Europe Animal Disinfectants Market Size, Share, Trends & Growth Forecast Report, Segmented By Type, Application, Form and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis 2026 to 2034

Market Size, 2025

$1.14 BnMarket Estimate, 2026

$1.21 BnMarket Forecast, 2034

$1.94 BnCAGR, 2026–2034

6.08%Europe Animal Disinfectants Market Size

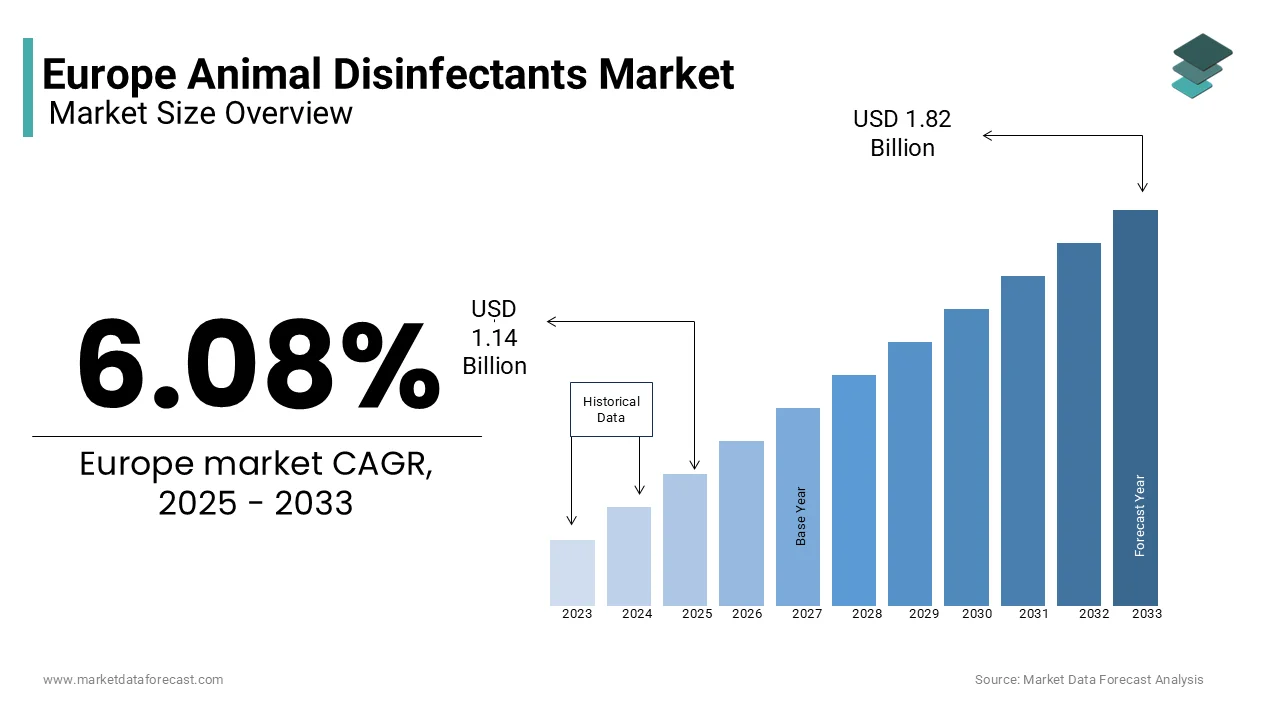

The Europe animal disinfectants market size was valued at USD 1.14 billion in 2025 and is anticipated to reach USD 1.21 billion in 2026 to from USD 1.94 billion by 2034, growing at a compound annual growth rate (CAGR) of 6.08% during the forecast period from 2026 to 2034.

Animal disinfectants are chemical formulations specifically designed to eliminate or reduce pathogenic microorganisms in livestock housing, poultry farms, veterinary clinics, transport vehicles, and equipment used in animal husbandry. These products range from quaternary ammonium compounds and iodophors to peroxygen-based and chlorine dioxide solutions that are critical components of biosecurity protocols mandated under European Union animal health legislation. According to the European Food Safety Authority, most commercial pig and poultry farms in the EU have implemented structured disinfection routines as part of compulsory on-farm biosecurity plans. The sector operates under stringent regulatory oversight from the European Chemicals Agency and the European Medicines Agency, which evaluate active substances for efficacy, environmental persistence, and toxicity to non-target species.

