Europe Apiculture Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Product, Application, And By Region (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU), Industry Analysis Forecast From (2025 to 2033)

Europe Apiculture Market Size

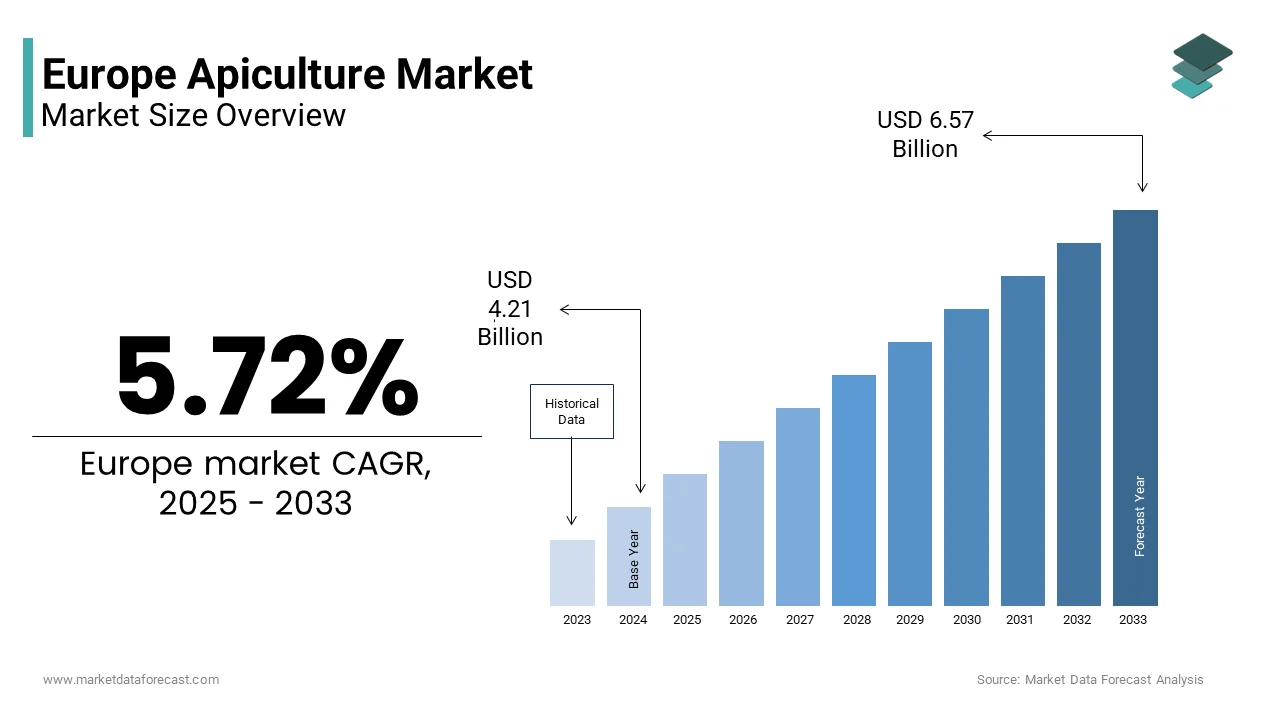

The European apiculture market was valued at USD 3.98 billion in 2024 and is anticipated to reach USD 4.21 billion in 2025 and USD 6.57 billion by 2033, estimated to grow at a CAGR of 5.72% during the forecast period from 2025 to 2033.

Apiculture includes the scientific and traditional practice of beekeeping,g focused on honey production, pollination services,s and the sustainable management of Apis mellifera populations. Beyond honey, ey the sector generates bees, wax,olis royal jelly, and venom,m all valued in food, cosmetics, and complementary medicine. According to the European Commission, around 80% of crop and wild-flowering plant species in the EU depend on animal pollination, which indicates the ecological importance of honeybees. As per Eurostat, there were approximately 18 million managed honeybee colonies across the EU in 2024, with significant concentrations in Spain, Romania, and Greece. According to the European Commission's estimations, insect pollination contributes over €15 billion annually to EU agricultural output, highlighting apiculture’s economic and environmental centrality. Recent policy frameworks, including the EU Pollinators Initiative and the Common Agricultural Policy’s eco-schemes, have elevated bee health as a biodiversity priority. Die Europäische Kommission+1. Despite these efforts, colony losses remain a concern, with the European and Mediterranean Plant Protection Organization reporting average annual winter mortality rates of 20–30% in several member states. This complex interplay of ecological service, agricultural dependency, and environmental vulnerability justifies the definition of the contemporary Europe apiculture market as both strategically vital and environmentally fragile.

