Europe Beverage Container Market Research Report - Segmented By Material( Plastic , Paperboard Containers ) & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis on Size, Share, Trends & Growth Forecast (2025 to 2033)

Europe Beverage Container Market Size

The Europe Beverage Container Market was valued at USD 5.23 billion in 2024. The Europe Generic Drugs Market is expected to have 5.30 % CAGR from 2024 to 2033 and be worth USD 8.32 billion by 2033 from USD 5.51 billion in 2025.

The Europe beverage container market refers to the industry involved in the manufacturing and distribution of packaging solutions for liquid beverages, including plastic bottles, glass bottles, aluminum cans, cartons, and steel containers. These containers are used across a wide range of beverage categories such as carbonated soft drinks, bottled water, juices, energy drinks, alcoholic beverages, and dairy products. The market is shaped by evolving consumer preferences, regulatory pressures toward sustainability, and innovations in packaging materials aimed at extending shelf life and enhancing convenience.

According to the European Environment Agency, beverage packaging accounts for a significant portion of municipal waste, prompting increased scrutiny on recyclability and material sourcing. As a result, companies are shifting toward lightweight and eco-friendly alternatives. Also, the European Commission’s Circular Economy Action Plan emphasizes reducing single-use plastics, influencing manufacturers to explore biodegradable and reusable container options.

Consumer demand for on-the-go consumption formats has also fueled the adoption of portable and durable beverage containers, particularly in urban centers. In countries like Germany and France, deposit return schemes have been instrumental in promoting recycling and reuse practices. Meanwhile, Nordic nations are leading in the adoption of plant-based packaging derived from renewable resources.

MARKET DRIVERS

Increasing Demand for On-the-Go Consumption Formats

One of the primary drivers of the Europe beverage container market is the rising preference for on-the-go consumption among consumers, especially in urban areas. Busy lifestyles, growing urbanization, and changing dietary habits have led to an increase in the consumption of ready-to-drink beverages packaged in convenient, portable containers. In response, beverage producers and packaging manufacturers have prioritized the development of lightweight, shatterproof, and resealable containers. Plastic PET bottles and aluminum cans dominate this segment due to their durability and ease of use. For instance, the UK Soft Drinks Association reported that a significant share of bottled beverages sold in convenience stores come in single-serve sizes tailored for mobile consumption. Similarly, in Spain, vending machine sales have surged notably since 2021, reflecting a broader trend of impulse buying and portability-driven purchasing behavior

Growth of Premium and Functional Beverages

Another significant driver of the Europe beverage container market is the expanding market for premium and functional beverages such as sports drinks, energy drinks, organic juices, and fortified waters. Consumers are increasingly seeking health-conscious and value-added beverage options, necessitating specialized packaging that preserves product integrity while enhancing brand appeal. According to the European Food Safety Authority, per capita consumption of functional beverages has considerably risen annually over the past five years, driven by heightened awareness of wellness and nutrition. Premium beverage brands often rely on distinctive container designs, recyclable materials, and barrier technologies to differentiate themselves in competitive markets. In Germany, the craft beverage sector has seen rapid expansion, with microbreweries and artisanal drink makers opting for aluminum cans and glass bottles to maintain product quality and convey a sense of authenticity. Beverage container manufacturers are responding by investing in advanced filling and sealing technologies that ensure freshness and extend shelf life.