MARKET DRIVERS

Stringent EU Biosecurity Mandates Drive Routine Disinfectant Use

European Union legislation increasingly enforces rigorous on-farm biosecurity measures, are directly elevates demand for approved animal disinfectants, which is one of the primary factors driving the growth of the European animal disinfectants market. Regulation (EU) 2016/429 on transmissible animal diseases is fully applicable since 2021, and this requires all commercial livestock holdings to implement documented hygiene and disinfection protocols. According to the European Food Safety Authority, disinfectants used against high-consequence pathogens such as foot-and-mouth disease must be listed in the EU Reference Laboratory’s validated product register. In Germany, the Federal Ministry of Food and Agriculture has expanded digital traceability systems for livestock farm hygiene documentation, while France’s Ministry of Agriculture enforces regular third-party audits of disinfection practices in large-scale poultry operations. These regulatory imperatives have transformed disinfectant application from a discretionary practice into a legally binding operational requirement, further ensuring consistent demand regardless of market cycles.

Rising Incidence of Zoonotic and Epizootic Disease Outbreaks

The rising frequency of epizootic disease events in Europe intensifies reliance on effective disinfection as a frontline containment measure is further boosting the animal disinfectants market growth in Europe. Each outbreak triggers compulsory depopulation and multi-stage disinfection of affected facilities under Directive 2005/94/EC, which requires substantial volumes of virucidal agents per site. National authorities such as those in the Netherlands and France reported large-scale bird culling operations during 2023, accompanied by extensive use of chlorine-and peroxide-based disinfectants to control viral spread. During the same period, African Swine Fever (ASF) persisted across multiple EU member states, with confirmed infections in domestic pigs and wild boar reported by the European Commission’s Animal Disease Information System. These outbreaks led to strict biosecurity enforcement, including perimeter disinfection at farm entry points, vehicle wash areas, and transport corridors. The continued circulation of zoonotic pathogens, along with sporadic detections of avian influenza viruses in wildlife such as foxes and seals, is promoting the need for routine, preventive disinfection practices across Europe.

MARKET RESTRAINTS

Regulatory Restrictions on Hazardous Active Substances

The progressive chemical safety framework of the European Union imposes significant limitations on commonly used disinfectant ingredients, which is one of the major factors restraining the regional market growth. According to the European Chemicals Agency (ECHA), several active substances previously used in veterinary disinfectants have been withdrawn or not renewed under the Biocidal Products Regulation (BPR) due to concerns about environmental persistence, aquatic toxicity, or potential endocrine-disrupting properties. Among these, formaldehyde-based formulations faced significant restrictions after classification as a carcinogen category 1B under the CLP Regulation (EC No 1272/2008). Regulatory agencies across the EU, including the German Federal Institute for Risk Assessment (BfR), have emphasized that many older disinfectant formulations no longer comply with updated environmental and safety standards. Reformulating these products requires renewed efficacy validation under EN 17154 and EN 14675 standards, a process that involves high testing and documentation costs for manufacturers. Smaller producers face particular challenges in meeting these requirements, which are leading to a gradual reduction in the number of approved broad-spectrum disinfectants available on the market.

Price Volatility of Raw Chemical Inputs

Fluctuations in the cost and availability of key chemical precursors in Europe are further hindering the European animal disinfectants market growth. According to the European Industrial Gases Association (EIGA), hydrogen peroxide prices in Europe rose sharply between 2022 and 2,023, driven by elevated energy costs and reduced production at key facilities in Germany and Belgium that serve as major manufacturing hubs for the compound. Similarly, data from the European Chlorine Industry indicate a notable decline in chlorine output in 2022, as several electrolysis plants curtailed operations amid record natural gas prices. These upstream disruptions have translated into higher costs for formulated disinfectant products. A 2023 assessment by European livestock associations reported that a majority of pig and poultry producers experienced double-digit increases in disinfectant prices. Circumstances such as these are influencing some farms to moderate application frequency or shift toward lower-cost formulations. Supply chain instability has further amplified cost pressures. According to the European Chemical Transport Association, logistical disruptions, particularly those linked to shipping delays through the Red Sea corridor in early 2024 were affected the import of tertiary amines, which are a key precursor for quaternary ammonium compounds widely used in biosecurity applications.

