Europe Banking as a Service Market Size, Share, Trends & Growth Forecast Report, Segmented By Component (Platform, Service (Professional Service, Managed Service)), Type, Enterprise Size, End User, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis From (2026 To 2034)

Market Size, 2025

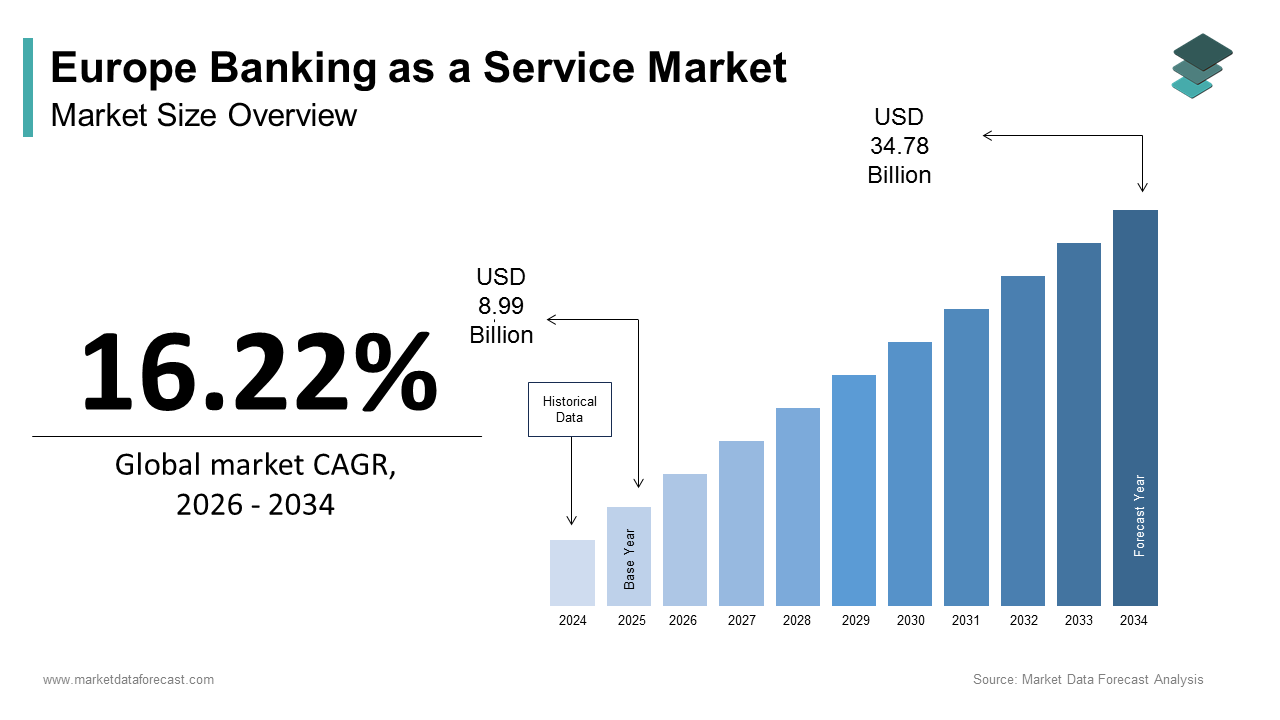

$8.99 BnMarket Estimate, 2026

$10.45 BnMarket Forecast, 2034

$34.78 BnCAGR, 2026–2034

16.22%Europe Banking as a Service Market Report Summary

The Europe banking as a service market was valued at USD 8.99 billion in 2025 and is projected to reach USD 34.78 billion by 2034, growing from USD 10.45 billion in 2026 at a CAGR of 16.22% during the forecast period. Market growth is driven by rapid digital transformation in financial services, rising demand for embedded finance, and strong adoption of API-driven banking infrastructure across Europe. Favorable open banking regulations, increasing fintech innovation, and the need for scalable, compliant banking platforms are accelerating BaaS adoption among banks, fintechs, and non-banking financial institutions. The growing shift toward modular, cloud-native banking architectures continues to strengthen the Europe banking as a service market.

Key Market Trends

- Increasing adoption of API-based banking models to enable embedded finance and faster product launches

- Strong demand for end-to-end BaaS platforms supporting payments, accounts, and compliance

- Rising participation of fintechs and NBFCs leveraging licensed banking infrastructure

- Expansion of cloud-native core banking and real-time payment capabilities

- Growing alignment of BaaS offerings with regulatory compliance and digital sovereignty initiatives

Segmental Insights

- Based on component, the platform segment dominated the Europe banking as a service market in 2025, supported by demand for integrated solutions covering payments, accounts, compliance, and reporting.

