Europe Bag Filter Market Size, Share, Trends & Growth Forecast Report – Segmented By Type, Filter Media, Application, End User, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Bag Filter Market Report Summary

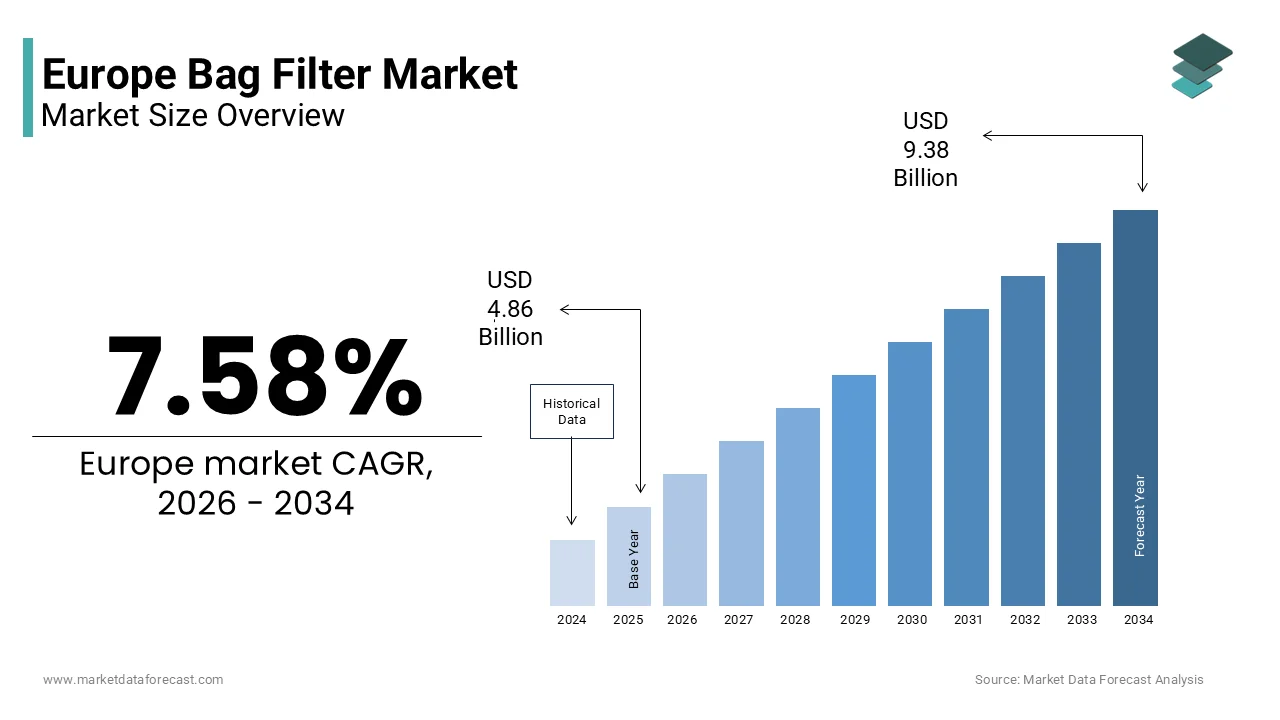

The Europe bag filter market was valued at USD 4.86 billion in 2025, is estimated to reach USD 5.23 billion in 2026, and is projected to reach USD 9.38 billion by 2034, growing at a CAGR of 7.58% during the forecast period from 2026 to 2034. The growth of the Europe bag filter market is driven by stringent environmental regulations, increasing industrial air pollution control requirements, and growing investments in sustainable manufacturing practices. Bag filters are widely used across industries to improve air quality, reduce particulate emissions, and ensure compliance with emission standards. Additionally, the expansion of power generation, cement, metal processing, chemical, and pharmaceutical industries is further supporting market growth across Europe.

Key Market Trends

-

Stringent environmental regulations on industrial emissions are driving the adoption of advanced bag filtration systems across Europe.

-

Rising investments in industrial air pollution control technologies are supporting market growth.

-

Increasing demand for energy-efficient and high-performance filtration solutions is encouraging product innovation.

-

Growing industrialization in sectors such as cement, power generation, chemicals, and metals is expanding the application of bag filters.

-

Advancements in filter media technologies are improving filtration efficiency, durability, and operational performance.

Segmental Insights

-

Based on type, the pulse jet bag filters segment dominated the Europe bag filter market in 2025. The segment's leadership is attributed to its high filtration efficiency, continuous operation capability, low maintenance requirements, and widespread adoption across industrial dust collection applications.

-

Based on filter media, the non-woven segment held the largest share of the Europe bag filter market in 2025. The segment's dominance is driven by its superior dust retention capacity, high filtration efficiency, durability, and suitability for a wide range of industrial environments.