MARKET RESTRAINTS

Regulatory Restrictions on Single-Use Plastics

A major restraint affecting the Europe beverage container market is the tightening regulatory environment surrounding single-use plastics. The European Union has implemented stringent directives aimed at reducing plastic waste, particularly under the Single-Use Plastics Directive, which bans or restricts several disposable items, including certain types of plastic beverage containers. As a result, manufacturers are facing increased pressure to transition to alternative materials such as aluminum, glass, or bio-based polymers, which can be more expensive and logistically complex to produce and distribute. In France, for example, new legislation mandates that all beverage containers must be fully recyclable by 2030, forcing companies to redesign packaging lines and invest in sustainable materials. Similarly, in Italy, local governments have introduced extended producer responsibility (EPR) schemes that require beverage companies to contribute financially to recycling infrastructure

Volatility in Raw Material Prices

Another critical constraint on the Europe beverage container market is the volatility in raw material prices, particularly for aluminum, PET resin, and glass. These materials constitute a substantial portion of production costs, and fluctuations in their availability and pricing directly impact profitability and supply chain stability. PET resin, derived from crude oil and natural gas, has also experienced significant price swings. The International Energy Agency notes that global oil prices surged during the same period, increasing input costs for plastic bottle manufacturers. This volatility makes it difficult for beverage container producers to forecast expenses and maintain consistent pricing strategies. Companies in Germany and the Netherlands have reported delays in securing raw material supplies, leading to production bottlenecks and order backlogs. Smaller manufacturers, in particular, struggle to absorb these fluctuations without passing them on to customers, potentially impacting competitiveness.

MARKET OPPORTUNITIES

Expansion of Sustainable Packaging Solutions

A compelling opportunity emerging in the Europe beverage container market is the rapid expansion of sustainable packaging solutions. As consumer awareness and regulatory pressure intensify regarding environmental issues, beverage companies are actively seeking alternatives to traditional plastic containers. According to the Ellen MacArthur Foundation, over 70 European beverage brands have committed to using 100% recyclable or compostable packaging by 2025, signaling a major shift in industry priorities. Manufacturers are investing heavily in bio-based plastics, post-consumer recycled (PCR) materials, and refillable container systems to meet these sustainability goals. In Sweden, for instance, Tetra Pak launched a fully renewable paper-based bottle prototype designed for long-term scalability in juice and dairy applications. Similarly, Coca-Cola’s PlantBottle initiative, which incorporates plant-based materials, has gained traction across multiple European markets. Deposit return schemes (DRS) in Germany, Norway, and the Netherlands have further incentivized the adoption of recyclable aluminum and glass containers.

Digitalization and Smart Packaging Innovations

Another transformative opportunity for the Europe beverage container market lies in the integration of digitalization and smart packaging technologies. Brands are increasingly leveraging innovations such as QR codes, NFC chips, and intelligent labeling to enhance consumer engagement, track product lifecycle, and improve supply chain transparency. According to McKinsey & Company, a notable share of beverage producers in Western Europe plan to adopt smart packaging solutions within the next three years to optimize marketing strategies and collect real-time consumer data. Companies are exploring interactive labels that provide information on ingredient sourcing, carbon footprint, and expiration tracking through smartphone scans. In Finland, Carlsberg Group introduced a digital label pilot program on select beer cans that connects consumers to augmented reality content and sustainability reports. Meanwhile, Italian dairy giant Parmalat integrated temperature-sensitive inks into its milk cartons to indicate potential spoilage, improving food safety and reducing waste. These advancements not only enhance product traceability but also support circular economy initiatives by encouraging responsible disposal and recycling.

MARKET CHALLENGES

Navigating Diverse Regulatory Frameworks Across Countries

A pressing challenge confronting the Europe beverage container market is the complexity of navigating diverse regulatory frameworks across different countries. While the European Union provides overarching directives on packaging sustainability and food safety, individual member states implement varying national laws, creating compliance hurdles for multinational manufacturers. According to the European Committee for Standardization (CEN), inconsistencies in labeling requirements, recyclability standards, and chemical migration limits complicate large-scale production planning and distribution logistics. For example, France’s Anti-Waste Law mandates specific recycled content thresholds for plastic beverage bottles, whereas Germany enforces strict deposit return system obligations for both plastic and aluminum containers. In contrast, Southern European countries such as Greece and Portugal have yet to fully implement EU-wide packaging regulations, resulting in uneven enforcement and market readiness. Apart from these, some regions impose additional taxes on non-recyclable packaging, influencing material selection strategies. These disparities force companies to maintain multiple product lines tailored to regional specifications, increasing operational costs and time-to-market.

