Europe Aviation Market Research Report – Segmented By Revenue Stream (Passenger, Freight)By Type (Commercial Aircraft, Military Aircraft, General Aircraft)By Component (Aircraft, MRO, Ground Handling Services) & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU) - Industry Analysis on Size, Share, Trends & Growth Forecast 2026 to 2034

Market Size, 2025

$120.08 BnMarket Estimate, 2026

$128.08 BnMarket Forecast, 2034

$202.61 BnCAGR, 2026–2034

5.9%Executive Summary: Europe Aviation Market

- Market Scope: Regional European aviation market analysis covering revenue streams, aircraft types, component categories, country leadership frameworks, and fleet modernization adoption metrics.

- Market Valuation: Valued at USD 120.08 billion in 2025, estimated at USD 128.08 billion in 2026, and projected to reach USD 202.61 billion by 2034, registering a CAGR of 5.90% from 2026 to 2034.

- Primary Growth Drivers: Rapid expansion of low-cost carrier (LCC) operations across Europe, digital transformation through AI, biometrics, automation, and mobile technologies, rising passenger traffic and enhanced regional connectivity, alongside growing investments in fleet modernization and airport infrastructure.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (Position) | Fastest-Growing / Key Growth Segment |

|---|---|---|

| By Revenue Stream | Passenger Aviation (largest revenue stream) | Freight Aviation (projected at a 7.2% CAGR) |

| By Aircraft Type | Commercial Aircraft (largest type) | Military Aircraft (projected at a 5.9% CAGR) |

| By Component Category | Aircraft (largest component) | MRO (Maintenance, Repair & Overhaul) Services (projected at a 6.4% CAGR) |

| By Region / Country | Germany (leading country with 21.3% market share in 2025) | Expanding aviation hubs across the rest of Europe |

Major Market Players & Market Structure

Market Structure: Highly competitive European aviation landscape characterized by fuel-efficient fleet modernizations, sustainable aviation fuel (SAF) investments under the ReFuelEU initiative, zero-emission and hybrid-electric aircraft development, AI-enabled digital operations, and regional LCC network expansions.

Key Companies: Air France KLM SA, Airbus SE, BAE Systems Plc, Collins Aerospace, Lufthansa Group, Ryanair, easyJet, and Rolls-Royce.

Europe Aviation Market Size

The Europe Aviation Market is projected to grow from USD 120.08 billion in 2025 to USD 128.08 billion in 2026 and reach USD 202.61 billion by 2034, registering a CAGR of 5.90% from 2026 to 2034.

The aviation in Europe is one of the most developed and interconnected aviation regions globally, supported by a dense network of airlines, airports, and regulatory frameworks that ensure high standards of safety and efficiency.

According to Eurostat, air travel remains a dominant mode of transport within Europe, with over 1.2 billion passengers carried in 2023 on intra-European routes alone. The market is highly diversified, featuring major legacy carriers such as Air France-KLM, Lufthansa Group, and British Airways, alongside low-cost airlines like Ryanair and easyJet that have reshaped consumer expectations around affordability and convenience.

A key distinguishing feature of the European aviation sector is its commitment to sustainability. As per the European Union Aviation Safety Agency (EASA), the region has taken a dominant role in integrating environmental policies into aviation operations, including participation in the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA).

Air freight also plays a crucial role in cross-border e-commerce and pharmaceutical logistics. Frankfurt Airport and Paris-Charles de Gaulle Airport are among the busiest cargo hubs in Europe, handling millions of tons of goods annually.

MARKET DRIVERS

Surge in Low-Cost Carrier (LCC) Operations

One of the primary drivers of the Europe aviation market is the rapid expansion of low-cost carrier (LCC) operations, which have significantly broadened air travel accessibility across the continent. These airlines have transformed mobility patterns by offering competitively priced tickets on both domestic and international routes, which is making air travel an affordable option for a broader demographic.

According to CAPA – Centre for Aviation, LCCs accounted for nearly 41% of total European passenger traffic in 2023, up from 32% in 2019, reflecting their growing influence in shaping the aviation landscape. Ryanair and easyJet remain dominant players, but regional operators such as Wizz Air and Transavia have expanded aggressively into Eastern and Southern Europe.