-

Based on application, the dust control segment accounted for the largest share of the Europe bag filter market in 2025. The segment's growth is supported by increasing industrial efforts to control airborne particulate emissions, improve workplace safety, and comply with stringent environmental regulations.

Regional Insights

-

The Europe bag filter market is witnessing strong growth due to rising environmental awareness, strict emission control regulations, and increasing adoption of advanced industrial filtration technologies.

-

Germany dominated the Europe bag filter market in 2025. The country's leadership is supported by its strong industrial manufacturing base, stringent environmental compliance standards, expanding automotive and chemical industries, and continuous investments in air pollution control technologies.

-

France remains a significant market due to increasing industrial modernization, growing investments in sustainable manufacturing, and strict environmental policies.

Competitive Landscape

The Europe bag filter market is highly competitive, with manufacturers focusing on advanced filtration technologies, product innovation, and sustainable air pollution control solutions to strengthen their market positions. Companies are investing in research and development, strategic partnerships, and expansion of high-performance filtration product portfolios to meet the evolving requirements of industrial emission control across multiple end-use industries. Key players operating in the Europe bag filter market include Donaldson Company Inc., Parker Hannifin Corporation, Camfil AB, Nederman Holding AB, AAF International, Thermax Limited, Babcock & Wilcox Enterprises, Mitsubishi Power, Freudenberg Filtration Technologies SE & Co. KG, Eaton Corporation, and Siemens AG.

Europe Bag Filter Market Size

The Europe bag filter market size was valued at USD 4.86 billion in 2025 and is projected to reach USD 9.38 billion by 2034 from USD 5.23 billion in 2026, growing at a CAGR of 7.58%.

Bag filters are industrial filtration systems that utilize fabric bags to capture particulate matter from gas streams in various manufacturing processes. These systems are critical components in air pollution control strategies, designed to remove dust, smoke, and other fine particles before emissions are released into the atmosphere. The operational mechanism involves forcing contaminated air through porous filter media, where particles are trapped on the surface while clean air passes through. This technology is widely deployed across sectors such as cement production, power generation, metal processing, and chemical manufacturing. According to the European Environment Agency, industrial facilities remain significant sources of particulate matter emissions, with the industrial sector contributing approximately 11% of total PM10 emissions in the region. The stringent regulatory landscape enforced by the European Union mandates strict adherence to emission limits, driving the continuous adoption and upgrading of filtration technologies. As per the Industrial Emissions Directive, large combustion plants and industrial installations must employ best available techniques to minimize environmental impact, positioning bag filters as a preferred solution due to their high efficiency rates exceeding 99%. The transition towards cleaner industrial practices is further supported by the European Green Deal, which aims for zero pollution by 2050. This regulatory pressure combined with the need for operational efficiency and worker safety ensures sustained demand for advanced bag filtration systems across the continent. The market is characterized by a focus on durability, energy efficiency, and compliance with evolving environmental standards.

MARKET DRIVERS

Stringent Environmental Regulations Mandating Emission Control

The implementation of rigorous environmental regulations across the European Union is a key factor propelling the expansion of the European bag filter market. The Industrial Emissions Directive establishes strict limit values for particulate matter emissions from various industrial sectors, compelling operators to install high efficiency filtration systems. According to the European Commission, non-compliance with these directives can result in substantial financial penalties and operational shutdowns, creating a strong incentive for industries to invest in reliable air pollution control technologies. The directive specifically targets sectors such as cement, lime, and magnesium oxide production, where particulate emissions are prevalent. Data from the European Environment Agency indicates that while overall industrial emissions have decreased, specific hotspots still require targeted interventions to meet local air quality standards. Bag filters are recognized as a best available technique under the directive due to their ability to achieve emission levels typically below 10 mg per cubic meter. This regulatory framework not only drives new installations but also necessitates the retrofitting of existing systems with advanced filter media to maintain compliance. Furthermore, national action plans in countries like Germany and France impose additional local restrictions that often exceed EU minimum requirements. As per industry assessments, the fear of regulatory sanctions and the desire to maintain social license to operate drive continuous investment in filtration infrastructure. This legal mandate ensures a steady demand for bag filters as industries strive to align their operations with the European Green Deal objectives for a toxic free environment.

