Europe Artificial Jewellery Market Size, Share, Trends, and Growth Analysis Report, Segmented by Material, Type, Distribution Channel, End User, and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

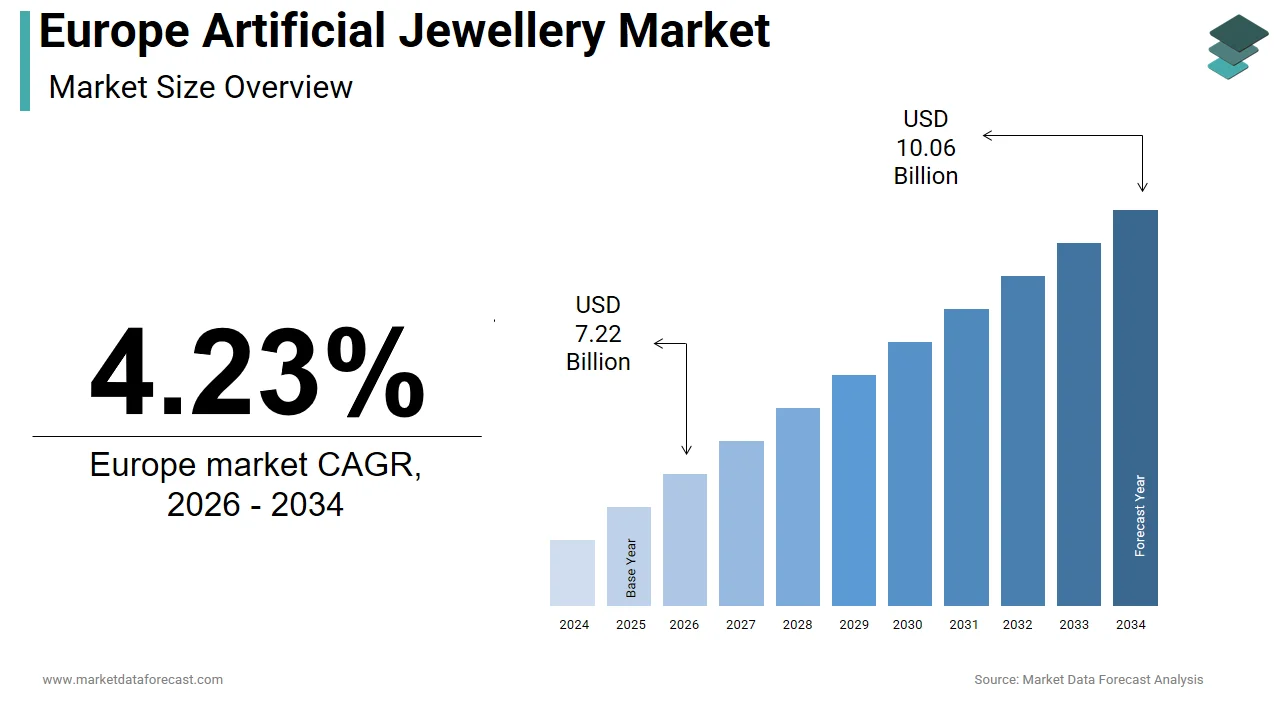

$6.93 BnMarket Estimate, 2026

$7.22 BnMarket Forecast, 2034

$10.06 BnCAGR, 2026–2034

4.23%Europe Artificial Jewellery Market Report Summary

The Europe artificial jewellery market was valued at USD 6.93 billion in 2025, is estimated to reach USD 7.22 billion in 2026, and is projected to reach USD 10.06 billion by 2034, growing at a CAGR of 4.23% from 2026 to 2034. Market growth is driven by increasing demand for affordable fashion accessories, rising influence of fast fashion trends, and growing consumer preference for versatile and stylish jewellery. Artificial jewellery offers cost-effective alternatives to precious jewellery while enabling frequent style changes. The expansion of e-commerce platforms, celebrity endorsements, and evolving fashion preferences are further supporting market growth across Europe.

Key Market Trends

- Rising demand for affordable and fashion-forward jewellery.

- Increasing influence of fast fashion and changing consumer trends.

- Growth of online retail and digital shopping platforms.

- Increasing popularity of customized and trendy accessories.

- Expansion of sustainable and eco-friendly jewellery options.