Consumer Shift Toward Refillable and Reusable Containers

Another significant challenge for the Europe beverage container market is the accelerating consumer shift toward refillable and reusable packaging models. Driven by environmental concerns and government-backed initiatives, consumers are increasingly favoring refill stations, bulk dispensers, and returnable bottle systems over single-use containers. According to the European Environmental Bureau, a significant portion of consumers in Germany and the Netherlands now prefer refillable packaging when available, citing reduced plastic waste and lower carbon footprints as key motivators. This shift poses a direct threat to traditional beverage container manufacturers reliant on disposable formats. Retailers such as Carrefour and Waitrose have expanded in-store refill stations for beverages, reducing the demand for single-use plastic and glass bottles. In response, beverage brands and packaging firms are being forced to invest in closed-loop systems, reverse logistics networks, and hygiene-certified cleaning facilities to adapt to the changing landscape. However, setting up these infrastructures requires significant capital expenditure and coordination with municipalities and waste management entities.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.30 % |

| Segments Covered | By Material and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | Ball Corporation (USA), Crown Holdings, Inc. (USA), Ardagh Group S.A. (Luxembourg), Owens-Illinois, Inc. (USA) |

SEGMENT ANALYSIS

By Material Insights

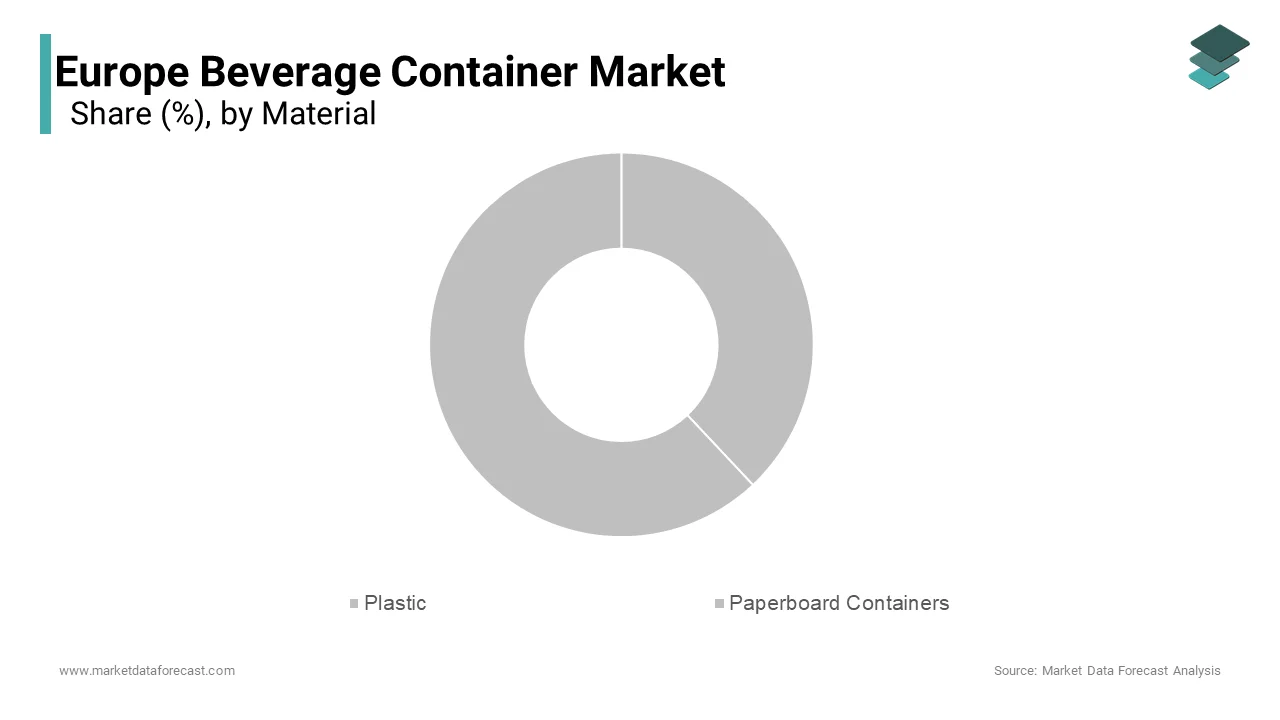

The plastic remained the largest material segment in the Europe beverage container market by capturing a 38.7% of total revenue in 2024. This dominance is primarily attributed to its widespread use in bottled water, carbonated soft drinks, and sports beverages due to its lightweight, durable, and cost-effective properties. According to PlasticsEurope, over 15 million tons of plastic packaging were produced in the EU in 2023, with beverage bottles accounting for nearly one-third of this volume. PET (polyethylene terephthalate) bottles are particularly favored by manufacturers for their shatterproof nature and ease of transportation. In Germany, which operates one of the most efficient deposit return systems in Europe, PET bottle recycling rates reached 98% in 2023, as reported by the German Environment Agency (UBA), making them a preferred option despite regulatory scrutiny.

The paperboard container segment is projected to advance at the fastest CAGR of 6.7% from 2025 to 2033 which is driven by rising demand for sustainable and renewable packaging solutions. As consumer awareness about plastic waste intensifies, beverage brands are increasingly adopting fiber-based cartons made from responsibly sourced wood pulp. According to the European Carton Makers Association (ECMA), carton-based beverage packaging consumption increased between 2021 and 2023, with Scandinavia and the Netherlands leading