Expansion of Industrial Manufacturing and Infrastructure Projects

The ongoing expansion of industrial manufacturing activities and large scale infrastructure projects across Europe generates sustained demand for bag filter systems to manage construction and production related dust, which is further contributing to the regional market growth. The post pandemic recovery has spurred significant investment in construction, renewable energy infrastructure, and manufacturing facilities, all of which produce substantial particulate matter during operation. According to Eurostat, the construction sector in the European Union experienced a moderate recovery trend, contributing approximately 5.5% to the total gross value added of the region in recent years. This surge in activity increases the volume of airborne dust containing silica, cement, and other harmful particles, necessitating effective filtration solutions to protect worker health and surrounding communities. Bag filters are extensively used in cement plants, which are essential for supplying materials for these infrastructure projects. The European Cement Association reports that cement production remains a key industrial activity, with EU27 production exceeding 160 million tonnes annually, each requiring robust emission control systems. Additionally, the push for domestic manufacturing resilience under the EU Industrial Strategy has led to the establishment of new production units in sectors such as steel and chemicals. These facilities integrate bag filters as standard equipment to comply with environmental permits. As per market observations, the correlation between industrial output growth and filtration system procurement is direct, as higher production volumes lead to increased particulate generation. This industrial expansion ensures a consistent baseline demand for bag filters, supporting market stability and growth across the region.

MARKET RESTRAINTS

High Initial Capital Investment and Maintenance Costs

The substantial initial capital expenditure required for installing bag filter systems acts as a significant restraint, particularly for small and medium sized enterprises operating on tight margins. High efficiency bag filters involve complex engineering, specialized filter media, and sophisticated cleaning mechanisms such as pulse jet systems, all of which contribute to elevated upfront costs. According to industry cost analyses, the installation of a comprehensive bag house system can range from hundreds of thousands to millions of euros depending on capacity and specification. For smaller industrial players, this financial burden can be prohibitive, leading them to delay upgrades or opt for less effective alternatives. Beyond the initial investment, the ongoing maintenance costs pose a continuous financial challenge. Filter bags have a limited lifespan and require regular replacement, typically every 1 to 3 years, depending on operating conditions and abrasion levels. The cost of replacement bags, along with labor for installation and disposal of spent filters, adds to the operational expenditure. As per facility management reports, maintenance can account for up to 20% of the total lifecycle cost of filtration systems. Additionally, the energy consumption associated with maintaining differential pressure across the filters contributes to higher utility bills. Industries facing economic uncertainty may prioritize short term cost savings over long term environmental compliance, slowing the adoption rate. This economic constraint is particularly evident in sectors with low profit margins, where the return on investment for advanced filtration systems is perceived as too slow to justify the immediate outlay.

Operational Limitations in High Temperature and Humid Conditions

Bag filters face inherent operational limitations when exposed to extreme temperatures and high humidity levels, restricting their applicability in certain industrial processes, which is further impeding the expansion of the European bag filter market. Standard filter media made from synthetic fibers such as polyester or polypropylene have temperature thresholds that, if exceeded, can lead to material degradation, shrinkage, or melting. According to technical specifications from major manufacturers, polyester bags typically withstand temperatures up to 135°C, while more expensive materials like PTFE can handle up to 260°C. Industries such as steel production and waste incineration often generate flue gases at temperatures exceeding these limits, requiring costly pre cooling systems or specialized high temperature media. High humidity presents another challenge, as moisture can cause dust particles to adhere to the filter surface, leading to blinding or clogging. This phenomenon increases pressure drop across the filter, reducing airflow efficiency and increasing energy consumption. As per operational case studies, humid conditions can reduce filter life by up to 50% due to accelerated chemical attack and mechanical stress. The need for additional equipment such as heat exchangers or humidity control systems adds complexity and cost to the filtration setup. In regions with variable weather conditions, maintaining optimal operating parameters becomes difficult, leading to inconsistent performance. These technical constraints limit the universal adoption of bag filters, forcing industries with harsh process conditions to consider alternative technologies such as electrostatic precipitators, thereby restraining market growth in specific high temperature segments.

MARKET OPPORTUNITIES

Integration of Smart Monitoring and IoT Technologies

The integration of Internet of Things sensors and smart monitoring technologies into bag filter systems presents a significant opportunity for the European bag filter market expansion. Modern bag filters equipped with digital sensors can continuously monitor parameters such as differential pressure, temperature, and flow rate, providing real time data to facility managers. According to industry trends, the adoption of Industry 4.0 principles in environmental control systems is accelerating, with over 30% of new installations featuring smart connectivity options. This data driven approach allows for precise optimization of cleaning cycles, reducing energy consumption and extending filter life. Predictive analytics can identify potential failures before they occur, minimizing unplanned downtime and maintenance costs. As per technology providers, smart filters can reduce maintenance expenses by up to 25% through optimized scheduling and early fault detection. The ability to remotely monitor multiple filtration units from a central dashboard enhances operational oversight for large industrial complexes. Furthermore, digital records of emission performance facilitate easier compliance reporting and auditing, addressing regulatory requirements efficiently. The European Union’s support for digital transformation in industry provides funding and incentives for adopting such technologies. As manufacturers develop more affordable and robust sensor solutions, the penetration of smart bag filters is expected to rise. This technological evolution transforms bag filters from passive equipment into active assets that contribute to overall plant efficiency, creating new value propositions for customers and driving market differentiation.