MARKET OPPORTUNITIES

Integration of Disinfection into Digital Farm Management Platforms

The convergence of biosecurity protocols with precision livestock farming technologies is one of the promising opportunities for the European animal disinfectants market. According to the Digital Agriculture Strategy of the European Commission, more than half of large-scale dairy and poultry farms in the EU have adopted farm management software integrating hygiene and disinfection scheduling modules. Major equipment suppliers such as DeLaval and Big Dutchman have incorporated disinfectant tracking and automation features within their IoT-enabled barn management systems, which issue alerts based on parameters such as animal throughput, occupancy, and pathogen-risk indices. This digitalization enables data-driven optimization of hygiene operations, adjusting disinfectant concentration, thus improving cost efficiency while maintaining compliance. Manufacturers are simultaneously advancing traceability and automation, introducing RFID-tagged disinfectant containers that automatically log batch numbers and consumption volumes to cloud-based traceability systems, in alignment with EU Regulation (EU) 2017/625 on official controls.

Expansion of Organic Antibiotic-Free Livestock Production

The rapid growth of organic and antibiotic-reduced animal farming in Europe is another major opportunity for the European animal disinfectants market. Under Council Regulation (EC) No 834/2007 and its implementing acts, synthetic biocides are prohibited in organic production, allowing only naturally derived agents such as acetic acid, lactic acid, and hydrogen peroxide obtained through biological fermentation. This segment requires specialized, low-residue formulations that balance microbicidal efficacy with environmental compatibility. For example, lactic-acid-based disinfectants must comply with EN 1656 bactericidal performance standards while maintaining pH levels suitable for compostable litter systems.

MARKET CHALLENGES

Environmental Persistence and Ecotoxicity Concerns

The long-term ecological impact of residual disinfectant compounds in agricultural runoff is a major challenge to the growth of the Europe animal disinfectants market. According to the European Environment Agency (EEA), quaternary ammonium compounds (QACs) have been detected in surface waters across several EU member states, particularly near intensive livestock areas, where concentrations in some samples have approached or exceeded ecological safety thresholds for aquatic organisms. These cationic surfactants are known to persist in the environment and can accumulate in sediments, potentially disrupting microbial processes essential for nutrient cycling. As per the research conducted by the Swedish University of Agricultural Sciences, repeated use of iodophor disinfectants can negatively influence soil nitrification activity, with measurable declines observed under controlled field conditions. Such findings indicate growing concerns about the ecotoxicological impacts of disinfectant residues in agricultural environments. Regulatory attention is also increasing; for instance, the European Chemicals Agency (ECHA) has proposed stricter hazard classifications for certain QACs, including alkyl dimethyl benzyl ammonium chloride, based on their persistence and bioaccumulation potential. This initiative could expand authorization and risk management requirements under REACH. Farmers consequently face trade-offs between biosecurity performance and environmental compliance, particularly in nitrate-vulnerable zones, where both manure management and chemical inputs are tightly regulated.

Fragmented Approval Processes Across Member States

The divergent national interpretations and authorization timelines delay market access and increase compliance costs for manufacturers, which further challenge the regional market expansion. According to the European Biocidal Products Industry Association, obtaining mutual recognition of a disinfectant approval across several EU markets typically takes over a year, with some member states, such as Italy and Spain, often requesting additional ecotoxicity or local efficacy data beyond the standard EU dossier. In certain cases, national authorities have rejected disinfectant products approved in other EU countries on grounds of differing local pathogen conditions or test requirements, even when EN standard validation was provided. These inconsistencies force companies to maintain multiple formulations or withdraw from smaller markets altogether. Industry surveys indicate that many small and medium-sized enterprises limit their product portfolios to a few EU countries due to regulatory fragmentation and high compliance costs. The resulting patchwork of available products complicates farm-level procurement, especially for multinational agribusinesses operating across borders. Until mutual recognition procedures are fully harmonized and national derogations minimized, the market will remain inefficient, hindering the rapid deployment of next-generation disinfectants during disease emergencies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.08% |

| Segments Covered | By Type, Form Application, and Region. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Zoetis (US), The Chemours Company (US), Nufarm Limited (US), The Dow Chemical Company (US), and Neogen Corporation (US) |