- Based on type, the API-based BaaS segment led the market in 2025, driven by flexibility, faster integration, and scalability for digital-first financial services.

- Based on enterprise size, the large enterprises segment held the majority share of 58.7% in 2025, reflecting strong adoption by established banks, large fintechs, and financial institutions.

- Based on end user, the NBFCs and fintech corporations segment dominated the market in 2025 by occupying a 63.5% share, supported bythe rapid expansion of embedded finance and digital lending models.

Regional Insights

- United Kingdom led the Europe banking as a service market in 2025 by accounting for 25.4% of the total market share, supported by a mature fintech ecosystem and progressive open banking regulations.

- Germany ranked second, driven by strong enterprise adoption and a regulatory-compliant digital banking framework.

- France remains a major market due to proactive regulatory support and alignment of BaaS with national digital sovereignty objectives.

- Netherlands witnessed steady growth, supported by its role as a digital gateway to Europe and the presence of major cloud regions certified for financial services.

- Sweden is expected to expand significantly from 2026 to 2034, driven by leadership in sustainable finance and advanced digital public infrastructure.

Competitive Landscape

The Europe banking as a service market is highly competitive and innovation-led, with providers focusing on scalable platforms, regulatory compliance, and API-driven ecosystems. Companies are strengthening their offerings through cloud-native core banking, real-time payments, and strategic partnerships with fintechs and enterprises to accelerate embedded finance adoption.

Prominent players in the Europe banking as a service market include Solaris SE, ClearBank Ltd, Banking Circle, Treezor, Modulr, Starling Bank, Adyen, Stripe, Marqeta, Thought Machine, Tink, Yapily, and Mambu.

Europe Banking as a Service Market Size

The Europe banking as a service market size was calculated to be USD 8.99 billion in 2025 and is anticipated to be worth USD 34.78 billion by 2034, growing from USD 10.45 billion in 2026 at a CAGR of 16.22% during the forecast period.

Banking as a Service (BaaS) refers to the provision of licensed banking infrastructure, such as payment processing, current accounts, card issuing, and compliance systems, via application programming interfaces to non-bank entities, including fintechs, e-commerce platforms, and corporates. This model decouples financial functionality from traditional branch-based institutions, enabling embedded finance at scale. The European BaaS ecosystem operates within a tightly regulated framework anchored by the Revised Payment Services Directive (PSD2) and the Capital Requirements Regulation, which mandate that only licensed credit institutions may provide core banking services. The European Banking Authority highlights a growing trend of non-bank entities leveraging partnerships with established financial institutions to launch branded financial products, allowing these firms to bypass the need for full banking licenses. Research emphasizes that the European Economic Area maintains a high-volume, diverse population of registered payment institutions, which reflects a heavily fragmented but highly innovative financial services market. Unlike global counterparts, Europe’s BaaS model is distinguished by its emphasis on regulatory interoperability, data sovereignty, and open yet secure architecture, principles enshrined in the EU Digital Finance Strategy and reinforced through national sandbox initiatives by authorities such as Germany’s BaFin and France’s ACPR.

MARKET DRIVERS

Mandatory Open Banking Regulations Under PSD2 Driving API Adoption

The Revised Payment Services Directive (PSD2) is a foundational driver of the Europe banking as a service market. It accomplishes this by legally mandating banks to share customer data with authorized third parties via secure APIs. The regulatory compulsion has enabled the emergence of BaaS as a compliant bridge between licensed banks and non-bank innovators. The European Banking Authority reports high levels of industry progress in deploying production-grade open APIs, reflecting widespread adoption of Open Banking across major European financial institutions. German-based Banking-as-a-Service providers are maturing, evolving from high-growth models to a focus on profitability and resilience by offering full-stack banking rails to fintech partners. French regulators are maintaining a steady, rigorous approach to licensing new payment and electronic money institutions, supporting the expansion of the embedded finance ecosystem. Unlike voluntary open banking models in other regions, Europe’s legal mandate ensures consistent technical standards, data formats, and liability frameworks, reducing integration risk and accelerating time to market for embedded finance solutions across payments, savings, and credit.