adoption trends. Major players such as Tetra Pak and Elopak have introduced fully recyclable and compostable cartons with plant-based barrier coatings to replace conventional plastic-lined alternatives. The Nordic Council of Ministers reported that a large share of liquid food and beverage cartons in Sweden and Finland are now collected for recycling, supporting circular economy initiatives. Apart from these, the European Commission’s Packaging and Packaging Waste Regulation encourages the use of renewable materials, further accelerating the shift toward paperboard-based containers.

COUNTRY LEVEL ANALYSIS

Germany commanded the Europe beverage container market contributing a 21.8% of total regional revenues in 2024. This position is attributed to the country’s strong beverage industry, well-established recycling infrastructure, and proactive policies promoting sustainable packaging. The German beverage sector is one of the most dynamic in Europe, with a diverse mix of domestic and international brands driving demand for both plastic and aluminum containers. Moreover, Berlin has been at the forefront of introducing biodegradable and plant-based packaging alternatives, with several startups and research institutions collaborating on next-generation beverage containers. Supported by strict regulatory enforcement and growing consumer awareness, Germany continues to set benchmarks for sustainability and innovation in the beverage packaging landscape.

France beverage container market is driven by strategic regulatory leadership and a strong emphasis on environmental sustainability. According to INSEE, the French national statistics institute, the country spent €8.2 billion on beverage packaging in 2023, with increasing investments directed toward recyclable and reusable formats. France’s Anti-Waste Law for a Circular Economy mandates that all plastic beverage bottles must contain at least 50% recycled content by 2025, pushing manufacturers to adopt greener production methods. Major retailers like Carrefour and Auchan have expanded refill stations and incentivized reusable bottle returns, aligning with national sustainability goals. Also, Paris has become a hub for packaging innovation, with companies such as Carbios pioneering enzymatic plastic recycling technologies.

The United Kingdom focuses on sustainable innovation and is supported by strong investments in sustainable packaging innovation and consumer-driven demand for eco-friendly options. According to the UK Department for Environment, Food & Rural Affairs (DEFRA), a large share of consumers prefer beverages packaged in recyclable or compostable materials, influencing brand strategies and retailer policies. The UK Soft Drinks Association reported that 60% of bottled beverages now feature post-consumer recycled (PCR) plastic content, with major producers aiming for 100% recyclability by 2025. Companies like Coca-Cola European Partners and Britvic have accelerated their transition to lighter-weight bottles and plant-based resins.

