Europe Automotive Casting Market Size, Share, Trends & Growth Forecast Report, Segmented By Material Type, Process, Application, Vehicle Type, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Market Size, 2025

$22.89 BnMarket Estimate, 2026

$24.16 BnMarket Forecast, 2034

$37.16 BnCAGR, 2026–2034

5.53%Europe Automotive Casting Market

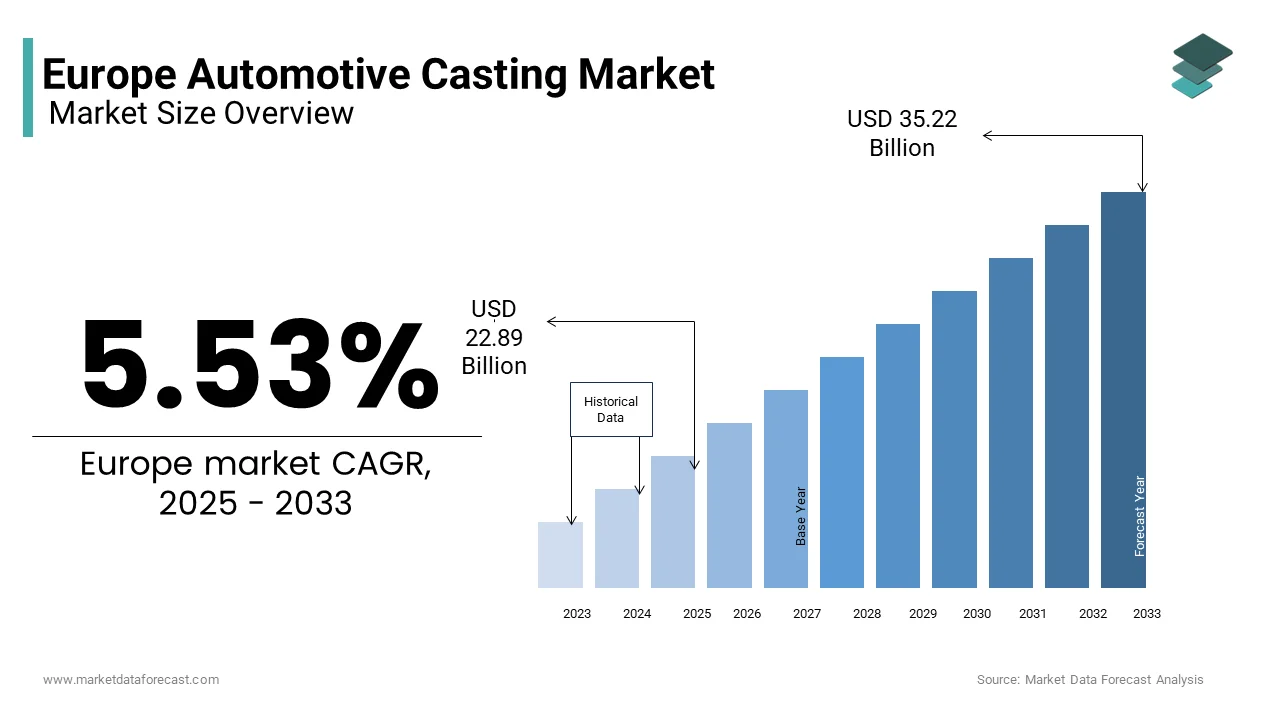

The Europe automotive casting market size was valued at USD 22.89 billion in 2025 and is anticipated to reach USD 24.16 billion in 2026 to reach USD 37.16 billion by 2034, growing at a CAGR of 5.53% during the forecast period from 2026 to 2034.

The Europe automotive casting market refers to the production and supply of metal components, primarily aluminum, iron, and steel castings, used in the manufacturing of passenger vehicles, commercial vehicles, and electric vehicles across the continent. These components include engine blocks, cylinder heads, transmission cases, suspension parts, and structural elements that are critical to vehicle performance and safety. As a key supplier to global automakers, Europe’s casting industry is deeply integrated into automotive value chains, particularly in countries like Germany, Italy, France, and Spain.

The region's foundries have been adapting to lightweight material demands due to stricter emission norms and rising electric vehicle adoption. In 2023, aluminum casting accounted for more than 50% of total metal usage in automotive components, as per data from the European Foundry Association (CAEF). This shift aligns with the EU’s Green Deal initiative, aiming for carbon neutrality by 2050, influencing manufacturers to invest in advanced casting technologies and sustainable production practices.