SEGMENTAL ANALYSIS

By Type Insights

In 2025, the hydrogen peroxide segment held 34.3% of the Europe animal disinfectants market share. The regulatory acceptance under EU organic and environmental standards is propelling the growth of the hydrogen peroxide segment in the European market. Hydrogen peroxide is widely endorsed across European regulatory frameworks due to its rapid decomposition into water and oxygen, leaving no toxic residues. As per the European Commission’s 2023 update to the list of approved active substances for biocidal products, hydrogen peroxide remains fully authorized for use in livestock disinfection without concentration restrictions, unlike quaternary ammonium compounds, which face growing limitations. The integration of hydrogen peroxide disinfectants into automated cleaning systems is further boosting the segmental expansion in the European market. The compatibility of hydrogen peroxide with robotic and CIP (clean-in-place) systems in large-scale livestock operations drives the dominance of the hydrogen peroxide segment in the European market. Furthermore, Industry reports indicate that a majority of new dairy and poultry facilities across the EU now incorporate hydrogen peroxide–based automated disinfection cycles, which reflects its widespread acceptance in mechanized sanitation. Its stability in solution, non-corrosive nature toward stainless steel, and rapid kill kinetics allow seamless integration into timed sanitation protocols without manual intervention; these factors are further contributing to the growth of the hydrogen peroxide segment in this regional market.

The lactic acid segment is lucrative and is estimated to showcase a CAGR of 13.4% over the forecast period. The rising demand for lactic acid in organic and antibiotic-free production systems is majorly boosting the growth of the lactic acid segment in the European market. Lactic acid is increasingly favored in organic livestock farming due to its natural origin and GRAS (Generally Recognized As Safe) status. According to Eurostat, the number of organic pig and poultry farms in the EU continued to grow in 2023, reflecting stricter limits on the use of synthetic biocides. The proven efficacy of lactic acid against key zoonotic pathogens is further boosting the growth of the lactic acid segment in the European market. As per the research from recognized European veterinary institutes, appropriately concentrated lactic acid solutions can achieve multi-log reductions of Campylobacter jejuni on poultry housing surfaces and consistent with EN 13727 standards.

By Form Insights

The liquid form segment led the market by accounting for 77.4% of the regional market share in 2025. The domination of the liquid form segment is primarily driven by its operational efficiency in large-scale livestock facilities. Liquid disinfectants are inherently suited to high-throughput sanitation in modern animal production systems. Across the EU, most commercial poultry and swine farms use pressure washers, fogging systems, or automated sprayers that rely on ready-to-use liquid formulations, according to industry assessments. Powders require on-site dissolution, introducing variability in concentration and increasing labor time. The compatibility of liquid form animal disinfectants with digital dosing and monitoring technologies is further favouring the expansion of the liquid form segment in the European market. The integration of liquid disinfectants into smart farm systems enhances precision and compliance. According to the recent agricultural technology reviews from European universities, the adoption of IoT-enabled dosing pumps in new dairy facilities is growing as these can automatically mix concentrated liquids with water based on sensor-driven hygiene protocols.

The powder form segment is estimated to grow at a CAGR of 9.9% over the forecast period, owing to the cost and logistics advantages for small and remote farms. Powder disinfectants provide notable economic and operational flexibility for small-scale and geographically isolated livestock operations. In such settings, powder formulations offer extended shelf life, eliminate the need for temperature control, and reduce shipping weight by up to 80% compared to liquids. Furthermore, the renewed adoption of localized disinfection methods such as footbaths and equipment soaking is reinforcing the demand for powder-based products.

By Application Insights

The poultry segment was the leading performer in the European animal disinfectants market in 2025 by accountingfor 36.3% share. The growth of the poultry segment in the European market is mainly credited to the intensive biosecurity protocols driven by avian influenza outbreaks.

The poultry sector faces unparalleled disinfection demands due to recurrent highly pathogenic avian influenza epizootics. According to the World Organisation for Animal Health (WOAH), Europe recorded over two thousand poultry farm outbreaks between 2023 and early 2024, which is demanding for the mandatory multi-stage disinfection under EU Directive 2005/94/EC. All-in-all-out production systems and high turnover rates are further contributing to the growth of the poultry segment in the European market. Poultry operations predominantly use all-in-all-out management, as these can provide complete facility disinfection between flocks.

The aquaculture segment is predicted to grow at a CAGR of 13.8% over the forecast period in the European market due to the expansion of EU sustainable aquaculture under the farm-to-fork strategy.

The European Union’s Farm to Fork Strategy aims to promote a substantial increase in sustainable aquaculture production by 2030, which is driving investment in biosecurity infrastructure. According to the European Commission, EU aquaculture output was around 1.3 million metric tons in 2023, with salmon, sea bass, and trout farms expanding particularly in Northern Europe and the Mediterranean. Stringent regulations on antibiotic use in fish farming are also boosting the growth of the aquaculture segment in the European market. Antibiotic use in European aquaculture remains among the most restricted globally, creating reliance on preventive hygiene. According to the European Medicines Agency, antibiotic sales for food-producing aquatic species in the EU declined significantly between 2018 and 2023. In response, farms are increasingly adopting disinfection as a primary disease control tool. This regulatory and ecological convergence fuels the segmental growth.