MARKET DRIVERS

Rising Consumer Demand for Natural and Traceable Apiary Products

European consumers increasingly prioritize transparency, authenticity,y and natural origin in food and wellness products, which is directly fuelling premiumization in the apiculture sector and is one of the key factors propelling the European apiculture market growth. According to the European Commission’s 2024 Consumer Food Insights Survey, 68% of EU citizens actively seek products with short ingredient lists and clear geographic provenance, with raw honey and beeswax among the fastest-growing natural categories. This shift has elevated demand for single-origin certified organic and monofloral honeys, particularly in Germany, France,ce and the Nordic countries where clean label expectations are strongest. As per the International Federation of Organic Agriculture Movements, over 420,000 hectares of EU farmland were under organic apiculture management in 2023, a 12% increase from 2021. Retailers like EDEKA in Germany and Carrefour in France now dedicate exclusive shelf space to traceable honey with QR codes linking to hive location, harvest date, and pollination flora. Furthermore, the European Cosmetic Regulation EC 1223/2009 encourages the use of natural bee derivatives in personal care, driving demand for ethically sourced propolis and royal jelly. This consumer-led revaluation of apiary products as premium natural commodities has incentivized small-scale beekeepers to adopt certification and digital traceability systems, thereby reinforcing market differentiation and value creation beyond commodity pricing.

Policy Support for Pollinator Conservation and Sustainable Agriculture

The European Union has institutionalized pollinator protection as a pillar of its biodiversity and food security strategy, thereby creating structural support for apiculture, which is also contributing to the apiculture market expansion in Europe. The EU Pollinators Initiative,tive launched in 2018, mandates member states to monitor bee health, reduce pesticide risks, and restore pollinator habitats. As per the European Environment Agency, 24 out of 27 EU countries have now integrated pollinator action plans into their National Biodiversity Strategies. According to the European Commission, the Common Agricultural Policy 2023–2027 allocates direct payments to farmers who maintain beehives or establish flowering buffer strips with over 1.2 million hectares of agri‑environmental flower margins established by 2024. Additionally, the Sustainable Use of Pesticides Regulation restricts neonicotinoid use, a measure directly linked to improved colony survival rates. In Sweden and the Netherlands,therlands national bee health programs provide free hive inspections and pathogen screening to registered beekeepers, as noted by the European and Mediterranean Plant Protection Organization. These regulatory and financial instruments not only mitigate environmental threats but also professionalize apiculture by linking stewardship to income support. This policy ecosystem transforms beekeeping from a marginal activity into a recognized component of ecological riculture, enhancing its economic viability and societal recognition.

MARKET RESTRAINTS

Persistent High Colony Mortality Due to Pathogens and Parasites

Varroa destructor mite infestations combined with viral co-infections represent the most severe biological threat to European apiculture, causing unsustainable colony losses, which is a major restraint to the European apiculture market growth. According to the European and Mediterranean Plant Protection Organization, average winter colony mortality across the EU reached 27% in 202,3 with peaks of 45% in parts of Belgium and northern Italy. The Varroa mite weakens bees by feeding on their fat bodies and transmitting deformed wing virus, which impairs flight and foraging. As per the Joint Research Centre of the European Commission, over 90% of non-treated hives collapse within 2 years, rs highlighting the parasite’s lethality. Despite available miticides, resistance is emerging, ng and organic acids like oxalic and formic acid require precise application timing that many small-scale beekeepers lack the training to execute. Climate variability further complicates treatment windows with unseasonal warm spells triggering brood rearing outside standard protocols. The absence of a standardized EU-wide surveillance system means infestations often go undetected until collapse. This biological fragility undermines honey yields, pollination reliability,y and keeper livelihoods, ds creating a persistent barrier to sectoral stability and scalability.