MARKET DRIVERS

Growth in Electric Vehicle Production Across Europe

One of the most significant drivers of the Europe automotive casting market is the rapid expansion of electric vehicle (EV) production. As governments push for decarbonization and automakers pivot toward electrification, EV sales in Europe surged to nearly 3.2 million units in 2023, marking a year-on-year increase of almost 20%, according to the International Energy Agency (IEA). This transition has created a surge in demand for lightweight aluminum castings used in battery housings, motor casings, and structural components.

Electric vehicles require extensive use of cast parts to reduce overall weight while maintaining structural integrity. For instance, Tesla’s Model Y uses a large single-piece aluminum casting for its rear underbody, significantly reducing the number of parts and enhancing production efficiency. Traditional automakers such as BMW and Volkswagen are also adopting similar strategies, integrating die-cast components into their EV platforms. As reported by McKinsey & Company, the average aluminum content in an EV is approximately 280 kg, compared to about 150 kg in internal combustion engine (ICE) vehicles. This growing reliance on aluminum castings directly stimulates market growth.

Moreover, the European Union’s regulatory framework, including the 2035 ICE phase-out mandate, compels automakers to accelerate EV production. This regulatory push, combined with increasing consumer acceptance and charging infrastructure development, ensures sustained demand for automotive casting solutions tailored for electric mobility.

Expansion of Localized Manufacturing Hubs in Eastern Europe

Another pivotal driver fueling the Europe automotive casting market is the steady growth of localized manufacturing hubs in Eastern Europe, particularly in Poland, the Czech Republic, Hungary, and Romania. These countries have emerged as attractive investment destinations due to lower labor costs, skilled workforce availability, and strong government incentives aimed at boosting industrial activity. According to Eurostat, the manufacturing sector in Central and Eastern Europe expanded by 4.7% in 2023, outpacing Western Europe’s growth rate of 2.1%.

Automotive giants such as Stellantis, Volkswagen, and Toyota have established or expanded production facilities in these regions, leading to increased demand for local casting suppliers. This trend supports domestic foundries and encourages foreign casting firms to set up operations locally, reducing logistics costs and lead times.

Furthermore, the reshoring and nearshoring trends post-pandemic have prompted automakers to shorten supply chains and diversify sourcing. This strategic shift reinforces the role of Eastern Europe as a robust casting and component manufacturing hub, offering long-term growth potential for the automotive casting market.

MARKET RESTRAINTS

Supply Chain Disruptions Due to Raw Material Shortages

A major restraint affecting the Europe automotive casting market is the persistent disruption in raw material supply chains, particularly for aluminum and copper. The energy crisis triggered by geopolitical tensions, especially following Russia’s invasion of Ukraine, has led to soaring electricity prices, which directly impact the cost and availability of primary aluminum. According to the European Aluminium Association, European smelters collectively reduced aluminum production by over 1 million metric tons between 2022 and 2023 due to high energy costs.

This decline in domestic aluminum output has forced casting manufacturers to rely more heavily on imported raw materials, increasing both cost and delivery lead times. In 2023, import dependency for aluminum reached 35%, up from 20% in 2021, as stated by the European Commission. Also, freight delays and container shortages further exacerbate supply chain bottlenecks, causing production halts and order backlogs across foundries.

These disruptions not only raise input costs but also create uncertainty for long-term contracts between casting suppliers and automotive OEMs. The volatility in raw material markets continues to pose a significant challenge to the stability and scalability of the Europe automotive casting industry.

Rising Labor Costs and Skilled Workforce Shortage

Another significant constraint on the Europe automotive casting market is the rising labor costs coupled with a shortage of skilled workers in the foundry industry. Despite technological advancements, foundry operations remain labor-intensive, requiring expertise in metallurgy, mold design, and quality control. However, as per the European Trade Union Confederation (ETUC), the average hourly wage in the metalworking sector rose by 6.5% in 2023, driven by inflation and a tight labor landscape.

Simultaneously, the aging workforce and lack of interest among younger generations in foundry jobs have led to a critical skills gap. Vocational training programs have struggled to keep pace with industry needs, resulting in recruitment challenges for small and medium-sized foundries.