Growing Demand in Renewable Energy and Waste to Energy Sectors

The expanding renewable energy sector, particularly biomass power generation and waste to energy facilities offers substantial growth opportunities for the bag filter market in Europe. As Europe transitions away from fossil fuels, the number of biomass plants and waste incineration facilities is increasing to meet energy demands and manage waste sustainably. According to the European Biomass Association, biomass energy production has grown steadily, with thousands of plants operating across the continent. These facilities generate flue gases containing fine particulate matter, ash, and other pollutants that require efficient filtration before release. Bag filters are ideally suited for these applications due to their high collection efficiency for submicron particles. Similarly, waste to energy plants, which are crucial for circular economy initiatives, rely heavily on advanced air pollution control systems to handle complex and variable waste streams. As per the Confederation of European Waste to Energy Plants, there are over 500 such facilities in Europe, each requiring robust filtration solutions to comply with strict emission standards. The unique composition of biomass and waste emissions necessitates specialized filter media resistant to chemical corrosion and abrasion, creating niche opportunities for manufacturers. Government policies promoting renewable energy and waste reduction provide financial support and regulatory backing for these sectors. As investment in green energy infrastructure continues to rise, the demand for specialized bag filters tailored to these applications will expand, offering a lucrative avenue for market participants to diversify their portfolios.

MARKET CHALLENGES

Competition from Alternative Filtration Technologies

Bag filters face intense competition from alternative air pollution control technologies such as electrostatic precipitators and ceramic filters, which offer distinct advantages in specific applications, which is a significant challenge to the European bag filter market growth. Electrostatic precipitators are often preferred in large scale power plants and heavy industries due to their lower pressure drop and ability to handle high temperature gases without cooling. According to comparative studies, electrostatic precipitators can be more cost effective for very large gas volumes, despite higher initial capital costs. Ceramic filters, although more expensive, offer superior durability and resistance to harsh chemical environments, making them suitable for extreme industrial conditions. The choice between these technologies depends on factors such as particle size, gas volume, temperature, and chemical composition, leading to a fragmented market where bag filters do not always dominate. As per industry experts, the decision making process is highly technical, and customers often opt for hybrid systems or alternatives based on specific process requirements. The continuous innovation in competing technologies, such as improved electrode designs for precipitators, further challenges the market position of bag filters. Manufacturers must constantly innovate to highlight the advantages of bag filters, such as higher efficiency for fine particles and lower sensitivity to resistivity changes. This competitive landscape requires significant investment in research and development to maintain relevance, posing a challenge for companies with limited resources. The existence of viable alternatives means that bag filter providers must carefully target segments where their technology offers clear superiority.

Supply Chain Disruptions and Raw Material Volatility

The bag filter market in Europe is vulnerable to supply chain disruptions and volatility in raw material prices, which can impact production schedules and profitability. Key materials used in filter media, such as synthetic polymers, fiberglass, and specialty chemicals, are subject to global market fluctuations. According to commodity price indices, the cost of raw materials like polypropylene and polyester has experienced significant variability due to factors such as energy prices and geopolitical tensions. These fluctuations make it difficult for manufacturers to maintain stable pricing and margin structures. Additionally, the reliance on global supply chains for specialized components and fabrics exposes the market to logistical bottlenecks. Recent events have highlighted the fragility of these networks, with delays in shipping and availability affecting production timelines. As per manufacturing surveys, lead times for custom filter bags have increased, causing project delays for end users. The shortage of skilled labor for installation and maintenance further exacerbates these challenges, limiting the capacity to meet surging demand. European manufacturers also face competition from lower cost imports, which can distort market dynamics and pressure local producers. The need to balance cost competitiveness with quality and compliance adds complexity to strategic planning. Companies must develop resilient supply chain strategies, including local sourcing and inventory buffering, to mitigate these risks. However, these measures often increase operational costs, challenging the overall economic viability of market participants in a price sensitive environment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.58% |

| Segments Covered | By Type, Filter Media, Application, End User, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Donaldson Company Inc., Parker Hannifin Corporation, Camfil AB, Nederman Holding AB, AAF International, Thermax Limited, Babcock & Wilcox Enterprises, Mitsubishi Power, Freudenberg Filtration Technologies SE & Co. KG, Eaton Corporation, and Siemens AG. |