Fragmented Regulatory Framework for Honey Authenticity and Labeling

EU-wide food safety standards, national disparities in honey composition enforcement, and geographical indication protection create market distortions and consumer mistrust, which further hamper the apiculture market growth in Europe. According to the European Commission’s 2023 Food Fraud Report, honey was the third most adulterated food product in the EU, with 19% of tested samples containing added sugar,,s syrups, or non-declared botanical sources. While Regulation EC 1223/2008 defines honey as a natural product without additives, enforcement varies significantly. Romania and Bulgaria report adulteration rates above 30%, whereas Germany and Austria detect fewer than 8% due to rigorous laboratory screening. The lack of harmonized pollen analysis protocols enables mislabelling of origin with honey from non-EU countries, es often blended and relabelled as European. As per the European Consumer Organisation (BEUC), 61% of consumers doubt the authenticity of supermarket honey, particularly in private label segments. These inconsistencies erode premium pricing for genuine local producers and discourage investment in traceability. Although the EU has proposed stricter DNA and isotopic testing standards, their implementation remains voluntary, delaying a unified authenticity regime. This regulatory fragmentation sustains unfair competition and inhibits consumer confidence essential for market growth.

MARKET OPPORTUNITIES

Expansion of Urban and Community-Based Beekeeping Initiatives

Cities across Europe are emerging as unexpected hubs for apiculture driven by municipal sustainability agendas and citizen science movements, which is a potential opportunity for the European apiculture market. According to the European Urban Beekeeping Network, over 120 cities, including Paris, Berlin, in Copenh a, gen anBarcelonana now host formal urban beekeeping programs with more than 25,000 hives installed on rroofsftops public gardens, and institutional campuses as of 2024. These initiatives servea dual purpose,s enhancing local pollination for urban agriculture while raising public awareness about biodiversity loss. The City of Paris alone maintains 600 hives managed by trained municipal beekeepers pr, producing over 1,000 kilograms of honey annually for civic use. As per the Urban Sustainability Platform funded by the European Investment Bank, urban hives have demonstrated 15–20% higher honey yields than rural counterparts due to diverse floral resources and lower pesticide exposure. Universities and schools increasingly integrate apiary modules into environmentalcurriculaula fostering intergenerational knowledge transfer. This re-localization of apiculture not only diversifies production geographies but also cultivates a new generation of bee stewards, rds creating resilient micro ecosystems that buffer against rural colony collapse and strengthen the social license of beekeeping.

Development of Apitherapy High-Value Bee-Derivedived Ingredients

Beyond honey, the therapeutic and cosmetic applications of bee products are unlocking premium value chains for European apiculturists, which is another notable opportunity for the European apiculture market. Propolis, royal jell,,y and bee venom are increasingly incorporated into evidence-based complementary medicine,,erdermatologyy and anti-aging formulations due to their antimicrobial,ial antioxidan,t,, and anti-inflammatory properties. According to the European Cosmetics Association, natural bee derivatives featured in 28% of new skincare launches in Western Europe in 2023, a 40% increase from 2020. Clinical research is advancing legitimacy; a 2024 multicenter trial published by Charité Berlin demonstrated that topical propolis reduced healing time in minor burns by 32% compared to standard care. In Romania and Bulgariaa specialized apiaries now produmedical-gradeade royal jelly under Good Manufacturing Practice certification for export to German and Swiss nutraceutical firms. As per the European Traditional Herbal Medicinal Products Directive, standardized bee venom extracts are approved for osteoarthritis pain management in 14 EU countries. These high-margin applications incentivize beekeepers to diversify income streams beyond volatile honey markets while promoting hive health through gentle harvesting protocols. This valorisation of secondary bee products transforms apiculture into a multifunctional bioeconomy with significant export potential.

MARKET CHALLENGES

Climate-Induced Floral Resource Instability

Erratic weather patterns and shifting phenology are disrupting the synchrony between bee foraging cycles and floral bloom periods across Europe, which is challenging the apiculture market growth in Europe. According to the Copernicus Climate Change Service, the growing season in Western and Central Europe advanced by 8–12 days between 2000 and 2023, causing mismatches where bees emerge before key nectar sources flower. In 202,2 a severe drought across Southern Europe reduced lavender and sunflower yields by 35–50% as per the Joint Research Centre, directly diminishing honey production in France and Spain. Conversely, ly intense rainfall in spring delays bloom and washes away nec, ta,r compromising colony nutrition during critical buildup phases. As per the European Environment Agency, over 60% of EU regions now experience at least climate-relatedated forage stress event annually, impacting honey quality and quantity. Beekeepers are forced to supplement with sugar syrup,s, which lowers honey authenticity and increases operational costs. The unpredictability of nectar flows also complicates planning for migratory beekeeping, a key practice for pollination contracts. This ecological volatility undermines the foundational resource base of apiculture,e threatening both economic viability and pollination reliability.