Segmental Insights

- Based on material, the metal segment dominated the Europe artificial jewellery market by capturing 58.4% share in 2025, driven by durability and aesthetic appeal.

- Based on type, the earrings segment led the market with 34.6% share in 2025, supported by high demand for versatile and everyday fashion accessories.

- Based on distribution channel, the retail stores segment held the largest share of 48.9% in 2025, driven by strong in-store consumer engagement and product visibility.

Regional Insights

The Europe artificial jewellery market is witnessing steady growth across major countries due to strong fashion culture and consumer demand.

- Italy led the regional market in 2025 with 22.8% share, supported by its strong fashion industry and design expertise.

- France followed with 19.8% share in 2025, driven by its global influence in luxury and fashion trends.

- Germany holds a significant position due to consumer preference for quality, durability, and functional design.

Competitive Landscape

The Europe artificial jewellery market is competitive, with the presence of both global fashion brands and regional jewellery manufacturers. Market players are focusing on design innovation, expanding product portfolios, and strengthening online and offline distribution channels. Fast fashion integration and brand collaborations are shaping competitive dynamics across the market.

Prominent companies operating in the Europe artificial jewellery market include Tanishq, Kalyan Jewellers, PC Jeweller, Malabar Gold and Diamonds, Swarovski, Chopard, Pandora, Zales, H&M Group, and Kay Jewelers.

Europe Artificial Jewellery Market Size

The size of the Europe artificial jewellery market was worth USD 6.93 billion in 2025. The regional market is anticipated to grow at a CAGR of 4.23% from 2026 to 2034, reaching USD 10.06 billion by 2034 from USD 7.22 billion in 2026.

The artificial jewellery is non-precious adornments crafted from base metals, alloys, glass, synthetic stones, and plastics, designed to mimic the aesthetic appeal of fine jewellery at accessible price points. The definition now extends beyond mere imitation to include artisanal craftsmanship, sustainable materials, and statement pieces that serve as primary elements of personal expression. The region boasts a robust manufacturing heritage, particularly in countries like Italy and France, where traditional techniques blend with modern production methods. According to Eurostat, the European Union recorded over 447 million inhabitants in 2024, providing a massive consumer base with varying disposable income levels that support both mass-market and premium costume jewellery segments. Furthermore, the rise of social media has transformed jewellery into a visual currency, with platforms like Instagram driving demand for photogenic accessories. As per the European Commission, the creative industries contribute significantly to the EU economy, with fashion and accessories playing a pivotal role in employment and cultural export.

MARKET DRIVERS

Proliferation of Fast Fashion and Trend Acceleration Cycles

The symbiotic relationship with the fast fashion industry, which has drastically accelerated trend cycles and normalized frequent accessory rotation, is driving the growth of Europe artificial jewellery market. European consumers, particularly Generation Z and Millennials, have adopted a mindset where jewellery is viewed as a disposable or semi-disposable commodity rather than a lifelong investment, mirroring the consumption patterns of ready-to-wear clothing. Data indicates that the average European consumer purchases clothing and accessories 60% more frequently than they did fifteen years ago, driven by the constant influx of new styles from retailers like Zara, H&M, and Mango, according to industry consumption studies. This rapid turnover necessitates a steady supply of affordable, trendy jewellery that complements specific outfits for short durations. Social media platforms amplify this effect, with viral trends lasting only a few weeks, compelling users to buy new pieces to stay relevant online. The ability of artificial jewellery manufacturers to replicate high-end designs quickly and at a fraction of the cost allows them to capitalize on these fleeting trends effectively. Consequently, the market thrives on volume and velocity, with brands releasing weekly collections to match the pace of fast fashion retailers by ensuring a continuous stream of revenue and maintaining high engagement levels among style-conscious demographics across the continent.

Rising Demand for Affordable Luxury and Personal Expression

The surging demand for affordable luxury and the use of accessories as a primary medium for personal expression amidst economic uncertainties is substantially propelling the growth of Europe artificial jewellery market. As inflation impacts disposable income across several European nations, consumers are increasingly opting for high-quality artificial jewellery that offers the aesthetic grandeur of precious metals and gemstones without the prohibitive costs. This shift is evident in the growing popularity of "democratic luxury," where brands offer premium finishes like gold plating and cubic zirconia that satisfy the desire for elegance. According to consumer confidence surveys conducted by the OECD, nearly 58% of European households have reduced spending on high-value items while maintaining or increasing expenditure on small indulgences like fashion accessories. Artificial jewellery allows individuals to curate diverse looks and express their unique identities without financial strain, fostering a culture of experimentation. The market has responded with elevated design standards, incorporating intricate detailing and hypoallergenic materials that rival fine jewellery.