These airlines leverage efficient fleet utilization, point-to-point route structures, and digital ticketing to reduce operational costs. Additionally, secondary airports have benefited from LCC growth, as these airlines often establish bases outside major metropolitan hubs to minimize landing fees and congestion delays. This decentralization has boosted regional connectivity and stimulated local economies. As per Eurocontrol, over 60 new routes were introduced by LCCs in 2023, primarily linking smaller cities across Central and Eastern Europe by reinforcing their role in driving sustained aviation demand.

Digital Transformation and Enhanced Passenger Experience

Digital transformation has emerged as a powerful driver in the Europe aviation market, enhancing operational efficiency while significantly improving the passenger experience. Airlines and airports have increasingly adopted automation, artificial intelligence, and mobile technologies to streamline check-in, baggage handling, security clearance, and boarding processes.

According to IATA, approximately 78% of European passengers used mobile check-in in 2023, compared to just 45% in 2019, which is demonstrating a shift toward self-service and contactless travel solutions. Biometric identification systems have been deployed at major hubs such as Amsterdam Schiphol and London Heathrow, reducing wait times and enhancing security.

Moreover, predictive analytics and AI-driven customer service tools are being leveraged to personalize travel experiences. As per a study by SITA, 64% of European airlines had implemented AI-based chatbots or virtual assistants by mid-2023 to handle customer inquiries more efficiently.

In-flight connectivity has also seen significant advancements, with airlines such as Lufthansa and Norwegian investing in high-speed Wi-Fi to meet rising passenger expectations. According to Inmarsat, inflight internet usage in Europe increased by 40% in 2023 by indicating growing reliance on digital engagement during flights. These innovations not only improve traveler satisfaction but also allow airlines to optimize fleet management, fuel consumption, and crew scheduling.

MARKET RESTRAINTS

Rising Environmental Regulations and Carbon Emission Pressures

Environmental regulations and increasing pressure to reduce carbon emissions have become a significant restraint on the growth of the Europe aviation market. Governments and regulatory bodies across the continent are implementing stringent policies aimed at curbing greenhouse gas emissions from the sector by aligning with the European Green Deal’s objective of achieving climate neutrality by 2050.

According to the European Environment Agency, aviation contributes approximately 3.6% of the EU's total greenhouse gas emissions by prompting policymakers to introduce measures such as the EU Emissions Trading System (EU ETS), Sustainable Aviation Fuel (SAF) mandates, and stricter CO₂ certification requirements for new aircraft.

The European Commission has mandated that airlines must use at least 2% SAF by 2025 is ramping up to 5% by 2030 and 63% by 2050 under the ReFuelEU Aviation initiative. However, the production and availability of SAF remain limited, and current costs are three to five times higher than conventional jet fuel, as per a report by McKinsey & Company.

Additionally, public sentiment against frequent flying due to environmental concerns has led to initiatives like flight shaming, influencing consumer behavior and potentially dampening demand for non-essential air travel. As per a survey by YouGov, 37% of European travelers considered alternative transportation modes instead of flying in 2023 due to sustainability concerns.

Geopolitical Tensions and Cross-Border Flight Disruptions

Geopolitical instability continues to pose a significant challenge to the Europe aviation market, affecting cross-border connectivity and disrupting long-established flight routes. Conflicts in Eastern Europe, trade disputes, and airspace closures have forced airlines to reroute flights is leading to longer travel times, increased fuel costs, and reduced profitability.

According to Eurocontrol, in 2023, European airlines experienced an average of 12% longer flight durations on certain routes due to airspace restrictions imposed in response to ongoing conflicts. Moreover, sanctions and diplomatic tensions have led to the suspension of air service agreements between European nations and countries in other regions, limiting market access for European carriers. For instance, airspace closures in Russia and Belarus have forced many European airlines to cancel direct flights to Asia and the Middle East, impacting transit traffic through European hubs.

Regional political disputes have also disrupted internal connectivity. As per the UK Civil Aviation Authority, post-Brexit negotiations have delayed the full restoration of some bilateral air service agreements, affecting capacity and frequency adjustments between the UK and mainland Europe.