Shortage of Skilled Beekeepers and Knowledge Transfer Gaps

Aging demographics and insufficient vocational training are creating a critical human capital deficit in European apiculture, which is further challenging the apiculture market expansion in Europe. According to Eurostat, the median age of EU beekeepers exceeds 58 years,, rs with fewer than 12% under the age of 35. In countries like Germany and the Netherlands, over 40% of registered beekeepers are expected to retire by 2030 as per national agricultural ministries. Traditional knowledge on swarm management, disease identification, and seasonal hive care is often informal and at risk of being lost. Although digital platforms and national beekeeping associations offer ccoursess uptake is limited by rural connectivity and language barriers. As per the European Federation of Beekeepers Associations, only 9 out of 27 EU countries have integrated apiculture into agricultural vocational curricula. This skills gap reduces adaptive capacity to emerging threats like Asian hornet invasions or new pathogens. Young entrants often lack mmentorsip leading to high early attrition rates. Without structured knowledge transfer mechanisms, the sector risks declining technical proficiency,ncy reduced hive productivity, and weakened resilience to environmental and biological stressors, undermining its long-term sustainability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.72% |

| Segments Covered | By Product, Application, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic ,& est of Europe |

| Market Leaders Profiled | Betterbee Inc. (U.S.), Miller’s Honey Company (U.S.), Dabur India Limited (India), Shangdong Bokang Apiculture Co. Ltd. (China), Beehive Botanicals Inc. (U.S.). |

SEGMENTAL ANALYSIS

By Product Insights

The honey segment was tthe largestand accounted for 65.7% of the European apiculture market share in 2024. The leading position of the honey segment in the European market is primarily attributed to its dual role as a traditional food commodity and a culturally embedded household staple across the continent. Annual per capita honey consumption in the EU averages 1.2 kilograms, with significantly higher intake in countries like Germany and Greece, where it is used in daily cooking, baking, and wellness rituals. As per Eurostat, the EU produced 275,000 metric tons of honey in 2023, yet imported an additional 220,000 metric tons to meet demand, underscoring structural supply deficits. Consumer preference for locally sourced, unprocessed honey has intensified,d with 59% of European shoppers willing to pay a 30% premium for traceable monofloral varieties, according to the European Consumer Organisation BEUC. National quality schemes such as France’s Label Rouge and Italy’s DOP certification further reinforce authenticity and command higher prices. The enduring culinary, medicinal, and symbolic value ofhoneye,,y combined with policy efforts to combat adulteration, ensures its continued centrality in the apiculture value chain.

The beeswax segment is fastest-growingwing product segment in the Europe apiculture market and is estimated to register a CAGR of 8.14% over the forecast period in this regional market. Factors such as the surging demand from the natural cosmetics and premium candle industries seeking sustainable alternatives to paraffin and synthetic polymers are majorly fuelling the growth of the beeswax segment in the European market. As per the European Cosmetics Association, natural beeswax was featured in 34% of new skincare and lip care launches in Western Europe in 202,3 owing to its emollient texture, biodegradability, and regulatory acceptance under EU cosmetic regulations. The artisanal candle sector has also embraced beeswax for its clean burn and subtle honey aroma, with European producers reporting a 45% increase in B2B orders from luxury home fragrance brands since 2021. Additionally, the EU Circular Economy Action Plan promotes bio‑based materials in packaging and coatings, creating new industrial applications. Unlike honey, beeswax production requires no additional forage resources as it is a hive byproduct,t thus offering beekeepers incremental revenue without expanding colony numbers. Thilow-inputut, high-value proposition, alongside strong environmental credentials,s positions beeswax as Europe’s most dynamically expanding apicultural output.

