Europe Anti Snoring Devices Market Size, Share, Trends & Growth Forecast By Device, Surgical Procedure and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Market Size, 2025

$0.41 BnMarket Estimate, 2026

$0.45 BnMarket Forecast, 2034

$1.04 BnCAGR, 2026–2034

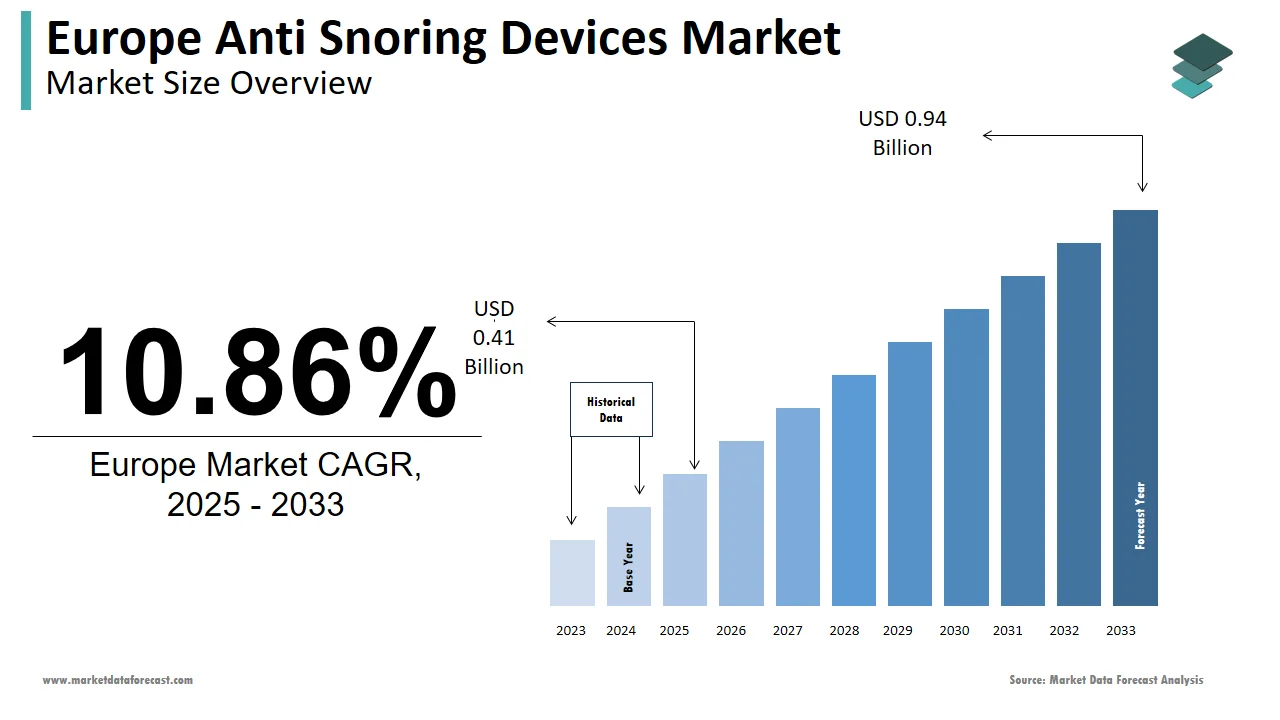

10.86%Europe Anti-Snoring Devices Market Size

The anti-snoring devices market size in Europe was valued at USD 0.41 billion in 2025. The European market is estimated to be worth USD 1.04 billion by 2034 from USD 0.45 billion in 2026, growing at a CAGR of 10.86% from 2026 to 2034.

Anti-snoring devices are medical and wellness-oriented products designed to mitigate or eliminate snoring by improving upper airway patency during sleep. In Europe, these include mandibular advancement devices, nasal dilators, positional therapy aids, tongue stabilizing devices, and smart wearable technologies. Unlike generic sleep aids, these interventions target the mechanical or anatomical origins of snoring, which is often a precursor to obstructive sleep apnea. According to sources, Snoring is common, with an estimated 45% of adults in general snoring occasionally and 25% snoring regularly. Also, Habitual snoring prevalence can range from 20% to 60% across different adult populations and studies. As per research, poor sleep quality contributes to a 22 percent higher risk of cardiovascular disease across the European region. Furthermore, National health surveys in Germany, France, and the UK consistently identify sleep disturbance as a top five non-clinical health concern. These epidemiological and behavioral indicators underscore a sustained and medically relevant demand for effective, accessible anti-snoring solutions across the continent.