MARKET RESTRAINTS

Stringent Regulatory Compliance Regarding Chemical Safety

The implementation of stringent regulatory frameworks concerning chemical safety and material composition is hampering the growth of Europe artificial jewellery market. The European Union enforces some of the world's toughest regulations under the Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) framework, which strictly limits the presence of hazardous substances such as nickel, lead, and cadmium in consumer products. Nickel allergy alone affects approximately 10 to 20% of the European population, prompting rigorous enforcement of release limits to protect public health according to the European Chemicals Agency. Compliance with these regulations requires extensive testing, certification, and supply chain transparency, imposing significant financial and administrative burdens on manufacturers, especially small and medium-sized enterprises. Non-compliance can result in severe penalties, product recalls, and reputational damage, deterring market entry and innovation. Additionally, the upcoming Digital Product Passport initiative will mandate detailed tracking of material origins and chemical compositions, further increasing operational complexity. These regulatory hurdles slow down time-to-market and restrict the use of certain cost-effective alloys, limiting the flexibility of designers and creating barriers for smaller players who lack the resources to navigate the complex legal landscape, thereby stifling overall market dynamism.

Perceived Low Durability and Quality Concerns

The pervasive perception of low durability and inferior quality associated with it is additionally hampering the growth of Europe artificial jewellery market. Unlike fine jewellery, many artificial pieces are prone to tarnishing, discoloration, and breakage after limited use, leading to consumer dissatisfaction and a reputation for disposability. Studies indicate that nearly 40% of European consumers hesitate to purchase artificial jewellery due to concerns about skin irritation and rapid degradation of the finish, as per consumer behavior analysis. This awareness is exacerbated by the prevalence of low-cost, mass-produced items that prioritize speed over craftsmanship, resulting in a saturated market filled with subpar products. The lack of standardized quality benchmarks across the broader non-luxury segment further confuses buyers, making it difficult to distinguish between high-quality costume pieces and cheap imitations. Consequently, brands struggle to build long-term relationships with customers who view these purchases as transient rather than valuable additions to their collection.

MARKET OPPORTUNITIES

Expansion of Sustainable and Eco-Friendly Jewellery Lines

The expansion of sustainable and eco-friendly jewellery lines to the growing environmental consciousness of European consumers is creating new opportunities for the growth of Europe's artificial jewellery market. As awareness of the fashion industry's ecological footprint intensifies, there is a burgeoning demand for accessories made from recycled metals, upcycled materials, and biodegradable components. The European Green Deal and the Circular Economy Action Plan have galvanized consumer interest in products that align with sustainability goals, creating a fertile ground for brands that prioritize ethical sourcing and production. Brands leveraging materials like recycled brass, ocean-recovered plastics, and lab-grown stones can tap into this lucrative niche, differentiating themselves from conventional competitors. Furthermore, the adoption of transparent supply chains and eco-certifications enhances brand credibility and trust. The opportunity extends to the development of rental and resale models for high-quality costume jewellery, promoting a circular economy that reduces waste.

Integration of Advanced E-Commerce and Augmented Reality Technologies

The integration of advanced e-commerce platforms and augmented reality (AR) technologies to enhance customer experience and drive sales conversion is additionally creating new opportunities for the growth of Europe's artificial jewellery market. With the region boasting high internet penetration and a tech-savvy population, digital channels offer immense potential for showcasing the visual appeal of jewellery. AR tools allow customers to virtually try on earrings, necklaces, and rings using their smartphone cameras, addressing the tactile limitation of online shopping and reducing return rates. This technology empowers consumers to make informed purchasing decisions from the comfort of their homes, expanding the reach of brands beyond physical store locations. Additionally, AI-driven personalization engines can analyze user preferences and browsing history to recommend tailored jewellery collections by enhancing engagement and average order value. The rise of social commerce, where purchases are made directly through social media platforms, further amplifies this opportunity.