By Application Insights

The food and beverages segment held 75.8% of the European apiculture market share in 2024. Honey remains the primary driver used not only as a sweetener but also as a functional ingredient in bakery, confectionery, dairy, and beverage formulations for its moisture retention, antimicrobial properties, and flavor complexity. As per FoodDrinkEurope, over 12,000 food products launched in the EU in 2023 listed honey as a ingredientedie,nt with bakery items alone accounting for 38% of these introductions. Traditional culinary practices further entrench usage; for example, Greek households consume an average of 2.4 kilograms of honey per capita annually,lly primarily in breakfast and dessert applications as noted by the Hellenic Beekeepers Association. The clean label movement has amplified demand as manufacturers replace high fructose corn syrup and artificial sweeteners with natural honey. Retailers like Aldi and Lidl have introduced exclusive regional honey lines sourced directly from local cooperatives, reinforcing origin authenticity. This deep integration into both industrial and household food systems ensures the food and beverages segment remains the foundational application pillar of European apiculture.

The cosmetics segment is likely to register the highest CAGR of 9.14% over the forecast period in this regional market, due to the consumer demand for natural, sustainable, and bioactive ingredients in personal care formulations. Beeswax, propolis, and royal jelly are increasingly incorporated into lip balms, creams, and serums for their emulsifying, humectant, and anti‑aging properties. As per a 2024 consumer survey by Mintel, 71% of European beauty buyers consider bee‑derived ingredients a marker of product authenticity and efficacy. Regulatory alignment further supports adoption; the EU Cosmetic Regulation EC 1223/2009 permits these substances without synthetic modification, enhancing their clean label appeal. Major b brandsuding L’Oréal, Weleda, and Dr Hauschka, haveexpanded apiary-sourcedd ingredient portfolios with traceability certifications from hive to jar. Moreover, the European Green Deal’s emphasis on bioeconomy encourages formulation shifts toward renewable inputs. Unlike food applications, cosmetics offer higher margins and lower volume requirements, enabling small-scale beekeepers to access premium B2B markets. This convergence of regulatory support, consumer preference, and economic incentive propels cosmetics as the most rapidly advancing apiculture application frontier.

REGIONAL ANALYSIS

Spain Apiculture Market Analysis

Spain dominated the apiculture market in Europe in 2024 with 20.2% of the European market share. The country hosts more than 2.8 million managed hives, the largest colony count in the EU, supported by diverse Mediterranean flora, including orange, lavender, and rosemary, which enable year‑round honey flows. As per the National Statistics Institute, Spain produced more than 75,000 metric tons of honey in 2023, making it Europe’s top honey producer. The sector is highly professionalized, with cooperative structures like COAG and ASAJA facilitating export to France, Germany, and Italy. Government support through the Common Agricultural Policy includes direct payments for hive maintenance and pollination services, particularly in almond and fruit‑growing regions like Andalusia. Additionally, Spain’s favorable climate allows migratory beekeeping across altitudinal gradients, ensuring continuous forage access. According to the Spanish Ministry of Agriculture, recent investments in authenticity testing infrastructure have reduced adulteration and strengthened premium positioning for Denominación de Origen honeys such as Miel de Granada. This combination of scale, biodiversity, policy support, and market integration cements Spain’s dominant role.

Germany Apiculture Market Analysis

Germany had thesecond-largestt share of the Europe apiculture market in 2024. Despite temperate climate limitations, Germany exhibits the highest per capita honey consumption in the EU at 1.8 kilograms annually, as noted by the German Beekeepers Association. The market is characterized by strong demand for organic and regional honeys, with more than 60% of retail sales commanded by locally branded products. According to the German Beekeepers Association, Germany hosts more than 120,000 hobby and professional beekeepers. These producers benefit from rigorous quality controls under the German Honey Ordinance, which mandates strict pollen analysis and moisture limits. Urban beekeeping has flourished in cities like Berlin and Munich with municipal programs installing hives on public buildings and corporate campuses. Furthermore, Germany is a major importer of bulk honey, primarily from Eastern Europe, which it refines and repackages under premium private labels. Consumer awareness campaigns by organizations like Stiftung Warentest have heightened scrutiny on origin and purity, driving traceability innovation. These demand‑side sophistication and regulatory rigor sustain Germany’s high‑value apiculture ecosystem.