SEGMENTAL ANALYSIS

By Type Insights

The pulse jet bag filters segment dominated the market by capturing the highest share of the European market in 2025 due to their ability to clean filter bags while the system remains in operation, ensuring uninterrupted industrial processes. This cleaning mechanism uses short bursts of compressed air to dislodge dust cakes from the filter media, maintaining low pressure drop and high filtration efficiency. According to engineering standards, pulse jet systems can achieve cleaning cycles as frequent as every few seconds, which is critical for industries with high dust loading such as cement and power generation. The continuous operation capability minimizes downtime and maximizes production throughput, making it the preferred choice for large scale facilities. As per industry benchmarks, pulse jet systems maintain collection efficiencies above 99.9% even under variable load conditions, ensuring consistent compliance with strict European emission limits. The modular design of pulse jet collectors allows for easy expansion and maintenance, reducing lifecycle costs for operators. The technology’s adaptability to various filter media types further enhances its versatility across different industrial applications. Manufacturers prioritize pulse jet designs because they offer the best balance between performance, energy consumption, and operational reliability. This technical superiority drives widespread adoption in sectors where process continuity is paramount, solidifying its position as the leading segment in the regional market.

On the other side, the reverse air bag filters segment is projected to register the highest CAGR of 7.5% over the forecast period owing to their suitability for high temperature and abrasive industrial applications. This cleaning method uses a gentle reverse flow of air to collapse the bags and dislodge dust, which causes less mechanical stress on the filter media compared to pulse jet or shaker systems. According to technical specifications, reverse air systems are ideal for handling flue gases at temperatures exceeding 200°C, common in steel production and waste incineration. The gentle cleaning action preserves the integrity of fragile filter media such as fiberglass, which is often required for high temperature filtration. For instance, reverse air filters demonstrate superior longevity in environments with highly abrasive dust particles, reducing the frequency of bag replacements. This durability is crucial for industries operating in harsh conditions where maintenance access is difficult or costly. The ability to handle large gas volumes with stable pressure drops make reverses air systems attractive for modernization projects in heavy industries. As European industries upgrade aging infrastructure to meet newer environmental standards, the demand for robust and durable filtration solutions like reverse air systems is increasing. This specific niche application drives the rapid growth of the segment despite the overall dominance of pulse jet technology in general applications.

By Filter Media Insights

The non-woven segment had the major share of the European bag filter market in 2025 due to its superior ability to capture fine particulate matter with high efficiency. Unlike woven media, non-woven fabrics consist of fibers bonded together mechanically, chemically, or thermally, creating a dense structure that traps particles on the surface rather than within the depth of the fabric. According to filtration studies, non-woven media can achieve efficiency levels of 99.9% for particles as small as 1 micron, making it ideal for meeting stringent European air quality standards. This surface filtration mechanism allows for easier cleaning and lower pressure drops compared to depth filtration methods. As per industry data, the majority of new bag filter installations in Europe specify non-woven media due to its consistent performance and reliability. The versatility of non-woven media allows it to be manufactured from various synthetic fibers such as polyester, polypropylene, and PTFE, catering to different chemical and temperature requirements. This adaptability ensures that non-woven media can be used across a wide range of industries including pharmaceuticals, food processing, and chemicals. The demand for high purity air in these sectors drives the preference for non-woven media. Its dominance is further reinforced by the availability of specialized coatings and treatments that enhance resistance to moisture, oil, and chemical attack, extending service life and performance.

However, the glass fiber segment is emerging as the fastest growing segment in the Europe bag filter market and is projected to expand at a CAGR of 8.08% over the forecast period owing to its exceptional resistance to extreme temperatures and chemical corrosion. Glass fiber can withstand continuous operating temperatures up to 260°C, which is making it indispensable for high temperature applications such as asphalt production, carbon black manufacturing, and waste incineration. According to material science data, glass fiber maintains its structural integrity and filtration efficiency even in aggressive chemical environments where synthetic fibers would degrade rapidly. This durability is crucial for industries dealing with acidic or alkaline flue gases, which are common in chemical processing and metal smelting. For instance, the increasing complexity of industrial waste streams requires more robust filtration materials, boosting demand for glass fiber media. The ability of glass fiber to handle thermal shocks without shrinking or melting provides an added layer of safety and reliability for plant operators. This technical superiority addresses specific pain points in heavy industries, driving adoption despite higher costs. The growing emphasis on handling hazardous emissions safely further propels the growth of glass fiber media. As industries push the boundaries of process conditions to improve efficiency, the need for high performance media like glass fiber becomes more pronounced, which is fuelling its rapid market expansion.