Rising Demand for Embedded Finance from Non-Financial Sectors

Non-financial enterprises across e-commerce, mobility, and gig economy sectors are increasingly embedding financial services to enhance customer retention and unlock new revenue streams. Consequently, this trend is fueling the growth of the Europe Banking-as-a-Service market. A growing majority of European small and medium enterprises conducting online sales are adopting integrated payment and payout solutions to streamline their operational workflows. Companies offer instant driver payouts via BaaS-powered wallets while online retailers such as Zalando provide buy now, pay later options through partnerships with licensed BaaS enablers like Mambu and Modulr. The European Commission’s Digital Markets Act further incentivizes this trend by requiring large online platforms to enable interoperability, which includes financial functionality. A substantial portion of European e-commerce businesses are planning to adopt BaaS infrastructure to launch proprietary, branded financial products such as loyalty wallets. This shift transforms traditional merchants into financial touchpoints, reducing dependency on legacy banks and creating a distributed financial ecosystem where BaaS providers serve as the regulated backbone, enabling speed, compliance, and scalability without capital-intensive licensing.

MARKET RESTRAINTS

Stringent and Fragmented Licensing Requirements Across EU Jurisdictions

Divergent national licensing regimes for electronic money institutions and credit institutions restrain the growth of the Europe banking as a service market. The European Central Bank, in cooperation with national authorities, requires a significant minimum capital, as mandated by the Capital Requirements Directive, for a full banking license, with the total application and approval process frequently extending over a long duration from submission to completion. National regulators impose additional supervisory standards on licensed entities, even though the passporting mechanism permits cross-member state operations. Germany’s BaFin mandates real-time liquidity monitoring, whereas Italy’s Banca d’Italia requires on-site compliance officers for BaaS providers. The European Banking Authority and the European Central Bank have highlighted that increasing complexities in ICT and cloud outsourcing, combined with strict regulatory interpretations, have led to increased scrutiny, resulting in longer, more complex licensing processes for financial institutions. As regulatory demands, such as those regarding outsourcing and IT resilience, become more stringent in the European Union, Banking-as-a-Service (BaaS) startups are facing substantial, escalating, and time-consuming operational and legal expenses to ensure compliance, requiring a large portion of their early-stage capital. Moreover, non-harmonized anti-money laundering supervision, such as varying thresholds for customer due diligence across France and Poland, complicates pan-European scaling. The licensing landscape will remain a structural bottleneck for BaaS innovation until regulatory convergence strengthens, aided by initiatives such as the proposed Financial Data Access Regulation.

Data Privacy Constraints Under GDPR Limiting Personalization and Risk Modeling

The General Data Protection Regulation imposes strict limits on the processing of personal and financial data, constraining BaaS providers’ ability to develop personalized credit scoring and dynamic risk models, which in turn hinders the expansion of the Europe banking-as-a-service market. According to sources, GDPR requires explicit user consent for each specific data use case and prohibits automated decision-making with legal or significant effects unless safeguards are implemented. This restricts BaaS platforms from leveraging alternative data, such as transaction patterns or utility payments, for inclusive credit underwriting as commonly practiced in other regions. European data regulators are increasingly penalizing financial entities that fail to secure explicit customer permission before using personal data for automated credit decisions or marketing profiles. Similarly, the European Banking Authority’s guidelines on consumer protection in embedded finance emphasized that financial personalization must not lead to discriminatory pricing. These constraints reduce the efficacy of AI-driven risk engines. Structural differences and data fragmentation in the European financial market lead to more conservative lending practices for higher-risk applicants compared to the more market-driven approach used in the United States. GDPR ensures data protection, but it simultaneously imposes, intended or not, barriers to innovation and financial inclusion in BaaS platforms.

MARKET OPPORTUNITIES

Expansion of Sustainable Finance Through BaaS-Enabled Green Accounts

The EU’s sustainable finance agenda provides a strategic opportunity for BaaS providers to power eco-conscious financial products aligned with regulatory mandates, which is predicted to boost the growth of the Europe banking as a service market. Under the EU Taxonomy and the Corporate Sustainability Reporting Directive, companies must disclose environmental impact data, which creates demand for green banking infrastructure. BaaS platforms such as Treez and Tomorrow have launched carbon tracking current accounts that automatically categorize spending by emissions intensity and offset via certified projects. The European Commission is strengthening its commitment to sustainable finance through the Digital Europe Programme by funding digital infrastructure that enables fintechs to create tools for environmental tracking and green banking services. Additionally, Article 10 of the proposed Green Bond Standard requires issuers to report fund allocation, a requirement easily fulfilled through BaaS-powered sub-accounts with immutable ledger tracking. Driven by the need for climate transition, a significant portion of European small and medium-sized enterprises are prioritizing banking partnerships that provide access to green financing and environmental, social, and governance reporting support. BaaS providers enable non-banks to comply with new regulations and differentiate their offerings in a saturated embedded finance market through pre-certified green loan origination and impact dashboards.