MARKET DRIVERS

Escalating Prevalence of Sleep Disordered Breathing Linked to Lifestyle and Aging

The growing incidence of sleep disordered breathing, particularly among middle aged and older populations, is a key accelerator for the Europe anti-snoring devices market. Snoring is not merely a nuisance; it is a recognized symptom of upper airway resistance and a risk marker for obstructive sleep apnea. According to sources, the high prevalence and increasing recognition of sleep-related breathing disorders, driven by factors such as aging populations and rising obesity rates, is creating a significant and growing demand for diagnostic tools and treatment options across Europe. As per studies, a majority of the EU adult population is classified as overweight or obese, a persistent and rising trend which directly contributes to the increasing incidence of sleep apnea and related health complications, thereby expanding the potential patient pool for sleep disorder solutions. In parallel, Europe’s aging demographic, where a percentage of the population will be aged 65 or older by 2030, amplifies anatomical vulnerability to airway obstruction. National health registries reflect this burden. These structural health trends create a persistent clinical and consumer need for non-invasive interventions. Growing awareness of the correlation between untreated snoring and health risks, including hypertension, stroke, and daytime fatigue, is driving a greater need for easily obtainable anti-snoring devices in both clinical and retail markets.

Rising Consumer Preference for Non-Invasive and At Home Sleep Solutions

Regional consumers are increasingly favoring self-managed, and non-surgical approaches to sleep health, which propels the expansion of the Europe anti-snoring devices market. This is driven by convenience, cost considerations, and stigma avoidance associated with clinical sleep diagnostics. Unlike continuous positive airway pressure therapy, which requires prescription and nightly machine use, anti-snoring devices offer discreet, low barrier entry points for early intervention. According to a study, a share of adults who snore regularly would prefer to try an oral or nasal device before seeking medical consultation. This shift is reinforced by digital health trends: telehealth platforms in Germany and the Netherlands now offer virtual consultations for custom fitted mandibular devices, reducing wait times and improving accessibility. Retail dynamics also reflect this preference. Moreover, public health campaigns have normalized conversations around snoring, positioning it as a modifiable health behaviour rather than an inevitable part of aging. This cultural and behavioural transformation is accelerating adoption of over the counter and digitally guided anti-snoring solutions across urban and rural communities alike.

MARKET RESTRAINTS

Limited Reimbursement and Fragmented Healthcare Coverage Across EU Member States

The inconsistent and often absent reimbursement for these products under national health systems is one of the most significant constraints on the Europe anti-snoring devices market. While continuous positive airway pressure therapy for diagnosed sleep apnea is typically covered, anti-snoring devices, especially oral appliances and nasal aids, are frequently classified as wellness or cosmetic items rather than medical necessities. According to studies, several countries are working on frameworks for digital health and medical devices, only a handful have national value assessment and reimbursement policies in place, with differing mechanisms and conditions. In the remaining 24 member states, patients bear full out of pocket costs, which can exceed 300 euros for professionally fitted devices. This financial barrier suppresses uptake, particularly among older and lower income populations who are most affected by snoring. The absence of harmonized EU guidelines on device classification further fragments the market, discouraging manufacturers from investing in clinical validation needed for broader reimbursement eligibility. Market growth will remain constrained by issues of affordability and access as long as anti-snoring interventions are not systematically integrated into preventive care pathways.

Low Diagnostic Rates and Under Recognition of Snoring as a Medical Condition

Snoring is frequently dismissed as a benign social issue rather than a potential indicator of serious respiratory pathology, despite its prevalence, which leads to critically low diagnosis and intervention rates, and thereby inhibits the expansion of the Europe anti-snoring devices market. According to sources, a significant underdiagnosis problem exists regarding sleep-disordered breathing, with fewer than 15 percent of adults who habitually snore undergoing formal sleep assessment and less than 5 percent receiving a confirmed diagnosis. This under recognition stems from limited primary care training. Public awareness is similarly lacking. Moreover, demand for anti-snoring devices is driven more by partner complaints or social embarrassment than clinical guidance, limiting the use of evidence-based solutions. "The absence of systematic screening protocols results in many individuals using ineffective or unregulated products. This knowledge gap not only delays appropriate care but also erodes trust in legitimate medical devices when initial over the counter attempts fail, which creates a cycle of disengagement that hampers market development and public health outcomes alike.