By Application Insights

The dust control segment led the market by capturing the leading share of the European market in 2025. The growth of the dust control segment in the European market can be attributed to the mandatory occupational health and safety standards that require strict control of airborne particulates in industrial workplaces. Exposure to respirable dust, particularly silica and wood dust, poses serious health risks such as silicosis and cancer, prompting rigorous enforcement of exposure limits. According to the European Agency for Safety and Health at Work, millions of workers are exposed to hazardous dust annually, necessitating effective engineering controls like bag filters. The Carcinogens and Mutagens Directive sets binding limit values for workplace exposure, compelling employers to install high efficiency filtration systems. Bag filters are widely recognized as the most effective technology for capturing fine dust at source points such as grinding, cutting, and conveying operations. As per safety audits, facilities with comprehensive dust control systems report significantly lower incidence rates of respiratory illnesses among workers. This health imperative drives continuous investment in dust collection infrastructure across sectors like woodworking, metal fabrication, and mining. The legal liability associated with non-compliance further motivates companies to prioritize dust control. The widespread awareness of health risks among employees and unions also pressures management to maintain high standards. This strong regulatory and social mandate ensures that dust control remains the largest application area for bag filters in the region.

On the other side, the air pollution control segment is the fastest growing application segment in the Europe bag filter market and is expected to register a CAGR of 9.22% over the forecast period owing to the increasingly stringent emission limits for industrial flue gases. The European Green Deal and the Zero Pollution Action Plan aim to reduce air pollution to levels no longer harmful to human health, imposing tighter restrictions on particulate matter, sulfur oxides, and nitrogen oxides. According to the European Environment Agency, industrial combustion remains a major source of air pollutants, requiring advanced control technologies. Bag filters are essential for capturing particulate matter from flue gases in power plants, incinerators, and chemical factories. The requirement to meet emission levels below 10 mg per cubic meter drives the adoption of high efficiency bag filters with specialized media. As per regulatory updates, new permits for industrial facilities often mandate the use of best available techniques, with bag filtration being a preferred option. The pressure to reduce environmental impact and avoid penalties accelerates investment in air pollution control systems. This regulatory push is complemented by public demand for cleaner air, creating a strong social license for strict enforcement. The combination of legal mandates and societal expectations fuels the rapid growth of this application segment.

REGIONAL ANALYSIS

Germany Bag Filter Market Analysis

Germany dominated the bag filter market in Europe in 2025 with the largest share of the regional market and is likely to maintain its market-leading position and experience steady growth in adoption over the next few years due to its focus on high-end industrial engineering. The country is home to major cement, chemical, and automotive manufacturers that require advanced air pollution control systems. According to the Federal Ministry for the Environment, Germany has some of the strictest emission limits in Europe, compelling industries to invest in high efficiency filtration technologies. The Energiewende policy, which promotes renewable energy, has led to the construction of numerous biomass and waste to energy plants, further boosting demand for bag filters. German engineering firms are also leaders in the design and manufacture of filtration systems, contributing to domestic market strength. The country’s focus on Industry 4.0 has spurred the adoption of smart bag filters with IoT capabilities, enhancing operational efficiency. The continuous modernization of existing industrial facilities to meet evolving standards ensures sustained demand. The strong regulatory framework and technological leadership position Germany as the primary driver of the regional market.

France Bag Filter Market Analysis

France is expected to witness significant growth in the coming years as it accelerates its industrial modernization and energy transition strategies. The country’s commitment to reducing carbon emissions has led to increased investment in biomass energy and waste management facilities, which are key users of bag filters. According to the French Ministry of Ecological Transition, national air quality plans mandate strict control of industrial particulate emissions, driving adoption of filtration systems. The cement and steel industries in France are undergoing modernization to comply with EU directives, creating opportunities for bag filter suppliers. The presence of major international filtration companies in France fosters innovation and local production. The focus on circular economy practices, particularly in waste to energy, ensures long term growth potential. The combination of regulatory pressure and industrial diversification makes France a key market for bag filters in Western Europe.

Italy Bag Filter Market Analysis

Italy is set to continue its trajectory of upgrading industrial plants and investing in sustainable energy projects over the next few years. The country has a large number of small and medium sized enterprises in the manufacturing sector that are increasingly adopting filtration systems to comply with environmental norms. According to the Italian National Institute for Environmental Protection and Research, industrial emissions are closely monitored, and non compliant facilities face strict penalties. The renovation of older industrial plants to meet EU standards is a major driver for bag filter sales. Italy’s strong focus on design and efficiency has led to the adoption of compact and high performance filtration units. The growth of the waste to energy sector in northern Italy further boosts demand. The combination of traditional industrial strength and emerging green energy projects positions Italy as a dynamic market for bag filters in Southern Europe.