MAJOR CHALLENGES

Intense Competition from Counterfeit and Unbranded Products

The proliferation of counterfeit and unbranded products with regard to integrity and profitability is one of the challenges for the growth of Europe artificial jewellery market. The low barrier to entry and high demand for trendy designs have led to an influx of illicit goods that mimic established brands at significantly lower prices, often compromising on quality and safety standards. The European Union Intellectual Property Office estimates that the fashion and accessories sector loses billions of euros annually due to counterfeiting, with artificial jewellery being a frequent target due to its high volume and visual nature. These fake products not only divert revenue from legitimate businesses but also damage brand reputation when consumers associate poor quality or allergic reactions with the original labels. Online marketplaces and social media platforms have exacerbated this issue by providing anonymous channels for counterfeiters to reach unsuspecting buyers across borders. According to customs enforcement data, seizures of counterfeit jewellery in Europe increased by 15% in the last year, highlighting the scale of the problem. Combating this illicit trade requires substantial investment in legal actions, authentication technologies, and consumer education, which strains resources, particularly for smaller independent designers.

Volatility in Raw Material Costs and Supply Chain Disruptions

The volatility in raw material costs and persistent supply chain disruptions that threaten the stability and margins are one of the challenges for the growth of Europe artificial jewellery market. The industry relies heavily on base metals such as copper, zinc, and aluminum, as well as synthetic stones and plating materials, whose prices are subject to fluctuation due to geopolitical tensions, energy costs, and global demand shifts. Recent global events have caused raw material prices to spike by up to 25%, squeezing profit margins for manufacturers who operate on thin margins and rely on competitive pricing, according to commodity market reports. Furthermore, the concentration of supply chains in specific regions makes the market vulnerable to logistical bottlenecks, trade restrictions, and labor shortages. Delays in the shipment of components can disrupt production schedules and lead to stockouts during peak sales periods, resulting in lost revenue and dissatisfied customers. The transition to sustainable materials introduces additional complexities, as the supply of certified recycled metals and ethically sourced stones is currently limited and inconsistent. Navigating this volatile landscape requires agile supply chain management and strategic sourcing, which remains a daunting task for many market participants, particularly smaller entities lacking the leverage to negotiate favorable terms or absorb cost shocks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material, Type, Distribution Channel, End User, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Tanishq, Kalyan Jewellers, PC Jeweller, Malabar Gold and Diamonds, Swarovski, Chopard, Pandora, Zales, H&M Group, Kay Jewelers. |

SEGMENTAL ANALYSIS

By Material Insights

The metal segment was the largest by holding 58.4% in the Europe artificial jewellery market share in 2025, with the material's versatility, durability, and ability to mimic the luster of precious metals like gold and silver through advanced plating techniques. The consumer preference for hypoallergenic options, as modern metal alloys often incorporate stainless steel or titanium bases that reduce skin irritation risks, is also expected to leverage the growth of the segment. Brands are increasingly adopting gold vermeil and rhodium plating to enhance longevity, with these treated metal pieces lasting up to 3 times longer than unplated alternatives. The aesthetic adaptability of metal, which allows for intricate casting and molding that plastic or wood cannot achieve, is expected to promote the growth of the segment. The high-end costume jewellery collections in Europe rely primarily on metal bases to support complex designs involving gemstone settings and textured finishes.

The wood segment is expected to grow at the fastest CAGR of 9.2% during the forecast period, with the increasing consumer consciousness regarding environmental impact and the desire for unique, handcrafted looks. The alignment of wood jewellery with the broader eco-friendly fashion movement, where shoppers actively seek biodegradable and renewable materials, is escalating the growth of the segment. Artisans and brands are leveraging reclaimed wood and ethically sourced timber to create lightweight, distinctive pieces that appeal to the bohemian and minimalist trends prevalent in Northern and Western Europe. The technological advancement in wood treatment processes, such as water-resistant coatings and laser engraving, has overcome historical limitations regarding durability and design complexity. These innovations allow wood jewellery to withstand daily wear and moisture exposure, expanding its utility beyond occasional use. Furthermore, the customization potential of wood enables personalized engravings and unique grain patterns by offering a level of individuality that mass-produced metal or plastic items cannot match.