Integration with EU Instant Payment and Digital Euro Infrastructures

The rollout of pan-European instant payments and the impending digital euro pilot create a potential opportunity for BaaS providers to embed real-time settlement and programmable money features, which are anticipated to contribute to the expansion of the European banking as a service market. The SEPA Instant Credit Transfer scheme has seen significant growth in adoption across the euro area, driven by regulatory mandates ensuring that nearly all financial institutions are now connected to the infrastructure. BaaS enablers like Solaris and Modulr have integrated direct access to this rail, allowing their clients to offer sub-second payouts—a critical feature for gig economy and marketplace platforms. Furthermore, the ECB is advancing its digital euro project, having entered a preparatory phase to establish the technical foundation and design for a secure, programmable digital form of central bank money. BaaS providers are positioning themselves as on-ramps by developing wallet and smart contract interfaces compatible with the digital euro’s regulatory sandbox. The European Payments Council and ECB are actively collaborating with a wide range of industry participants, including Banking-as-a-Service (BaaS) platforms, to shape API standards and the framework for the digital euro. This early alignment ensures that when the digital euro launches in pilot form, BaaS clients, from neobanks to e-commerce firms, can instantly offer programmable payment features such as conditional disbursements, time-locked savings, and automated tax withholding, transforming embedded finance into a real-time programmable utility.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in API Based Banking Infrastructure

The API driven architecture central to BaS introduces expanded attack surfaces that heighten systemic cyber risk across the region’s financial ecosystem, which challenges the growth of the Europe banking as a service market. The European Union Agency for Cybersecurity reports that data security incidents within the financial sector are increasingly linked to compromised third-party suppliers, with API-related misconfigurations and authentication token leakage serving as significant, rising threats. Unlike monolithic core banking systems, BaaS relies on distributed microservices where each connection point between fintech clients and banking rails represents a potential vulnerability. Germany’s Federal Office for Information Security reported that the threat situation for digital systems remains tense, with increasing malicious activity targeting API-based payment initiation services and financial infrastructures. The complexity escalates with nested integrations; a single neobank may connect to a BaaS provider, which in turn relies on cloud infrastructure from AWS or Azure, creating multi-layer dependency chains. Few BaaS clients have the in-house expertise to audit their supply chains, despite the rigorous due diligence mandated by EBA Outsourcing Guidelines. The lack of uniform API security standards and shared threat intelligence exposes the BaaS model to widespread, compounding cyber breaches that could undermine market confidence in embedded finance.

Lack of Standardized Interoperability Protocols Across BaaS Providers

Technical fragmentation due to the absence of uniform API standards across providers, which constrains the expansion of the Europe banking as a service market. Leading European Banking-as-a-Service platforms, such as Solaris and Treezor, utilize proprietary, non-standardized data models and authentication flows. This lack of interoperability forces fintech clients to rebuild technical integrations for each new banking partner, increasing development efforts. The requirement to rebuild integrations for each banking partner significantly increases development costs for fintechs. While the Berlin Group’s NextGenPSD2 standard provides a consistent framework for regulatory compliance (payment initiation and account information), it does not cover the full spectrum of BaaS services, leaving areas like card issuance and lending fragmented. Consequently, a mobility startup launching in three EU countries may need to manage six different BaaS integrations with inconsistent error codes, latency profiles, and retry logic. The European Central Bank has acknowledged this gap and included API standardization in its roadmap, yet implementation remains voluntary. Standardization is critical; until a unified European API framework is enforced, market innovation will be hindered by redundant engineering and delayed rollouts.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 16.22% |

| Segments Covered | By Component, Type, Enterprise Size, End User, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Solaris SE, ClearBank Ltd, Banking Circle, Treezor, Modulr, Starling Bank, Adyen, Stripe, Marqeta, Thought Machine, Tink, Yapily, Mambu |

SEGMENTAL ANALYSIS

By Component Insights

The platform segment dominated the Europe banking as a service market by accounting for a substantial share in 2025. The dominance of the platform segment is driven by the foundational role platforms play as the technical and regulatory backbone enabling embedded finance. BaaS platforms provide licensed infrastructure, including current accounts, payment rails, card issuance, and compliance engines, through standardized APIs that allow non-banks to launch financial products without obtaining their own banking licenses. Driven by intense time pressures and high capital requirements, a substantial majority of fintechs entering the European market are opting to partner with Banking-as-a-Service providers rather than acquiring their own regulatory licenses. The ability of Banking-as-a-Service providers to scale is enabled by modern, cloud-based architectures, allowing single regulated entities to support a large number of fintech clients simultaneously under a unified compliance structure. Additionally, the European Commission’s Digital Finance Strategy explicitly encourages reusable financial infrastructure to reduce market fragmentation, a policy that directly favors platform standardization over fragmented service engagements. Rising regulatory demands for data sovereignty and auditability are driving, with high velocity, the adoption of GDPR-compliant, end-to-end encrypted logging platforms across the continent.