United Kingdom Bag Filter Market Analysis

The United Kingdom maintains a steady presence in the Europe bag filter market, influenced by its post Brexit environmental policies and strong industrial heritage. The UK’s Net Zero strategy has accelerated the closure of coal plants and the expansion of biomass and waste to energy facilities, driving demand for advanced filtration. According to the Department for Environment, Food and Rural Affairs, industrial air quality standards remain aligned with EU levels, ensuring continued need for compliance technologies. The manufacturing sector, particularly in the north of England, relies on bag filters for dust control in metal and chemical processing. The UK’s focus on innovation has led to the adoption of smart filtration solutions. The emphasis on sustainable industrial practices and the growth of renewable energy infrastructure support market stability. The regulatory clarity and investment in green technologies ensure that the UK remains a significant market for bag filters.

Spain Bag Filter Market Analysis

Spain is poised to expand its market presence significantly as it transitions its cement and waste sectors toward greener operations over the next few years. The country has invested heavily in wind and solar power, but also in biomass and waste to energy plants to manage agricultural and municipal waste. According to the Spanish Ministry for Ecological Transition, industrial emission controls are being strengthened to meet EU targets. The cement industry in Spain is a major consumer of bag filters due to the high dust loads generated during production. The modernization of industrial facilities to improve energy efficiency and reduce emissions is a key driver. The geographic concentration of industrial activity in Catalonia and the Basque Country creates localized demand hubs. The push for circular economy practices supports the growth of waste management facilities, further boosting demand for filtration systems. Spain’s strategic location and industrial base make it a vital market in Southern Europe.

COMPETITIVE LANDSCAPE

The competition in the Europe bag filter market is characterized by the presence of established global giants and specialized regional manufacturers who compete on technology, quality, and service. Global players leverage their brand recognition, extensive distribution networks, and financial resources to offer comprehensive solutions across multiple industries. They focus on innovation and digital integration to maintain a competitive edge. Regional manufacturers often compete by offering customized solutions, faster delivery times, and personalized customer support tailored to local market needs. The market is moderately fragmented with no single player dominating all segments. Competition is intense in terms of product performance, energy efficiency, and compliance with strict environmental regulations. Price competition exists but is secondary to value propositions such as total cost of ownership and reliability. Companies frequently engage in strategic alliances and acquisitions to expand their technological capabilities and geographic reach. The emphasis on sustainability and smart technologies is reshaping the competitive landscape, forcing participants to continuously innovate. Customer loyalty is driven by consistent performance and after sales support, making service quality a key differentiator in this mature yet evolving market.

KEY MARKET PLAYERS

Some of the notable key players in the Europe bag filter market are

- Donaldson Company Inc.

- Parker Hannifin Corporation

- Camfil AB

- Nederman Holding AB

- AAF International

- Thermax Limited

- Babcock & Wilcox Enterprises

- Mitsubishi Power

- Freudenberg Filtration Technologies SE & Co. KG

- Eaton Corporation

- Siemens AG

Top Players in the Market

- Donaldson Company Inc maintains a strong presence in the Europe bag filter market through its comprehensive portfolio of industrial filtration solutions tailored for diverse manufacturing sectors. The company leverages its extensive research and development capabilities to innovate high efficiency filter media that meet stringent European emission standards. Donaldson focuses on providing customized dust collection systems for industries such as cement, power generation, and metal processing. Recent actions include the expansion of its manufacturing facilities in Germany to enhance local supply chain resilience and reduce delivery times. The company actively engages in strategic partnerships with engineering firms to integrate smart monitoring technologies into its filtration systems. By emphasizing sustainability and energy efficiency, Donaldson strengthens its reputation as a reliable partner for industrial clients seeking compliant and cost effective air pollution control solutions across the continent.

- Camfil AB is a leading provider of air filtration solutions in Europe with a significant focus on industrial bag filters and dust collection systems. The company distinguishes itself through its commitment to clean air technology and sustainable practices, aligning closely with European environmental regulations. Camfil offers a wide range of filter bags made from advanced synthetic and glass fiber materials designed for harsh industrial conditions. Recent initiatives involve the launch of new product lines featuring improved resistance to chemical corrosion and high temperatures. The company invests heavily in digital tools that allow customers to monitor filter performance and optimize maintenance schedules. Camfil’s strong distribution network across Europe ensures rapid response to customer needs. Its dedication to innovation and customer service solidifies its position as a key contributor to the regional bag filter market.

- Freudenberg Filtration Technologies SE & Co. KG plays a pivotal role in the Europe bag filter market by supplying high quality filter media and complete filtration systems. The company is renowned for its expertise in non woven and woven filter fabrics that offer superior durability and filtration efficiency. Freudenberg serves a broad spectrum of industries including chemicals, pharmaceuticals, and food processing. Recent actions include the development of eco friendly filter media made from recycled materials, supporting the circular economy goals of European industries. The company collaborates with original equipment manufacturers to design integrated filtration solutions that maximize space efficiency and energy savings. Freudenberg’s focus on technical excellence and sustainability drives its growth in the region. Its ability to provide tailored solutions for complex industrial applications enhances its competitive edge and market presence.