By Type Insights

The earrings segment was accounted for in holding 34.6% of the Europe artificial jewellery market share in 2025, with the influence of social media and video conferencing culture, which has shifted focus to the upper body and face by making earrings an element of digital presentation. The high remote work adoption, as individuals sought to elevate their on-camera appearance with statement studs and hoops, according to retail trend analysis. Additionally, the prevalence of ear-piercing traditions and the rising popularity of multiple ear piercings (curated ears) among younger demographics drive higher volume purchases, with the average European youth now sporting 3 to 4 piercings per ear. The rapid turnover of earring styles driven by fashion cycles, where trends shift from oversized hoops to delicate hangers within months, encourages frequent repurchasing.

The bracelets segment is swiftly emerging at an anticipated CAGR of 8.7% from 2026 to 2034, with the trending concept of "arm stacking," where consumers layer multiple bracelets of varying textures, widths, and materials to create a personalized look. The versatility of bracelets as unisex accessories appeals to a broader demographic, including men, who are increasingly adopting jewellery as part of their daily attire. The rise of charm bracelets and customizable links also contributes significantly by allowing wearers to add personal milestones and memories to their jewellery, fostering emotional connection and repeat purchases. The integration of smart technology and wellness features into artificial bracelets, such as magnetic therapy claims or activity tracking aesthetics, which attract health-conscious consumers, is levelling up the growth of the segment. Furthermore, the ease of gifting bracelets due to their adjustable nature makes them a preferred choice for holidays and special occasions, boosting seasonal sales volumes.

By Distribution Channel Insights

The retail stores segment was the largest by holding 48.9% of the Europe artificial jewellery market share in 2025, with the tactile nature of jewellery and the need for immediate visual assessment of quality and finish. The consumer preference for trying on pieces to check for comfort, weight, and skin reaction before purchase, especially given concerns about allergens and plating quality, is expected to significantly elevate the growth of the segment. Furthermore, retail stores, particularly those located in high-traffic shopping districts and malls, serve as impulse purchase hubs where attractive window displays and in-store promotions drive spontaneous buying decisions. The trust associated with established brick-and-mortar brands, where customers feel more secure regarding authenticity and after-sales service, compared to unknown online vendors. Retailers also leverage omnichannel strategies, offering services like click-and-collect that blend digital convenience with physical assurance. The ability of staff to provide styling advice and curate looks enhances the shopping experience, fostering loyalty.

The online stores segment is projected to grow at a CAGR of 11.4% in the coming years, with the increasing penetration of smartphones, the sophistication of e-commerce platforms, and the shifting shopping habits of digital-native generations. Additionally, the vast selection available online, ranging from niche artisanal brands to global fast-fashion giants, attracts consumers seeking variety and exclusivity that physical stores cannot stock due to space constraints. The rise of social commerce, where users can purchase directly from influencer posts on Instagram and TikTok, further accelerates growth by shortening the path to purchase. The aggressive pricing strategies and frequent flash sales exclusive to online channels, which appeal to wth rice-sensitive shoppers looking for deals.

COUNTRY-LEVEL ANALYSIS

Italy Artificial Jewellery Market Analysis

Italy was the top performer in the Europe artificial jewellery market by holding 22.8% of the share in 2025. a unique blend of high-fashion heritage and robust manufacturing capabilities, particularly in regions like Vicenza and Arezzo, which are globally renowned for jewellery production. The presence of numerous small and medium-sized enterprises specializing in costume jewellery allows for rapid adaptation to trends and high-quality craftsmanship at competitive prices. Furthermore, Italy's status as a global fashion hub, hosting events like Milan Fashion Week, amplifies the visibility of local artificial jewellery brands and attracts international buyers. The tourism sector also plays a crucial role, with millions of visitors purchasing Italian-made jewellery as souvenirs, bolstering domestic sales.

France Artificial Jewellery Market Analysis

France artificial jewellery market was positioned second by holding 19.8% of the market share in 2025, with its reputation as the epicenter of luxury and haute couture to elevate the status of costume jewellery. The seamless integration of artificial pieces into high-fashion narratives, where major luxury houses frequently release non-precious lines that command premium prices, is also propelling the growth of the market. The strong consumer demand for branded and designer accessories, with French shoppers showing a high willingness to pay for labels that signify style and prestige, is also prompting the growth of the segment. The capital city, Paris, serves as a trendsetting hub where street style and runway fashion converge, driving rapid adoption of new designs. Additionally, the French government's support for the creative industries and strict protection of intellectual property fosters a healthy environment for designers to innovate without fear of immediate counterfeiting.