MARKET OPPORTUNITIES

Integration with Digital Sleep Health Platforms and Telemedicine

The convergence of anti-snoring devices with digital health ecosystems creates a major opportunity for the growth of the Europe anti-snoring devices market. Smart anti-snoring wearables now incorporate sensors that track snoring intensity, sleep position, and respiratory patterns, syncing data with mobile applications to provide personalized feedback and behavioral nudges. Companies have partnered with telemedicine providers in Germany and the Netherlands to offer remote consultations, 3D mouth scanning for custom devices, and AI powered therapy adjustments, all without requiring in person sleep lab visits. Public health systems are beginning to recognize this potential. This digital shift not only enhances user adherence but also generates real world evidence that can support regulatory approvals and reimbursement applications, unlocking scalable, preventive care models across the region.

Expansion into Preventive and Occupational Health Programs

These devices are gaining traction within European occupational and corporate wellness initiatives as employers recognize the link between sleep quality and productivity, which in turn provides fresh prospects for the expansion of the Europe anti-snoring devices market. According to research, poor sleep contributes to an increase in workplace errors and a higher risk of occupational injury, particularly in transport, healthcare, and manufacturing sectors. In response, companies across Scandinavia and Germany have begun offering anti-snoring screening and device subsidies as part of employee health packages. National policies are reinforcing this trend. anti-snoring products, once for individuals, are now being adopted by companies as institutional health investments due to their cost-effectiveness in boosting employee productivity.

MARKET CHALLENGES

Regulatory Ambiguity in Device Classification Across EU Jurisdictions

The lack of harmonized regulatory classification creates uncertainty for manufacturers and delays market access, and thereby challenges the growth of the Europe anti-snoring devices market. Devices may be categorized as medical devices, wellness products, or personal accessories depending on the member state and claimed functionality. For instance, a mandibular advancement device deemed a Class IIa medical device in France might be treated as a general consumer product in Poland, affecting clinical evidence requirements and labeling rules. This fragmentation complicates pan European launches and increases compliance costs, companies often need separate regulatory dossiers for each major market. The implementation of the EU Medical Device Regulation has intensified scrutiny, yet guidance on borderline products like nasal dilators remains vague. Regulatory unpredictability and market entry barriers will continue to stifle innovation until the European Medicines Agency (EMA) or a unified body issues clear classification criteria.

Consumer Skepticism Due to Proliferation of Low Efficacy and Unverified Products

Significant reputational and adoption issues stemming from an influx of low quality, unverified products sold through e commerce and social media channels, which further constrains the expansion of the Europe anti-snoring devices market. Many of these items, such as magnetic nose clips, herbal patches, or generic chin straps, make exaggerated claims without clinical backing, leading to poor user experiences and eroded trust in legitimate solutions. According to a study, 61 percent of the top-selling products on major online marketplaces lacked CE certification or any demonstrable efficacy data. This market noise confuses consumers. Even certified products suffer from this spillover effect, as consumers struggle to differentiate between evidence-based interventions and pseudoscientific gadgets. The lack of standardized performance benchmarks or independent validation labels further exacerbates the problem. Coordinated action from regulators, the industry, and healthcare providers is essential. Without it, the category could be perceived as unreliable, which would undercut public health objectives and deter investment in real innovation. This would involve promoting certified solutions and penalizing deceptive marketing.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Surgical Procedures, and County. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Sleeping Well LLC., Apnea Sciences Corporation, Tomed Dr. Toussaint GMBH, AccuMED Corp, Fisher & Paykel Healthcare, Apnea Sciences Corporation, ImThera Medical Inc., ResMed Inc., SomnoMed, Sleep Well Enjoy Life, Ltd, Haleon, MEDiTAS Ltd, and Nasal Devices. |