Top Strategies Used by Key Market Participants

Key players in the Europe bag filter market primarily employ product innovation and technological advancement to differentiate their offerings and meet evolving regulatory requirements. Companies invest heavily in research and development to create advanced filter media with higher efficiency, longer lifespan, and better resistance to extreme conditions. Strategic partnerships and collaborations with engineering firms and original equipment manufacturers are common to provide integrated solutions that combine hardware and software capabilities. Expansion of manufacturing facilities and distribution networks within Europe helps companies reduce lead times and improve customer service. Many participants focus on sustainability by developing eco friendly products and optimizing energy consumption in their systems. Digitalization is another major strategy, with firms integrating Internet of Things sensors for predictive maintenance and real time monitoring. Acquisitions of specialized technology firms allow larger players to expand their product portfolios and enter new market segments. These strategies collectively help companies strengthen their market position and respond effectively to the demands of industrial customers.

Europe Bag Filter Market News

- In March 2024, Donaldson Company Inc expanded its manufacturing facility in Germany to increase production capacity for industrial bag filters. This expansion is anticipated to improve supply chain efficiency and strengthen the presence in the Central European market.

- In June 2023, Camfil AB launched a new series of high temperature filter bags designed for waste to energy applications. This launch is anticipated to address specific needs of the growing renewable energy sector and strengthen the presence in niche markets.

- In September 2023, Freudenberg Filtration Technologies introduced eco friendly filter media made from recycled materials for industrial dust collection. This innovation is anticipated to support sustainability goals of European industries and strengthen the presence in green manufacturing segments.

- In January 2024, Nederman Holding AB acquired a specialized filtration technology startup to enhance its digital monitoring capabilities. This acquisition is anticipated to integrate smart features into bag filter systems and strengthen the presence in the Industry 4.0 segment.

- In November 2023, Air Clean Systems opened a new service center in France to provide faster maintenance and support for industrial clients. This opening is anticipated to improve customer satisfaction and strengthen the presence in the Western European market.

MARKET SEGMENTATION

This research report on the Europe bag filter market has been segmented and sub-segmented based on categories.

By Type

- Pulse Jet Bag Filters

- Reverse Air Bag Filters

- Shaker Bag Filters

By Filter Media

- Woven Media

- Non-Woven Media

- Glass Fiber Media

- Others

By Application

- Dust Control

- Air Pollution Control

- Product Recovery

- Water Treatment

- Others

By End User

- Power Generation

- Cement Production

- Chemical and Petrochemicals

- Pharmaceutical and Biotech

- Food and Beverage Processing

- Mining and Metallurgy

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe Bag Filter Market?

The Europe Bag Filter Market refers to the regional industry focused on the manufacturing, distribution, and application of bag filtration systems used to remove dust, particulate matter, and contaminants from air and industrial process streams.

2. Which end-user segment dominates the Europe Bag Filter Market?

The cement and manufacturing industries account for a significant share of the market due to their high dust generation and continuous need for effective air pollution control systems.

3. What factors are driving the growth of the Europe Bag Filter Market?

The market is driven by stringent environmental regulations, increasing industrialization, rising demand for air pollution control systems, and growing investments in sustainable manufacturing practices.

4. Which industries are the major users of bag filters?

Bag filters are widely used in cement, power generation, chemicals, pharmaceuticals, food and beverage, mining, metals, pulp and paper, and waste management industries.

5. What are the different types of bag filters?

Common types include pulse jet bag filters, shaker bag filters, reverse air bag filters, and cartridge-based filtration systems designed for various industrial applications.

6. Which countries lead the Europe Bag Filter Market?

Germany, France, the United Kingdom, Italy, and Spain are among the leading markets due to their strong industrial base, strict emission standards, and advanced manufacturing sectors.

7. Why are bag filters important in industrial applications?

Bag filters improve air quality by efficiently removing dust and particulate matter, protecting worker health, enhancing equipment performance, and ensuring compliance with environmental regulations.

8. What challenges does the Europe Bag Filter Market face?

Key challenges include high installation and maintenance costs, fluctuating raw material prices, filter replacement expenses, and competition from alternative filtration technologies.

9. What are the latest trends in the Europe Bag Filter Market?

Current trends include the adoption of energy-efficient filtration systems, smart filter monitoring technologies, high-performance filter media, and sustainable filtration solutions with longer service life.

10. What is the future outlook for the Europe Bag Filter Market?

The Europe Bag Filter Market is expected to witness steady growth over the forecast period, driven by increasing environmental awareness, stricter emission regulations, technological advancements in filtration systems, and rising investments in industrial air quality management.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com