Also, approximately 45% of European casting firms reported operational inefficiencies due to labor shortages in 2023. Automation is being adopted to mitigate this issue, but high capital expenditure limits its feasibility for smaller players.

MARKET OPPORTUNITY

Adoption of Additive Manufacturing in Casting Processes

A major opportunity shaping the future of the Europe automotive casting market is the integration of additive manufacturing (AM), commonly known as 3D printing, into traditional casting processes. This technology enables the production of complex geometries, reduces material waste, and accelerates prototyping cycles—offering a competitive edge to foundries embracing digital innovation. German and Italian foundries, in particular, have pioneered the adoption of AM-based sand and metal printing to produce intricate molds and cores without the need for expensive tooling. For instance, Siemens has collaborated with several foundries to implement digitally integrated casting systems that enhance precision and reduce time-to-market. As per Fraunhofer IPA, the application of 3D-printed sand molds has cut down prototyping lead times by up to 50% and lowered costs by 30% in pilot projects conducted in 2023.

Besides, the European Union has allocated over €500 million in funding under Horizon Europe for research into smart manufacturing technologies, including additive casting methods. This financial backing encourages startups and SMEs to explore scalable solutions, positioning Europe as a global leader in next-generation casting technologies.

Increasing Demand for Lightweight Components in Commercial Vehicles

An emerging opportunity within the Europe automotive casting market is the growing emphasis on lightweight components in commercial vehicles, driven by fuel efficiency mandates and logistics electrification. According to ACEA, heavy-duty trucks and buses account for over 6% of total CO₂ emissions in the EU, prompting regulators to introduce stricter emission standards. To comply, commercial vehicle manufacturers are increasingly turning to aluminum and magnesium castings to reduce vehicle mass without compromising strength.

In 2023, Daimler Truck and Volvo Group announced joint investments exceeding €2 billion in lightweight chassis and powertrain components, with a focus on aluminum casting technologies. This shift is creating a surge in demand for cast aluminum wheels, engine components, and suspension parts tailored for commercial fleets. Moreover, the electrification of urban delivery vans and refuse trucks is further accelerating the need for lighter structures to compensate for battery weight.

MARKET CHALLENGES

Environmental Regulations and Decarbonization Pressures

A significant challenge facing the Europe automotive casting market is the tightening environmental regulations imposed by the European Union as part of its Green Deal agenda. Foundries, being energy-intensive operations, are under increasing scrutiny due to their carbon emissions and resource consumption. The revised Industrial Emissions Directive (IED) and the Carbon Border Adjustment Mechanism (CBAM) have introduced stricter compliance requirements, compelling casting companies to invest in cleaner technologies and alternative fuels.

According to the European Environment Agency, the foundry sector contributes approximately 1.2% of total industrial CO₂ emissions in the EU. To meet the 2030 climate targets, the European Commission has mandated a 55% reduction in greenhouse gas emissions compared to 1990 levels. This necessitates substantial capital expenditure on emission control systems, hydrogen-based melting furnaces, and scrap recycling infrastructure.

Intensifying Competition from Low-Cost Casting Markets in Asia

Intensifying competition from low-cost casting markets in Asia poses a formidable challenge to the Europe automotive casting industry. Countries like India, Vietnam, and Thailand offer significantly lower production costs, supported by government subsidies, abundant raw materials, and favorable labor conditions. According to the Boston Consulting Group (BCG), the average cost of producing a ton of automotive casting in Southeast Asia is lower than in Western Europe.

This cost disparity is driving some automotive OEMs to relocate or outsource casting operations to Asian suppliers. For example, Stellantis and Renault have partially shifted component sourcing from European foundries to Indian and Chinese partners to reduce expenses. As reported by ACEA, automotive casting imports into Europe grew significantly in 2023, reflecting this trend.

Furthermore, Asian casting companies are investing in advanced technologies and certifications to meet international quality standards, thereby gaining access to European supply chains. According to the Confederation of Indian Industry (CII), India’s foundry sector exported over €2.5 billion worth of automotive castings to Europe in 2023, up from €1.8 billion in 2021.