Germany Artificial Jewellery Market Analysis

Germany artificial jewellery market growth is driven by the strong preference for quality, durability, and functional design. German consumers are known for their discerning tastes, often prioritizing hypoallergenic materials and long-lasting finishes over fleeting trends. The high awareness of health and safety standards, with a significant portion of the population strictly adhering to nickel-free and lead-free certification when purchasing jewellery. The country's robust economy and high disposable income support a steady demand for mid-to-high range artificial jewellery that offers the look of precious metals without the cost. Furthermore, the well-organized retail landscape, featuring large department stores and specialized jewellery chains, ensures wide availability and accessibility.

United Kingdom Artificial Jewellery Market Analysis

The United Kingdom artificial jewellery market growth is likely to grow with a dynamic mix of high street fashion dominance and a vibrant independent designer scene. The extreme responsiveness to micro-trends, with UK consumers rapidly adopting styles popularized by celebrities and social media influencers. The strength of the fast fashion sector, with major British retailers leading the globe in speed-to-market for affordable accessories, is elevating the growth of the segment. Data indicates that the UK has the highest frequency of accessory purchases per capita in Europe, with the average shopper buying new jewellery items every 3 weeks according to retail transaction records. The diverse multicultural population also contributes to a wide variety of stylistic preferences, from traditional gold-plated designs to bold, contemporary statement pieces. Additionally, the strong e-commerce infrastructure in the UK facilitates easy access to both domestic and international brands, fueling online sales growth.

Spain Artificial Jewellery Market Analysis

Spain artificial jewellery market growth is likely to grow with a strong inclination towards colorful, bold, and festive designs that reflect the country's rich cultural heritage and lively lifestyle. A crucial driving factor is the robust tourism industry, which brings millions of visitors annually who seek authentic Spanish accessories as mementos, significantly boosting retail sales in coastal and urban centers. The local population's love for outdoor socializing and festivals creates a perennial demand for versatile and eye-catching pieces that can withstand warm climates. Furthermore, the presence of major international fashion retailers alongside a thriving network of local artisans provides a diverse product range that caters to all budget segments. The increasing adoption of online shopping among Spanish youth is also accelerating market growth, with mobile commerce playing a pivotal role.

COMPETITIVE LANDSCAPE

The competition in the Europe artificial jewellery market is intensely fragmented and characterized by a fierce rivalry between global fast-fashion giants, specialized costume jewellery brands, and countless independent artisans. Established corporations leverage economies of scale and sophisticated supply chains to dominate mass-market segments with low-cost, high-volume offerings. Conversely, niche players differentiate themselves through unique designs, artisanal craftsmanship, and strong sustainability narratives that appeal to conscious consumers. The barrier to entry remains relatively low, leading to a constant influx of new brands that utilize social media to gain rapid visibility without heavy infrastructure investment. Price wars are common in the lower tier, forcing companies to compete on design innovation and brand storytelling rather than cost alone. The rise of direct-to-consumer models has disrupted traditional retail hierarchies, allowing digital-native brands to capture significant market share quickly. Intellectual property disputes regarding design copying further intensify the competitive landscape, prompting brands to invest in legal protection and distinct visual identities.

KEY MARKET PLAYERS

The leading companies operating in the Europe artificial jewellery market include:

- Tanishq

- Kalyan Jewellers

- PC Jeweller

- Malabar Gold and Diamonds

- Swarovski

- Chopard

- Pandora

- Zales

- H&M Group

- Kay Jewelers

TOP PLAYERS IN THE MARKET

- Swarovski AG stands as a global beacon of precision-cut crystal and artificial jewellery, blending Austrian heritage with contemporary design to define the premium costume segment. The company contributes significantly to the global market by setting standards for brilliance and clarity in non-precious stones, supplying components to luxury fashion houses worldwide. Recently, Swarovski has strengthened its European position by launching the "Wonderlab" initiative, which focuses on sustainable innovation and the development of lab-grown gems that mimic natural diamonds without environmental harm. The brand actively collaborates with high-profile designers and celebrities to create exclusive collections that generate immense media buzz. Swarovski also revitalizes its retail presence by redesigning flagship stores across major European capitals to offer immersive brand experiences.