The managed services sub-segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 28 4% between 2026 and 2034 due to the rising complexity of regulatory compliance and operational risk management that non-bank clients cannot handle internally. Under the EBA’s Outsourcing Guidelines, financial institutions must ensure continuous monitoring of third-party providers, a requirement that has pushed BaaS clients to outsource not just infrastructure but ongoing compliance operations. European Banking Authority suggests that BaaS adopters in France and the Netherlands are increasingly choosing to outsource their anti-money laundering monitoring and transaction screening to managed service providers in response to stricter compliance requirements. Providers like Treez and Qonto now offer full-stack managed services, including real-time fraud detection, liquidity management, and regulatory reporting tailored to national supervisory expectations. The German Federal Financial Supervisory Authority has found that fintechs utilizing specialized, managed BaaS services generally exhibit improved compliance with Anti-Money Laundering regulations compared to those that manage their own monitoring, due to better expertise and operational control. Stricter ICT risk controls under the EU's Digital Operational Resilience Act (DORA) are driving demand for outsourced resilience services, including incident response and penetration testing. This surge in demand is expected to accelerate growth in the high-value outsourcing market.

By Type Insights

The API Based BaaS segment led the Europe banking as a service market by capturing a significant share in 2025. The leading position of the API Based BaaS segment is attributed to the regulatory and technical architecture of the European financial ecosystem, which prioritizes interoperability through standardized application programming interfaces. The Revised Payment Services Directive (PSD2) legally compels banks to expose core functionalities via secure APIs enabling third parties to initiate payments and access account data, laying the groundwork for broader BaaS adoption. Unlike monolithic core banking systems, API based models allow granular integration where fintechs can embed only the services they need, such as IBAN issuance or SEPA transfer,s without overhauling their entire tech stack. Within the EU, Banking-as-a-Service providers increasingly adopt standardized technical protocols, such as RESTful APIs and OAuth authentication, to improve developer experience and secure data sharing under regulatory oversight. The Berlin Group's NextGenPSD2 standard serves as a common framework for numerous European financial institutions, reducing integration complexity and streamlining the development of Open Banking services. This regulatory alignment, coupled with developer familiarity, makes API based BaaS the default architectural choice for embedded finance across Europe.

The cloud-based BaaS segment is expected to exhibit a noteworthy CAGR of 31.2% during the forecast period, owing to the industry’s shift toward elastic infrastructure that supports rapid scaling, security, and cost efficiency. Unlike traditional on-premises banking systems, cloud native BaaS platforms leverage hyperscalers like AWS, Azure, and Google Cloud, which offer certified financial services environments compliant with EU data residency requirements under the EU Cloud Rulebook. European regulatory bodies are increasingly outlining data protection requirements for financial data access, while industry stakeholders are deploying localized sovereign cloud infrastructure across major EU hubs to enable BaaS providers to manage data sovereignty while leveraging scalable computing services. Banking-as-a-service providers are accelerating client onboarding timelines by leveraging cloud-based architectures to automate KYC and account provisioning processes. The European Central Bank has released guidance on outsourcing cloud services to help banks manage risks associated with digital technology and third-party dependency, focusing on strengthening supervisory oversight and operational resilience. Cloud elasticity is no longer just an advantage, but a necessity for the millions of micro-transactions in embedded finance, fueling the next generation of BaaS.

By Enterprise Size Insights

The large enterprises segment held the majority share of 58.7% of the Europe banking as a service market in 2025. The prominence of the large enterprise segment is credited to its strategic imperative to embed financial services into core business models to enhance customer lifetime value and unlock new revenue streams. Global e-commerce platforms, logistics firms, and mobility giants such as Zalando, Bolt, and Klarna deploy BaaS to offer branded payment solutions, instant payout,s and loyalty wallets at scale. These enterprises possess the technical maturity, regulatory bandwidth, and capital to integrate complex BaaS stacks across multiple jurisdictions. Their adoption is further accelerated by the Digital Markets Act, which requires gatekeepers to enable interoperability, prompting large platforms to build financial ecosystems using compliant BaaS rails. Moreover, large enterprises can absorb the upfront costs of custom API development and ongoing compliance monitoring, which smaller firms often cannot justify. Their influence extends beyond usage as they shape BaaS roadmaps through co-development agreements, ensuring features align with global operational needs.