MARKET OPPORTUNITIES

Expansion of Sustainable Aviation Fuels (SAFs) and Green Technologies

A transformative opportunity emerging in the Europe aviation market is the accelerated development and deployment of sustainable aviation fuels (SAFs) and green technologies aimed at decarbonizing air travel. According to the European Commission, under the ReFuelEU Aviation initiative, airlines operating within the EU will be required to blend at least 2% SAF into their fuel mix by 2025, scaling up to 63% by 2050. Several national governments, including Germany and France, have launched funding programs to support SAF production facilities, which is aiming to scale output and reduce cost disparities with conventional jet fuel.

Leading airlines such as KLM, Lufthansa, and Air France have already initiated pilot programs using bio-based and synthetic SAFs derived from waste materials and renewable hydrogen. Beyond fuels, the integration of electric and hybrid-electric propulsion systems is gaining momentum. Companies like Rolls-Royce and Airbus are developing zero-emission aircraft prototypes, with plans for short-haul electric flights by the late 2020s. As per BloombergNEF, the global SAF market could reach $150 billion by 2040, with Europe positioned as a key early adopter. This transition presents a substantial opportunity for aviation stakeholders to align with sustainability goals while securing future competitiveness in a rapidly evolving regulatory landscape.

Growth of Regional and Short-Haul Connectivity via Smaller Hubs

An emerging opportunity in the Europe aviation market lies in strengthening regional and short-haul connectivity through the strategic development of secondary airports and smaller hub operations. As major metropolitan airports face congestion and capacity constraints, there is increasing emphasis on utilizing underutilized regional airports to enhance domestic and cross-border mobility.

According to Eurocontrol, secondary airports handled over 28% of total European air traffic in 2023, with growth outpacing that of primary hubs. Cities such as Wrocław, Budapest, and Vilnius have seen increased airline presence from low-cost carriers seeking to expand their route networks without facing the high operational costs associated with major gateways. This trend is supported by government incentives and infrastructure investments aimed at improving runway capacity, terminal facilities, and intermodal transport links. Additionally, the rise of business travel corridors between mid-sized cities is creating demand for more frequent and flexible flight options. As per McKinsey & Company, corporate travelers in sectors such as consulting, finance, and engineering are increasingly opting for shorter flights connecting regional centers rather than transiting through congested hubs.

MARKET CHALLENGES

Workforce Shortages and Labor Unrest

One of the most pressing challenges currently affecting the Europe aviation market is the persistent shortage of skilled aviation personnel, including pilots, cabin crew, air traffic controllers, and ground staff. This labor crunch has been exacerbated by the pandemic-induced workforce reductions, early retirements, and training bottlenecks that have left airlines struggling to meet resurgent travel demand.

According to the European Cockpit Association, the pilot shortage in Europe reached critical levels in 2023, with some airlines operating with reduced schedules due to insufficient staffing. Training institutions reported a backlog in pilot certifications, as flight schools faced capacity constraints and regulatory hurdles. Simultaneously, labor unrest has intensified, with strikes becoming increasingly common across major European carriers. As per Eurofound, 2023 saw a 40% increase in aviation-related industrial actions compared to the previous year, driven by disputes over wages, working conditions, and post-pandemic restructuring efforts. Ground handling and air traffic control shortages have also contributed to widespread flight disruptions. Airlines have responded by offering signing bonuses, accelerating recruitment drives, and investing in automation to mitigate human resource gaps. However, resolving these issues requires long-term strategic planning, enhanced training partnerships, and improved labor relations to restore stability and efficiency across the aviation ecosystem.

Financial Volatility and High Operating Costs

Financial volatility and escalating operating costs continue to pose a formidable challenge for the Europe aviation market, which is threatening the profitability and sustainability of airlines even as passenger demand rebounds. The industry faces mounting pressures from fluctuating fuel prices, high debt burdens accumulated during the pandemic, and rising infrastructure levies imposed by airport authorities. According to the International Air Transport Association, European airlines experienced a 22% increase in fuel costs in 2023 compared to the previous year, despite improvements in fuel hedging strategies. Jet fuel prices remained elevated due to global supply chain disruptions and geopolitical tensions, squeezing profit margins for carriers unable to fully pass on these expenses to consumers. Furthermore, the economic slowdown in several European countries has constrained discretionary spending, leading to weaker yield recovery for airlines. As per a report by McKinsey & Company, European carriers recorded an average load factor of 82% in 2023 but struggled to achieve pre-pandemic revenue per available seat kilometer (RASK) levels.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2024 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Revenue Stream, Type, Component and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | Air France KLM SA, Airbus SE, BAE Systems Plc, Collins Aerospace. |