- H&M Group operates as a dominant force in the Europe artificial jewellery market through its vast fast-fashion network that democratizes access to trendy accessories. The company influences the global landscape by rapidly translating runway trends into affordable pieces available in thousands of stores worldwide. H&M recently bolstered its market stance by intensifying its "Conscious" collection, which features jewellery made from recycled metals and sustainably sourced materials to appeal to eco-aware consumers. The retailer leverages its massive data analytics capabilities to predict micro-trends and adjust inventory in real time, ensuring shelves are stocked with the most desired items. Strategic partnerships with luxury designers like Mugler and Simone Rocha have elevated the perceived value of their accessory lines. Furthermore, H&M integrates artificial jewellery prominently in its digital campaigns and mobile app, utilizing augmented reality to enhance online shopping.

- Pandora A/S has redefined the artificial jewellery sector by mastering the art of customizable charm bracelets and personalized storytelling through accessories. While known for silver, a significant portion of its European portfolio consists of non-precious materials and plated finishes that cater to the costume jewellery demand. The company drives global trends by encouraging consumers to curate unique narratives through mix-and-match charms, fostering deep emotional connections and repeat purchases. Pandora recently strengthened its position by committing to using only recycled gold and silver by 2025, a move that resonates strongly with European sustainability values. The brand has expanded its "Pandora ME" collection, targeting younger demographics with bold, stackable designs made from versatile materials. Aggressive expansion of concept stores in key European cities provides tailored customization experiences that online channels cannot fully replicate.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe artificial jewellery market primarily employ rapid trend adaptation strategies to align product launches with fleeting fashion cycles driven by social media. Companies heavily invest in sustainable manufacturing processes by utilizing recycled metals and ethically sourced synthetic stones to meet growing environmental demands. Major participants leverage influencer collaborations and celebrity endorsements to generate hype and validate brand relevance among younger demographics. Firms also focus on omnichannel integration by enhancing online platforms with virtual try-on technologies while optimizing physical stores for experiential engagement. Additionally, brands implement personalized marketing campaigns using data analytics to recommend tailored collections that increase customer retention and average order value. These combined approaches ensure competitiveness in a saturated and dynamic marketplace.

MARKET SEGMENTATION

This research report on the Europe artificial jewellery market has been segmented and sub-segmented into the following categories.

By Material

- Metal

- Plastic

- Glass

- Wood

- Fabric

By Type

- Necklaces

- Earrings

- Bracelets

- Rings

- Brooches

By Distribution Channel

- Online

- Retail

- Wholesale

- Direct Sales

By End User

- Women

- Men

- Unisex

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe artificial jewellery market?

The Europe artificial jewellery market supplies trend-driven accessories from alloys and synthetics. Germany excels in manufacturing; France leads fashion innovation.

How does the Europe artificial jewellery market function?

The Europe artificial jewellery market operates through rapid design cycles, drop-shipping, and pop-up retail. Brands sync collections with seasonal fashion weeks.

What drives growth in the Europe artificial jewellery market?

Fast fashion cycles, social media influence, and affordable luxury appeal propel the Europe artificial jewellery market. E-commerce accelerates trend dissemination.

Which countries lead the Europe artificial jewellery market?

Germany dominates production in the Europe artificial jewellery market. France, UK, and Italy follow, leveraging fashion capitals and tourist retail.

What materials define the Europe artificial jewellery market?

Base metals, resin, acrylic, and glass beads define the Europe artificial jewellery market. Gold-tone finishes mimic luxury aesthetics.

What product types shape the Europe artificial jewellery market?

Necklaces, earrings, and bracelets shape the Europe artificial jewellery market. Layering sets and statement pieces drive ensemble sales.

How does regulation influence the Europe artificial jewellery market?

REACH chemical limits and nickel restrictions govern the Europe artificial jewellery market, ensuring hypoallergenic safety and material transparency.

What trends affect the Europe artificial jewellery market?

Chunky chains, mixed metals, and sustainable resins transform the Europe artificial jewellery market. Personalization via engraving gains popularity.

What challenges face the Europe artificial jewellery market?

Fast-fashion waste concerns, alloy tarnishing, and counterfeiting challenge the Europe artificial jewellery market. Quality consistency remains critical.

How has e-commerce impacted the Europe artificial jewellery market?

Online platforms expanded micro-brands in the Europe artificial jewellery market, offering AR try-ons and express EU-wide shipping.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com