The small and medium enterprises (SMEs) segment is predicted to witness the highest CAGR of 34.7% from 2026 to 2034. The rapid expansion of the SMEs segment is propelled by the democratization of financial infrastructure that allows SMEs to compete with larger players through embedded finance. BaaS providers have responded with low-code platforms and pre-certified modules that reduce integration to days rather than months. For instance, Modulr’s SME dashboard enables online retailers to launch virtual IBANs and automate supplier payouts with no coding required. National development banks are also catalyzing adoption. Additionally, the EU’s SME Strategy emphasizes financial digitization as a competitiveness lever, further incentivizing uptake. The transition to pay-as-you-go BaaS pricing allows small businesses to access enterprise-level financial tools while managing cash flow, fueling rapid, widespread adoption.

By End User Insights

The NBFCs and Fintech Corporations segment was the largest in the Europe banking as a service market by occupying a 63.5% share in 2025 because of its foundational reliance on BaaS to deliver regulated financial services without holding capital-intensive banking licenses. Neobanks, digital lenders, and payment institutions depend on BaaS providers for core functionalities such as current accounts, payment processing, and card issuance, all delivered under the BaaS provider’s regulatory umbrella. Driven by intense regulatory scrutiny and compliance demands, new electronic money institutions in Germany increasingly rely on established Banking-as-a-Service platforms to manage their infrastructure, rather than building it in-house. The model enables fintechs to focus on user experience and niche verticals, such as green banking or gig economy payouts, while outsourcing compliance, liquidity management, and audit readiness. Moreover, the EBA’s proportionality principle allows smaller fintechs to outsource critical functions, provided oversight is maintained, and a regulatory stance that explicitly validates the BaaS model. Supported by a robust European fintech ecosystem, non-bank financial companies and fintech firms continue to drive the growth and evolution of Banking-as-a-Service platforms, accelerating the adoption of embedded finance.

The banks segment is estimated to register the fastest CAGR of 26.9% over the forecast period. Traditionally seen as a BaaS provider,s legacy banks are increasingly becoming BaaS consumers to modernize legacy systems and accelerate digital transformation. Incumbents like ING and BBVA use BaaS APIs to decouple front-end innovation from monolithic core banking systems, enabling rapid launch of niche products such as SME expense cards or carbon offset accounts. The implementation of the European Union's Digital Operational Resilience Act is accelerating the adoption of secure, external cloud-based Banking-as-a-Service (BaaS) modules for key functions like payment processing and identity verification, as financial institutions shift away from maintaining legacy, in-house infrastructure. Furthermore, banks are leveraging BaaS to participate in embedded finance ecosystems, offering their balance sheets through BaaS rails to fintechs in revenue-sharing models. Increasing numbers of mid-sized European financial institutions are integrating external Banking-as-a-Service (BaaS) providers to handle customer onboarding and transaction monitoring, aiming to meet stricter digital resilience requirements. This strategic pivot transforms banks from infrastructure owners to ecosystem partners, accelerating BaaS adoption across the entire financial value chain.

REGIONAL ANALYSIS

United Kingdom Banking as a Service Market Analysis

The United Kingdom was the top performer in the Europe banking as a service market by accounting for a 25.4% share in 2025. Despite Brexit, the country remains the epicenter of BaaS innovation due to its mature regulatory sandbox, early adoption of open banking, and concentration of fintech talent in London, Manchester, and Edinburgh. The Financial Conduct Authority continues to regulate a growing number of fintech enablers, including firms like Modulr and Bankable, facilitating embedded banking services across the UK and international markets. The UK’s Open Banking Implementation Entity established one of the world’s first standardized API frameworks, which became a blueprint for European BaaS interoperability. UK BaaS platforms are experiencing robust growth, powering a significant number of fintechs and serving a large, expanding consumer base. The UK government continues to support fintech infrastructure development following strategic reviews, aimed at strengthening the nation's leadership in embedded finance. The UK maintains its leadership in the European Banking-as-a-Service (BaaS) market by setting technical and compliance standards, driven by deep capital markets, agile regulation, and English language advantages.

Germany Banking as a Service Market Analysis

Germany was the second largest country in the Europe banking as a service market. The growth of the German market is fuelled by its rigorous regulatory environment, high capital requirements, and strong industrial base seeking embedded finance solutions. German Banking-as-a-Service pioneers have obtained full regulatory licenses, enabling them to provide financial infrastructure for numerous digital fintechs and corporate partners across Europe. Germany’s emphasis on data sovereignty and operational resilience aligns with the EU’s Digital Operational Resilience Act, making its BaaS providers preferred partners for risk-conscious enterprises. German BaaS platforms have become crucial to European digital payments, handling a significant portion of total European SEPA transaction volume, according to central bank reporting. The German federal government is investing in the modernization of Mittelstand companies, supporting the adoption of digital finance technologies and embedded banking services. Germany’s blend of regulatory credibility, engineering precision, and industrial demand ensures its position as Europe’s most trusted BaaS hub.