France Apiculture Market Analysis

France accounted for a prominent share of the European apiculture market in 2024. The country is renowned for its terroir‑driven honeys such as Lavender de Provence and Châtaignier du Morvan, which benefit from Protected Geographical Indication status,s ensuring premium pricing and export appeal. As per the National Federation of Beekeepers, France maintains approximately 1.6 million hives and produces around 25,000 metric tons of honey annually. The sector faces challenges from neonicotinoid legacy and Varroa pressure, re yet it benefits from robust institutional support, ort including the National Apiculture Program, which funds research, hive health monitoring, and young beekeeper training. According to the French Ministry of Ecological Transition, 85% of new beekeepers under age 40 receive startup grants and technical mentorship. France also leads in apitherapy with more than 200 certified centers using bee venom for inflammatory condition management. High culinary valuation of honey in patisserie and gastronomy further sustains domestic demand. This fusion of gastronomic heritage, scientific support, and quality branding underpins France’s influential market position.

Italy Apiculture Market Analysis

Italy is estimated to grow at a healthy CAGR in the European market during the forecast period. The country’s apiculture is distinguished by exceptional botanical diversity with more than 50 recognized monofloral honeys, including Acacia, Tiglio, and Eucalyptus, many protected under DOP and IGP schemes. As per the Italian Beekeepers Federation, Italy manages about 1.5 million hives and produces roughly 22,000 metric tons of honey annually, with significant output from Sicily and Tuscany. According to NielsenIQ, 67% of Italian households purchased raw, unfiltered honey directly from local producers in 2023. Italy is also a leader in beeswax valorization, supplying premium wax to cosmetics manufacturers in Switzerland and France. National initiatives like the Apilife project have introduced integrated pest management techniques, reducing chemical treatments by 40% since 2021. Despite challenges from Asian hornet invasions, Italy’s emphasis on quality craftsmanship and direct market linkages ensures resilient and differentiated apicultural output.

Greece Apiculture Market Analysis

Greece is anticipated to account for a considerable share of the European apiculture market during the forecast period. Greece boasts one of the highest bee densities per square kilometer in Europe, supported by extensive maquis shrubland and wild thyme fields that yield distinctive honeys like Thyme and Pine honeydew. As per the Hellenic Beekeepers Association, Greece produces more than 20,000 metric tons of honey annually, with per capita consumption reaching 2.4 kilograms, the highest in the EU. Much of the sector remains artisanal, with small‑scale beekeepers practicing transhumance across mountainous and island terrains to optimize floral access. According to the Aristotle University of Thessaloniki, a 2023 study confirmed polyphenol levels in Greek honey 30% above EU averages. Export demand from Germany and the Netherlands for raw, unprocessed batches continues to grow. Government programs under the Rural Development Program offer subsidies for organic certification and modern hive equipment. This blend of unique ecology, traditional knowledge, and biochemical quality secures Greece’s niche as a premium producer in the European apiculture landscape.

KEY MARKET PLAYERS

These are the market players that are dominating the Europe apiculture market.

- Betterbee Inc. (U.S.)

- Miller’s Honey Company (U.S.)

- Dabur India Limited (India)

- Shangdong Bokang Apiculture Co., Ltd. (China)

- Beehive Botanicals Inc. (U.S.)

MARKET SEGMENTATION

This research report on the European apiculture Market is segmented and sub-segmented into the following categories.

By-products

- beeswax

- honey

- live bees

- others

By Application

- agriculture

- food and beverages

- medical

- chemical

- paints

- cosmetics

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe apiculture market?

It involves the production of honey and other bee products, along with pollination services across Europe.

What is driving the Europe apiculture market growth?

Rising demand for natural, organic, and health-focused food products is driving market growth.

Which product dominates the Europe apiculture market?

Honey holds the largest market share due to its wide food and medicinal use.

How does organic food demand impact the market?

Growing preference for organic and chemical-free foods boosts demand for organic honey.

Which countries lead the Europe apiculture market?

Germany, Spain, France, Italy, and Poland are major contributors.

Why is apiculture important for European agriculture?

Bees support crop pollination, improving yields and agricultural sustainability.

What are the key challenges in the Europe apiculture market?

Bee diseases, pesticide exposure, climate change, and rising production costs.

How do regulations affect the market?

Strict EU quality and labeling rules ensure safety but raise compliance costs.

Do honey imports affect European producers?

Yes, low-cost imports create pricing pressure on local beekeepers.

What opportunities exist in the Europe apiculture market?

Growth in organic honey, premium varieties, and cosmetic and nutraceutical uses.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com