Italy holds significant position in the Europe beverage container market which is propelled by expanding deposit return schemes and increasing public-private collaboration on sustainable packaging. According to ISTAT, Italy’s national statistical institute, the country consumed over 12 billion beverage containers in 2023, with a key increase in recyclable packaging adoption compared to the previous year. Conai, Italy’s National Consortium for Packaging Recycling, reported that overall beverage container recycling rates improved within the first year of implementation.

Spain is witnessing a rising demand in eco-friendly packaging, driven by increasing demand for eco-friendly packaging and supportive government policies. Retailers such as Mercadona and Dia have expanded their private-label eco-packaged beverages, responding to consumer preferences for environmentally responsible products. With continued investment in clean packaging technologies and smart distribution models, Spain is solidifying its position in the European beverage container market.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the Europe Beverage Container Market are Ball Corporation (USA), Crown Holdings, Inc. (USA), Ardagh Group S.A. (Luxembourg), Owens-Illinois, Inc. (USA), Tetra Pak International S.A. (Switzerland), Amcor plc (Switzerland), Gerresheimer AG (Germany), Vetropack Holding Ltd. (Switzerland), DS Smith P.

The competition in the Europe beverage container market is highly dynamic, characterized by a mix of multinational corporations, regional manufacturers, and emerging eco-packaging startups vying for market share across multiple material segments. Established players such as Amcor, Tetra Pak, and Ball Corporation dominate due to their extensive production capabilities, innovation pipelines, and deep-rooted relationships with major beverage brands. However, smaller, agile firms are gaining traction by focusing on niche sustainable packaging solutions and digitalized supply chain models.

A defining feature of the competitive landscape is the increasing emphasis on sustainability, with companies striving to meet stringent EU directives and consumer demand for environmentally responsible packaging. This has led to intensified R&D efforts in recyclable, compostable, and refillable container technologies. Additionally, regulatory disparities across European countries pose challenges, requiring firms to adapt packaging strategies regionally.

Brand differentiation is increasingly tied to environmental credentials, prompting players to invest in closed-loop systems, lightweighting, and plant-based materials. As deposit return schemes expand and public awareness grows, the ability to offer cost-effective, high-performance, and eco-friendly beverage containers will determine long-term success in this rapidly evolving market.

Top Players in the Europe Beverage Container Market

Amcor plc

Amcor is a global leader in responsible packaging and holds a significant presence in the Europe beverage container market. The company specializes in flexible and rigid plastic packaging, supplying to major beverage brands across carbonated drinks, bottled water, juices, and dairy products. Amcor is recognized for its commitment to sustainability, actively developing recyclable, reusable, and compostable packaging solutions. Its innovation-driven approach ensures alignment with evolving regulatory standards and consumer expectations regarding environmental impact.

The company plays a crucial role in advancing circular economy principles by collaborating with industry stakeholders and investing in material science research. Amcor’s extensive production network across Europe enables it to deliver high-performance beverage containers while maintaining supply chain efficiency. Through strategic partnerships and product development focused on lightweighting and barrier technology, Amcor continues to shape the future of beverage packaging on both regional and global scales.

Tetra Pak International S.A.

Tetra Pak is a dominant player in the Europe beverage container market, particularly in the liquid food and drink carton segment. The company offers a comprehensive range of aseptic cartons used for packaging milk, juice, plant-based beverages, and still drinks. Tetra Pak is widely known for its long-standing commitment to sustainable packaging, including the use of renewable materials and the development of fully recyclable and biodegradable alternatives.

Its contribution extends beyond product manufacturing, as the company actively engages in promoting recycling infrastructure and consumer education across Europe. Tetra Pak also integrates digital technologies into its packaging solutions, enhancing traceability and brand engagement. With strong footholds in Scandinavia, Germany, and France, Tetra Pak remains a key innovator and market influencer in the beverage container industry, shaping trends in eco-conscious packaging design and functionality.