France Banking as a Service Market Analysis

France is also a major player in the Europe banking as a service market due to its proactive regulatory stance and strategic alignment of BaaS with national digital sovereignty goals. ACPR has streamlined licensing for electronic money institutions, reducing approval times for qualified BaaS applicants. Indigenous financial technology firms have established themselves as dominant forces in the European market for small business management and professional financial services. The French government is currently prioritizing a rigorous fiscal agenda centered on narrowing the national budget deficit through targeted corporate tax measures and reduced public spending. Financial institutions and startups are increasingly collaborating to integrate advanced digital infrastructure into various commercial and savings platforms. France’s emphasis on ethical finance, data localization, and public-private collaboration positions it as a laboratory for socially responsible BaaS innovation within the European framework.

Netherlands Banking as a Service Market Analysis

The Netherlands grew steadily in the Europe banking as a service market owing to its role as a logistics and digital gateway to Europe, with Amsterdam hosting major cloud regions for AWS and Microsoft Azure certified for financial services. Dutch BaaS providers like bunq and Mambu leverage this infrastructure to offer low-latency, scalable banking rails compliant with EU data residency rules. The Netherlands Authority for the Financial Markets AFM has established a dedicated innovation hub that fast-tracks BaaS licensing for firms demonstrating strong cybersecurity and consumer protection protocols. The Dutch fintech ecosystem, supported by regulatory flexibility and Banking-as-a-Service (BaaS) providers, has become a key launchpad for pan-European services, offering rapid time-to-market for new financial players. Furthermore, the Port of Rotterdam utilizes digital trade finance and automated payment ecosystems to create tangible, real-world, non-consumer applications. Fintechs are increasingly utilizing Dutch BaaS platforms for rapid expansion across Europe, with regulatory frameworks in the Netherlands supporting quick implementation. Additionally, the Port of Rotterdam is actively applying BaaS technology to modernize and automate trade finance payments, demonstrating practical, B2B utility. The Netherlands' combination of advanced ICT, high English fluency, and flexible regulations makes it the ideal launchpad for expanding BaaS services throughout Northwest Europe.

Sweden Banking as a Service Market Analysis

Sweden is anticipated to expand in the Europe banking as a service market from 2026 to 2034 due to its leadership in sustainable finance and digital public infrastructure. Swedish BaaS enablers like Tink, acquired by Visa but retaining European operations, pioneered open banking APIs now adopted across the EU. Newer players such as Northmill Bank offer BaaS rails integrated with real-time carbon footprint tracking, aligning with Sweden’s net-zero 2045 target. The Swedish government’s “Digital First” policy mandates that all public services be API accessible, creating a culture of interoperability that extends to finance. Moreover, Sweden’s universal BankID system provides seamless, strong authentication that BaaS platforms leverage to reduce onboarding friction. Sweden is pioneering the next generation of value-driven Banking-as-a-Service (BaaS) in Europe, fueled by high trust in digital institutions, robust environmental governance, and agile regulation.

COMPETITION OVERVIEW

Competition in the Europe banking as a service market is intensifying as licensed fintechs, traditional banks, and global technology firms vie to become the preferred infrastructure layer for embedded finance. The market is bifurcated between specialized BaaS enablers like Solaris and Modulr that focus exclusively on API driven banking rails and neobanks such as Qonto that blend direct customer offerings with BaaS capabilities. Regulatory licensing acts as both a barrier and a differentiator, with players holding full banking licenses commanding greater trust and service breadth than e-money institutions. Competition is not based on price alone but on compliance robustness, technical reliability, and the depth of value-added services such as ESG analytics or real-time fraud detection. National regulatory divergence—such as varying outsourcing rules in Germany versus Spain—favors players with multi-jurisdictional licensing and operational agility. Meanwhile, large cloud providers and payment networks are entering the space through partnerships, increasing pressure on pure play BaaS firms to differentiate through domain expertise and developer experience. This dynamic creates a high-stakes race to become the invisible yet indispensable engine of Europe’s financial future.

KEY MARKET PLAYERS

A few major players of the Europe banking as a service market include

- Solaris SE

- ClearBank Ltd

- Banking Circle

- Treezor

- Modulr

- Starling Bank

- Adyen

- Stripe

- Marqeta

- Thought Machine

- Tink

- Yapily

- Mambu

Top Strategies Used by the Key Market Participants

Key players in the Europe banking as a service market are prioritizing regulatory compliance by obtaining national banking or e-money licenses to serve as the legal backbone for non-bank clients. Companies are investing in cloud native core banking platforms to ensure scalability, security, and data residency in line with EU requirements. Strategic partnerships with fintechs, e-commerce firms, and software vendors are being forged to embed financial services directly into non-financial customer journeys. Providers are expanding their API libraries to include value-added services such as sustainability tracking, fraud prevention, and real-time payment initiation. Additionally, firms are launching managed service offerings that handle ongoing compliance, anti-money laundering monitoring, and operational resilience to reduce the regulatory burden on clients and strengthen long term retention in a highly scrutinized financial environment.