European foundries must respond by improving automation, optimizing energy use, and forming strategic alliances to maintain competitiveness. However, the influx of cost-effective alternatives from Asia continues to pressure margins and market share, making it imperative for European casting firms to innovate and differentiate through superior quality, customization, and localized service capabilities.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.32% |

| Segments Covered | By Vehicle Type, Product Type, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

| Market Leaders Profiled | Bedford Machine & Tool Inc., Cast Products, Inc, Casteks Metal Science Co., Ltd., Dynacast International Inc, By Form Technologies, Inc, Endurance Technologies Limited, Georg Fischer Ltd., Gibbs Die-casting Group, Impro Precision Industries Limited, Kinetic Die Casting Company, Inc., Kopf Holding GmbH, Lakeside Casting Solutions, LLC, Minda Corporation Limited, Mino Industry USA, Inc, Ningbo Parison Die Casting Co., Ltd, Ningbo Yinzhou Ke Ming Machinery Manufacturing Co., Ltd., Production Castings, Inc, Regensburger Druckgusswerk Wolf GmbH Rockman Industries Limited, Ryobi Limited, Sandhar, Sipra Engineers Pvt. Ltd., Sunbeam Lightweighting Solutions Pvt. Ltd. |

SEGMENTAL ANALYSIS

By Material Insights

The iron casting remained the largest segment in the Europe automotive casting market by accounting for 4.72% of total material usage in 2024. This dominance is primarily attributed to its extensive application in engine blocks and brake components, particularly in internal combustion engine (ICE) vehicles, which still form a significant portion of automotive production in the region.

Germany, being the largest automotive manufacturing hub in Europe, consumes over 1.8 million metric tons of iron castings annually, according to the VDMA Association for Foundry Technology. The high thermal resistance, durability, and cost-effectiveness of iron make it indispensable for heavy-duty applications such as cylinder liners, transmission housings, and exhaust manifolds. In addition, commercial vehicle manufacturers like MAN Truck & Bus and Scania continue to rely on iron-based components due to their mechanical strength and load-bearing capacity.

Despite the shift toward lightweight materials driven by electrification, iron casting maintains a strong foothold in legacy powertrain systems.

The aluminum casting is the quickest expanding segment in the Europe automotive casting market, registering a CAGR of 7.8% between 2025 and 2033. This rapid expansion is largely driven by the automotive industry’s focus on reducing vehicle weight to meet stringent EU emission norms and improve energy efficiency, especially in electric vehicles (EVs).

The average aluminum content in an EV has risen to nearly 280 kg compared to 150 kg in conventional vehicles, as noted by McKinsey & Company in early 2024. Battery enclosures, motor casings, and structural components are increasingly being manufactured using high-pressure die-cast aluminum alloys to enhance performance while reducing mass. For instance, Volkswagen's MEB platform uses aluminum casting for over 40% of its chassis components, significantly lowering overall vehicle weight.

Additionally, regulatory mandates such as the EU’s 2035 ICE phase-out target are accelerating the adoption of aluminum across major OEMs. As per ACEA, EV sales in Europe surpassed 2.7 million units in 2023, reinforcing the growing demand for lightweight casting solutions.

By Process Insights

The sand casting held the maximum portion of the Europe automotive casting market by accounting for 51% of total production volume in 2024. This process is widely adopted for manufacturing large, complex components such as engine blocks, cylinder heads, and transmission cases, which require high dimensional stability and cost-effective tooling. One of the key reasons for sand casting’s dominance is its adaptability to both small-scale prototyping and high-volume production runs. German foundries, in particular, have optimized green sand and resin-bonded sand processes to support automotive OEMs such as BMW and Mercedes-Benz. Moreover, sand casting is well-suited for producing iron and steel-based components, which remain essential for traditional powertrains and commercial vehicles.

The die casting is the fastest-growing process in the Europe automotive casting market by recording a CAGR of 9.2%. This rapid progress is fueled by the rising demand for precision-engineered, lightweight components in electric vehicles (EVs), where aluminum die casting plays a pivotal role in battery housing, chassis structures, and motor casings. High-pressure die casting (HPDC) enables automakers to produce monolithic components with minimal assembly requirements, enhancing production efficiency. Tesla’s Gigafactory in Berlin, for example, utilizes Giga Press technology to manufacture single-piece rear underbody castings, drastically reducing part count and assembly complexity. According to McKinsey & Company, the use of HPDC in EV platforms can reduce manufacturing costs and assembly time.

Furthermore, increasing investments in advanced die-casting equipment by foundries across Italy and Spain are supporting this growth trajectory.