SEGMENT ANALYSIS

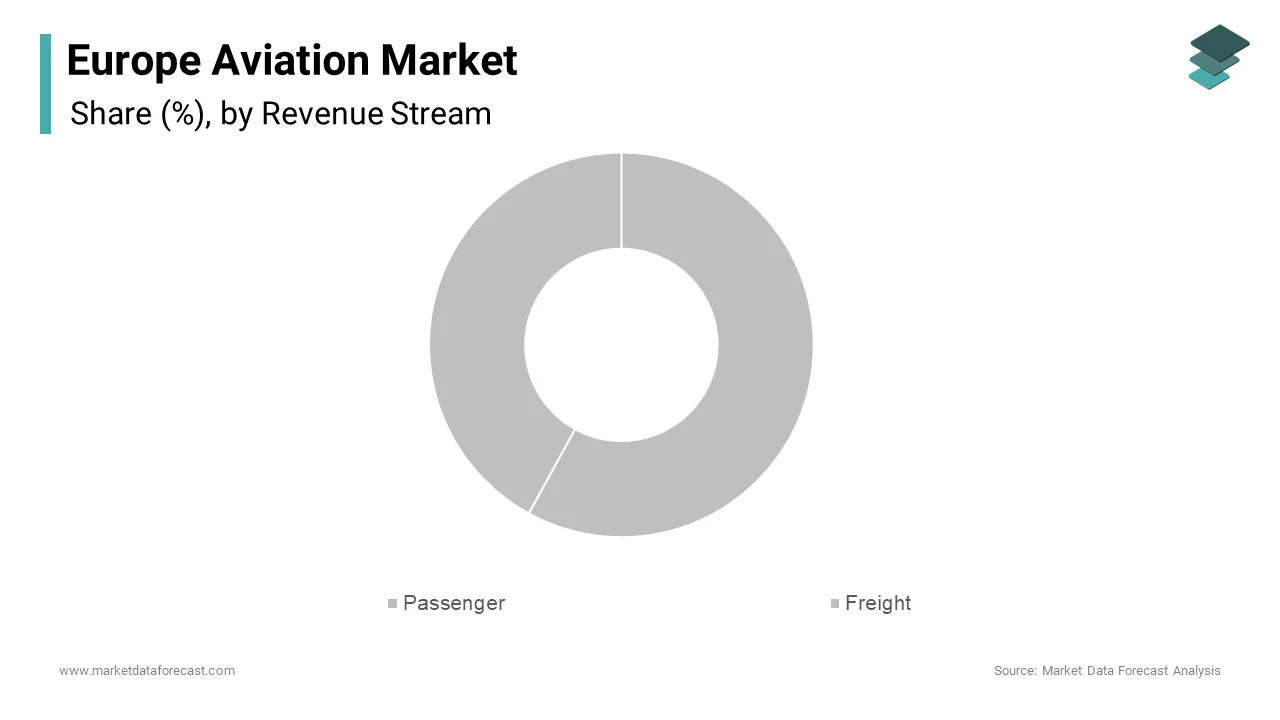

By Revenue Stream Insights

The passenger aviation segment dominated the Europe aviation market share in 2025. This overwhelming dominance is primarily due to the region’s high air travel penetration, dense population centers, and extensive connectivity between urban and regional hubs.

According to Eurostat, over 1.3 billion passengers traveled on European flights in 2023, including both intra-EU and international routes. The widespread presence of low-cost carriers such as Ryanair and easyJet has made air travel more accessible, significantly boosting demand across short-haul and medium-haul markets. Another key driver is the strong business travel culture within Europe, particularly among corporate professionals moving between major economic centers like London, Paris, Frankfurt, and Amsterdam. Additionally, tourism remains a critical pillar supporting passenger aviation. As per IATA, digitalization initiatives such as mobile check-ins, biometric boarding, and AI-driven customer service have further enhanced efficiency and convenience by contributing to sustained growth in passenger volumes despite economic fluctuations.