COUNTRY LEVEL ANALYSIS

Germany Animal Disinfectants Market Analysis

Germany dominated the animal disinfectants market in 2024 by holding 20.9% of the regional market share. The dense concentration of industrial livestock operations and stringent biosecurity enforcement in Germany are majorly driving the German market growth. According to the Federal Statistical Office, Germany houses around 23 million pigs and nearly 100 million poultry birds, and creates a vast sanitation infrastructure. The Animal Health Act of Germany mandates documented disinfection after each animal movement, with non-compliance subject to significant penalties. According to the Federal Ministry of Food and Agriculture, most commercial farms use disinfectants approved under EU reference standards. Additionally, Germany leads in digital farm compliance, with thousands of livestock holdings utilizing digital platforms to log disinfection events in real time, supporting audit requirements under the Integrated Administration and Control System.

France Animal Disinfectants Market Analysis

France was the second-largest regional segment for the animal disinfectants market in Europe in 2024. The diverse livestock base and proactive response to avian influenza in France are primarily driving the French market growth. With around 142,000 poultry farms, which is the highest in the EU, France faces intense disinfection pressure, especially following widespread avian influenza outbreaks in 2023. The French government distributed large volumes of state-procured disinfectants to affected zones, prioritizing hydrogen peroxide and peroxyacetic acid formulations. France also enforces the “EcoAntibio” plan that links farm support programs to biosecurity compliance, including disinfectant usage documentation. According to FranceAgriMer, a majority of dairy and pig farms have submitted digital hygiene records to qualify for payments in recent years. This policy linkage between public funding and sanitation practice sustains consistent demand across production types.

Spain Animal Disinfectants Market Analysis

Spain accounted for a substantial share of the Europe animal disinfectants market in 2024. The large-scale intensive farming and vulnerability to African Swine Fever are driving the Spanish market growth. Spain hosts Europe’s largest pig herd, which is estimated at around 35 million animals and concentrated in Catalonia and Aragon, as per the Spanish Ministry of Agriculture. Following African swine fever detections in wild boar near the Portuguese border, Spain implemented compulsory vehicle disinfection measures at farm access points in 2023. The National Pig Federation noted a marked increase in disinfectant procurement by integrated producers that year. Spain also leads in poultry exports, requiring compliance with third-country standards that mandate residue-free sanitation. This dual pressure from disease threat and export hygiene fuels high-volume, high-frequency disinfectant use across its agro-industrial corridors and propels the Spanish market growth.

Netherlands Animal Disinfectants Market Analysis

The Netherlands is estimated to hold a prominent share of the European market over the forecast period due to its ultra-intensive livestock density and export-oriented biosecurity standards. Dutch farms export a significant share, which is estimated at over 70% of their animal products, and this demands disinfection protocols aligned with importing countries such as Japan and South Korea. The Netherlands Food and Consumer Product Safety Authority requires all export-certified farms to use disinfectants that meet OIE Terrestrial Manual standards, which emphasize virucidal efficacy. In recent years, the Dutch government has provided targeted funding support for the adoption of advanced disinfection and fogging systems in poultry farms, linking public health and export competitiveness.

Italy Animal Disinfectants Market Analysis

Italy is anticipated to account for a notable share of the European market over the forecast period due to the mix of small traditional farms and large northern dairy operations. Italy’s 3.8 million dairy cows, which are concentrated in Lombardy and Emilia-Romagna, are driving the demand for udder and milking equipment disinfectants. According to the Italian National Institute of Statistics, a majority of dairy farms implement post-milking teat disinfection, which is a practice mandated under EU Regulation 853/2004. Italy also faces recurring Salmonella outbreaks in pig farms, which prompted regional authorities in Veneto and other northern regions to promote lactic acid–based sanitation programs. Unlike Northern Europe, Italy’s market is fragmented, with over 250,000 small holdings relying on agricultural cooperatives for bulk disinfectant procurement. This cooperative distribution model, combined with EU rural development funds, sustains steady demand for animal disinfectants in Italy despite economic pressures on small farmers.