By Application Insights

The engine components segment spearheaded in the Europe automotive casting market with a 45.3% market share in 2024. This control is mainly propelled by the continued reliance on internal combustion engines (ICEs) in passenger and commercial vehicles, despite the rise of electric mobility. Cast iron and aluminum alloys are extensively used in engine blocks, cylinder heads, and pistons, with Germany leading in production due to its robust automotive manufacturing base. The high thermal resistance and durability of these materials make them ideal for engine applications where reliability and heat dissipation are critical. Even as the transition to electric vehicles accelerates, hybrid models still incorporate ICEs, ensuring sustained demand for engine castings. Also, commercial vehicle manufacturers such as Daimler Truck and Volvo continue to utilize cast iron engine parts, further solidifying this segment’s stronghold in the market.

The suspension components are moving ahead as the rapidly advancing application segment in the Europe automotive casting market, expanding at a CAGR of 8.4%. This development is basically driven by the increasing adoption of lightweight aluminum and magnesium castings in suspension systems to enhance ride quality, handling, and fuel efficiency.

Electric vehicle (EV) manufacturers are particularly focused on reducing unsprung mass—components not supported by the vehicle’s suspension springs—to improve battery efficiency and driving dynamics. Companies like Audi and BMW have incorporated die-cast aluminum control arms into their EV platforms to achieve these benefits.

Additionally, stricter emissions regulations and consumer demand for comfort-oriented features are pushing automakers to innovate in chassis design. This trend is expected to drive further demand for high-performance castings in suspension systems, making this segment a key growth driver in the coming years.

By Vehicle Insights

The passenger vehicles dominated the Europe automotive casting market by accounting for a8.5% of total casting demand in 2024. This segment’s influence is due to the sheer volume of cars produced and sold across the continent, particularly in Germany, France, and Italy, which together contribute a notable share of Europe’s total automotive output. Each vehicle contains multiple cast components, including engine blocks, transmission housings, and suspension parts, many of which are made from aluminum and iron alloys. The shift toward electric passenger vehicles has further boosted demand for aluminum castings, especially in battery enclosures and chassis structures. Moreover, established automotive brands such as Volkswagen, Renault, and BMW continue to invest heavily in localized casting supply chains to ensure quality and efficiency.

The commercial vehicles accelerated with the highest CAGR of 7.1%. This is mainly fueled by the electrification of logistics fleets and the rising demand for durable, lightweight components tailored for heavy-duty applications. Heavy trucks and delivery vans are undergoing significant transformation as governments mandate cleaner transport solutions. According to ACEA, electric commercial vehicle registrations in Europe increased in 2023 compared to the previous year. This shift has led to higher demand for aluminum and magnesium castings in chassis frames, motor casings, and suspension components to offset the additional weight of batteries without compromising payload capacity. German and Swedish truck manufacturers such as Daimler Truck and Volvo Group have been at the forefront of adopting lightweight casting technologies.

COUNTRY LEVEL ANALYSIS

Germany Automotive Casting Market

Germany was in the top position in the Europe automotive casting market by commanding 28.5% of the total regional output in 2024. As Europe’s largest automotive manufacturer, Germany produced over 4.5 million vehicles in 2023, according to ACEA, creating substantial demand for casting components used in engines, transmissions, and chassis systems. The country’s advanced industrial infrastructure, coupled with a dense network of Tier-1 foundries and automotive suppliers, supports a highly integrated casting ecosystem. Companies such as Rheinmetall Automotive and Georg Fischer operate state-of-the-art facilities specializing in aluminum and iron casting for both internal combustion and electric vehicle platforms. Apart from these, government-backed initiatives such as the National Platform for Electric Mobility have spurred innovation in lightweight casting technologies, particularly for EV battery enclosures and structural components. With ongoing investments in Industry 4.0 and digital foundry management systems, Germany remains a dominant force in shaping the future of automotive casting across Europe.

France Automotive Casting Market

France has a strong industrial base in the market. It benefits from a well-established manufacturing landscape, with major players such as Stellantis and Renault relying on domestic casting firms for engine, transmission, and structural components. The French government has actively supported the transition to low-emission mobility through subsidies and R&D funding, encouraging foundries to adopt lightweight casting techniques. Moreover, French foundries have embraced automation and digital process optimization to enhance efficiency and reduce waste. These developments reinforce France’s competitive position in the regional casting market.