The freight aviation segment is lucratively growing with a CAGR of 7.2% in the next coming years. This rapid ascent is driven by surging e-commerce activity, increased cross-border trade, and the strategic importance of air cargo in pharmaceutical and high-value logistics. E-commerce expansion has been a key catalyst. As per Statista, online retail sales in the EU reached €789 billion in 2023, necessitating faster delivery networks that rely heavily on air transport. Companies like DHL Express, FedEx, and UPS have expanded their fleets and hub capacities to meet this demand.

Pharmaceutical logistics is another major contributor. Europe is home to some of the world’s largest pharmaceutical producers, and temperature-sensitive drug shipments require specialized air freight services. As per IATA, pharmaceutical cargo now accounts for over 25% of air freight value in Europe.

By Type Insights

The commercial aircraft segment held the largest share of the Europe aviation market in 2025. According to Eurostat, over 1,200 commercial aircraft operated daily in European airspace in 2023, serving more than 500 airports across the continent. Airbus, headquartered in France, remains a global leader in aircraft manufacturing, producing over 600 commercial aircraft deliveries worldwide in 2023, with a significant portion deployed across European fleets. Additionally, fleet modernization efforts have contributed to sustained demand for new commercial aircraft.

The military aircraft segment is swiftly emerging with a CAGR of 5.9% in the next coming years. This growth is primarily driven by heightened defense spending, geopolitical tensions, and modernization programs undertaken by several NATO-aligned European nations.

According to the Stockholm International Peace Research Institute (SIPRI), defense expenditures in Western Europe increased by 8.4% in 2023, with countries such as Germany, Poland, and Sweden committing to multi-billion-euro upgrades of their air forces.Poland has also been actively expanding its military aviation capabilities, signing contracts for additional F-35A fighters and C-295 transport aircraft. As per the Polish Ministry of National Defence, these acquisitions are part of a broader strategy to align with NATO readiness standards and enhance national security amid regional instability.

By Component Insights

The aircraft segment held the 54.3% of the Europe aviation market share in 2025. According to the European Union Aviation Safety Agency (EASA), the active commercial aircraft fleet in Europe exceeded 8,500 units in 2023, with Airbus leading deliveries to major carriers such as Lufthansa, Iberia, and easyJet. Leasing and financing activities further support this segment’s growth. As per Avation PLC, one of the leading aircraft lessors in Europe, lease agreements accounted for nearly 60% of new aircraft acquisitions in 2023, offering airlines flexibility amid fluctuating demand. Moreover, environmental regulations are prompting fleet renewal cycles. As per a report by McKinsey & Company, airlines are retiring older, less efficient aircraft such as the Boeing 747 and Airbus A340 in favor of newer models like the A320neo and A350XWB, which offer improved fuel efficiency and lower emissions.

The MRO segment is esteemed to grow with a CAGR of 6.4% in the next coming years. This growth is being fueled by rising aircraft utilization, aging fleets, and the increasing complexity of modern aircraft systems requiring specialized maintenance solutions. This surge is partly due to the post-pandemic rebound in air travel, which has led to higher flight frequencies and increased wear-and-tear on aircraft engines, avionics, and landing gear. Older aircraft require more frequent inspections and component replacements, driving demand for comprehensive MRO services. sssThird-party MRO providers are gaining prominence as airlines seek cost-effective alternatives to in-house maintenance. Companies like Lufthansa Technik, SR Technics, and HAECO have expanded their European operations to accommodate growing demand.

COUNTRY LEVEL ANALYSIS

Germany led the Europe aviation market with a 21.3% of share in 2025 with its status as a major economic and transportation hub. The country hosts some of the busiest airports in Europe, including Frankfurt Airport, Munich Airport, and Berlin Brandenburg Airport, which serve as key transit points for intercontinental flights. Lufthansa Group, Germany’s flagship carrier, plays a central role in shaping the country’s aviation landscape. A key driver of Germany’s aviation strength is its robust aerospace manufacturing sector. Airbus operates a major final assembly line in Hamburg, where A320 family aircraft are produced. Additionally, MTU Aero Engines and Diehl Aerospace contribute significantly to engine technology and cabin systems, respectively. The government has also supported aviation sustainability through initiatives promoting sustainable aviation fuels (SAFs) and hydrogen-powered aircraft development.

