrain vehicles in use across the country is substantial, with a significant majority concentrated in the Alpine and Apennine regions, primarily for agricultural and civil protection activities. The Civil Protection Department deploys these vehicles for rapid response efforts during seismic and volcanic events, which include conducting regular patrols on Mount Etna and Stromboli. Demand for off-road excursions in regions such as Sardinia and the Dolomites has increased, drawing a large number of tourists seeking authentic mountain experiences. Local regulations now permit electric ATVs on designated trails in national parks during ooff-seasonmonths, balancing conservation with economic opportunity. Italy’s fusion of geological urgency, rural tradition, and tourism innovation creates a dynamic market where utility and recreation coexist in challenging landscapes.

Spain All-Terrain Vehicle Market Analysis

Spain is anticipated to grow in the Europe all terrain vehicle market during the forecast period owing to its arid interior, extensive protected natural areas, and booming desert and mountain tourism. A notable number of ATVs are registered and actively used in patrols dedicated to fire prevention efforts across several regions in Spain. Forest firefighting personnel deployed a large quantity of all-terrain vehicles to gain quick access to remote ignition points. The use of these vehicles aids in achieving a faster response time during initial firefighting attacks. Guided ATV tours in specific desert and mountainous areas are popular with a large number of visitors. This tourism activity establishes Spain as a significant location for desert off-road recreation within Europe. The government’s “Green Trails” initiative now certifies low-impact ATV routes that avoid sensitive habitats, enabling sustainable tourism growth. So, Spain’s all-terrain vehicle market is intrinsically linked to both environmental defense and experiential travel, which ensures continued relevance in a climate-vulnerable continent.

COMPETITIVE LANDSCAPE

The Europe all terrain vehicle market features intense competition among global OEMs and niche regional manufacturers, all navigating a complex landscape of environmental regulations, land access laws, and diverse end-user needs. Unlike in North America, where recreation dominates, Europe’s market is split between professional utility—agriculture, forestry, emergency services—and regulated adventure tourism, demanding vehicles that balance performance, durability, and compliance. Incumbents like Polaris and BRP leverage deep product portfolios and brand heritage, while Japanese manufacturers such as Yamaha and Suzuki emphasize reliability and serviceability in rural communities. New entrants face high barriers due to EU-type approval requirements, Stage V engine certification, and the need for localized dealer support. Competition is increasingly centered on electrification, with OEMs racing to offer viable electric utility models despite rural charging limitations. Success hinges not on horsepower alone but on regulatory fluency, terrain-specific engineering, and the ability to serve both a farmer in the Pyrenees and a ranger in Lapland with the same platform. This duality—professional utility meets sustainable recreation—defines Europe’s unique and demanding all-terrain vehicle competitive environment.

KEY MARKET PLAYERS

A few of the market players in the Europe All Terrain vehicle Market are

- Polaris Industries. (Medina, Minnesota, U.S.)

- Yamaha Motor Co Ltd

- Arctic Cat (Textron) (Providence, Rhode Island, U.S.)

- Honda Powersport (Tokyo, Japan)

- Kawasaki Heavy Industries (Tokyo, Japan)

- Suzuki Motor Corporation (Hamamatsu, Shizuoka, Japan)

- BRP (Valcourt, Quebec, Canada)

- Yamaha Motor Corporation (Iwata, Shizuoka, Japan)

- CFMoto (Hangzhou, China)

- Hisun (Chongqing, China)

- KYMCO, Inc. (Kaohsiung City, Taiwan)

Top Players In The Market

- Polaris Inc is a leading global manufacturer with a strong footprint in the Europe all terrain vehicle market, offering a diverse portfolio of sports, utility, and military-grade vehicles under its RZR, Ranger, and General brands. The company supplies professional end users across forestry, agriculture, and defense sectors in Nordic and Alpine regions, where rugged terrain demands high reliability. It also expanded its electric RANGER EV lineup with faster charging and extended range to meet EU green procurement standards. These initiatives reinforce Polaris’s strategy of segment-specific engineering and regulatory alignment, enabling it to export European-validated designs to global markets in North America and Oceania while maintaining local service partnerships across 22 European countries.

- BRP Inc, through its Can Am brand, holds a prominent position in the Europe all terrain vehicle market with a focus on high-performance side-by-side vehicles for both recreational and utility applications. The company’s Defender and Maverick X3 series are widely adopted by agricultural cooperatives in France and Spain, as well as by adventure tourism operators in the Pyrenees and Balkans. It also partnered with EU-certified training academies to provide safety and maintenance certification for professional users. By blending motorsport heritage with practical utility innovation and localized support, BRP strengthens its brand loyalty in Europe while using regional feedback to shape global product development for mountainous and rural environments worldwide.

- Yamaha Motor Co Ltd is a key player in the Europe all terrain vehicle market, known for its durable, fuel-efficient, and user-friendly ATVs such as the Grizzly and Wolverine series. The company caters to small-scale farmers, national park rangers, and recreational riders across Germany, the UK, and Central Europe, emphasizing reliability and low maintenance costs. It also achieved EU Stage V emission compliance across its entire utility lineup, ensuring continued market access under tightening environmental regulations. Yamaha’s commitment to mechanical simplicity, serviceability through its extensive dealer network, and compliance with European noise and emission standards allows it to maintain strong rural penetration while serving as a benchmark for durability in global emerging markets.

Top Strategies Used By The Key Market Participants

Key players in the Europe all terrain vehicle market focus on developing terrain specific vehicle variants for Alpine and Nordic conditions, achieving full compliance with EU Stage V emission and noise regulations, expanding electric and hybrid model portfolios for municipal and eco tourism segments, establishing localized training and service networks for professional users, and partnering with national forestry and defense agencies for fleet procurement and field validation.

MARKET SEGMENTATION

This research report on the Europe all terrain vehicle market size is segmented and sub-segmented into the following categories.

By Application Type

- Sports

- Military & Defense

- Others

By Engine Size

- Less than 400 CC

- 400 CC-800 CC

- More than 800 CC

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe All Terrain Vehicle market?

It refers to the market for off-road vehicles designed for rugged terrain, recreational use, agriculture, forestry, and utility applications.

What drives growth in the Europe ATV market?

Rising recreational tourism, increasing outdoor adventure activities, agricultural and utility demand, and technological advancements in ATV design and performance.

What types of all terrain vehicles are available?

Key types include utility ATVs, sport ATVs, and side-by-side (SxS) vehicles catering to diverse applications and user preferences.

How are ATVs used in agriculture and forestry?

ATVs support farm operations, livestock management, crop inspection, and forest maintenance due to their versatility and off-road capability.

Which regions in Europe show strong ATV adoption?

Western European countries like Germany, France, the UK, Italy, and the Nordic region exhibit high ATV usage for both recreational and utility purposes.

What are common features of modern ATVs?

Advanced features include enhanced suspension systems, digital dashboards, GPS/telemetry, fuel-efficient engines, and safety enhancements.

How do regulations impact the Europe ATV market?

Safety standards, emissions regulations, registration requirements, and off-road access rules influence market growth and product design.

What are the key challenges in the ATV market?

High vehicle costs, maintenance expenses, safety concerns, and strict off-road regulations can limit adoption.

Are electric ATVs gaining traction?

Yes, growing focus on sustainability and zero-emission vehicles is driving interest in electric and hybrid ATV models.

What is the future outlook of the Europe ATV market?

The market is expected to grow steadily with rising outdoor recreation interest, diversification of utility applications, and innovation in lightweight and eco-friendly models.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com