Italy Automotive Casting Market

Italy holds a prominent position in the Europe automotive casting market. This nation is home to a vast number of specialized casting firms, many of which supply components to global automakers such as Ferrari, Lamborghini, and Fiat.

With over 1.3 million vehicles produced in 2023, according to ACEA, Italy sustains a steady demand for cast components across engine, transmission, and chassis applications. Italian foundries are known for their expertise in high-pressure die casting and sand casting, particularly for aluminum and iron-based components. Additionally, the Italian government has introduced incentives for sustainable manufacturing practices, prompting foundries to invest in hydrogen-based melting furnaces and scrap recycling infrastructure.

Spain Automotive Casting Market

Spain is seeing a growing casting presence in the market and has steadily expanded its casting capabilities to support a growing automotive production base, which reached an enormous number of units in 2023, placing Spain among Europe’s top five vehicle producers. Spanish foundries play a crucial role in supplying cast components to both domestic and foreign automakers operating in the country, including Seat (a subsidiary of Volkswagen Group), Renault, and Toyota. According to ANFAC, exports of automotive castings from Spain grew in 2023, reflecting increasing international demand for locally produced components. Moreover, Spain has benefited from government-backed initiatives aimed at promoting green manufacturing and nearshoring opportunities.

United Kingdom Automotive Casting Market

The United Kingdom is a transitioning manufacturing landscape. Despite challenges posed by Brexit-related trade barriers and a shrinking domestic automotive production base, the UK continues to maintain a presence in high-value casting segments, particularly for premium and niche vehicle manufacturers. British foundries specialize in precision aluminum casting for luxury and performance vehicles, leveraging advanced engineering capabilities to differentiate themselves in a competitive market.

However, the shift toward electrification has prompted restructuring within the sector. As reported by PwC, several UK casting firms have pivoted toward EV-specific components, investing in new die-casting machinery and battery enclosure manufacturing capabilities.

KEY MARKET PLAYERS

A few of the market players in the Europe automotive casting market include

- Bedford Machine & Tool Inc.

- Cast Products, Inc.

- Casteks Metal Science Co., Ltd.

- Dynacast International Inc.

- Rheinmetall Automotive AG

- Fonderie AEterna S.p.A.

- By Form Technologies, Inc

- Endurance Technologies Limited

- Georg Fischer Ltd.

- Gibbs Die-casting Group

- Impro Precision Industries Limited

- Kinetic Die Casting Company, Inc.

- Kopf Holding GmbH

- Lakeside Casting Solutions

- LLC

- Minda Corporation Limited

- Mino Industry USA, Inc

- Ningbo Parison Die Casting Co., Ltd.

- Ningbo Yinzhou Ke Ming Machinery Manufacturing Co., Ltd.

- Production Castings, Inc.

- Regensburger Druckgusswerk Wolf GmbH Rockman Industries Limited

- Ryobi Limited

- Sandhar

- Sipra Engineers Pvt. Ltd.

- Sunbeam Lightweighting Solutions Pvt. Ltd.

TOP PLAYERS IN THE MARKET

- Georg Fischer is a leading global manufacturer of precision casting components, with a strong presence in Europe’s automotive sector. The company's automotive division specializes in lightweight aluminum and iron castings for engine, transmission, and structural applications. Known for its high-quality engineering solutions, Georg Fischer supplies major European OEMs such as BMW, Volkswagen, and Daimler. Its commitment to innovation, particularly in sustainable foundry practices and digital process integration, has reinforced its reputation as a reliable partner in automotive manufacturing ecosystems across Germany, France, and Italy.

- Rheinmetall Automotive is a key player in the European automotive casting market, offering a broad portfolio of components for both conventional and electric vehicles. The company excels in producing complex cast parts for powertrain systems, chassis, and electrified drivetrains. With production facilities across Germany and partnerships throughout Europe, Rheinmetall supports major automakers with tailored casting solutions that align with evolving emission standards and performance requirements. Its focus on technological advancement, including additive manufacturing and hybrid casting techniques, positions it as a forward-thinking supplier in the region.

- Based in Italy, Fonderie AEterna is a prominent manufacturer of aluminum and magnesium castings for automotive applications. The company serves several renowned European and international automakers, delivering components for engines, transmissions, and body structures. Recognized for its expertise in high-pressure die casting, AEterna emphasizes flexibility and customization to meet specific design and performance needs. Its strategic investments in energy-efficient foundries and advanced quality control systems have strengthened its competitive edge, making it a trusted name in the European casting landscape.