COMPETITIVE LANDSCAPE

The Europe Animal Disinfectants Market features a dual competitive structure comprising multinational chemical and animal health corporations alongside specialized regional formulators. Large players leverage regulatory expertise, global supply chains, and R&D capabilities to dominate high-end segments such as automated and organic-compliant disinfection. In contrast, local manufacturers compete on price and distribution agility, particularly in Southern and Eastern Europe, where small-scale farms predominate. The market is also witnessing vertical integration, with ingredient suppliers forming alliances with equipment makers to offer bundled sanitation solutions. Regulatory fragmentation across member states creates both barriers and opportunities, favoring companies with dedicated EU compliance teams.

KEY MARKET PLAYERS

A few of the market players in the Europe animal disinfectants market

- Zoetis (US)

- The Chemours Company (US)

- Nufarm Limited (US)

- The Dow Chemical Company (US)

- Neogen Corporation (US)

Top Players In The Market

- Neoprosan is a European specialist in organic compliant animal health solutions with a strong focus on lactic acid and peroxygen-based disinfectants. The company supplies products to over 30 countries globally, with a core emphasis on markets requiring residue-free sanitation for organic and antibiotic-reduced livestock systems. Neoprosan has deep integration into EU regulatory frameworks, holding certifications from Ecocert and Soil Association Certification. In 2023 and 2024, the company expanded its production capacity in Belgium to meet rising demand from Nordic and Alpine dairy cooperatives. It also launched a digital dosing guide platform that helps farmers comply with EU traceability requirements, with its position as a science-driven,sustainability-aligned supplier in both European and global organic supply chains.

- Anitox Corporation is a global leader in feed and facility biosecurity, with significant operations across Europe specializing in pathogen control for poultry and swine. The company’s proprietary Termin 8 and Synergize formulations are widely used in high biosecurity environments, including breeder farms and hatcheries. Anitox contributes to global standards through partnerships with the World Organisation for Animal Health and the European Food Safety Authority. Recently, it established a dedicated regulatory affairs unit in Brussels to accelerate biocidal product approvals under the EU BPR.

- Evonik Industries is a German multinational that supplies high-purity hydrogen peroxide and specialty quaternary ammonium compounds used in animal disinfectants across Europe and beyond. Through its Care Chemicals and Health Care segments, Evonik provides active ingredients to formulators and integrated animal health companies worldwide. The company leverages its chemical engineering expertise to develop stabilized, low-residue disinfectant precursors compliant with REACH and Biocidal Products Regulation.

Top Strategies Used By The Key Market Participants

Key players in the Europe Animal Disinfectants Market prioritize regulatory compliance by aligning formulations with the European Union Biocidal Products Regulation and organic certification standards. They invest in research and development to create biodegradable and residue-free chemistries that meet environmental safety thresholds. Strategic partnerships with veterinary associations and farming cooperatives enhance on-ground adoption and technical support. Companies also integrate their products with digital farm management systems to enable traceable and auditable disinfection protocols. Additionally, they expand production capacity in Central and Northern Europe to ensure supply chain resilience and respond swiftly to disease outbreaks.

MARKET SEGMENTATION

This research report on the European animal disinfectants market has been segmented and sub-segmented into the following categories.

By Type

- Hydrogen Peroxide

- Phenolic Acid

- Iodine

- Lactic Acid

- Others

By Form

- Powder

- Liquid

By Application

- poultry

- dairy cleaning

- swine

- equine

- dairy and ruminants

- aquaculture

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are animal disinfectants used for in livestock farming?

They eliminate harmful microorganisms to maintain hygienic animal housing conditions.

Why is biosecurity driving demand for animal disinfectants in Europe?

Farmers prioritize disease prevention to protect herd health and avoid production losses.

How do animal disinfectants differ from regular cleaning products?

They are specifically formulated to control pathogens common in animal environments.

Which livestock sectors use disinfectants most frequently in Europe?

Poultry, dairy, swine, and aquaculture operations rely heavily on routine disinfection.

Why are hygiene protocols becoming stricter on European farms?

Regulations emphasize preventive health measures to reduce disease outbreaks.

How do animal disinfectants support antibiotic reduction strategies?

Cleaner environments lower infection risks, reducing reliance on medicinal treatments.

What surfaces are commonly treated with animal disinfectants?

Floors, equipment, transport vehicles, feeding systems, and housing units require regular sanitation.

How does climate influence disinfectant usage across Europe?

Cold and humid conditions can increase pathogen survival, requiring frequent sanitation.

What role does farm automation play in disinfectant application?

Automated spraying systems ensure consistent coverage and labor efficiency.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com