Ball Corporation

Ball Corporation is a leading manufacturer of metal beverage containers, with a strong presence in the European market. The company supplies aluminum cans to major soft drink, beer, energy drink, and sparkling water producers, capitalizing on the growing shift toward recyclable and infinitely reusable packaging formats. Ball’s operations in Europe reflect its dedication to reducing carbon emissions and supporting the circular economy through advanced can recycling initiatives.

The company has been instrumental in driving the transition away from single-use plastics, leveraging its scalable production capabilities and investment in lightweight can technology. Ball also emphasizes sustainability through investments in clean manufacturing processes and closed-loop systems that minimize waste and energy consumption. With increasing demand for aluminum-based beverage containers due to their environmental benefits, Ball continues to expand its influence across Europe, reinforcing its position as a global leader in sustainable beverage packaging.

Top strategies used by the key market participants

One major strategy employed by leading players in the Europe beverage container market is sustainable material innovation , where companies focus on developing recyclable, biodegradable, and reusable packaging solutions to align with tightening environmental regulations and shifting consumer preferences. This includes the adoption of bio-based polymers, post-consumer recycled (PCR) content, and alternative fiber-based containers.

Another key strategy is strategic partnerships and collaborations , particularly with raw material suppliers, recycling organizations, and beverage brands to enhance the value chain’s sustainability and efficiency. These alliances help firms access new technologies, improve recycling infrastructure, and co-develop next-generation packaging formats tailored to specific market needs.

Lastly, market expansion through localized production facilities allows companies to reduce transportation emissions, comply with regional regulations, and respond more swiftly to changing customer demands. By establishing manufacturing hubs closer to end markets, leading players enhance supply chain resilience and reinforce their competitive positioning across diverse Europe

RECENT HAPPENINGS IN THE MARKET

In January 2024, Amcor launched a new line of 100% recyclable mono-material stand-up pouches for premium juice and smoothie brands in Western Europe, aiming to replace multi-layered non-recyclable alternatives and support circular packaging goals.

In March 2024, Tetra Pak partnered with a Finnish forestry group to develop a fully renewable and compostable beverage carton made from sustainably sourced wood fibers, targeting the Nordic and German markets where consumer demand for green packaging is strongest.

In June 2024, Ball Corporation expanded its aluminum can production facility in Poland, increasing capacity to meet rising demand from Eastern European beverage producers transitioning away from plastic bottles to more sustainable packaging formats.

In August 2024, Crown Holdings introduced an ultra-lightweight two-piece aluminum can in Italy, designed to reduce material usage by 15% without compromising structural integrity, aligning with the country’s anti-waste packaging legislation.

In November 2024, DS Smith, a leading paperboard packaging firm, acquired a French startup specializing in biodegradable barrier coatings for beverage cartons, enhancing its portfolio of sustainable liquid packaging solutions for dairy and plant-based drink producers across Europe.

MARKET SEGMENTATION

This research report on the europe beverage container market has been segmented and sub-segmented into the following categories.

By Material

- Plastic

- Paperboard Containers

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe.

Frequently Asked Questions

What types of beverage containers are most popular in Europe?

The most common types include glass bottles, aluminum cans, PET plastic bottles, cartons, and pouches. Glass and aluminum are favored for premium beverages, while PET is popular for mass-market products due to its lightweight nature.

How important is sustainability in the European beverage container market?

Sustainability is a top priority, with strong consumer demand for recyclable, reusable, and compostable containers. The EU's Circular Economy Action Plan and Single-Use Plastics Directive are major drivers of this trend.

Which countries in Europe have the largest beverage container markets?

Germany, the United Kingdom, France, Italy, and Spain are the largest markets, driven by high consumption rates and strong manufacturing bases.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com