Top Strategies Used By Key Market Participants

- One of the primary strategies employed by leading players in the Europe automotive casting market is technological innovation, particularly in lightweight materials and advanced casting techniques. Companies are investing heavily in research and development to create high-strength, low-weight components that support fuel efficiency and electrification goals. This includes adopting new alloys, improving casting accuracy, and integrating Industry 4.0 technologies into production processes.

- Another critical approach is strategic collaborations and partnerships with automotive OEMs and tier suppliers. By aligning closely with vehicle manufacturers, casting firms can co-develop customized solutions that meet specific design and performance requirements. These alliances also facilitate early involvement in new vehicle programs, ensuring long-term supply contracts and enhanced market positioning.

- Lastly, sustainability-focused initiatives are gaining prominence as companies strive to comply with stringent environmental regulations. Foundries are modernizing their operations through energy-efficient melting furnaces, recycling programs, and carbon-neutral production pathways to maintain competitiveness while reducing environmental impact.

RECENT MARKET NEWS

- In February 2024, Georg Fischer announced the expansion of its aluminum casting facility in Eschen, Liechtenstein, focusing on high-pressure die-casting solutions tailored for electric vehicle platforms. This move enhances its capacity to meet rising demand for lightweight components and strengthens its foothold in the European EV supply chain.

- In June 2023, Rheinmetall Automotive acquired a minority stake in a German-based startup specializing in AI-driven casting process optimization. This investment aims to integrate real-time data analytics into production lines, improving efficiency and reducing defect rates across its European foundries.

- In November 2023, Fonderie AEterna launched a new green sand casting line at its plant in Italy, specifically designed to serve commercial vehicle clients. The initiative supports increased demand for durable, large-format castings while reinforcing the company’s commitment to flexible, sustainable manufacturing.

- In January 2024, Linamar Corporation expanded its European casting operations by opening a new production center in Poland, targeting nearshoring opportunities and strengthening its presence in the Central European automotive supply chain.

- In September 2023, thyssenkrupp Materials announced a partnership with an Austrian clean energy provider to transition its casting plants in Germany to hydrogen-based melting furnaces, aligning with EU decarbonization targets and enhancing its environmental credentials in the region.

MARKET SEGMENTATION

This research report on the Europe automotive casting market is segmented and is sub-segmented into the following categories.

By Material Type

- Iron

- Steel

- Aluminium

By Process

- Sand Casting

- Die Casting

- Investment Casting

By Application

- Engine

- Transmission

- Suspension

By vehicle Type

- Commercial vehicles

- Passenger vehicles

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the size of the Europe electric vehicle market in 2024?

The Europe EV market is valued at hundreds of billions of dollars in 2024, reflecting strong adoption of battery-powered passenger cars, vans, and charging ecosystems.

What drives EV demand in Europe?

Government incentives, tightening emission rules, expanding charging networks, and a growing consumer shift toward cleaner mobility.

Which country leads the Europe electric vehicle market?

Germany is the largest EV market, supported by domestic automotive production, subsidies, and rapid charging infrastructure growth.

Which segment dominates the Europe EV market?

Battery electric vehicles (BEVs) hold the largest share as consumers and fleets prioritize zero-emission driving.

Why is Europe one of the fastest-growing EV regions globally?

Because it has strict carbon targets, strong regulatory backing, and major automakers investing heavily in electrification.

What challenges affect EV growth in Europe?

Charging access gaps, battery cost pressures, grid readiness, and the phase-down of incentive schemes in some countries.

Which technologies are shaping the Europe EV market?

Fast-charging systems, solid-state batteries, vehicle-to-grid capabilities, and software-driven energy management.

Are electric vehicles becoming cost-competitive in Europe?

Yes battery prices are falling, and EV operating costs are lower, making ownership more attractive over time.

How do European policies support EV expansion?

Subsidies, tax breaks, CO₂ compliance rules, and bans on future internal-combustion vehicle sales in several countries.

What is the long-term outlook for the European EV market?

The market is expected to grow rapidly through 2035, driven by electrified manufacturing pipelines, strict climate mandates, and rising consumer acceptance.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com