SEGMENTAL ANALYSIS

By Product Type Insights

The mandibular advancement devices (MADs) segment held the leading share of 42.4% of the Europe anti-snoring devices market in 2024. The prominence of the MADs segment is attributed to its clinically validated efficacy, regulatory acceptance, and growing integration into mainstream sleep care pathways. MADs work by gently repositioning the lower jaw forward during sleep, thereby preventing airway collapse, a mechanism supported by robust evidence. National health systems reinforce this adoption. Germany’s statutory health insurers began partial reimbursement for dentist prescribed MADs in 2022, leading to an increase in fittings. Additionally, telehealth innovations have streamlined access, companies offer remote 3D intraoral scanning and direct shipping across the EU, which reduces reliance on in person visits. Consumer trust is further bolstered by CE certification under the Medical Device Regulation, which mandates biocompatibility and performance testing. These interconnected clinical, regulatory, and digital enablers solidify MADs as the cornerstone of non-invasive snoring management in Europe.

The EPAP devices segment is predicted to witness the highest CAGR of 12.8% from 2026 to 2034. These small nasal valves generate gentle back pressure during exhalation, stenting the airway open without electricity or bulky equipment. Their growth is fueled by superior portability, ease of use, and strong clinical validation in real world settings. Regulatory clarity has also accelerated adoption. EPAP products hold Class IIa medical device status across all EU member states, enabling pharmacy and e commerce distribution. Moreover, digital integration is enhancing adherence. Newer EPAP models sync with smartphone apps to track usage and snoring trends, appealing to tech savvy consumers. Emerging as a primary early intervention solution, particularly among younger and mobile European populations, EPAP offers the benefits of minimal side effects and eliminates the need for uncomfortable dental impressions.

By Surgical Procedures Insights

The Uvulopalatopharyngoplasty (UP3) segment remained the prominent segment in the anti-snoring devices market by accounting for a 38.4% share in 2024. The growth of the UP3 segment is fuelled by decades of clinical use, standardized training in otolaryngology residencies, and inclusion in national treatment guidelines for severe obstructive sleep apnea. This procedure involves excision of excess soft palate tissue, uvula, and sometimes tonsils to widen the airway. National health systems support its use. Long term outcome data also reinforces its position. Despite risks such as velopharyngeal insufficiency, its predictable anatomy-based approach and surgeon familiarity sustain its leadership in the surgical landscape.

The radiofrequency ablation (RFA) segment is estimated to register the fastest CAGR of 9.6% during the forecast period. RFA uses controlled thermal energy to shrink and stiffen soft palate or tongue base tissue, reducing vibration and collapse with minimal invasiveness. Its appeal lies in outpatient feasibility, rapid recovery, and repeatability, procedures take under 20 minutes under local anesthesia. Technological refinements have enhanced precision, modern impedance controlled RFA systems reduce collateral damage and improve safety profiles. Apart from these, cost efficiency plays a role. RFA procedures cost less than UP3, which makes them attractive in partially privatized systems. These advantages position RFA as a scalable, patient centric alternative in an era prioritizing minimally invasive care.

COUNTRY LEVEL ANALYSIS

Germany Anti-snoring Devices Market Analysis

Germany outperformed other countries in the Europe anti-snoring devices market and accounted for a 24.7% share in 2024. The domination of the German market is primarily driven by its advanced healthcare infrastructure, high diagnostic rates, and early adoption of integrated sleep solutions. The country performs significant number of sleep studies annually, the highest in Europe. This robust diagnostic base funnels patients toward evidence-based interventions, including mandibular devices and EPAP. Reimbursement policies further stimulate demand. Digital health integration is notable. Germany’s DiGA fast track approval system includes two anti-snoring apps that guide device use, enhancing adherence. Public awareness campaigns by the German Lung Foundation have also destigmatized snoring. These structural, financial, and educational factors establish Germany as the continent’s most mature and dynamic anti-snoring market.