The United Kingdom held 15.3% of the Europe aviation market in 2025 with a strong presence despite post-Brexit regulatory adjustments and capacity constraints. London Heathrow remains one of the busiest international gateways, facilitating extensive connectivity between Europe, North America, and Asia. British Airways, part of the IAG group, is a major player in both passenger and cargo aviation. A notable trend in the UK aviation sector is the push toward decarbonization. As per the Department for Transport, the Jet Zero Strategy aims to achieve net-zero domestic aviation by 2040, with significant investments in SAF production and electric aircraft trials.

However, Brexit-related disruptions have impacted air service agreements and workforce mobility. As per a House of Lords report, delays in pilot training approvals and ground staff shortages have affected operational efficiency at several regional airports.

France aviation market growth is likely to grow at faster rate with its world-class airport infrastructure and a strong presence in aircraft manufacturing. Paris-Charles de Gaulle Airport serves as a major international hub, handling over 60 million passengers in 2023, according to Groupe ADP.

The French government has also taken proactive steps to promote sustainable aviation. Under the “France 2030” investment plan, €1.5 billion has been allocated to develop hydrogen-powered aircraft and advanced propulsion technologies. As per the French Ministry of Economy, these initiatives aim to position France as a global leader in zero-emission aviation.

Additionally, Air France continues to play a crucial role in the European and African markets, leveraging its hub at Charles de Gaulle to connect diverse destinations. However, the airline has faced financial pressures due to rising fuel costs and labor disputes, as noted in reports by BloombergNEF.

Spain aviation market growth is driven by its thriving tourism industry and strategic geographic location linking Europe with Africa and Latin America. Madrid-Barajas and Barcelona-El Prat airports serve as key entry points, accommodating millions of international visitors annually.

Iberia, part of the IAG group, remains the dominant airline, operating extensive domestic and international networks. As per the Spanish Ministry of Transport, the airline carried over 25 million passengers in 2023, benefiting from strong recovery in Mediterranean tourism. Low-cost carriers such as Vueling and Ryanair have also expanded rapidly, offering budget-friendly options for domestic and regional travel.

Italy aviation market growth is likely to grow with the historical significance as a cultural and business destination. Rome-Fiumicino and Milan-Malpensa are the country’s main international hubs, facilitating both leisure and corporate travel.

Alitalia’s restructuring into ITA Airways has marked a turning point for Italian aviation. Tourism remains a core driver, with over 60 million international visitors arriving in 2023, many via air. Regional airports such as Naples, Venice, and Catania have seen increased airline interest, particularly from low-cost operators seeking to capitalize on underserved markets.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the Europe Aviation Market are Air France KLM SA, Airbus SE, BAE Systems Plc, Collins Aerospace, DAHER, Dassault Aviation SA, Deutsche Lufthansa AG, Diehl Stiftung and Co. KG, Draken International, LLC, Embraer SA, GKN Aerospace Services Ltd., Honeywell International Inc., Leonardo Spa, MTU Aero Engines AG.

The competition in the Europe aviation market is intense and multifaceted, shaped by a mix of legacy carriers, low-cost airlines, aircraft manufacturers, and emerging green aviation players. Legacy airlines such as Air France-KLM, Lufthansa Group, and British Airways continue to leverage their established brand reputations, hub-and-spoke networks, and premium service offerings to maintain market share. However, they face growing pressure from agile low-cost carriers like Ryanair, easyJet, and Wizz Air, which have redefined pricing structures and route flexibility, capturing significant portions of short-haul traffic.

Aircraft manufacturers such as Airbus and Boeing compete not only on technological innovation but also on sustainability credentials, as the industry shifts toward hydrogen propulsion, electric aircraft, and sustainable aviation fuels. Additionally, new entrants and startups are disrupting traditional aviation models with urban air mobility and hybrid-electric aircraft development.

On the ground, MRO providers, airport operators, and cargo logistics firms are also engaged in fierce competition, striving to offer more efficient, cost-effective, and environmentally responsible solutions. As regulatory scrutiny intensifies and consumer preferences evolve, the race for differentiation through innovation, service excellence, and decarbonization efforts is accelerating across all segments of the European aviation market.