Leading Players in the Market

- Solaris SE is a German fintech and licensed bank that serves as a leading Banking as a Service provider across Europe. The company offers a full suite of embedded finance infrastructure, including current accounts, payment processing, card issuing, and lending rails through compliant APIs. Solaris powers numerous clients globally, including Klarna, Vivid Money, and Samsung Pay, enabling them to deliver regulated financial products without holding banking licenses. The company contributes to the global market by exporting its regulatory and technical framework to international partners while maintaining strict adherence to EU standards. It also expanded its cloud native core banking platform to support real-time SEPA and instant payment integrations, strengthening its position as a scalable and compliant BaaS enabler for European and global innovators.

- Modulr Finance Limited is a UK-based BaaS platform authorized by the Financial Conduct Authority and the Central Bank of Ireland, offering programmable payment and account infrastructure. The company serves fintechs, gig economy platforms, and enterprises across Europe by providing API driven access to regulated e-money and payment services. Modulr’s contribution to the global market lies in its robust compliance architecture and seamless integration with UK and EU payment schemes, including Faster Payments, SEPA, and Bacs. These innovations reduce technical barriers for non-financial businesses seeking to embed financial services while reinforcing Modulr’s reputation as a secure and developer-friendly BaaS partner across regulated European markets.

- Qonto SAS is a French neobank and BaaS provider that combines business banking with embedded finance capabilities for SMEs and fintech partners. Licensed as an electronic money institution by the French Prudential Supervision and Resolution Authority, Qonto offers IBAN issuance, card management, expense tracking, and treasury services via APIs. The company strengthens the global BaaS ecosystem by championing a user-centric approach that blends financial functionality with intuitive design, setting new benchmarks for SME banking experiences. It also integrated real-time carbon footprint analytics into transaction data, aligning with EU sustainable finance mandates. Through these initiatives, Qonto not only serves European entrepreneurs but also influences global standards for ethical and accessible embedded finance.

MARKET SEGMENTATION

This research report on the Europe banking as a service market has been segmented and sub-segmented based on component, type, enterprise size, end user, and region.

By Component

- Platform

- Service

- Professional Service

- Managed Service

By Type

- API Based BaaS

- Cloud-Based BaaS

By Enterprise Size

- Large Enterprise

- Small & Medium Enterprise

By End User

- Banks

- NBFC/Fintech Corporations

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the Europe BaaS market?

Key growth drivers include rising fintech adoption, demand for embedded finance, digital transformation of banks, open banking regulations, and increasing use of APIs by non-financial companies.

2. Which countries are leading the Europe BaaS market?

The market is led by the UK, Germany, France, the Netherlands, and Spain due to strong fintech ecosystems, favorable regulations, and high digital banking penetration.

3. What role does regulation play in the Europe BaaS market?

Regulations such as PSD2 and open banking frameworks promote competition, data sharing, and innovation, enabling faster adoption of BaaS solutions across Europe.

4. Who are the major participants in the Europe BaaS ecosystem?

The ecosystem includes licensed banks, fintech platforms, API providers, payment processors, and non-bank enterprises offering embedded financial services.

5. What services are commonly offered under Banking as a Service in Europe?

Common services include digital accounts, payments, card issuing, lending, compliance, KYC/AML, and transaction monitoring.

6. Which industries are adopting BaaS solutions in Europe?

Industries such as e-commerce, retail, travel, telecom, healthcare, real estate, and mobility are actively adopting BaaS to embed financial services.

7. What are the main challenges in the Europe BaaS market?

Key challenges include regulatory compliance complexity, cybersecurity risks, data privacy concerns, integration costs, and dependency on banking partners.

8. How are traditional banks responding to the BaaS trend in Europe?

Traditional banks are partnering with fintechs, developing API platforms, modernizing core banking systems, and launching white-label banking services.

9. What opportunities exist for fintech startups in the Europe BaaS market?

Opportunities include niche financial products, SME banking solutions, vertical-specific embedded finance, and cross-border payment services.

10. What is the future outlook for the Europe Banking as a Service market?

The market is expected to witness strong growth, driven by increasing embedded finance adoption, regulatory support, digital transformation, and expansion into new industries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com