United Kingdom Anti-Snoring Devices Market Analysis

The United Kingdom followed closely in the Europe anti-snoring devices market by capturing a share of 19.5% in 2024. The growth of the UK market is , characterized by strong consumer self-management trends and a hybrid public private healthcare system. The National Health Service focuses on providing CPAP therapy for diagnosed cases of sleep apnea, but the lack of NHS coverage for anti-snoring devices has led to a significant market for private and e-commerce alternatives. The Medicines and Healthcare products Regulatory Agency maintains clear classification of MADs and EPAP as Class IIa devices, ensuring product safety without excessive barriers. Telehealth platforms like Somnus and SnoreMD have flourished, offering virtual consultations and home impression kits. Furthermore, workplace wellness programs in sectors increasingly subsidize anti-snoring solutions following Health and Safety Executive guidance linking snoring to fatigue related risk. This blend of regulatory clarity, digital innovation, and occupational health integration sustains the UK’s leading role.

France Anti-Snoring Devices Market Analysis

France is steadily growing in the Europe anti-snoring devices market, with strong physician gatekeeping and public health emphasis on preventive care. The French National Authority for Health includes custom MADs in its official treatment algorithm for mild obstructive sleep apnea, ensuring full reimbursement when fitted by certified stomatologists. Snoring is increasingly addressed in primary care. General practitioners use standardized screening tools like the Epworth Sleepiness Scale during routine visits. Consumer behavior also supports growth. Apart from these, France leads in surgical innovation, with RFA and pillar implant procedures growing rapidly in private clinics across Paris and Lyon. This synergy of policy driven access, clinical integration, and patient trust underpins France’s consistent market position.

Italy Anti-Snoring Devices Market Analysis

Italy expanded moderately in the European anti-snoring devices market due to its aging population and rising obesity rates that amplify snoring prevalence. Private healthcare spending on sleep solutions expanded, despite ongoing limitations in public reimbursement. ENT specialists in northern regions like Lombardy and Emilia Romagna have pioneered hybrid approaches, combining MADs with positional therapy for optimal outcomes. Consumer awareness is also rising. E-commerce plays a critical role. Online sales of CE-marked anti-snoring devices increased. Italy's healthcare sector is becoming a more dynamic market for medical devices and surgical solutions, driven by increased regional autonomy in healthcare management and stronger patient advocacy.

Netherlands Anti-Snoring Devices Market Analysis

The Netherlands is anticipated to grow in the Europe anti-snoring devices market between 2025 and 2033 owing to its integrated care models and leadership in digital sleep health. The Dutch Healthcare Authority mandates multidisciplinary sleep clinics that include dentists ENTs and pulmonologists, ensuring holistic evaluation before device prescription. Reimbursement is progressive, basic health insurance covers MADs for patients. Innovation thrives in this ecosystem. Dutch startups pioneered position control wearables now adopted across Europe. Public awareness is high. This combination of coordinated care, insurance alignment, and homegrown innovation solidifies the Netherlands’ position as a forward-looking market.

COMPETITIVE LANDSCAPE

The Europe anti-snoring devices market features a multi tiered competitive landscape comprising global medical device companies specialist oral appliance manufacturers and consumer health brands. Competition is shaped less by price and more by clinical credibility regulatory status digital integration and professional endorsement. Established players like ResMed and SomnoMed dominate the medical segment with CE certified Class IIa devices supported by robust clinical data while consumer brands such as Haleon lead in the wellness space through retail reach and brand familiarity. Emerging startups are introducing smart wearables and AI driven solutions but face challenges in clinical validation and regulatory approval. The implementation of the EU Medical Device Regulation has raised quality and safety standards increasing barriers to entry but also strengthening trust in certified products. Collaboration between device makers healthcare providers and payers is becoming essential to navigate reimbursement complexities and demonstrate health economic value. This evolving ecosystem fosters innovation while prioritizing patient safety and evidence based outcomes.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe anti-snoring devices market include

- Sleeping Well LLC

- Apnea Sciences Corporation

- Tomed Dr. Toussaint GMBH

- AccuMED Corp

- Fisher & Paykel Healthcare

- ImThera Medical Inc.

- ResMed Inc.

- SomnoMed

- Sleep Well Enjoy Life, Ltd

- Haleon

- MEDiTAS Ltd

- Nasal Devices

TOP PLAYERS IN THE MARKET

- ResMed is a global leader in sleep and respiratory care with a significant footprint in the Europe anti-snoring devices market through its non CPAP solutions including nasal EPAP products like Theravent and SnoreRx. The company leverages its clinical credibility and extensive distribution network to offer medically validated alternatives for primary snoring. It also expanded reimbursement documentation support in Germany and France to facilitate insurance coverage. These initiatives reinforce ResMed’s strategy of embedding anti-snoring solutions within broader sleep health pathways while maintaining scientific rigor and regulatory compliance across the region.