Top Players in the Market

Airbus (France/Germany)

Airbus is a global leader in commercial and military aircraft manufacturing, with its headquarters spread across France and Germany. The company plays a central role in shaping the European aviation landscape through its innovative aircraft designs, including the A320neo, A350, and A380 series. Airbus has been instrumental in advancing sustainable aviation technologies, such as hydrogen-powered flight concepts and fuel-efficient engines. Its collaboration with European governments and research institutions supports the continent’s transition toward greener air travel.

Lufthansa Group (Germany)

As one of Europe’s largest airline groups, Lufthansa operates multiple carriers including Swiss, Austrian Airlines, and Eurowings, offering extensive regional and international connectivity. The group contributes significantly to cargo logistics, passenger services, and aircraft maintenance through its subsidiary Lufthansa Technik. Lufthansa continues to influence the market by integrating digital transformation into customer service, investing in sustainable aviation fuels, and optimizing fleet efficiency to align with environmental regulations.

International Airlines Group (IAG) (United Kingdom/Spain)

Formed through the merger of British Airways and Iberia, IAG is a major force in the European aviation sector. It also owns low-cost carrier LEVEL and regional operator Aer Lingus, providing a diversified portfolio across premium and budget travel segments. IAG actively participates in industry sustainability initiatives and has committed to achieving net-zero carbon emissions by 2050. Its strategic expansion and focus on hybrid business models continue to reinforce its competitive edge across Europe.

Top strategies used by the key market participants

One of the primary strategies adopted by key players in the Europe aviation market is fleet modernization and technological innovation. Airlines and manufacturers are investing heavily in next-generation aircraft equipped with advanced aerodynamics, lightweight materials, and fuel-efficient propulsion systems to meet evolving environmental standards and reduce operational costs.

Another crucial strategy involves strengthening partnerships and alliances to enhance route networks and improve cost-sharing mechanisms. Major carriers are engaging in codeshare agreements, joint ventures, and interline partnerships to expand their reach while maintaining financial stability amid fluctuating demand and regulatory changes.

Companies are prioritizing digital transformation to optimize operations and elevate customer experience. This includes implementing AI-driven revenue management systems, mobile check-in platforms, biometric boarding, and predictive maintenance tools.

RECENT HAPPENINGS IN THE MARKET

In February 2024, Airbus launched a new hydrogen technology demonstrator program aimed at accelerating the development of zero-emission aircraft by reinforcing its prominence in sustainable aviation innovation within Europe.

In May 2024, Lufthansa introduced a revised corporate travel booking platform integrated with real-time carbon emission tracking, enhancing transparency and supporting businesses in meeting sustainability goals.

In July 2024, International Airlines Group announced a strategic restructuring of its regional operations by consolidating Aer Lingus and LEVEL under a unified fleet management system to improve cost efficiency and route optimization.

In September 2024, Rolls-Royce partnered with easyJet to test hydrogen-powered jet engine technology at a UK-based research facility, marking a significant step toward cleaner propulsion systems for future commercial flights.

In November 2024, ITA Airways signed a long-term alliance agreement with Air France-KLM and Delta Air Lines by expanding code-sharing options and improving connectivity between European and transatlantic routes.

MARKET SEGMENTATION

This research report on the europe aviation market has been segmented and sub-segmented into the following categories.

By Revenue Stream

- Passenger

- Freight

By Type

- Commercial Aircraft

- Military Aircraft

- General Aircraft

By Component

- Aircraft

- MRO

- Ground Handling Services

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe.

Frequently Asked Questions

What role do low-cost carriers play in the European aviation market?

Low-cost carriers like Ryanair, easyJet, and Wizz Air have significantly disrupted the market by offering affordable travel options. They now command a large share of short-haul flights and are expanding their networks to underserved routes.

What is the impact of geopolitical tensions on European aviation?

Conflicts like the Russia-Ukraine war have affected flight routes, increased fuel prices, and restricted access to airspace, leading to higher operational costs and route adjustments.

How is digitalization transforming aviation in Europe?

Airlines and airports are adoptingn are AI and automation for operations and customer service Biometric check-ins Smart baggage handling Real-time analytics for flight and crew management

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com