- Haleon plays a distinctive role in the Europe anti-snoring market through its well known over the counter brands such as Breathe Right nasal strips. The company capitalizes on high brand recognition consumer trust and extensive retail presence in pharmacies and supermarkets across Western and Southern Europe. In recent years Haleon has invested in clinical studies to substantiate the airflow benefits of its external nasal dilators and launched refreshed packaging with clearer usage guidance. It also partnered with European sleep foundations to support public awareness campaigns linking nasal congestion to snoring. Haleon establishes a new market position for its products by defining them as accessible entry points that merge wellness principles with medical solutions.

- SomnoMed is a specialist in custom fitted mandibular advancement devices with deep clinical roots and a strong presence in European dental and sleep clinics. The company’s flagship SomnoDent line is prescribed by sleep dentists in multiple European countries and is known for its titratable design and high patient compliance. It also collaborated with European sleep societies to develop standardized training modules for dentists on oral appliance therapy. These actions strengthen SomnoMed’s position as a clinical partner of choice and support the professionalization of anti-snoring care across Europe.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe anti-snoring devices market focus on clinical validation through peer-reviewed studies to differentiate their products and support regulatory and reimbursement efforts. They invest in digital health integration by linking devices to mobile apps and telehealth platforms to improve user adherence and collect real-world evidence. Companies pursue strategic partnerships with healthcare professionals, including dentists, ENTs, and sleep physicians, to embed products into clinical care pathways. Brand building through public health collaborations and consumer education campaigns helps destigmatize snoring and drive early intervention. Apart from these, they expand product portfolios to include both medical-grade and over-the-counter options, catering to diverse user needs and access levels. Regulatory compliance under the EU Medical Device Regulation remains a priority, ensuring consistent CE certification across markets. These strategies collectively enhance credibility, accessibility, and long-term market sustainability.

MARKET SEGMENTATION

This Europe anti-snoring devices market research report is segmented and sub-segmented into the following categories.

By Product Type

- Mandibular Advancement Devices (MADs)

- Tongue Retaining Devices (TRD)

- Nasal Dilator

- Chin Strap

- Position Control

- Pillow

- Tongue Stabilizing Device (TSD)

- EPAP

By Surgical Procedures

- Uvulopalatopharyngoplasty (UP3)

- Laser-Assisted Uvula Palatoplasty (LAUP)

- Radiofrequency Ablation (RFA)

- Sclerotherapy

- Pillar

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving growth in the europe anti-snoring devices market?

Growth in the europe anti-snoring devices market is driven by rising awareness of snoring health impacts, aging populations, obesity, and lifestyle factors

2. Which product types dominate the europe anti-snoring devices market?

Oral appliances like mandibular advancement devices dominate the europe anti-snoring devices market due to comfort and effectiveness

3. How does technology influence the europe anti-snoring devices market?

Technological advances such as smart devices and telehealth support user adherence and convenience in the europe anti-snoring devices market

4. Which regions lead the europe anti-snoring devices market?

Western and Northern Europe lead the europe anti-snoring devices market with higher awareness and better healthcare accessibility

5. How important is e-commerce in the europe anti-snoring devices market?

E-commerce growth boosts accessibility and convenience, significantly expanding the europe anti-snoring devices market

6. What role does the aging population play in the europe anti-snoring devices market?

An aging population with increased sleep disorders drives demand for user-friendly anti-snoring devices in the europe market

7. How do lifestyle factors affect the europe anti-snoring devices market?

Sedentary lifestyles, obesity, and alcohol use contribute to higher snoring prevalence, fueling the europe anti-snoring devices market growth

8. What are the challenges in the europe anti-snoring devices market?

Challenges include patient adherence, product comfort, regulatory differences across europe, and limited awareness in some regions

9. What are the main distribution channels in the europe anti-snoring devices market?

Retail pharmacies and online stores are the main distribution channels for the europe anti-snoring devices market

10. How do clinical applications influence the europe anti-snoring devices market?

Clinical usage grows due to professional recommendations and diagnostics, improving patient outcomes in the europe anti-snoring devices market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com